PHD - JRO: Not Too Late To Take Advantage Of Rising Rates

2023-03-13 09:00:00 ET

Summary

- As the Fed looks to continue to raise interest rates in 2023, floating rate funds like JRO stand to benefit and offer well-covered high yield income.

- At a discount to NAV of more than -10% and a monthly distribution of $0.074 yielding 11%, JRO is a Buy.

- Three other Nuveen floating rate funds including JFR, NSL, JSD, are merging with JRO, pending shareholder approval.

While the Federal Reserve continues the fight against inflation by raising the base interest rate, I have previously written about several CEFs that benefit from the rising rate environment with investments in floating rate loans. Funds that invest in senior secured floating rate loans have seen their net income rising as the loans they hold pay higher yielding interest rates, allowing them to increase the distributions that they are able to pay out to shareholders.

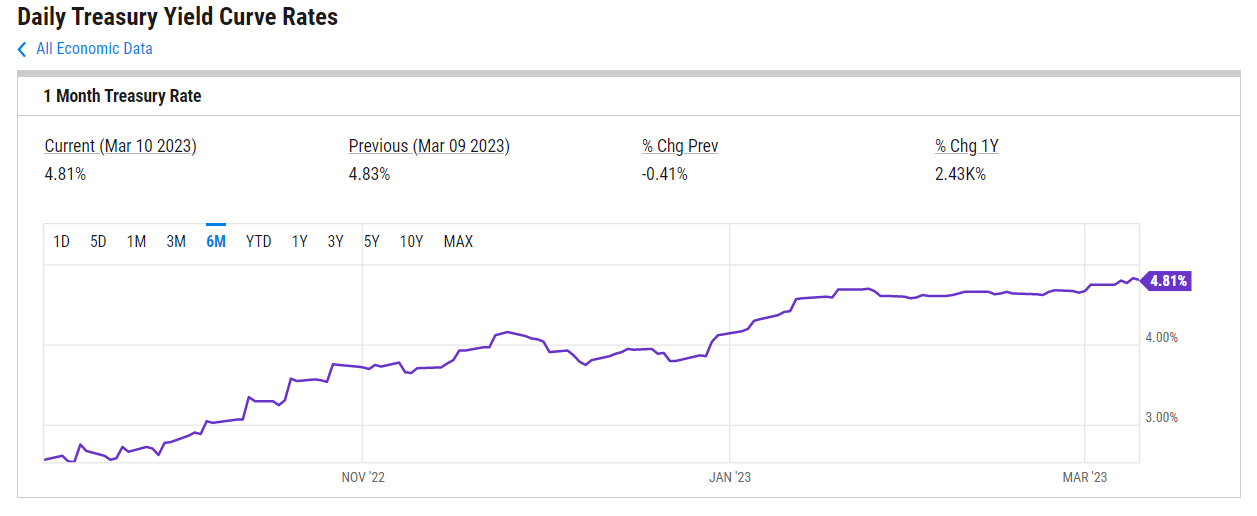

The current Treasury yield is sitting at about 4.8% and is expected to rise at least another 25 to 50 bps after the next Fed meeting. The chart below from YCharts illustrates the steady increase in the base rate over the past 6 months. As recently as this week, Fed Chair Powell cautioned that interest rates are likely to be even higher than previously anticipated.

Current market pricing moved higher following Powell’s remarks, to a range of 5.5%-5.75%, according to CME Group data. Powell did not specify how high he thinks rates ultimately will go.

{kind=link}

So, while this is bad news for growth stocks like technology and small caps that are harmed by higher rates and could lead to a broader downturn in the markets affecting many asset classes due to increasing fears of a recession approaching, several fixed income funds that benefit from rising rates should offer some shelter from this financial storm by providing high yield income even as the market price of the fund declines.

In the case of the Nuveen floating rate funds such as Nuveen Floating Rate Income Opportunity fund ( JRO ), which I last wrote about in December, the fund has seen a slight decline in price over the past 3 months, but with distributions reinvested the total return has been nearly flat compared to a slight loss of -3.43% in the S&P 500.

Seeking Alpha

In the case of JRO, which is similar to several other Nuveen funds that hold floating rate instruments such as Nuveen Floating Rate Income fund ( JFR ), Nuveen Senior Income fund ( NSL ), and Nuveen Short Duration Credit Opportunities Fund ( JSD ), about 82% of the fund holdings are in senior loans with most of the remaining in corporate bonds. Partly due to the similar nature of the 4 different fund holdings and in order to achieve a larger fund with lower operating expenses and higher earnings potential along with increased trading volume, Nuveen has proposed to merge the 4 funds into the JFR fund, if the merger is approved by shareholders at the upcoming annual meeting.

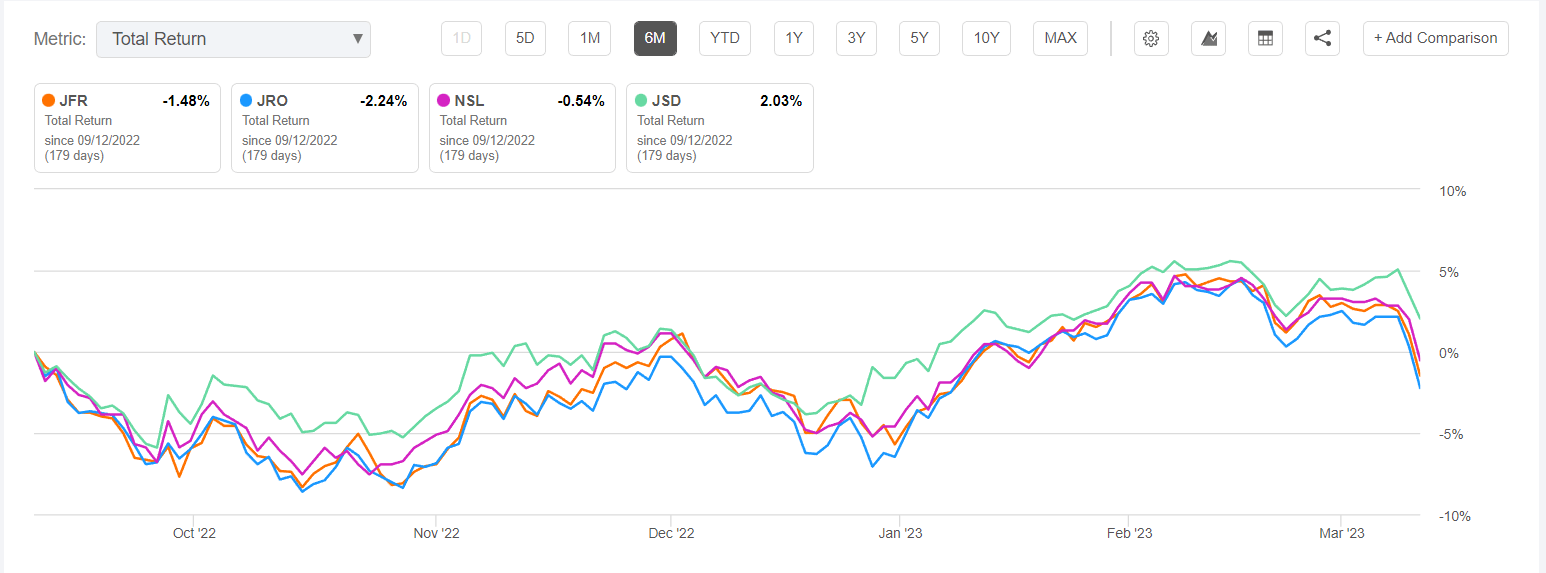

Comparing the 6-month total returns of the 4 Nuveen funds shows a very similar performance with a rising share price up until the last month or so. With dividends reinvested the total return has been relatively flat ranging between -2% and +2%.

{kind=link}

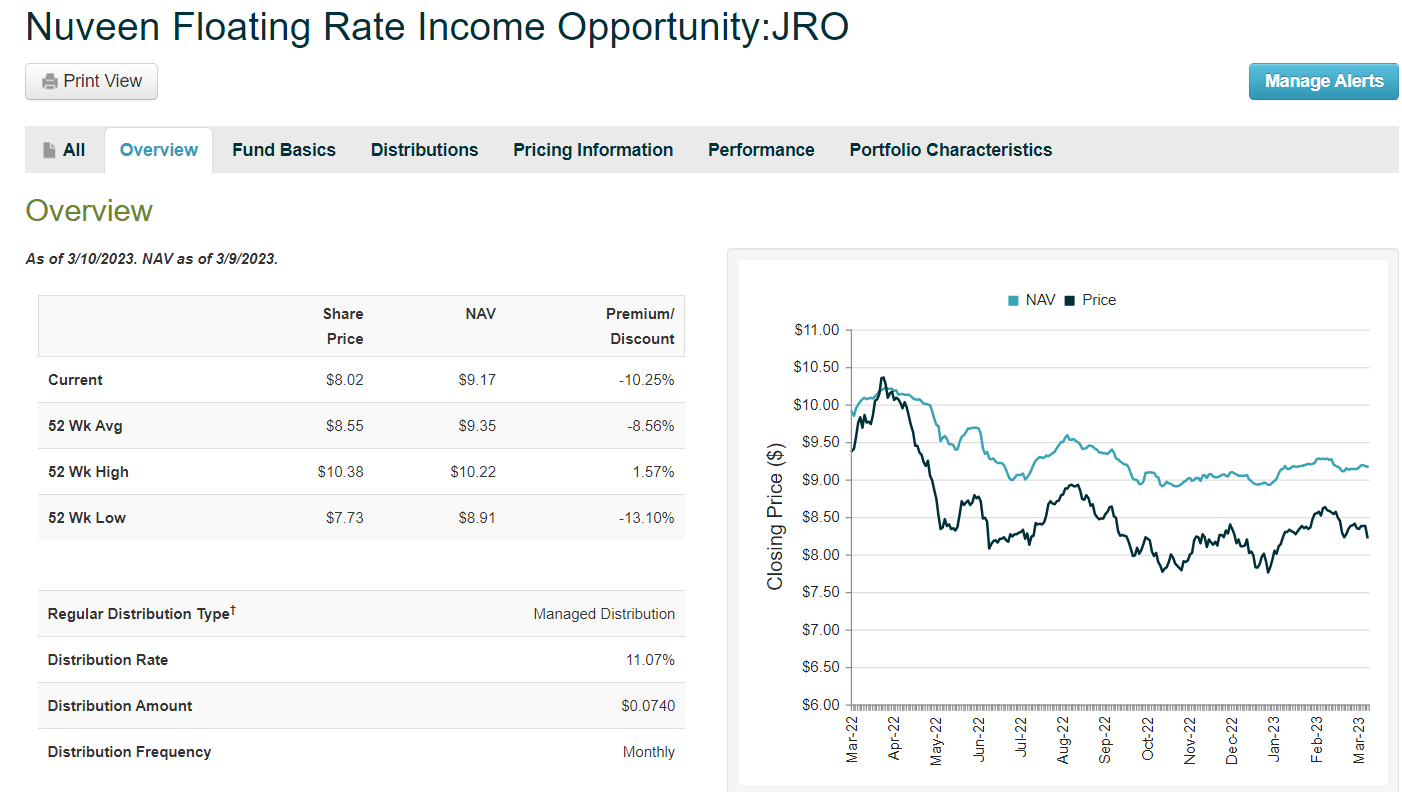

At the time of the December article, the JRO fund was trading at about a -8% discount to NAV and was yielding 10.5% based on monthly distributions of $0.074. As of market close on 3/10/23 the market price has declined to $8.02 and the yield has risen to 11%. The NAV of the fund is estimated at $9.17 leading to a market price discount of -10.25%.

The JFR fund, which will be the remaining fund after the merger is complete (if approved), is also trading at a discount of about -10% and yields 11%. JRO has total investment exposure of about $600M with 38.5% leverage. JFR has slightly more AUM with total investment exposure of $860M and has roughly 38.7% leverage.

While the focus of this article is the JRO fund, I recently sold my JRO shares and rotated into JFR instead with the expectation that it will be the surviving fund post-merger and should have better total return potential going forward, while trading at a similar discount and yielding nearly the same income.

JRO Characteristics

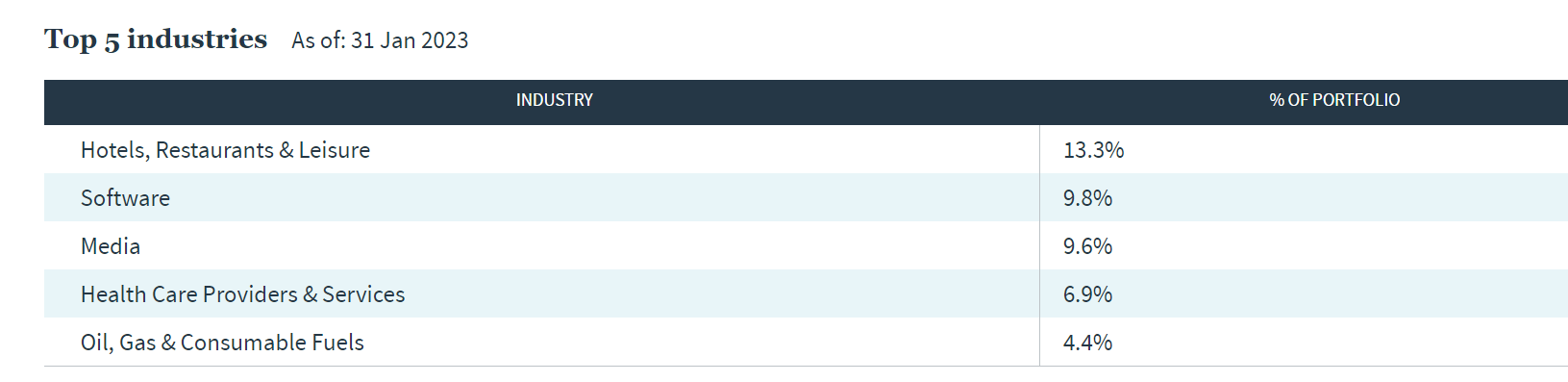

As of January 31, 2023, the number of holdings was 479 with an effective maturity of 4.59 years and an average leverage-adjusted effective duration of 0.71 years. The average bond price as a percent of par was $94.95. The asset allocation includes about 82% senior loans and 14% corporate bonds, with a smattering of common stocks, warrants, and asset-backed securities to round things out. The top 5 industries represented by the fund holdings are shown in this snapshot from the fund website .

{kind=link}

The credit quality of the fund holdings includes about 12.6% BBB, 38.7% BB, 42.4% B, and 4.5% CCC rated loans with less than 2% unrated. The fund’s call exposure consists of more than 87% callable in the next 12 months. That could be another potential positive for the fund if they can call some of the lower interest rate securities and re-issue new ones at higher rates.

The fund’s portfolio review from December 31, 2022, described the fund’s positioning going into 2023 based on general market conditions and expectations for a slowing economy.

We continued to favor higher-rated debt from larger, more liquid issuers, while mostly avoiding lower-rated, speculative credits (those rated B-/B3) whose yields were lower than what we would accept given their level of risk. We favored larger issuers with more scale, given their ability to pass through higher input costs and potential for withstanding an economic slowdown, were one to occur. The Fund also maintained exposure to select lower-quality assets with favorable total return potential. With risk premiums widening, we sought investment opportunities among names that met our risk/reward standards.

Fund Distributions

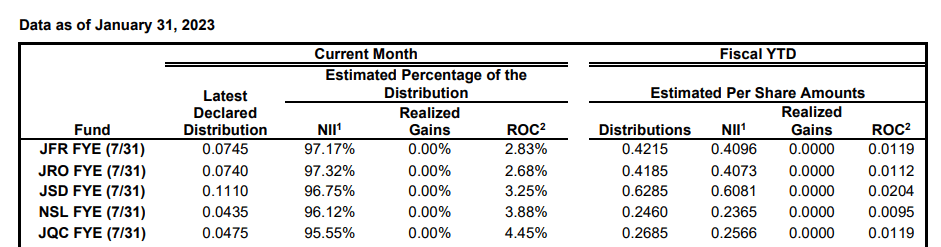

Each of the 4 floating rate funds that are expected to merge, JRO, JFR, NSL, and JSD, adopted a level distribution program. According to the February 28, 2023 fund notice , the funds intend to distribute a stable, although not guaranteed, level distribution that is not dependent on the timing of income earned or capital gains realized.

The majority of the distributions paid fiscal YTD (fiscal year ending July 31) include mostly NII with very little ROC.

{kind=link}

The JRO fund increased the monthly distribution twice in 2022, which indicates that the fund holdings did realize a benefit from the floating rate nature of those senior loans as interest rates increased. With the likely continuation of rate increases by the Fed in 2023, I would not be surprised to see another increase in the monthly distribution later this year as well.

Comparison to Similar Funds

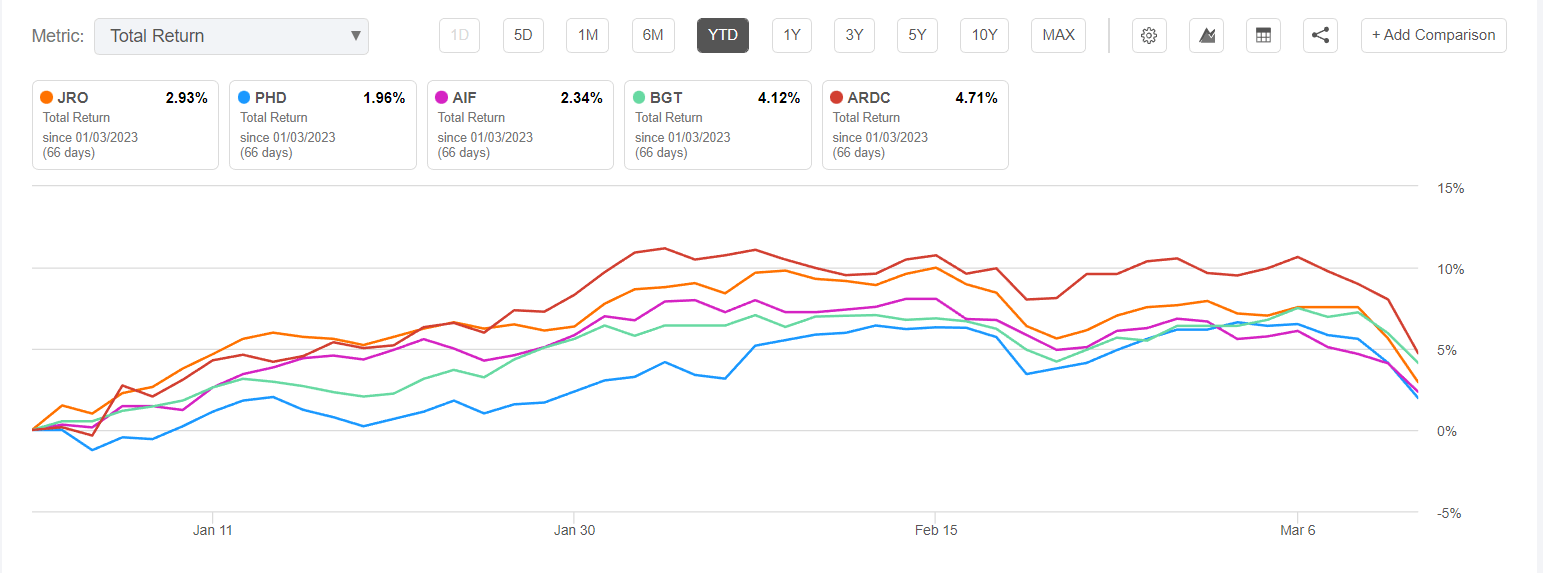

In my previous article I had also compared JRO to several other floating rate, leveraged loan funds. Some similar funds that also invest in senior loans that are mostly floating rate include Pioneer Floating Rate Trust ( PHD ), Ares Dynamic Credit Allocation Fund ( ARDC ), Apollo Tactical Income Fund ( AIF ), and Blackrock Floating Rate Income Trust ( BGT ). Each of those funds has also recently raised the distribution, and in some cases multiple times over the past 6 months. The YTD total return of those funds relative to JRO has been comparable as shown in this comparison chart.

{kind=link}

Risks and Recommendations

During the week ending March 10, which was one of the worst weeks in months for the overall market, the failure of the Silicon Valley Bank put a scare into investors who fear that sudden deleveraging could lead to a systemic breakdown in the financial sector. That could have obvious ripple effects through other lenders and potentially cause unexpected losses to pile up. The financial sector is now down -8.5% YTD and is one reason why the price of JRO has declined in recent weeks.

However, the JRO fund invests primarily in senior secured loans, which are higher in the capital stack than HY bonds, convertible, preferred, or common stock, and are secured by company assets. The likelihood of a systemic failure in the financial industry is still relatively small at this point and appears to be more isolated to somewhat “idiosyncratic” events, at least according to some analysts, that are not likely to impact the broader banking sector.

In my opinion, this market overreaction offers investors an opportunity to purchase shares of JRO at a reduced price that is not in too much danger of further downside. The discount to NAV has widened with the price drop but the NAV is steady so far in 2023 as shown in the snippet below from CEFconnect.

{kind=link}

I am not completely brushing aside the possibility that the broader market action could continue to the downside in the coming weeks, however, the overall economy is still showing signs of strength and loan defaults remain at historically low levels , although starting to rise slightly. Floating rate leveraged loan funds are well positioned to continue to benefit from rising rates and should remain in an income investors portfolio, in my opinion.

I rate JRO a Buy at the current discount of -10% to NAV and while it pays a well-covered 11% yield. And if the pending merger of the 4 Nuveen funds is approved, that could help to narrow the discount as the merger gets closer to completion, as long as the overall market does not take a huge dive to the downside before then.

For further details see:

JRO: Not Too Late To Take Advantage Of Rising Rates