TMHC - KB Home: A Great Home For Your Money As Earnings Near

2024-01-05 09:17:13 ET

Summary

- KB Home is expected to announce worse year-over-year financial results for the final quarter of 2024, but analysts are optimistic about the forward-looking data.

- The homebuilding industry is showing signs of recovery, with strong orders and a drop in cancellation rates.

- Despite some signs of weakness, KB Home's stock has performed well, and the company is trading at an attractive price.

On January 10, after the market closes, the management team at homebuilder KB Home ( KBH ) is expected to announce financial results covering the final quarter of the company's 2023 fiscal year. Judging by the company's share price performance over the past several months, you might think that analysts are forecasting rapid growth for the enterprise. But in fact, the exact opposite is true. Year over year, financial results should come in worse for the most part. However, it is the forward-looking data that has analysts excited. If current trends persist, management will show that the home building industry continues to be in a state of recovery. Strong orders, combined with a drop in the cancellation rate, will likely demonstrate that the worst days for the company and the space as a whole are in the past. Add on top of this how cheap the stock is, and some attractive upside could be in store for investors.

Mixed expectations

In early 2023, I found myself taking a rather bearish stance on the home building industry as a whole. I still rated certain companies in a positive manner because of how cheap they were and because of the long-term outlook for the space. But my view is that inflationary pressures, combined with high interest rates aimed at combating that inflation, would curtail home construction for at least 12 to 18 months. But less than six months into the year, the data, in the form of new orders and cancellation rates, was coming in strong enough for me to change my mindset in a bullish manner.

One of the firms that I have been bullish on is KB Home. From my last article on the business in September of 2023, in which I said that additional upside existed from that point, KBH shares have spiked 20.5% at a time when the S&P 500 is up 5%. And since my first bullish article on the company in March of last year, the stock is up a whopping 55.6% compared to the 16.3% seen by the broader market. Of course, it hasn't been the only beneficiary. The S&P Homebuilders Select Industry Index ( SPSIHO ), for instance, is up 47.6% over the past year.

{kind=link}

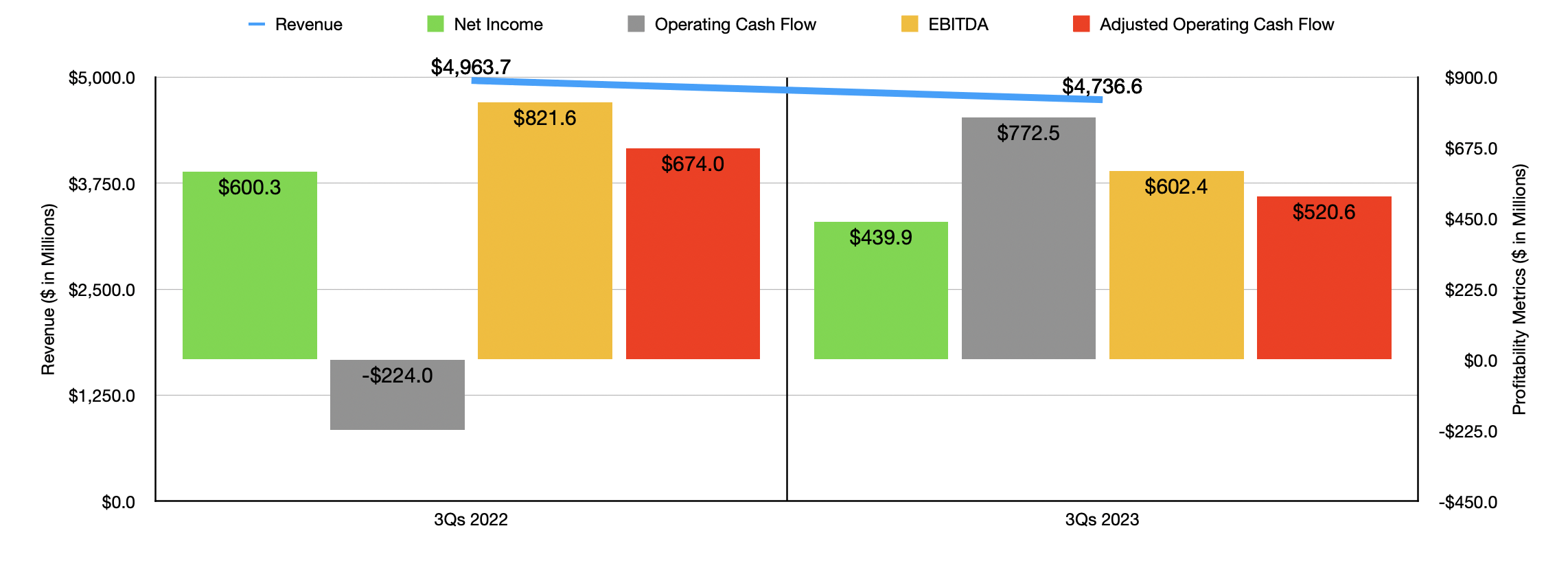

This kind of upside for KB Home has occurred even as the company has seen some signs of weakness. In the chart above, for instance, you can see revenue, profits, and cash flows, covering the third quarter of the firm's 2023 fiscal year compared to the same time one year earlier. If you compare this to the data in the chart below that shows results for the first nine months of 2023 as a whole compared to the same nine months of 2022, you can see an acceleration of the pain as the year progressed.

{kind=link}

On the revenue side for the third quarter, sales hit $1.59 billion. That's 14% lower than the $1.84 billion reported the same time one year earlier. This drop in revenue can be attributed to a couple of factors. For starters, the number of homes delivered during that window of time came in at only 3,375. That's a drop of 6.6% compared to the 3,615 homes delivered one year earlier. For the first nine months of 2023, relative to the same time the prior year, home deliveries fell a more modest 1.2% from 9,952 to 9,829. Another issue involved the average selling price of these homes. By the third quarter of 2023, the average price of a home delivered had fallen to $466,300. That's a drop from the $508,700 reported one year earlier. Another thing that's telling is the fact that, year over year, the backlog of homes for the company managed to decline from 10,756 to 7,008.

{kind=link}

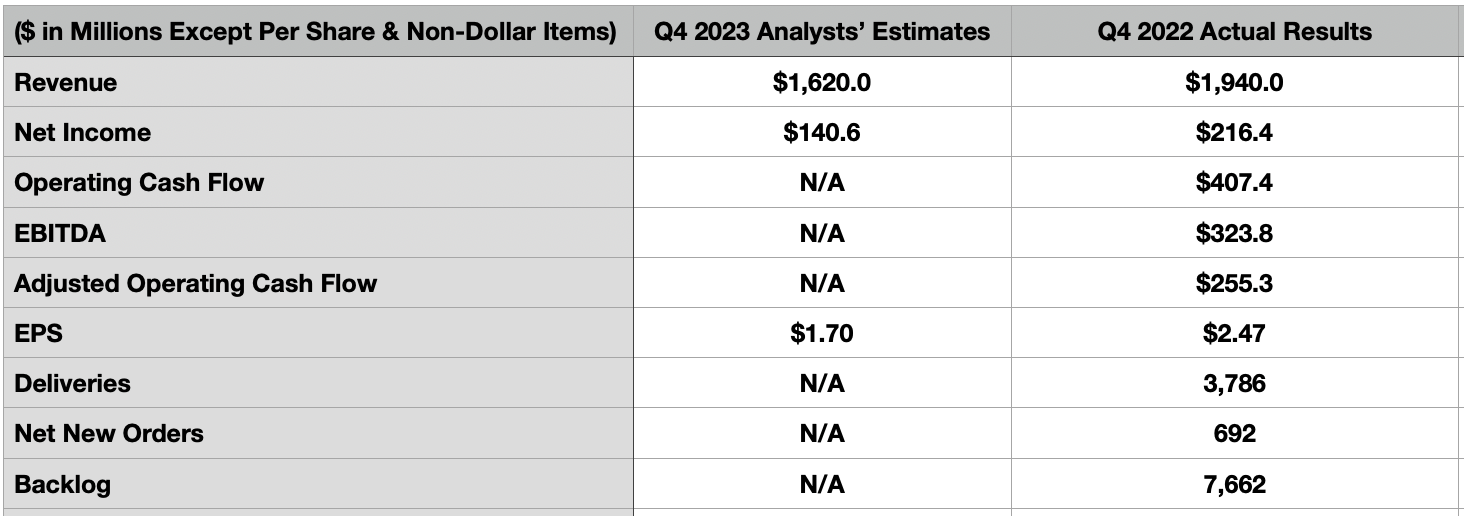

When it comes to the final quarter of 2023, investors should expect continued pain from a revenue and profit perspective. At this moment, analysts are forecasting revenue of $1.62 billion. That would be down from the $1.94 billion that the company reported in the final quarter of 2022. What's interesting is that management is currently forecasting revenue for the year of $6.31 billion. This means that management is of the opinion that housing revenue for the final quarter should be around $1.57 billion. Management did not provide any guidance when it came to financial services revenue. So there could be some amount in between there that is made-up by that particular source of sales. Regardless, what we do know is that management is forecasting an overall average selling price for the year of $481,000 per unit. And with the average selling price for the first nine months coming in at $479,200, there is the expectation of a meaningful improvement over what the company saw in terms of pricing in the third quarter. How high this price will need to be will depend in large part on the number of deliveries achieved. For context though, the average selling price for the final quarter of 2022 was $510,400 and that was based on 3,786 deliveries.

{kind=link}

When it comes to the bottom line, analysts are currently forecasting earnings per share of $1.70. That would represent a rather meaningful decline from the $2.47 per share reported the same time of 2022. It would also translate to net profits dropping from $216.4 million to $140.6 million. Analysts have not provided any estimates when it comes to other profitability metrics. But for context, operating cash flow in the final quarter of 2022 was $407.4 million. If we adjust for changes in working capital, then operating cash flow in the final quarter of 2022 would have been $255.3 million. And finally, EBITDA was $323.8 million.

{kind=link}

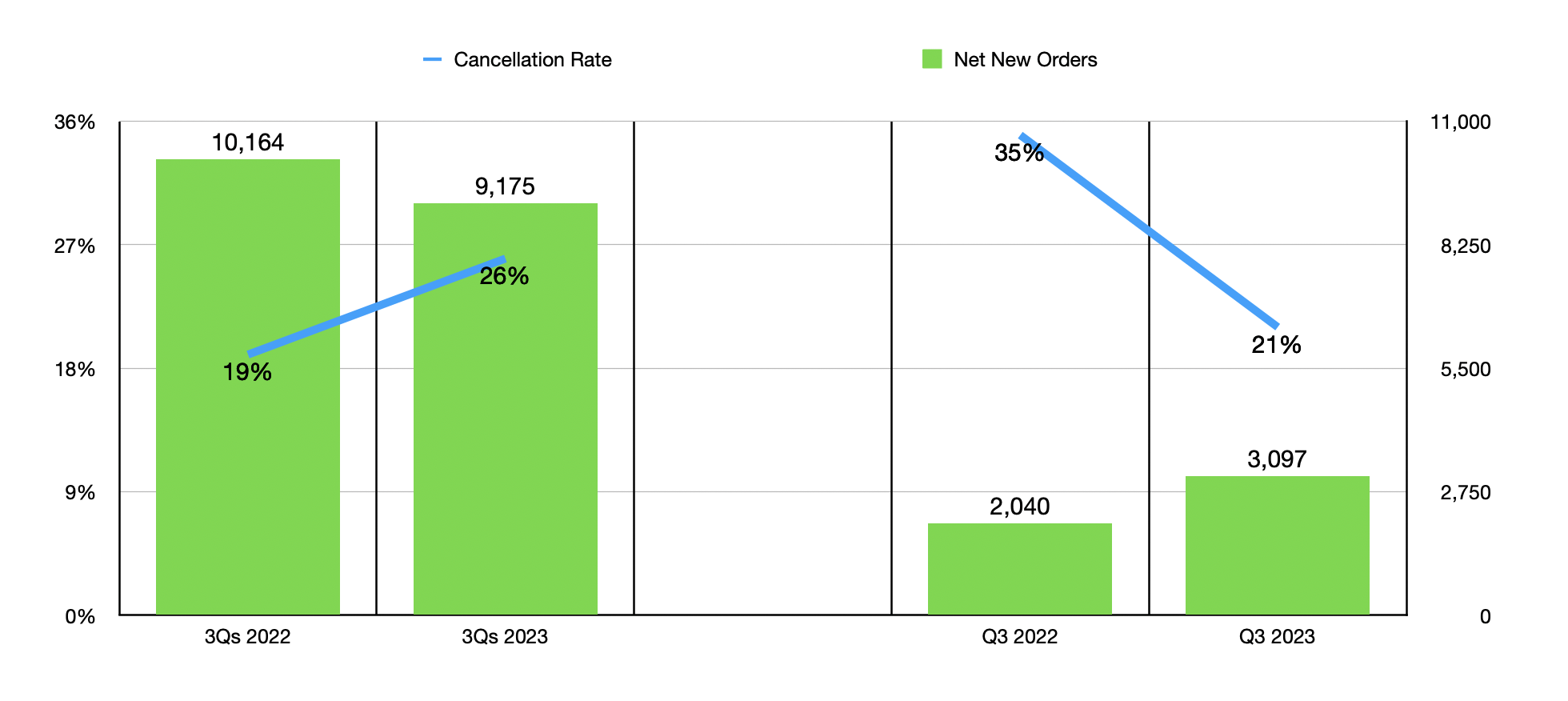

With numbers and expectations like this, I can understand why some investors would be worried about buying into a stock, especially one that has risen as much as KB Home has. However, leading up to this point, there have also been some really positive signs. Although for the first nine months of 2023, net orders are still down compared to what they were the year prior, in the past couple of quarters the picture has changed. In the third quarter of this past fiscal year, for instance, net new orders for homes came in strong at 3,097. That represents an increase of 51.8% compared to the 2,040 net new orders placed the same time one year earlier. In all likelihood, the company will report substantially higher orders than the 692 that were placed in the final quarter of 2022.

{kind=link}

In addition to this, the firm has also seen its cancellation rate drop. Again, for the first nine months relative to the same nine months one year earlier, the cancellation rate has still grown from 19% to 26%. But in the third quarter on its own, the cancellation rate was down to only 21%. Although still well above the historical average for the enterprise, it represents a massive improvement over the 35% cancellation rate that the company reported for the third quarter of 2022.

{kind=link}

My opinion on the business might be different if shares were expensive. But this does not appear to be the case. We don't know exactly how the company will perform for the final quarter. But if analysts are correct, total net profits for 2023 will have been $580.5 million. This implies adjusted operating cash flow of around $696.2 million and EBITDA of somewhere around $814.5 million. Using these estimates, I was able to value the company as shown in the chart above. That chart also has valuation figures using data from 2022. Meanwhile, in the table below, I compared KB Home to five similar firms. On a price to earnings basis, three of the five companies ended up being cheaper than it. This number drops to two, with another being tied with it, when we use the EV to EBITDA approach. Though when it comes to the price to operating cash flow approach, our prospect was the most expansive when compared to the four firms that had positive readings.

| Company |

| Price / Earnings |

| Price / Operating Cash Flow |

| EV / EBITDA |

| KB Home |

| 8.2 |

| 6.9 |

| 7.2 |

| Taylor Morrison Home Corp ( TMHC ) |

| 6.4 |

| 4.7 |

| 5.5 |

| Legacy Housing Corporation ( LEGH ) |

| 8.9 |

| N/A |

| 7.2 |

| Meritage Homes ( MTH ) |

| 7.7 |

| 6.0 |

| 5.7 |

| Century Communities ( CCS ) |

| 11.1 |

| 6.6 |

| 10.5 |

| Beazer Homes USA ( BZH ) |

| 6.1 |

| 5.5 |

| 8.6 |

Takeaway: KBH Is A Buy

As things stand, I believe that the worst for the housing market is long gone. Orders are growing nicely and cancellation rates are coming down. We are likely to see continued weakness in the near term because of the delayed impact of the pain on this enterprise and those like it. But as long as we don't have any negative surprises when it comes to the cancellation rate or net new orders, I have no reason to be anything other than optimistic about the future. Clearly, relative to similar firms, the easy money has been made. But I do think that the entire industry is currently trading on the cheap. Management seems to agree with me on this. During the third quarter alone, the business repurchased 1.5 million shares for $82.5 million. And for the first nine months of 2023, management repurchased 5.7 million shares for a total of $249.6 million. All combined, this leads me to keep the company rated a ‘buy’ for now.

For further details see:

KB Home: A Great Home For Your Money As Earnings Near