VNO - JRI: Real Assets Can Protect Against Inflation But Watch The NAV Closely

Summary

- Real assets share many of the same qualities as other things that increase in price during inflation so they can help protect your wealth in that environment.

- JRI invests in a portfolio of infrastructure and real estate to provide investors with a high level of current income.

- The majority of the companies in the fund's portfolio enjoy stable cash flows and are recession-resistant.

- The fund failed to cover its distributions over the first half of 2022, although just barely.

- The fund is currently trading at an incredibly attractive discount to NAV.

One of the biggest problems facing many Americans today is the incredibly high rate of inflation that has been permeating our economy. This inflation is so bad that it has forced 63% of Americans to live paycheck-to-paycheck. As such, many investors may be seeking ways to protect their wealth against the loss of purchasing power that has resulted from this inflation. One of the best ways to do that is to invest in real assets because these assets have many of the same characteristics that other things that appreciate in value during such an environment do so should hold their value fairly well in an inflationary environment. Unfortunately, it can sometimes be difficult to purchase such assets. There are, however, a few ways that we can add these assets and generate income at the same time. One of the best of these methods is to purchase shares of a closed-end fund that focuses on the sector. These funds provide an easy way to access a portfolio of companies that own real assets. In most cases, these professionally-managed funds can also provide a yield that is higher than pretty much anything else in the market. In this article, we will discuss the Nuveen Real Asset Income and Growth Fund ( JRI ), which is one such fund in this category. This fund certainly delivers a market-beating yield as its shares boast a 9.92% yield as of the time of writing. I have discussed this fund before but more than a year has passed since that time so obviously, a great many things have changed. This article will therefore focus specifically on those changes as well as provide an updated analysis of the fund’s finances.

About The Fund

According to the fund’s webpage , the Nuveen Real Asset Income and Growth Fund has the stated objective of providing a high level of income and capital appreciation. This is certainly not unusual for an equity fund as equities are by their very nature total return instruments. After all, equity investors are typically looking for both income and capital gains when they purchase stock in a company. This fund may be able to do better on the income front than many other equity funds, however. This is because companies that own real assets tend to have higher dividend yields than other companies. The term “real assets” is admittedly broad but it generally refers to companies that own tangible and irreplaceable assets that earn them money. The fund itself defines these as infrastructure companies and real estate investment trusts. I would likely also include natural resources and traditional energy companies in this category, but the fund does not actually invest in these.

As just hinted at, one of the best things about real estate investment trusts and infrastructure companies is that they tend to have fairly high yields. This is because both types of companies tend to be fairly slow growth. As such, they pay out a significant proportion of their cash flows to investors. The fact that they tend to have fairly low growth rates means that they typically do not have the high valuation multiples that companies in many other industries possess. These two factors combined result in stocks issued by these companies having fairly high yields. This is something that should appeal to investors that are looking to protect their wealth and generate a high level of income at the same time. The fact that owning these companies can help increase an investor’s income is also nice at overcoming the higher expenses that we all face in our daily lives due to inflation.

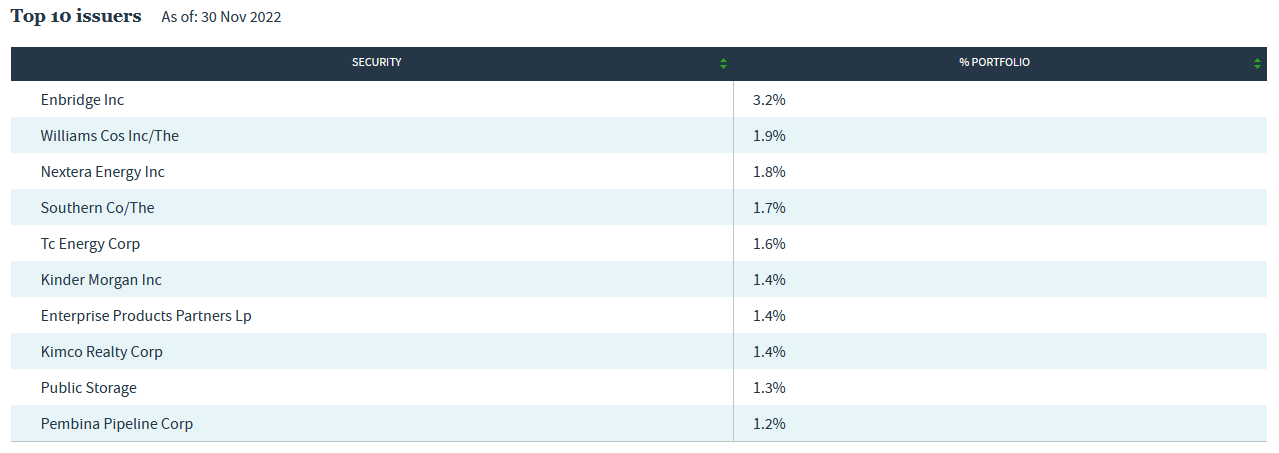

As my regular readers are no doubt well aware, I have devoted a significant amount of time and effort to discussing infrastructure companies here at Seeking Alpha over the past ten years. I have also discussed real estate investment trusts, although certainly not to the same degree. As such, the majority of the largest positions in the fund will likely be familiar to most readers. Here they are:

{kind=link}

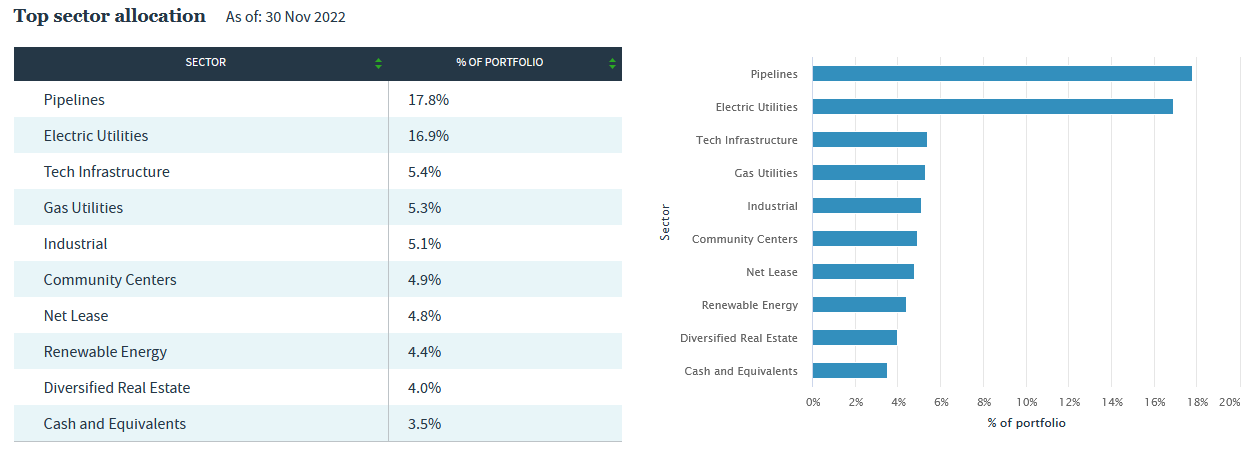

I have discussed many of these companies in-depth on this site for many years. Regular readers should be quite familiar with Enbridge ( ENB ), The Williams Companies ( WMB ), TC Energy ( TRP ), Kinder Morgan ( KMI ), Enterprise Products Partners ( EPD ), and Pembina Pipeline ( PBA ). These are all among the largest natural gas and crude oil pipeline operators in North America. In addition, many of them have significant growth prospects over the next several years due to the growing demand for natural gas. I discussed this potential in great detail in a recent article that I published to Energy Profits in Dividends. We do not only see pipeline operators here, though. We also see electric utilities in the form of both NextEra Energy ( NEE ) and The Southern Company ( SO ) along with real estate companies such as Kimco Realty ( KIM ) and Public Storage ( PSA ). With that said though, we can see that the pipeline companies dominate the largest positions in the portfolio, which is also true if we look at the whole portfolio:

{kind=link}

With that said though, the portfolio’s weighting towards pipeline companies is not as large as might be expected when we look solely at the top ten issuers. In fact, electric utilities comprise almost as large of a position. This is actually quite nice when we consider some of the characteristics of both of these companies. In particular, pipeline operators and electric utilities tend to have remarkably stable cash flows regardless of conditions in the broader economy. I explain the reasons for this in numerous previous articles and will not waste space by providing a very detailed explanation here. In short, pipeline operators conduct their business under long-term contracts that include volume-based compensation and minimum volume commitments. Electric utilities provide a service that is generally considered a necessity for modern life so people usually prioritize paying their utility bills ahead of discretionary expenses. This fact about electric utilities is very attractive when we consider how many people are living paycheck-to-paycheck right now and the likelihood of the economy entering into a recession in the near future. This characteristic of stable cash flows is not exclusive to these companies either as many real estate investment trusts also enjoy it. This is mostly because of the long-term nature of the leases that real estate companies have with their tenants. However, some real estate investment trusts, such as the owners of retail real estate, are somewhat more vulnerable to recessions than pipeline operators or electric utilities. Overall, though, the fund’s portfolio looks very good for conservative risk-averse investors considering today’s economic climate and it should prove to be resistant to a near-term recession.

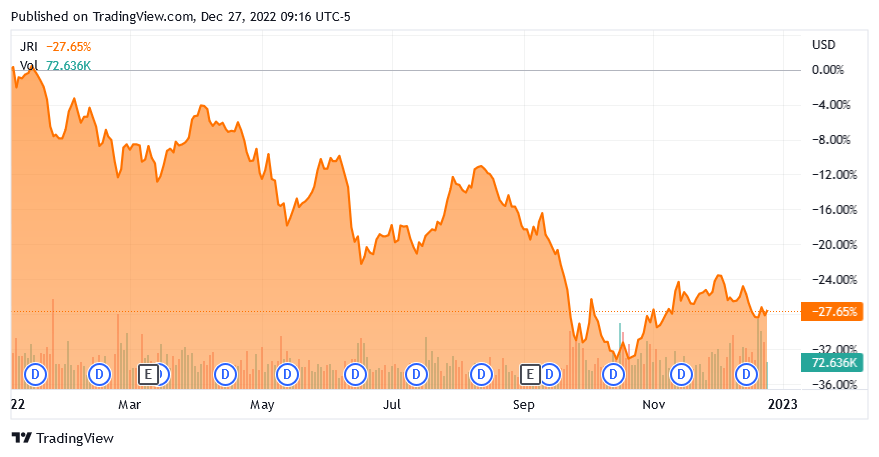

There have been a number of changes since we last looked at the fund. In particular, Vornado Realty ( VNO ), SSE plc ( SSEZF ), Dominion Energy ( D ), Simon Property Group ( SPG ), and Emera ( EMRAF ) were replaced by TC Energy, Kinder Morgan, Kimco Realty, Public Storage, and Pembina Pipeline. This may lead one to think that the fund has a relatively high turnover but this is not necessarily the case. The fact that several of the new additions to the largest positions list are pipeline operators is telling. The energy sector has been by far the best-performing sector in the market over the past year so this might be a case of these companies outperforming the ones that are no longer on the list. With that said though, the fund does have a 73.00% annual turnover, which is somewhat on the high side. The reason that this is important is that trading stocks or other assets costs money, which is ultimately billed to the shareholders. This creates a drag on the portfolio’s performance since management must generate sufficient returns to both cover these added expenses and still deliver a return that satisfies the investors. This is a very difficult task to accomplish and it is one of the reasons why few actively-managed funds manage to outperform their corresponding benchmark indices. This one has not had the best performance as the Nuveen Real Asset Income and Growth Fund is down 27.65% year-to-date:

{kind=link}

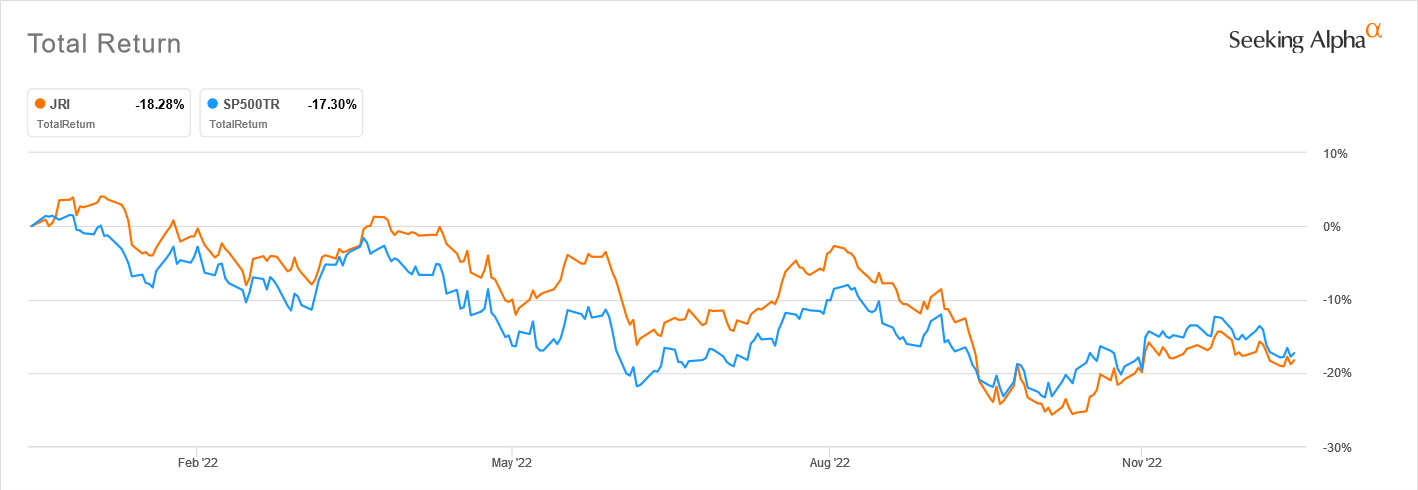

With that said though, when you consider the total return, this fund has not done too badly. Its total return over the past twelve months is –18.28% versus –17.30% for the S&P 500 Index ( SP500 ):

{kind=link}

The S&P 500 Index is far from a perfect comparison though since the index is very heavily weighted towards companies that the fund will never invest in. This fund has significantly outperformed the real estate indices over the same period, primarily because both the energy and utility exposure outperformed both real estate and the S&P 500 over the period. Overall, though, we can see that this fund is holding up pretty well in the current environment.

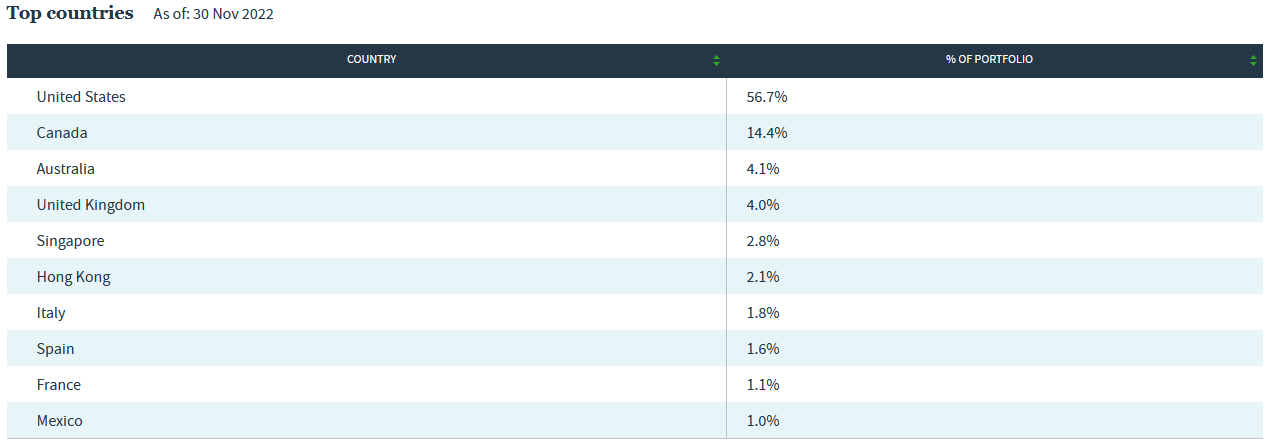

A look at the largest positions in the fund will immediately lead one to think that the Nuveen Real Asset Income and Growth Fund is exclusively an American fund. In fact, we only see two companies on the largest positions list (Enbridge and Pembina Pipeline) that are not American companies. However, a look at the entire portfolio reveals that it is much more diversified internationally. We can see this here:

{kind=link}

As we can see, fully 43.3% of the portfolio is invested outside of the United States. This is something that is quite nice to see because of the protection that it provides us against regime risk. Regime risk is the risk that some government or other authority will take some action that proves to have an adverse impact on a company in our portfolios. The only real way to protect ourselves against this risk is by ensuring that only a relatively small proportion of our assets is exposed to any given country. This fund is doing that much more effectively than might be expected, although its exposure to the United States is more than the country’s actual representation in the global economy. That is not exactly unexpected for a fund that is invested in pipeline operators, utility companies, and real estate investment trusts as many of these companies are rare to find outside of the United States. The fund seems to be doing as good a job as it can at international diversification given the situation, which is overall quite nice to see.

Real Assets As Protection Against Inflation

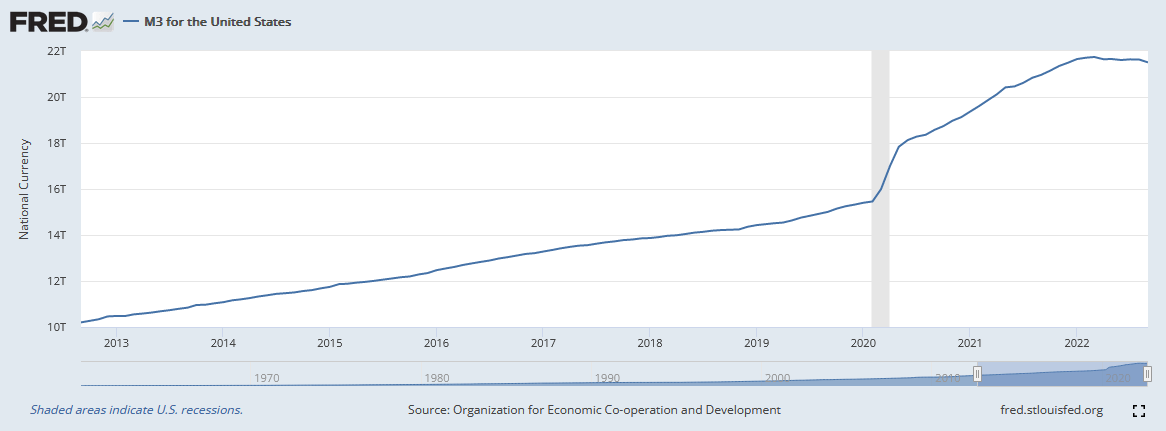

As stated in the introduction, real assets can help protect your wealth against the ravages of inflation. In order to understand why this would be true, it is important to understand the causes of inflation. Economists generally state that inflation is a naturally occurring phenomenon but this is not exactly correct. In fact, inflation is caused by the growth of the money supply exceeding the actual production of goods and services in the economy. This is because such a situation results in a growing number of currency units attempting to purchase each unit of actual production. This has been the case in the United States over the past decade. We can see this by comparing the money supply of the United States to the country’s gross domestic product.

The best measurement to use to evaluate the money supply is M3. While it is true that the Federal Reserve uses M2, M3 is M2 plus institutional time deposits over $100,000. While these time deposits are not as liquid as cash or regular money market funds, they still represent money that can enter the economy pretty quickly if needed. Thus, this is a better metric to use for our purposes than M2. As of September 2022 (the most current date for which data is currently available), the M3 money supply of the United States is $21.5034 trillion. In September 2012, it was $10.2008 trillion:

{kind=link}

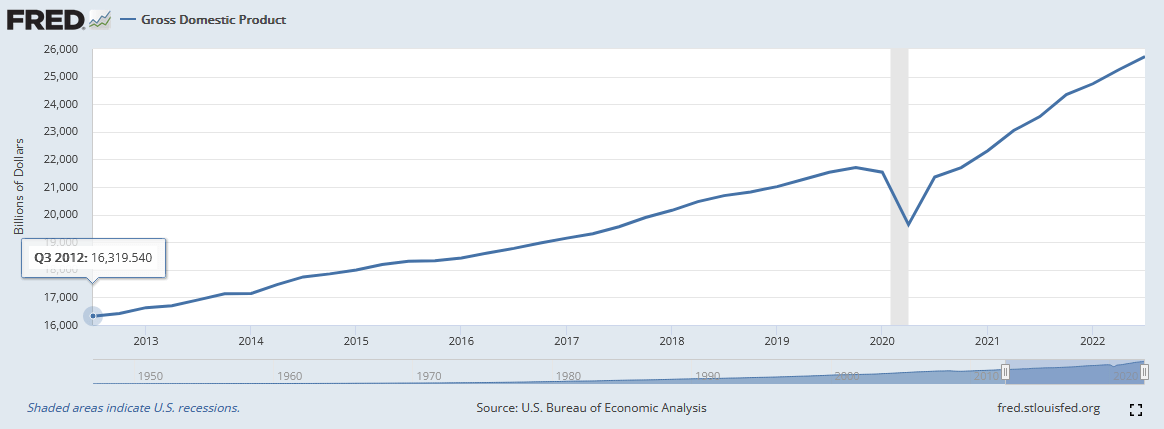

This represents a 110.80% increase over the period. This is substantially more than the gross domestic product growth over the same period:

{kind=link}

The Q3 2022 gross domestic product was $25.723941 trillion. In Q3 2012, it was $16.319540 trillion. This is a 57.47% increase over the same period. Thus, the money supply has grown nearly twice as fast as the economy’s actual production. This is the root cause of the inflation that we are seeing today.

Real assets share the same characteristics as many of the same things that increase in price during an inflationary environment. The most notable of these characteristics is that all of these things can only be created by an actual human or mechanical effort. Unlike fiat money, we cannot create a pipeline, building, or electric grid by simply pushing a button on a computer. Thus, there will always be a limited supply of these assets as there is only a limited number of raw resources, machines, workers, and similar things to create them. As such, these things should increase in price along with everything else during inflationary periods. We have certainly seen this with steel and labor costs over the past year, which has made it much more expensive to construct a pipeline and made existing pipelines that much more precious. The same is true of real estate despite the fact that we have seen the shares of real estate investment trusts decline over the past year. The reason for this is that rising interest rates have caused mortgages to become less affordable so desperate sellers are forced to unload their properties at fire sale prices. This has done nothing to actually change the intrinsic value of the real estate. As real assets should hold their value pretty well, so should the companies that own these companies. As we have already discussed, the companies that the fund invests in are also generally recession-resistant. Thus, this fund should prove to be a reasonably good holding for the current environment.

Distribution Analysis

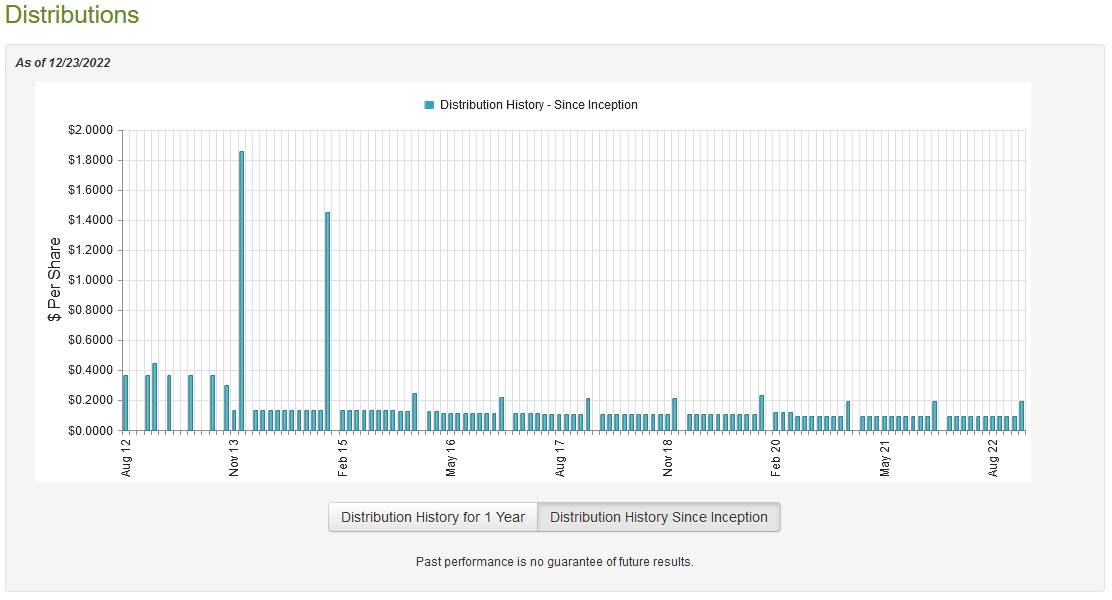

As stated earlier in this article, the primary objectives of the Nuveen Real Asset Income and Growth Fund are to deliver a high level of current income and capital appreciation. In order to accomplish this, the fund invests in infrastructure and real estate investment trusts, both of which tend to possess fairly high yields. This provides the fund with a high level of income that it will be paying out to its investors. In addition to this, the fund will generally pay out much of its capital gains. As such, we can assume that this fund will have a reasonably high distribution yield. This is certainly the case as the fund pays out a monthly distribution of $0.0965 per share ($1.1568 per share annually), which gives the fund a 9.92% yield at the current share price. Unfortunately, the fund has not been particularly consistent about its distribution over its history as it has steadily declined since its inception. However, the fund has maintained its current distribution since 2020:

{kind=link}

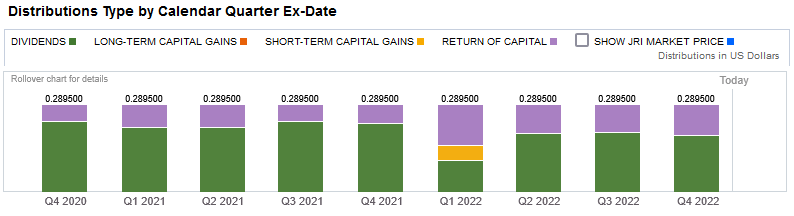

The fund most recently cut its distribution in 2020, which is not exactly surprising. In fact, most infrastructure and midstream funds cut their distributions around the same time. This was due to the uncertainty in the energy sector when resource prices collapsed along with demand following the institution of the COVID-19 lockdowns. Although most midstream companies were able to maintain their cash flows just fine, some of them still cut their distributions in order to strengthen their balance sheets and reduce their need for capital markets. The fact that the fund’s distribution has steadily declined over time might still be disappointing to those investors that are seeking a stable and secure source of income with which to pay their bills, though. More conservative investors might also be concerned that the fund pays out quite a lot of return of capital distributions:

{kind=link}

The reason that this may be concerning is that a return of capital distribution can be a sign that the fund is returning the investors’ own money back to them. This is obviously not sustainable over any sort of extended period. However, there are other things that can cause a distribution to be classified as a return of capital. One of these things is the distribution of money received from master limited partnerships, which is a business structure that encompasses many energy infrastructure companies. The distribution of unrealized capital gains is something else that could result in a return of capital distribution. As these are both things that this fund might be doing, it is important that we analyze the fund’s finances in order to determine exactly how it is paying for its distributions and how sustainable they are likely to be.

Fortunately, we do have a relatively recent document to consult for this purpose. The fund’s most recent financial report corresponds to the six-month period ending June 30, 2022. Although this report will not include any information about the fund’s performance over the past few months, the first half of the year was an interesting time for the markets as it saw both the beginning of the Federal Reserve’s monetary tightening policy and the invasion of Ukraine, which caused energy prices to become rather volatile. Although midstream companies are not directly affected by energy prices, their equity prices certainly are. This report should give us some good insight into how well the fund handled these things. It is also a much newer report than what we had available the last time that we reviewed the fund so it is certainly worth looking at. During the six-month period, the Nuveen Real Asset Income and Growth Fund received a total of $13,529,039 in dividends and $4,411,256 in interest from the investments in its portfolio. After we net out the money that the fund paid in foreign withholding taxes, it had a total income of $17,227,086 during the half-year period. The fund paid its expenses out of this amount, leaving it with $12,538,935 available for investors. This was not enough to cover the $15,895,680 that the fund paid out in distributions, although it got much closer than I expected. Still, this is something that may be concerning at first glance.

The fund does have other ways to obtain the money that it needs to cover the distributions, however. One of these methods is through capital gains. As might be expected from the strong performance of energy infrastructure companies during the first half of the year, the fund had some success at this during the period. It achieved net realized gains of $2,921,818 during the period but this was more than offset by $75,815,030 net unrealized losses. Overall, the fund’s assets declined by $76,249,957 during the half-year period after accounting for all inflows and outflows. Overall, the fund did fail to cover its distribution since even the net investment income and net realized capital gains are not sufficient to cover it, although the fund did get very close. It may have to cut the distribution if things do not improve in the market, particularly for the real estate companies in the portfolio. We should keep an eye on the fund’s asset base to ensure that its net asset value does not decline too much going forward. It might be okay for the time being, though.

Valuation

It is always critical that we do not overpay for any asset in our portfolios. This is because overpaying for any asset is a surefire way to generate a suboptimal return on that asset. In the case of a closed-end fund like the Nuveen Real Asset Income and Growth Fund, the usual way to value it is by looking at the fund’s net asset value. The net asset value of a fund is the total current market value of all of the fund’s assets minus any outstanding debt. It is therefore the amount that the shareholders would receive if the fund were immediately shut down and liquidated.

Ideally, we want to purchase shares of a fund when we can acquire them at a price that is less than the net asset value. This is because such a scenario implies that we are buying the fund’s assets for less than they are actually worth. That is fortunately the case with this fund today. As of December 23, 2022 (the most recent date for which data is currently available), the fund had a net asset value of $13.62 per share but only trades for $11.77 per share. This gives the fund’s shares a discount of 13.58% at the current price. This is quite a bit better than the 12.53% discount that the fund’s shares have averaged over the past month and it is a very nice discount in general. Overall, the price certainly looks right here.

Conclusion

In conclusion, real assets can work pretty well as a way to protect your wealth against the ravages of inflation over the long term. The Nuveen Real Asset Income and Growth Fund provides a good way to add these assets to your portfolio and generate a high yield at the same time. This is something that is undoubtedly going to appeal to more conservative investors. Unfortunately, the fund did fail to cover its distribution during the most recent period, although only barely. Still, we do want to keep an eye on the fund’s net asset value to ensure that it remains reasonably stable. The price is incredibly attractive right now so it might be worth taking a position in all things considered.

For further details see:

JRI: Real Assets Can Protect Against Inflation, But Watch The NAV Closely