KELTF - Kelt Exploration: Management Got The Memo

2023-06-30 06:57:51 ET

Summary

- Kelt Exploration's management switched from an asset strategy to a cash flow strategy.

- Cash flow will be reinvested to grow the company because this is a growth story.

- The equity sales ended with the asset sales (for the most part). Now the strategy is growth within cash flow.

- Valuation ratios have shrunk along with the rest of the industry making this company a bargain.

- This small company is for patient investors because you never know when a small company like this one will attract market attention.

(Note: Kelt Exploration is a Canadian company that reports using Canadian dollars unless otherwise noted.)

Kelt Exploration (KELTF) management began building this company as an asset story. As such, periodic sales were needed to keep the debt at a controllable level. But then the market attitude towards such a strategy changed. This management picked up on that change to set a very different strategic future that is more in tune with current market desires. But the market has yet to really pick up on the attitude change by management.

Historical Review

This is likely what the market remembers:

Kelt Management Presentation Of Major Sales History (Kelt Exploration Corporate Presentation May 2023)

{kind=link}

This was a strategy that included "running up the debt" and then using the sales to repay the debt and reinvest in the business to "rinse and repeat". At one time a lot of companies did this, and it was a fairly popular strategy.

But asset stories tend to struggle when the market turns down. This management beat those odds as shown above with two sales during the particularly trying period of 2015-2020.

The problem with this is that management always started over as essentially an asset story yet again. Despite the successes, the stock was going nowhere fast.

The last sale left the company with a whole roughly 16 KBOED of production. Compared to the market value of the stock outstanding, this was a proverbial "drop in the bucket".

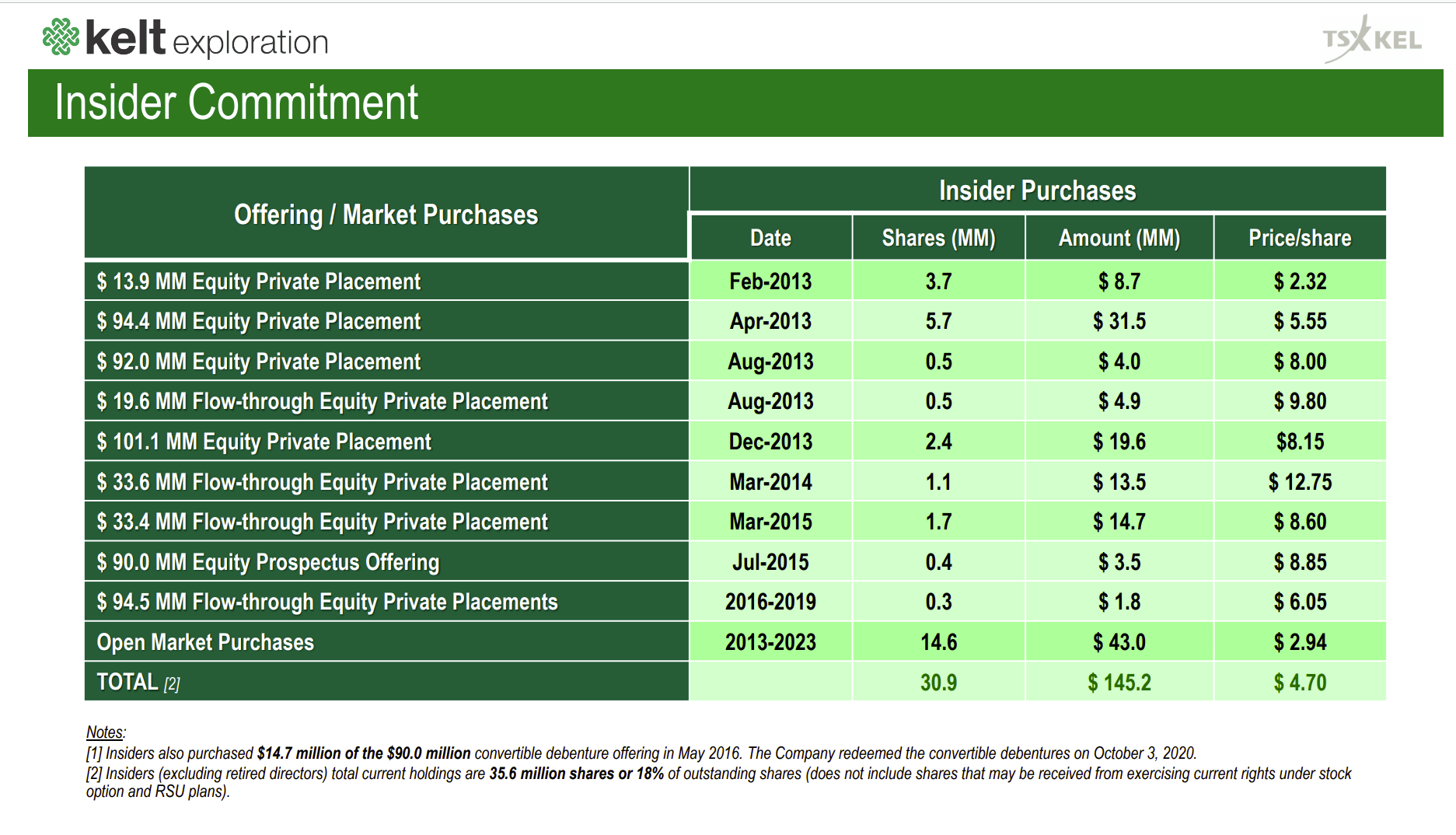

Kelt Exploration Presentation Of Share Offerings And Insider Purchases (Kelt Exploration Corporate Presentation May 2023)

{kind=link}

In addition to the asset sales, the outstanding stock was growing at a healthy pace as shown above. Even though insiders were purchasing the stock, the market was not buying into the faith shown by management.

After the last sale in fiscal year 2020, management used the proceeds to repay debt and has largely remained debt free ever since. That implies growth within cash flow which is a good deal slower than was the case in the past. However, it fits into the current atmosphere of what Mr. Market expects companies to do.

Production History

Now since that last sale in fiscal year 2020, production has grown. But because production is relatively small, the company is likely to remain a growth story for the foreseeable future. Management is very good at building and selling things. So, at some point, the whole company may get sold. But that means income investors probably need to look elsewhere.

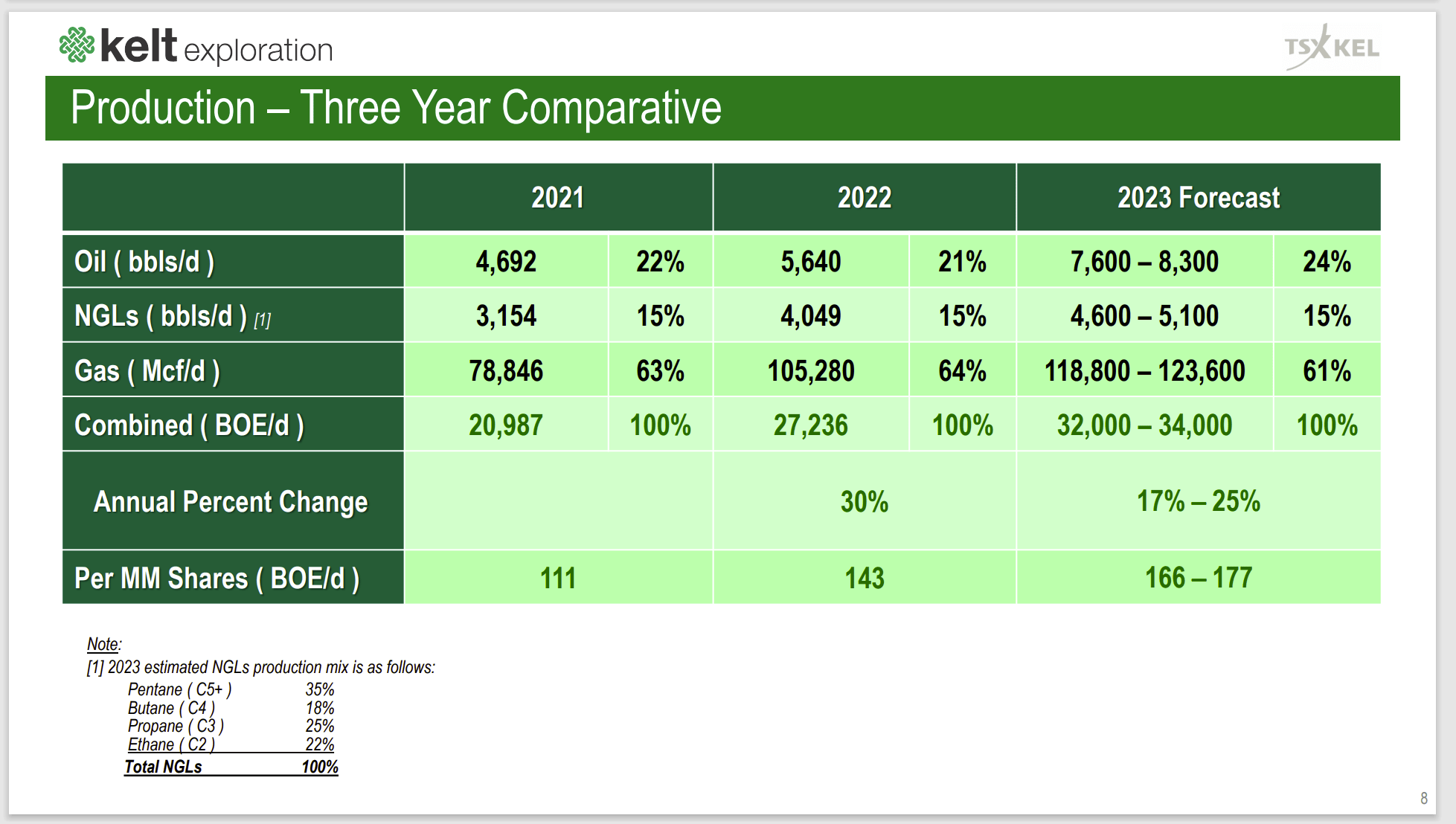

Kelt Exploration Three Year Production Growth History (Kelt Exploration Corporate Presentation May 2023)

{kind=link}

The ability to grow production at the pace shown above is a sign of some profitable acreage. There is enough oil production here to probably assure above average profitability in a lot of industry pricing scenarios.

This is yet another thing that the market will discover about this natural gas producer. The revenue stream is more valuable than that of dry gas producers.

Latest Quarter

The industry has largely been out of favor over the last few years. So, the progress made here has largely gone unnoticed. Instead. a lot of key valuation measures have contracted in line with the industry.

Complicating matters is that the market did not like the strategy of the past and so has likely not yet picked up on the change in strategy for the last few years and for the foreseeable future.

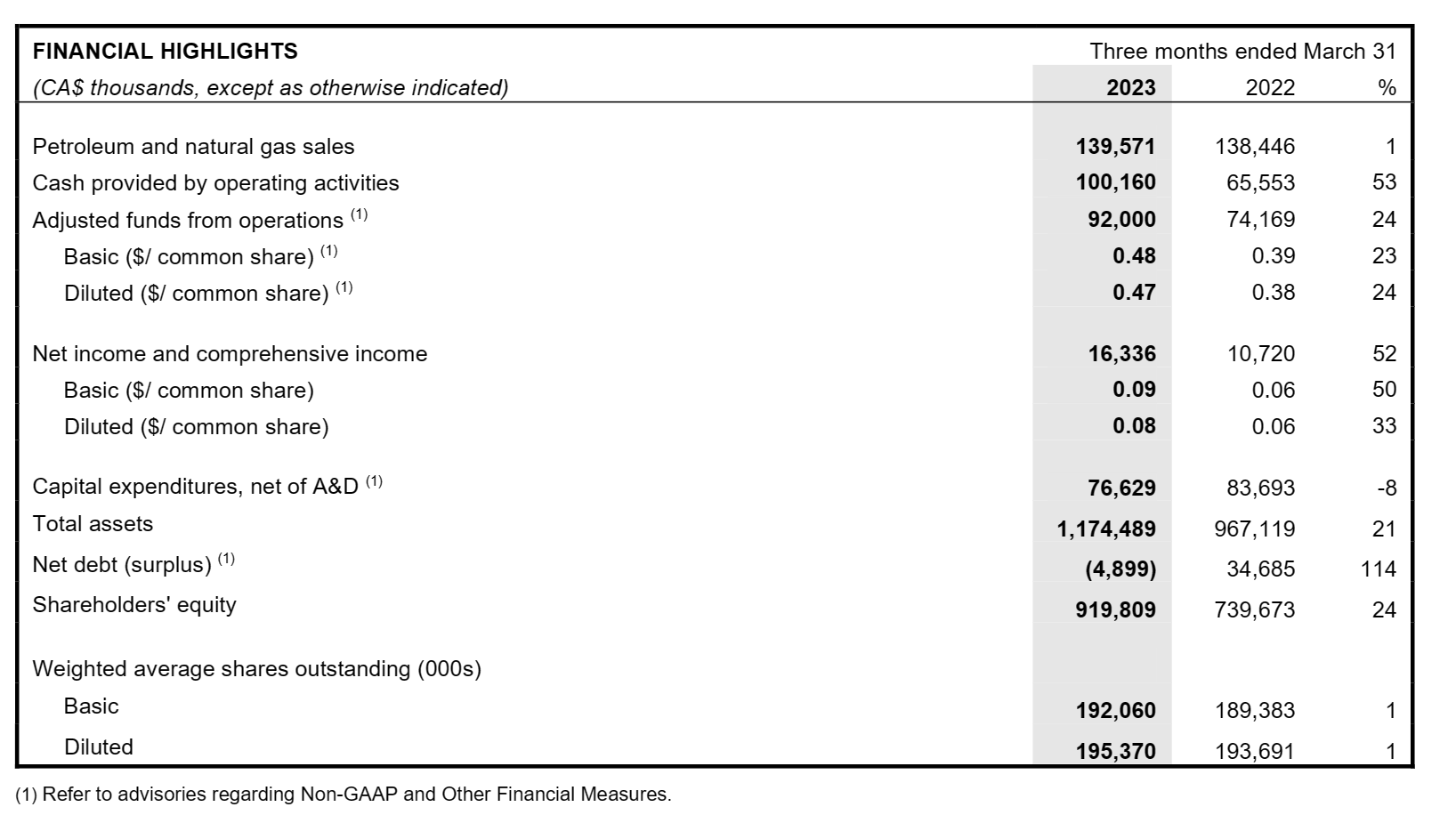

Kelt Exploration First Quarter 2023, Earnings Summary (Kelt Exploration First Quarter 2023, Earnings Press Release)

{kind=link}

Now with cash flow approaching a value level not seen in some time, this company has a valuation comparable to many I follow. But with a far more experienced management, it may make a solid speculation that management can do more faster with these assets than some of the less experienced managements that I follow.

Risk Mitigation

This management has built and sold assets to some top companies in the industry. That is a very rare accomplishment among small companies.

Management experience mitigates the risk that fast growth often brings to a company. This management knows how to rapidly build by adding infrastructure and personnel to mitigate the small company risk.

The company shows negative net debt which mitigates the financial risk inherent in those investment proposals. This is an industry with very low visibility. Therefore, it is imperative to have a strong balance sheet. Negative net debt fits that requirement.

The other risk is that an investment like this requires patience. There is no telling when the market will recognize the accomplishments here. As long as management keeps going and the main story does not change in an unacceptable way to the investor, then patiently waiting is what is needed. Too many investors get involved in something like this only to sell before the market notes the company successes.

Costs And Netbacks

This company has very reasonable costs for the production mixture. But it needs to be noted that management depends upon a matrix of prices to determine breakeven. That makes breakeven analysis challenging when looking at only one commodity product.

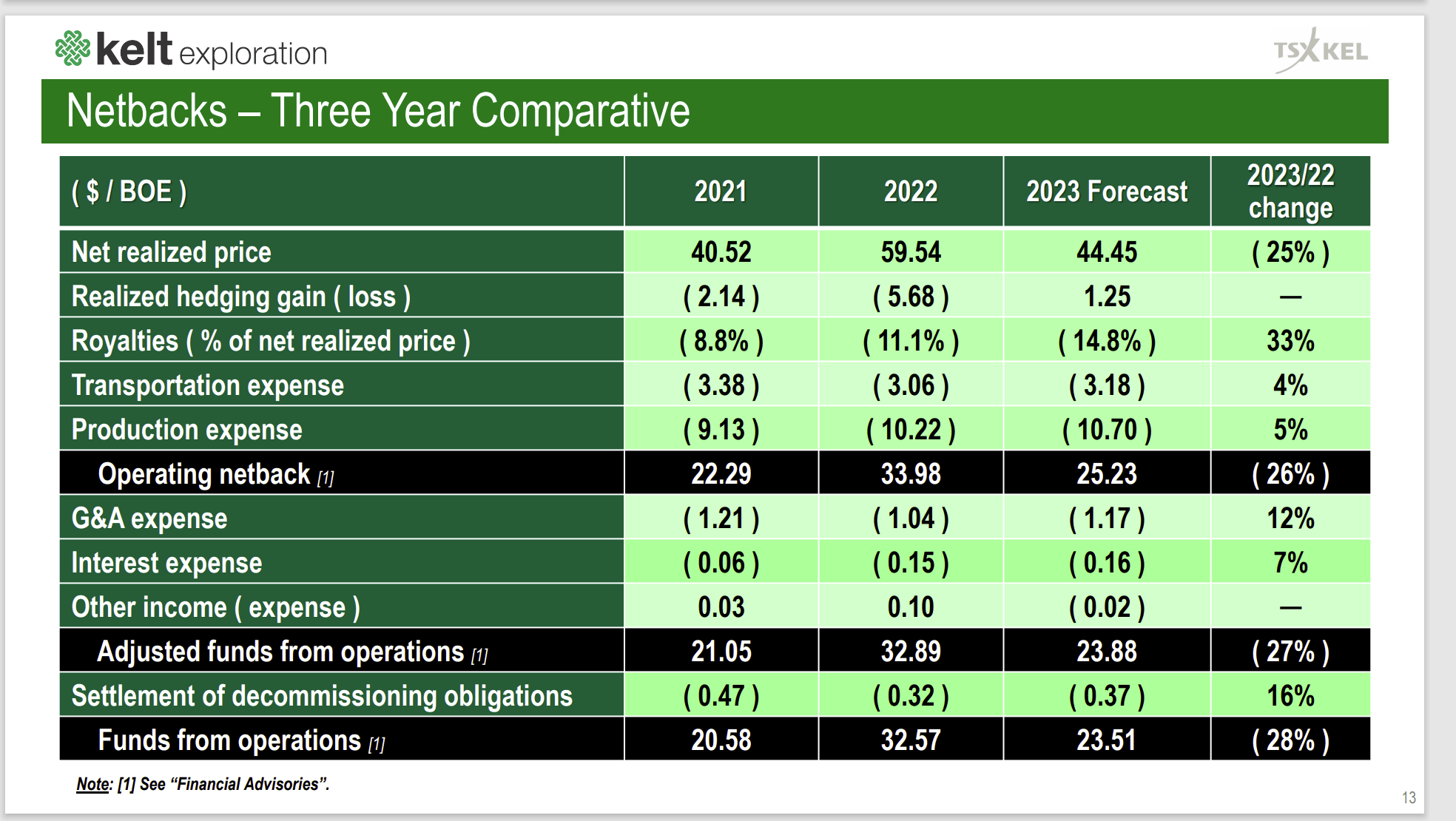

Kelt Exploration Netbacks And Costs Three Year History (Kelt Exploration Corporate Presentation May 2023)

{kind=link}

Management has a production expense that is higher than dry gas and even some low-cost oil producers. However, the overall operating netback and other key items appear to be more than reasonable. The administration expenses are actually among the lowest of the companies I follow.

Management is able to get the natural gas to various market through transportation agreements. That is going the "extra mile" and is a good sign of a proactive management. I follow a lot of companies that dump the production nearby at whatever price they can get. That is not the case here. As production grows, management will likely be able to get some better pricing based upon the larger volumes.

Key Takeaways

Kelt management is very experienced at building and selling. This negates the typical small company risks of less experienced management. Furthermore, the net debt is negative. So, the company essentially has a debt free balance sheet that mitigates financial risk as well.

Like many small producers, this company is out of favor with a stock price that was "left for dead". However, management is growing production at a rapid pace. A 25% growth rate of production would mean that production will triple roughly every 5 years. That kind of continued growth will attract attention at some point.

For the patient investor, this small company is a decent investment proposal (a strong buy consideration) as part of a basket of small companies. The management experience and debt free balance sheet point to far lower than usual small upstream company risk. I would consider selling when management either makes a major sale or sells the whole company.

For further details see:

Kelt Exploration: Management Got The Memo