KKOYF - Kesko: The Upside Is Once Again Here

2023-06-28 23:16:39 ET

Summary

- I've not covered Finnish company Kesko in years, but have made a successful investment in the company, selling shares at a 170% return on rate when the price hit €32/share.

- I highlight the importance of recognizing overvaluation in investments, using Kesko as an example, and state that even if I sold at €5/share before the peak, it was still a good decision.

- I've decided to update readers on Kesko because I believe Finnish companies deserve more coverage and that Kesko, now near €17/share, is once again an interesting investment opportunity.

Dear readers/followers,

I actually stopped following and writing on Kesko ( OTCPK:KKOYF ) for SA several years back, with my latest article on the company being over 3 years ago at this point. Since that time, Kesko has become one of my all-time successful finish investments - because I sold it when the company's share price hit €32/share at an RoR of over 170% including dividends. This was long ago now - almost 2 years, as it happens.

{kind=link}

Kesko is a very good example of why you, as an investor, should be able to recognize overvaluation, or follow someone who has the ability to recognize overvaluation. As you can see above, what would have happened if I hadn't sold? I would still be at a profitable level, for sure - especially including those dividends - but I would be nowhere close to where I was when I sold. Even if I sold €5/share before the highs, this does not bother me. It was still the right choice.

I made the decision today, to update you on Kesko Oyj because I believe:

- Finnish companies deserve more coverage on SA

- This is a great company, and as of going below €17/share, it has once again become an interesting investment potential.

Let's review what Kesko offers, and why you should consider investing.

Kesko - Plenty to like about Finnish Trading

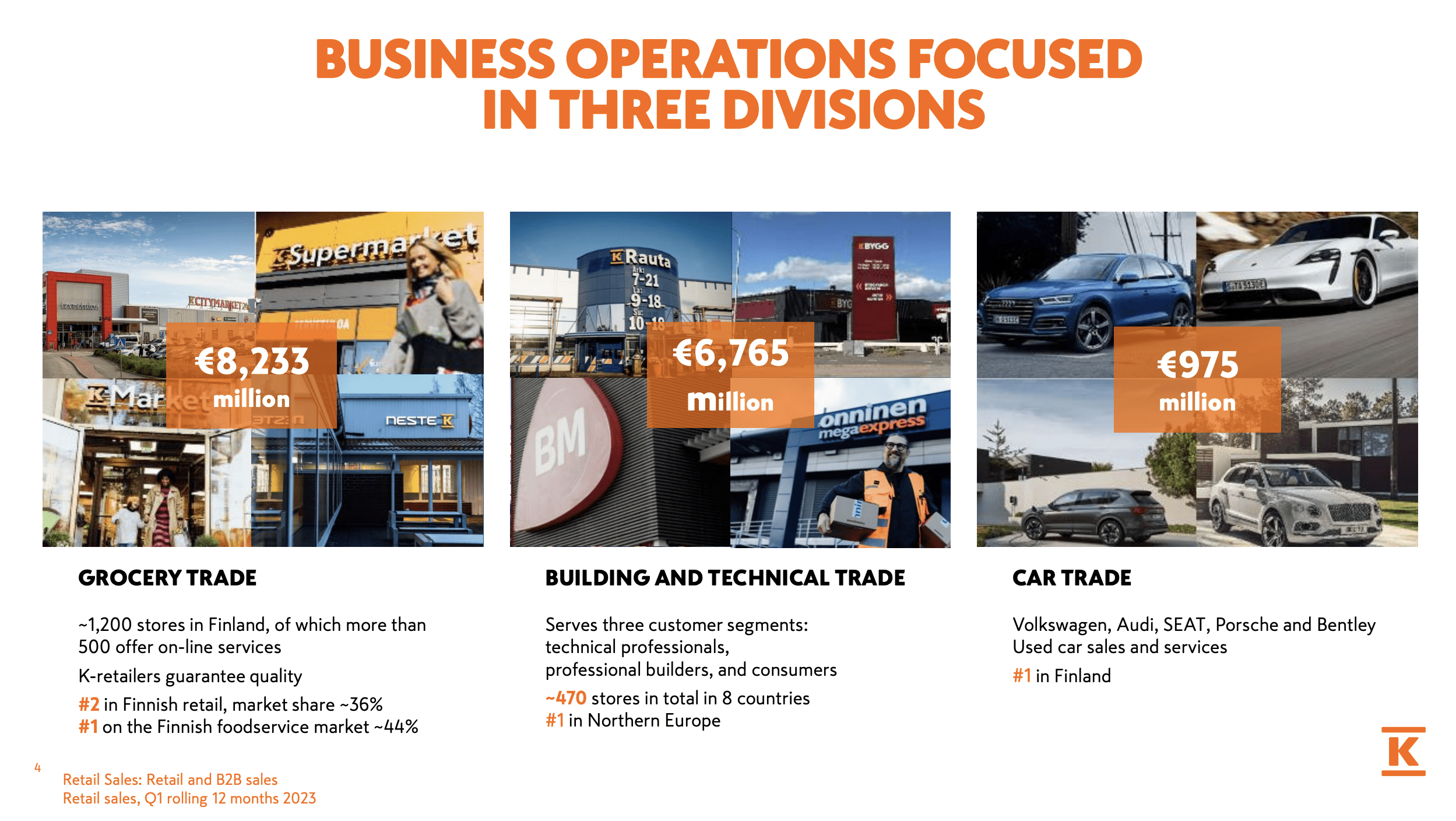

Kesko is what is known as a "trading company", but this gives you the wrong picture. Instead, when you look at Kesko, you should have the following picture in mind, namely that the company covers the very attractive fields of:

- Grocery trade

- Building/Technical trade

- Car trade

Much like the Swedish company ICA, which was taken private over a year ago, Kesko was formed when four wholesaling companies merged during the early 20th century (1940).

The driving force behind this merging was the need to purchase goods for retailers (who became shareholders) and start a larger degree of cooperation between retailers.

This is a Scandinavian model, and Kesko has evolved into a very interesting sort of company - serving small retailers around Finland, to the centralized organization that Kesko and the K-retailers are today. The ambition here was the improvement of an ever-evolving, customer-oriented, and profitable operating model.

The company is the second-largest grocer in all of Finland in terms of both market share and sales. The company's role includes the purchasing of FMCG, selection management, logistics, and the overall development of chain concepts and the ever-growing store network (much like Swedish corp-similar ICA). Kesko manages three sizes of K-food chain stores. But the appeal does not stop there. It's also a market participant in the building/technical trade , and it sells cars and dominates brands like Volkswagen, Audi, Seat, and adjacent attractive brands.

Through its cooperation with VV-Auto and Konekesko, Kesko represents the leading brands in the area and is responsible for sales as well as after-sales services for these vehicles.

{kind=link}

The company also represents Porsche and Bentley in Finland.

Looking at this you might ask yourself how it is even possible for one company to do this in an entire country and an operating area that also includes Norway and Sweden as well as the Baltics.

{kind=link}

I pose to you the following question, dear reader - how could this not be attractive at the right price? You know my investment style. Groceries and things people "need", are the best things you can invest in, as I see it. Kesko checks all of these boxes, and then some. Its exposure to building/cars does give it some infrastructure and economic correlation atypical for an FMCG company - that's part of what we see here - but the bulk of the company is attractive and recession-proof operations which have done well over time - they're just not worth over €30/share.

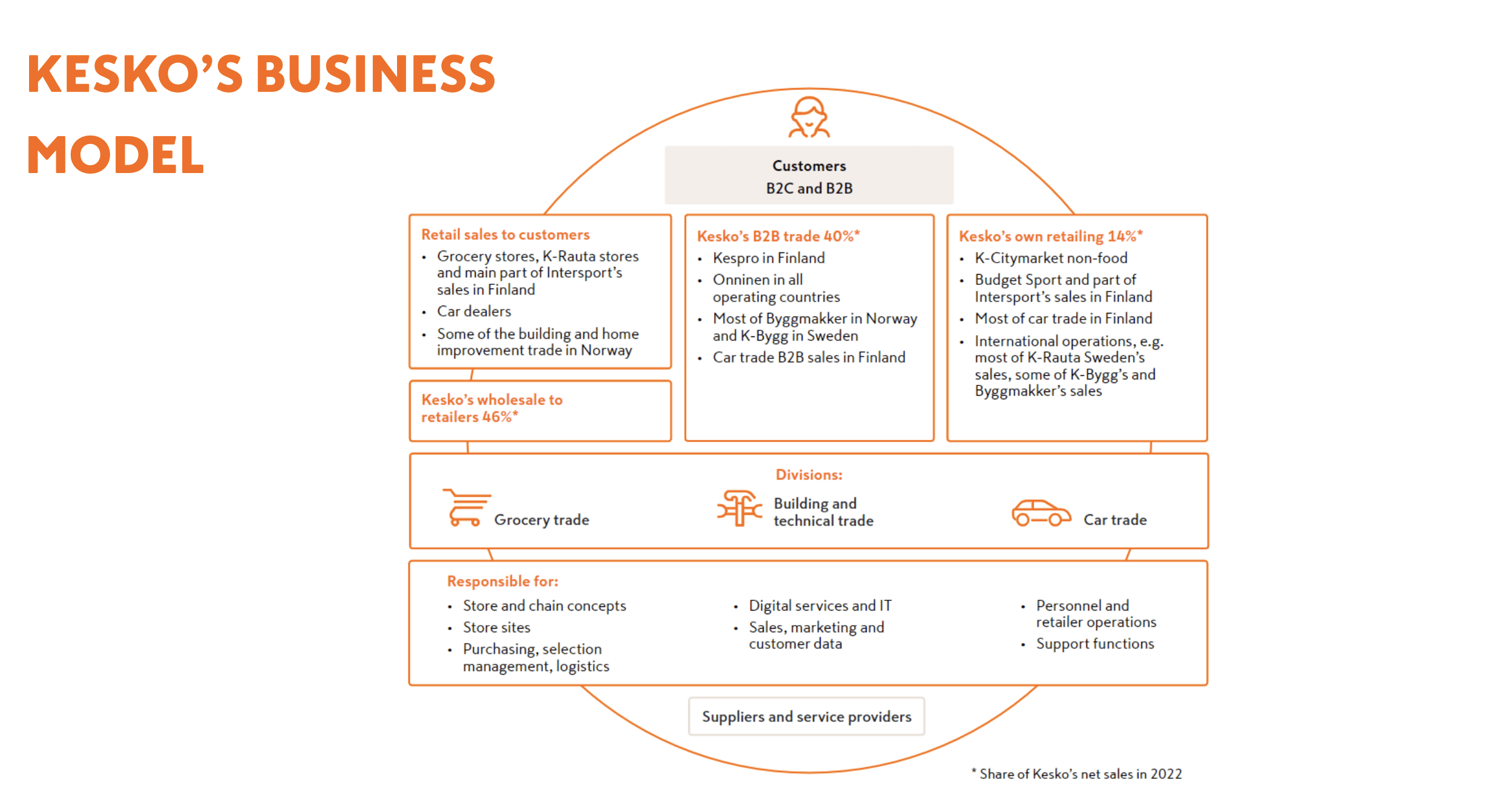

The company serves both B2C and B2B customers, with B2B at about 40% of sales. It's an ecosystem that, once you understand it, is incredibly attractive in terms of its mix of wholesale and retail.

{kind=link}

Over the past few years, the company's growth ambition has been to bring everything under far fewer "flags" than it has been previously - making everything part of the "K" brand. We've previously had brands like KodinYkkönen, Anttila, Musta Pörssi, Konekesko, K-payta, VV-Auto, K-Rauta/Rautia, and various brands of K-markets - that's to be consolidated into no more than 2-5 brands per segment, everything under the company's one level.

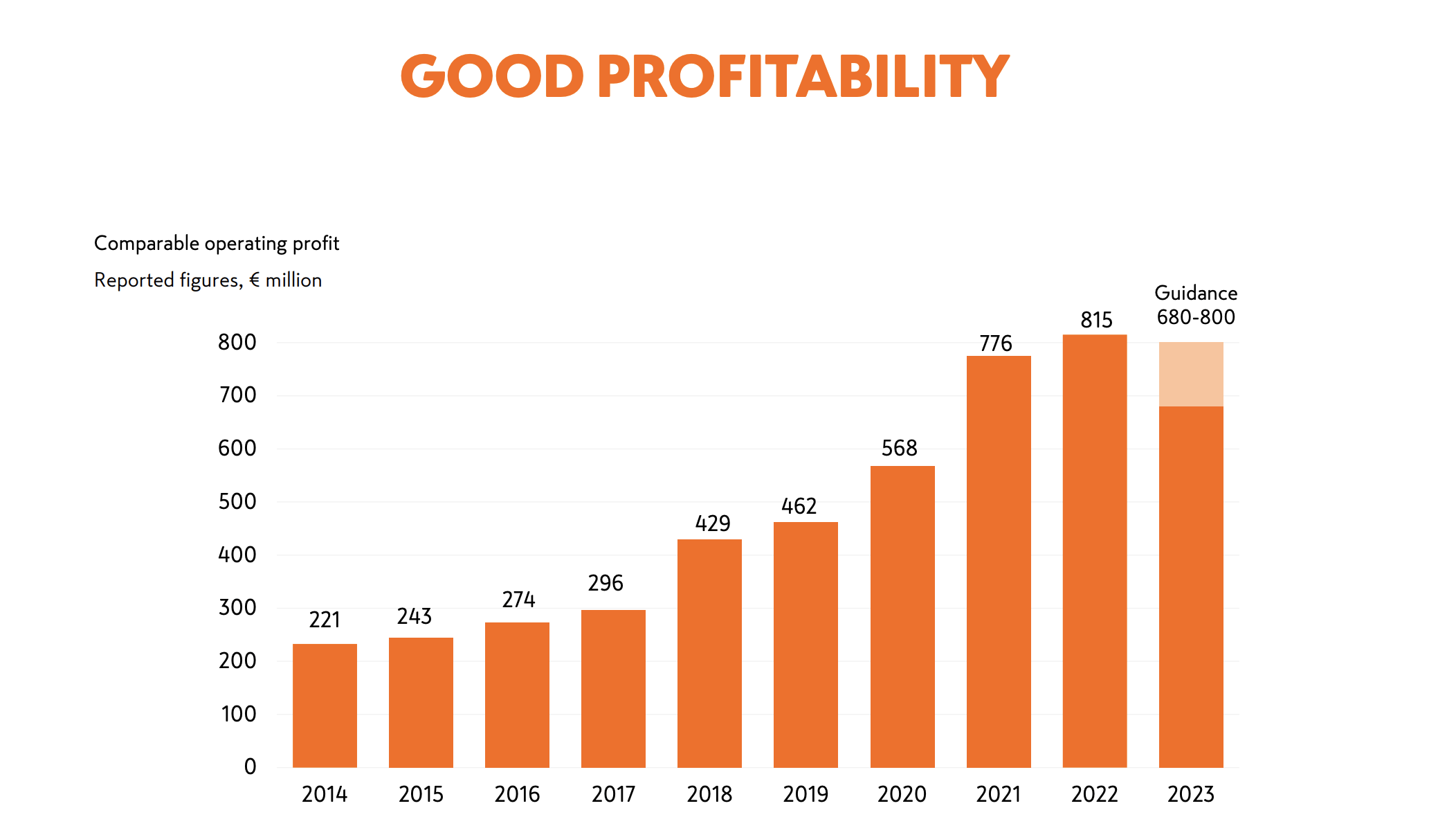

To say that Kesko has "succeeded" would be, as I see it, a gross understatement. The company has been a superb investment and remains a very good operation - the problem has always been valuation, and the market's willingness to assign an ever-higher premium to what are impressive, but not outlandish numbers of sales growth and profitability.

{kind=link}

Kesko remains at a 36% overall market share, and is the largest grocer in terms of its network, in all of Finland. It's also the largest online grocer, and it has 1.6M customers every day. Private labels make up more than 50% share of sales, which is one of the highest numbers you can find among any retailer. It's a leading player in the building trade, with B2B at 80% of sales. It also leads new car sales at 17% of the total and represents some of the most beloved brands in all of Europe.

Future profitability and growth are hampered by its already-extensive market share. It means we're limited mostly to cost efficiencies and improvements rather than expansion into further geographies and areas, which I view as limited and not in the company's current interest. The dividend remains a priority for the company, but I wouldn't count on it growing, going forward. Instead, we might even see a small cut in the payout. However, the company has been steadfast in its commitment to the payout for the past 7 years.

{kind=link}

Despite what I would consider a problematic macro, the company managed 1Q very well. Grocery trade grew, with a particularly strong performance for Kesko, and a 4.4% YoY growth in sales, as well as only a marginal decline in earnings and operating margin, to 4.5%, which is still very much within the framework of acceptability for a grocery company - especially one with Kesko's overall mix.

The company also continues M&A expansion, with the technical wholesale operator Elektroskandia in Norway, together with Zenitec in Sweden, and divested its MAN truck business in Finland, increasing efficiencies and synergies on a forward basis.

ROCE remains positive. Grocery is also at almost 20%, with building and technical trade close to 17.5%. Car is obviously the lowest, but is actually up since 2022, with a nearly 14% ROCE, leading to a group-wide ROCE of over 16% - excellent.

The main risk I view with Kesko is that one of its growth ambitions or project fails does not give the return expected. However, because of a beyond-solid grocery and technical trade backbone that represents a market share of over 35% in very good home geography, I believe anyone saying this company faces fundamental risk understands only a limited amount of what the company "Is" and "does".

The main risk for investment in Kesko is valuation. Kesko has shown an atypical volatility for the FMCG segment, and I was able to pick up shares at below €10/share years ago, leading to portions of my investment having RoR of over 300%+ when I divested the shares.

I now want to show you what Kesko, at this valuation, may offer you.

Kesko - The valuation means that the upside is significant, and safety is massive here.

My investment in Kesko is also personal. I currently work 100 miles north of the arctic circle on a consulting contract, which means that aside from seeing the snow, ice, and reindeer and the few people that live up there, I very often find myself visiting the local K-market and other Kesko brands.

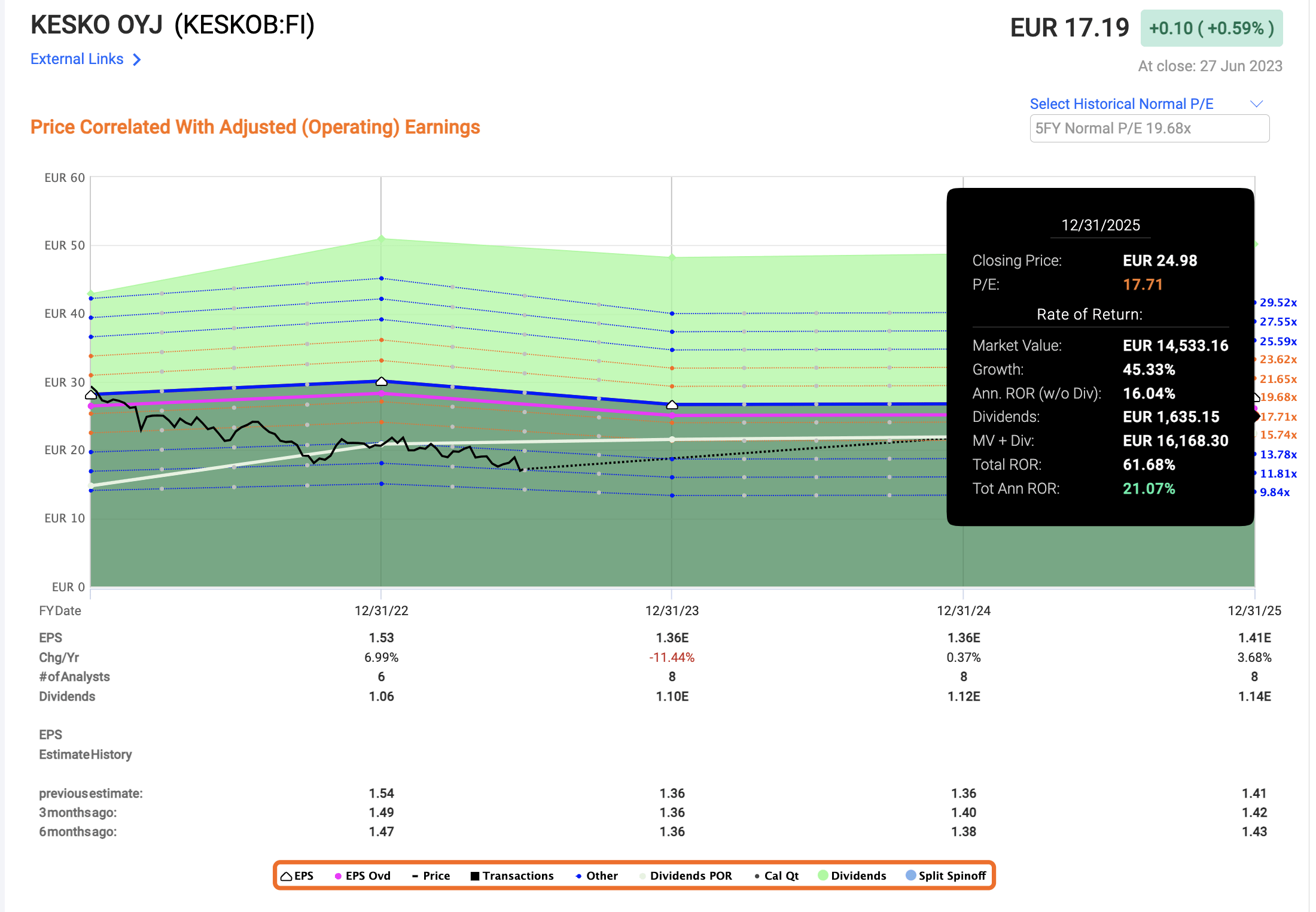

While this company doesn't deserve the 25-28x P/E premium it once held when I sold, I do believe it, like any qualitative grocer deserves a premium - one closer to around 17-19x P/E for the long term. It's currently in a growth slump, expecting a double-digit drop in 2023, followed by flat development for the coming few years.

However, because of the resiliency of the company's operations, I view this premium as more valid than in other companies, so I'm comfortable forecasting up to 18-19x P/E.

{kind=link}

This makes that 21% annual RoR conservative, to my mind. S&P Global analysts would concur with the perspective of undervaluation, putting the company close to my overall target of €22/share, and coming in at €21.5/share. However, I want to note that these same analysts gave the company a €30/share target yet still did not have a "BUY" rating - so take these ratings with a spoonful of salt, as always.

The lowest S&P Global rating target here is €18.5/share, which gives Kesko a significant potential upside.

One could argue that Kesko suffers from risks from competition in all of its segments and that businesses such as home improvement, furniture, building/technical trade, and similar offerings are subject to competition from entrants like Amazon ( AMZN ). However, similar to Sweden, while Amazon is coming/has come, the fundamental change brought about in the USA and other nations has not materialized here. These geographies hold complex labor laws and logistical challenges, and with inflation and cost increases, I do not see a significant danger that e-vendors will be able to push out an incumbent that already has a solid footing in the B2B and wholesale trade to any significant extent.

The risks in the company are therefore relegated, as I see it, to valuation and its growth potential. Growth potential is "easily" discounted using the valuation, and at this price, I view Kesko as having significant potential to outperform, which to me takes away from the risks brought on by the company's growth projects and M&As.

I view Kesko as able to outperform at anything below €20/share, and I view €22/share as a good price target here - so I'm going back in, and I like what I see here.

Here is my new Thesis for Kesko.

Thesis

- Kesko is one of the more interesting grocers in Scandinavia, with its unique combination of cars, grocery, and building trade. I view this combination as inherently attractive, and Kesko as a proven, profitable manager of this mix with the ability to generate above-market returns and attractive dividends. The current yield for the company is above 6%, and I view it likely to stay at that level on a forward basis. Current dividend estimates are even for an increase.

- Based on this, I give Kesko a conservative share price target of €22/share, though the company could easily go as high as €25-€28/share again once its new initiatives and structure are realized.

- Due to that, this company has a double-digit upside, a high yield, and is at a very attractive overall price level.

- I give Kesko a "BUY" rating here.

Remember, I'm all about:

- Buying undervalued - even if that undervaluation is slight and not mind-numbingly massive - companies at a discount, allowing them to normalize over time and harvesting capital gains and dividends in the meantime.

- If the company goes well beyond normalization and goes into overvaluation, I harvest gains and rotate my position into other undervalued stocks, repeating #1.

- If the company doesn't go into overvaluation but hovers within a fair value, or goes back down to undervaluation, I buy more as time allows.

- I reinvest proceeds from dividends, savings from work, or other cash inflows as specified in #1.

Here are my criteria and how the company fulfills them (italicized).

- This company is overall qualitative.

- This company is fundamentally safe/conservative & well-run.

- This company pays a well-covered dividend.

- This company is currently cheap.

- This company has a realistic upside that is high enough, based on earnings growth or multiple expansion/reversion.

I believe the company fulfills all of my targets and criteria here, making it an attractive "BUY".

For further details see:

Kesko: The Upside Is Once Again Here