KB - KB Financial: A Bargain From South Korea

2023-12-12 20:55:23 ET

Summary

- KB Financial Group is a large financial holding, including the largest bank from South Korea. The stock is very cheap compared to Japanese and American peers.

- The group has an impressive growth track record and has shown resilience during the pandemic.

- The low valuation in combination with a high shareholder yield of 8.8% is a great opportunity for value investors who want to diversify to Asia and the Korean Won.

- Scaling of business, digitalisation, acquisitions, and eleven subsidiaries offer protection against strong competition, a non-existing wide moat, and economic and monetary shocks.

1. Investment thesis

KB Financial Group ( KB ) is a large financial holding from South Korea with eleven subsidiaries (KB Kookmin Bank, KB Securities Co., KB Insurance Co., KB Kookmin Card Co., KB Life Insurance Co., KB Asset Management Co., KB Capital Co., KB Real Estate Trust Co., KB Savings Bank, KB Investment Co. and KB Data Systems). On the one hand, a holding with so many subsidiaries can offset problems and profit slumps of one unit more easily. On the other hand, it is strongly dependent on financial developments and financially healthy customers. The holding's services are offered in several Asian countries (South Korea, China, Hongkong, Cambodia, Vietnam, and Indonesia) which is a moderate geographical diversification. However, economic shocks from one of these countries, especially China, can spill over to all its operations.

Within an economic growth scenario which is very likely in the near future, KB Financial Group's stock seems to be undervalued and can lead to satisfying shareholder returns due to low valuation and increasing earnings with more room for dividend and buyback increases. The stock is an attractive opportunity for individual investors to diversify to Asia and the Korean Won.

2. Business development and subsidiaries

First of all, KB Financial Group is constantly growing its operating income for years. The pandemic did not interrupt this positive development at all.

| year |

| 2017 |

| 2018 |

| 2019 |

| 2020 |

| 2021 |

| 2022 |

| 2023e |

| operating income (KRW T.) |

| 10.2 |

| 10.8 |

| 11.4 |

| 12.4 |

| 14.5 |

| 15.0 |

| 16.6 |

Operating income grew 62.7% (CAGR of 11.4%), which is an impressive result in a period with lockdowns and economic shocks. The group combined organic growth with M&A activities as it bought the Malaysian PRASAC Microfinance for around $1 bn in 2021. Furthermore, the company took over Hyundai Securities in 2016, acquired Prudential Financial Inc's South Korean Unit in 2020, and merged its stock brokerage firm KB Investment & Securities with Hyundai Securities under its new subsidiary KB Securities. Finally, KB bought the Bukopin Bank to expand in Indonesia in 2021. All in all, the stunning revenue growth shows that the group has managed to diversify its business and to strengthen its units step by step. It is also a sign of successful capital allocation which is a key quality of long-term compounders. According to its recent financial statement , ten of eleven subsidiaries showed a net profit this year. The three most important subsidiaries in terms of profit they contribute to the group (after nine months) are KB Kookmin Bank (KRW2.8 T.), KB Insurance (KRW680 B.), and KB Securities (KRW361 B.). In terms of profitability (ROE/ROA), KB Asset Management (24%/17.5%) and KB Real Estate Trust (16.2%/11.3%) stand out positively, but are not really important for the group's total profit.

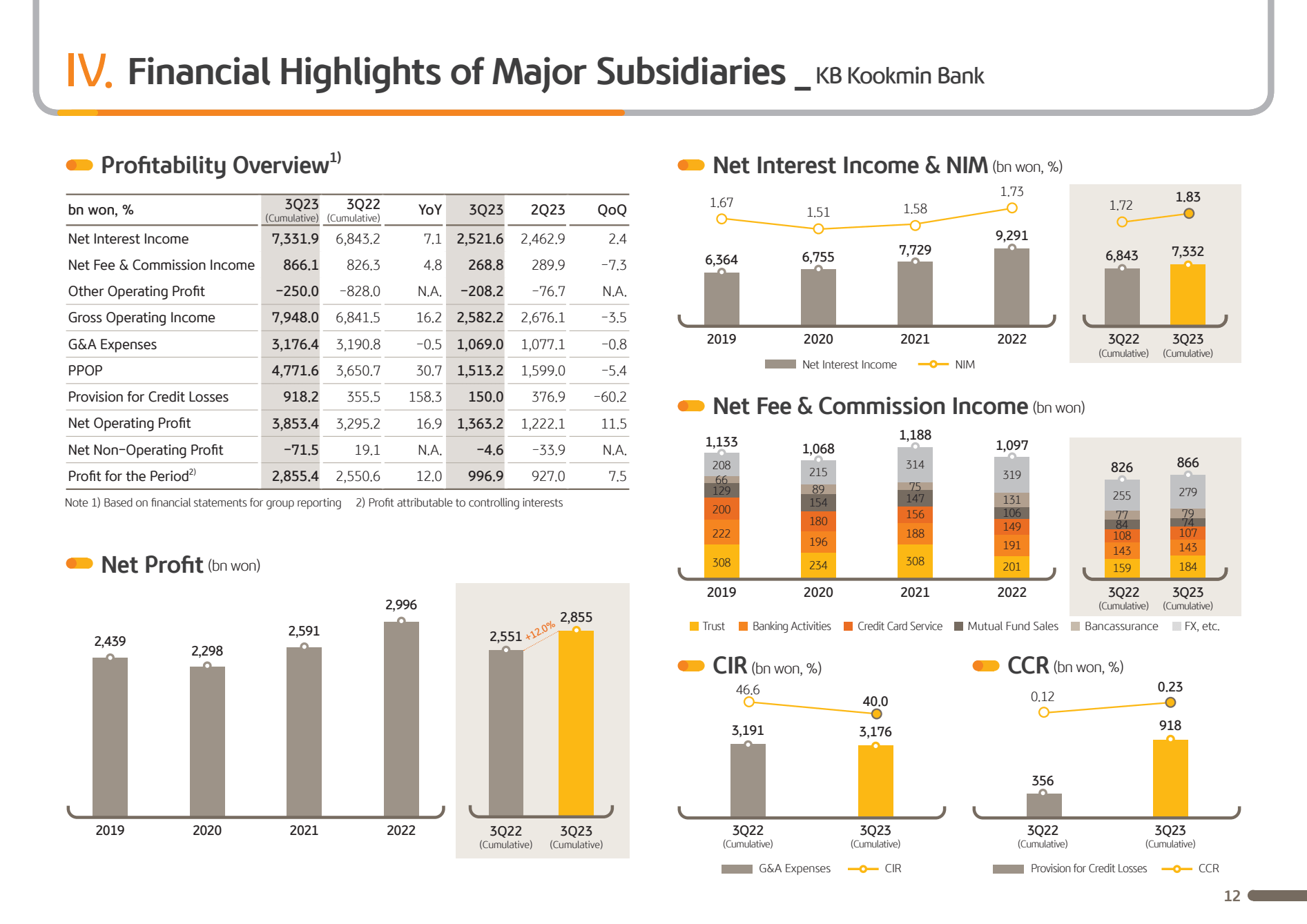

Firstly, KB Kookmin Bank is the biggest bank in South Korea and grew its assets by 78% within seven years (CAGR +8.5%) while South Korea's GDP just grew 24% in the same period. Next year growth for the country is expected to be 2.1% and will serve as a tailwind for Kookmin Bank as the bank is dependent on economic growth and stability. The bank's profit grew 12% YoY and although such a high growth rate is hard to maintain, the management showed that it can outperform the country's growth rate which was just 2.6% in 2022. Hence, near-term growth rates between 5-10% for interest income and net profits are likely.

Furthermore, the country's inflation rate as well as inflation rates in other countries like Japan or Vietnam were significantly higher in 2022 and 2023 than a few years ago. The net interest rate has also risen sharply to more than 4% and is now showing signs of normalization and returning to lower levels, albeit higher than in 2020 and 2021. Moderate inflation can help the bank to increase profitability and earnings. The current economic and monetary environment is favourable for Kookmin Bank, KB's biggest subsidiary. However, for banks, it has become harder to defend their business advantage against new financial startups and smaller banks. Strengthening its brand by focusing on customer loyalty and scaling the business, which means that the bank must win new clients while keeping costs under control, should be a key strategy for KB Kookmin Bank and KB's other subsidiaries. It seems that this is the strategy the management is currently pursuing with a 7.1% net interest income increase, a 12% profit increase, and decreasing G&A expenses.

{kind=link}

This strategy is supported by promoting digital platforms and online product sales which increased to 59% of the bank's total sales (+11 bp).

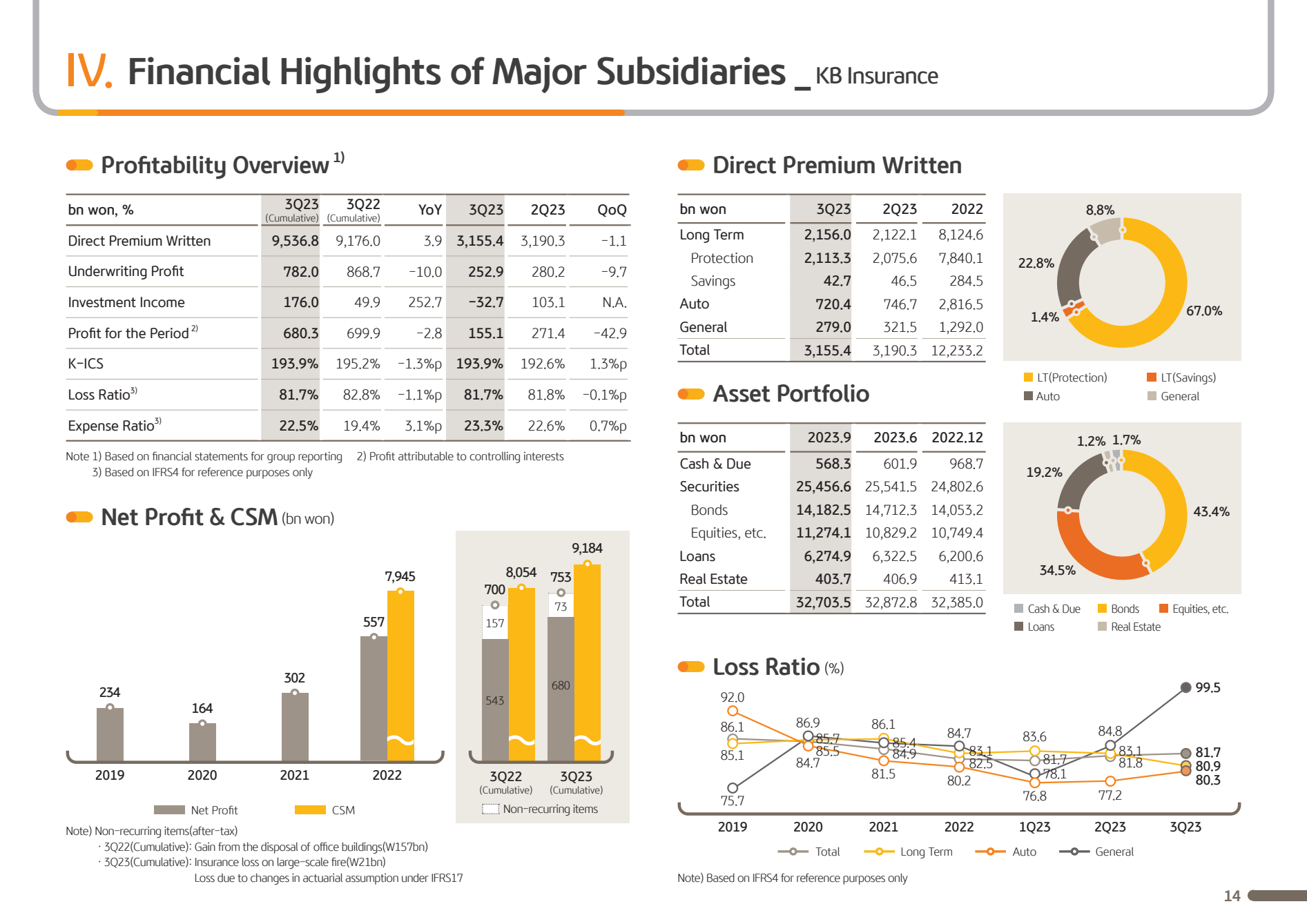

Secondly, KB Insurance is the second biggest contributor to the group's profit and the fourth most profitable subsidiary. In the third quarter direct premiums, underwriting profit and a negative investment income (which is more volatile) led to a 43% decrease in total net profit.

{kind=link}

The annual decrease is marginal so far and a better investment income in the fourth quarter can still increase KB's Insurance profit. As long as the subsidiary shows stable or slightly growing direct premium written, it will play a major role in KB's future success.

Thirdly, the subsidiary KB Securities increased profits YoY by 19% to KRW361 B., mainly supported by a high trading income and an increased interest income (+13%) as expected because of the monetary environment. G&A expenses increased by 12.2%, although net fee and commission income fell by 13.1% in the same period. In conclusion, the third most important subsidiary for KB Financial Group is also one of the most vulnerable businesses, since it is dependent on volatile trading income and must keep an eye on cost control and decreasing net fee and commission income, its biggest income generator. Moreover, KB Securities just ranked 8th among eleven subsidiaries in terms of profitability.

All in all, in the current economic and monetary environment KB Financial Group can grow moderately and increase profits by scaling up its two major subsidiaries with the help of online sales and brand strengthening. Investors should keep an eye on the growth and profitability metrics of KB's smaller subsidiaries though. If earnings of KB Security, KB Kookmin Card, or KB Life Insurance deteriorate, investors must quickly identify the cause to evaluate KB's overall economic situation. At the moment, the management is doing fine and is actively strengthening the business via digitalisation and acquisitions.

3. Valuation

The stock trades for $39 or KRW51800 which means that the stock:ADR ratio is 1. The market capitalization is $14.9 B. with 382.35 million shares outstanding.

The 10-year stock performance is very disappointing with a 2.36% total (!) gain (without dividends). Since 2001 the stock has been trading in a range between $18.8 and $97.2 which shows that it is far away from its all-time high. For 2023 the group is expected to earn KRW5.6 T. or KRW14646 per share (=$11.1). The stock's fundamental ratios can be found in the table below:

| P/E23 |

| CAPE7 |

| P/B |

| ROE |

| growth |

| yield |

| 3.5 |

| 5.2 |

| 0.33 |

| 11.7% |

| 5-10% p.a. |

| 8.8% |

The book value per share is KRW153785 or $116.6 which indicates a strong undervaluation as well as a P/E ratio below 4. The yield is a combination of a dividend yield of 5.8% (DPS= $2.26/KRW2981) and a possible execution of the rest of a share buyback of KRW600 B., which the author Value Pendulum called "highly likely" because concerns over a limitation of distributions for financial institutions are "overdone". Nearly KRW 300 B. have already been invested for the first half of the program in early 2023. The buyback represents a buyback yield of 3.0% (or KRW1569 per share) and combined, the shareholder yield climbs to 8.8% with a dividend payout ratio of just 20%. The expected growth rate is very conservative and KB Financial Group can also exceed these expectations. As a consequence, a higher dividend and constantly growing payouts are very likely. It is also likely that the rest of the buyback will be completed soon because, at the current share price, such a move would be very smart and would create great value for shareholders.

Peer comparison

Compared to the second largest Korean bank, Hana Financial Group, KB is valued equally with HFG showing a P/E ratio of 3.5, a P/B ratio of 0.35, and a dividend yield of 8%.

The ratios for Bank of China ( BACHF ) are also very low (P/E= 3.6, P/B= 0.28, yield= 9.1%), but Japanese banks or financial institutions like Mizuho Financial Group ( MFG ) have higher valuations and lower dividend yields. Looking at similar institutions in the USA, it is obvious that KB Financial Group is ridiculously cheap.

The peer comparison shows that KB is similarly valued to its Asian peers in South Korea and China, but significantly undervalued to Japanese and American financial stocks.

4. Risks

One major risk is a financial or economic shock which would hurt the Asian markets and KB's customers. The largest subsidiary, KB Kookmin Bank, would suffer the most. However, the past years have shown that the group can manage to grow in economically harsh environments (pandemic, lockdowns). The Asian markets will possibly grow and outpace other continents. Consequently, KB Financial Group has a geographic advantage that it can use to grow its customer base, assets, and earnings in the near future.

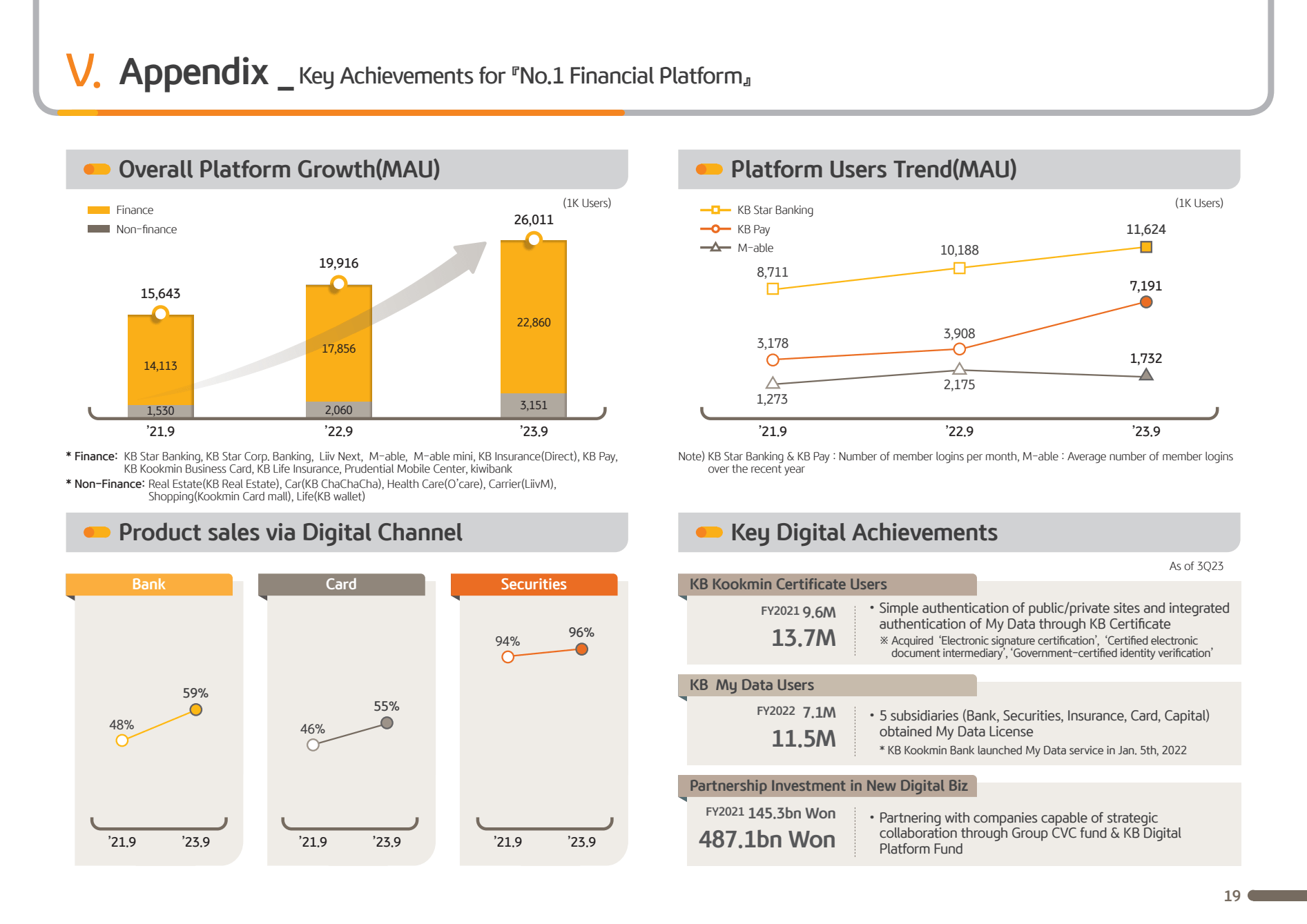

A second risk is a loss of customers due to a rising number of competitors as it is hard to establish a wide moat in banking and financial services. The group's answer to this risk is scaling up its business by improving overall costs and expanding online platforms.

{kind=link}

As shown in the slide above from the company's third quarter earnings release, recent user trends show that KB Financial Group is doing well by increasing platform user numbers by 26% YoY. Increasing online offers and products increase costs for now, but as shown before, the company managed to have its total costs under control and improve net earnings.

A third risk is a high inflationary economy with interest rates rising too fast. These conditions will be headwinds to KB's real estate and banking business as well as to its asset management, savings and securities business as they would hurt financial markets and the financial situation of its customers. However, 2022 was a year with extraordinarily high inflation rates which are now normalizing below 4%. Current inflation trends and economic expectations will help the company to thrive.

5. Conclusion

KB Financial Group is a fast-growing South Korean group that is profiting from the current economic environment. KB has shown that it can weather many storms and its diversified business can improve net interest income and earnings by scaling, brand strengthening, and digitalisation. The stock is cheap according to its low fundamentals and low valuation compared to Japanese or American peers. The group can easily raise the dividend and execute a huge share buyback program with potentially little risk of regulator intervention. Although the stock has performed badly over the last decade, it offers great value to investors who want to buy a bargain from South Korea.

For further details see:

KB Financial: A Bargain From South Korea