JPT - JPI: Highlighting Misconceptions About This 7.9%-Yielding Preferreds Term CEF

Summary

- Preferreds closed-end funds continue to hold appeal for income investors due to their relatively high credit quality, modest duration, and high yields.

- Term CEFs add another attractive feature due to the potential anchoring of the discount on the expected termination date of the fund as well as a return tailwind.

- Nuveen Preferred & Income Term Fund is a term preferred CEF and shares attractive features of both types of securities.

- The fund came up on the service, and we discuss a number of misconceptions about it.

- JPI trades at a 4% discount and 7.9% yield and remains a holding in our Income Portfolios.

This article was first released to Systematic Income subscribers and free trials on Dec. 24 .

Preferreds closed-end funds ("CEFs") remain key components of many income portfolios. This is due to their appealing combination of relatively high-quality holdings, modest duration, and attractive yields. In addition, term CEFs have an important advantage over typical CEFs due to the expected termination date, which not only anchors the discount but also provides a potential performance tailwind due to discount compression into the termination date.

The Nuveen Preferred & Income Term Fund ( JPI ) is a term preferred CEF that combines the two aspects highlighted above. In this article, we discuss a number of misconceptions related to the fund which came up on our service. JPI remains a holding in our Income Portfolios.

Misconceptions Relating To JPI

Nuveen Preferred & Income Term Fund recently came up on the service as subscribers asked us to respond to an unfavorable third-party commentary. In this section, we highlight some of these key misconceptions and why they are unfounded. Ultimately, income investors are best served when they get a fuller picture of the risk/reward on offer.

The main misconception is that JPI does not protect investors from rising interest rates because it is a term CEF rather than a target term CEF. And although this seems like a benign statement, it is built on a couple of layers of misunderstanding which are worth fleshing out to provide investors the full picture. Below, we discuss various elements of this larger misconception.

"JPI investors are not protected from interest rates climbing between now and when the CEF is scheduled to close because JPI is not a Target-term CEF"

This statement is entirely correct but it also contains very little informational content. For a bit of background, JPI, as a term CEF, has an expected termination date in August of 2024. CEFs can always propose to cancel the termination, push it out, or convert to a perpetual fund, so having a termination date by itself is not a guarantee that the fund will cease to exist.

That said, Nuveen has generally been good about either terminating its term CEFs or allowing investors to exit at the NAV via a tender offer, delivering on the very premise of term CEFs. A sister fund, Nuveen Preferred and Income 2022 Term Fund ( JPT ), was a preferreds term CEF with an expected termination date in 2022. However, it ended up being converted into a perpetual CEF after holding a tender offer at NAV. In other words, we don't know whether JPI will terminate or not, but most likely it will follow in the footsteps of JPT and convert into a perpetual fund after holding a tender offer. This will allow investors to sell their holdings at the NAV, monetizing a 4% discount compression or a 2% additional annual return.

An additional piece of background here is that there are two types of term CEFs: target-term CEFs and plain-vanilla term CEFs. Target-term CEFs have a NAV target which they set out to deliver (few actually succeed). The way they do this is by matching the termination date with the maturity of its assets, so a target-term CEF launching today with a termination date in 10 years would typically buy assets with 10-year maturities. The idea is that if all of its assets mature and pay back their principal, the fund should be able to return its original NAV to investors.

Let's come back to the original statement above that JPI does not protect investors from a rise in rates until its termination date in August 2024. Although on the face of it this is an innocuous statement, it is actually very odd on a couple of different levels.

First, it's not at all clear why investors need to approach CEF allocation with a strict rule of not taking any interest rate risk beyond August 2024. Avoiding any interest rate risk is not only very difficult but also undesirable in our view. For instance, as many investors discovered this year, more sectors are exposed to interest rate risk than it may seem, including bank loans, business development companies ("BDCs"), nearly all equity sectors, and more which have fallen by double-digit amounts despite not being mechanically exposed to changes in interest rates as bonds are.

A rising interest rate environment does not only push down the prices of bonds, but it can also push down prices of many unrelated sectors due to a broader withdrawal of liquidity and tightening of financial conditions.

Moreover, having long-duration exposure can be beneficial for investors in case of a macro downturn. These tend to be accompanied by falling interest rates, supporting the prices of longer-duration assets. The sharp rise in interest rates this year creates a much more balanced risk profile for interest rates over the next few years. In other words, yes interest rates could rise, but they could as easily fall, just like they have already fallen from their peak earlier this year with the 10Y Treasury yield moving lower by around 0.5%, driving up the prices of medium-duration assets that JPI, among other funds, holds.

And two, an investor who looks at a preferred CEF with a 2024 termination date would be making a gross mistake thinking that it somehow protects them from interest rate rises up to the termination date. Warning investors that JPI doesn't protect investors against interest rate risk is sort of like issuing a stern warning to investors that MLPs don't protect against downside in energy prices or that REITs don't protect against cyclical downturns. Well, duh.

As most investors in preferred shares understand perfectly well, nearly all preferreds have no contractual maturity. They can be redeemed by the issuer at a certain point, but this is something that the issuer will do only if it makes economic sense to them, not because they have to. In other words, investors who look at a preferred term CEF with a 2024 termination date and somehow think that the fund's assets mature before 2024 would be betraying a total lack of understanding of what preferreds are as an asset class.

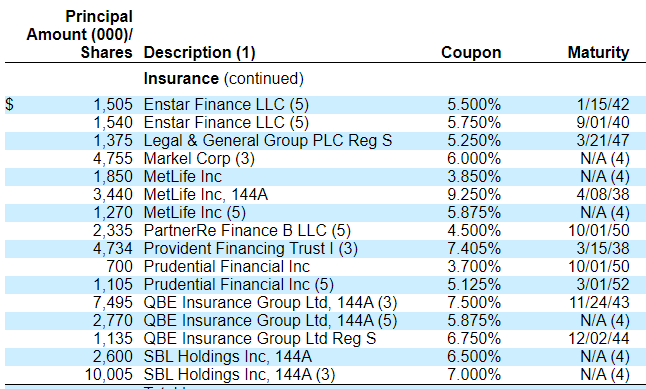

"JPI assets have either very long maturities or are perpetual, creating a high level of interest rate risk"

An extract of the fund's holdings in the insurance sector confirms that it either holds perpetual (shown as N/A (4)) or securities with very long-dated maturities.

{kind=link}

However, it's important to make a distinction between long maturities and interest rate risk. The key point is that most of the fund's holdings are Fix/Float securities, i.e., those that start off with a fixed coupon and then switch to a floating-rate coupon, unless redeemed. The initial fixed-rate period is typically set at 5 years.

What this also means is that the closer these securities are to their first call date, the less sensitive they become to changes in longer-term interest rates. In other words, a security with a maturity of 2042 should not be viewed as a 20-year bond, something that would have enormous price sensitivity to changes in rates (roughly 15% for a 1% change in interest rates).

However, this is far from the case for most of the fund's securities which float in a few years and hence whose duration exposure is closer to 2-3% for a 1% change in longer-term interest rates. The fund has half its assets in institutional preferreds, nearly all of which are Fix/Float, and the rest in CoCos and retail preferreds, many of which are also Fix/Float. In short, don't look at preferreds maturities in gauging interest rate risk.

"JPI holds two interest rate swaps with a market value of around 1% of total assets, maturing in 2024, which does not provide much interest rate protection."

What we really appreciate in these misconception articles is when there are multiple misconceptions packed into a single statement and this is a very good example of it because there are 3.

First, we can't look at the impact of derivative instruments like interest rate swaps based on their market value. That's because there is no relationship between their market value and the amount of financial exposure they carry. This is not very intuitive, since investors are much more familiar with cash instruments such as stocks and bonds where, in nearly all cases, there is a direct relationship between their exposure and their market value. For instance, if I hold a $10k position in specific Treasury bonds, that's 10x as much interest rate exposure as a $1k position in the same bond.

However, derivatives don't work this way. Typically, derivatives such as interest rate swaps have a market value of around zero when they are initiated, regardless of the amount of exposure they carry. That's because a swap is an exchange of two types of cash flows, fixed-rate cash flows versus floating-rate cash flows. And when the swap is initiated, the trade is done on a fair-value basis (ignoring the commission) so that its market value comes out not far from zero. Therefore, the market value of any given swap is not going to tell you what its exposure is.

What we need to do instead is look to the notional amount of the swap. JPI has two swaps with a total notional of $157m, which is about 20% of the fund's total assets - not an insignificant amount. The swap is a receive-floating/pay-fixed swap which offsets the mostly fixed-rate cash flows the fund receives.

The second misconception element here is that we shouldn't focus on the swaps to give us a good idea of the fund's interest rate exposure. That's because it's not going to give us a full picture of the fund's interest rate profile. We would also have to know the proportion of the fund's fixed-rate vs. floating-rate holdings, the percentage of its fixed-rate holdings that convert to floating-rate cash flows later on (i.e., so-called Fix/Float preferreds which is the default profile of institutional preferreds), the fund's liability interest-rate profile and more.

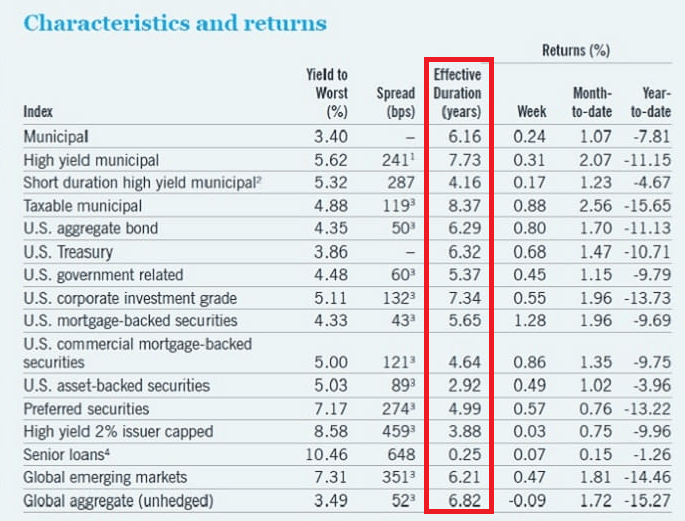

However, rather than wading through all this information, the fund actually makes it very simple for us to get a sense of its interest rate exposure by providing a duration metric on its website, and that number is 3.12. In other words, the fund behaves like a bond with a maturity of roughly around 3.5 years (duration tends to be slightly lower than the maturity of the bond).

How does this compare in the broader income market? The table below, also from Nuveen, captures the duration profile of the popular income sectors. What we see is that the only income sector with a decisively lower duration is bank loans (ABS comes close with a duration of 2.9). In other words, JPI offers investors one of the lowest interest rate exposures in the broader income space. For the geeks in the audience, we should also consider convexity, which describes how duration changes with respect to interest rates, a very useful metric for callable securities like preferreds. It will suffice to say that, because most preferreds are trading well below "par," duration is just about as long as it's going to get so. Unlike in 2021, investors don't need to worry a whole lot about the duration increasing with rising rates.

{kind=link}

The third misconception element in the statement above is that there are different kinds of interest rate exposure that investors need to worry about. The most obvious one is how prices react to changes in longer-term interest rates (which is described by the duration metric). But in the context of leveraged CEFs, we should also consider how changes in short-term interest rates impact the fund's income.

And here is where these low interest rate swaps shine.

The fund has $281m of total borrowings (through a credit facility and a repo). JPI pays OBFR (pretty close to the more familiar SOFR and not far from 1-Month Libor) + 0.85% on the credit facility and OBFR + 0.80% on its smaller repo. On its $157m of swap, JPI receives 1-Month Libor and pays around 2%.

In other words, we can collapse the fund's borrowings (where it pays around OBFR + 0.84% on average) and swaps (where it receives 1-Month Libor). On $157m of its borrowings or about 56%, the fund pays around 2.8% fixed (the sum of: receives 1 Month Libor/pays 2% on the swaps and pays OBFR + 0.84% on the borrowings). On the rest of its $124m of borrowings the fund carries on paying around OBFR + 0.84% which is around 5.15% at today's rates and will rise at least another 0.5% or so over the coming months as the Fed completes its hiking cycle.

In summary, on more than half of its borrowings, the JPI fund pays around 1% less than what the U.S. government pays on its 5Y Treasury bonds and around 2.4% less than what most other leveraged CEFs pay on their borrowings. This is because few other leveraged CEFs bother using interest rate swaps to hedge their interest rate exposure. This provides a significant increase in the amount of additional income the fund can pass on to its investors and is a fantastic benefit for shareholders.

Takeaways

Nuveen Preferred & Income Term Fund remains a very attractive fund in our view due to its combination of relatively high-quality securities (70% in investment-grade securities), modest duration of just over 3, and attractive 7.9% yield (with 101% coverage). Moreover, the fund's term structure (as well as Nuveen's strong track record in providing investors an exit at the NAV around the termination date) means there is a likely additional 2% annual return tailwind into its late-2024 expected termination date, creating a close to 10% total yield. Finally, because the fund hedges more than half of its leverage facility, it enjoys an unusually low cost of leverage relative to the broader credit CEF space, allowing it to pass on more of its generated income to investors. JPI remains in our Income Portfolios.

For further details see:

JPI: Highlighting Misconceptions About This 7.9%-Yielding Preferreds Term CEF