PBA - Keyera: Earnings And KAPS Pipeline Update

2023-05-22 15:24:24 ET

Summary

- Keyera's share price outperformed Canadian peers Enbridge and Pembina Pipeline over the past six months, holding up well against the sector's downturn.

- Distributable cash flow declined because of weaker results in the marketing segment.

- The KAPS pipeline becoming fully operational in Q3 2023 will be the main thing to look out for.

- The stock isn't more appealing than at the time of my last article. Therefore, I have to reiterate my hold rating.

Author's Note: Since Keyera Corp. is reporting in Canadian Dollars, all numbers refer to Canadian Dollars (unless stated otherwise).

Introduction

This will be an update on my initial article regarding Keyera Corp. ( KEYUF ) ( KEY:CA ). Since my last article (November 22, 2022), Keyera reported earnings for Q4 2022 and Q1 2023 and gave updates regarding the KAPS Pipeline, a project that Keyera itself describes as a game changer for the company.

I want to provide an update regarding the aforementioned earnings reports and the KAPS Pipeline project before giving my take on valuation and a conclusion. Regarding an overview of Keyera's business, I will refer you to my initial article where I described the different business segments and how Keyera earns money.

Performance since the last article

In the conclusion of my last article, I stated that Keyera was fairly valued and should be able to generate 11% long-term returns (7% dividend yield + 4% earnings growth potential). Nevertheless, I rated it a hold because of concerns about higher refinancing costs. I also stated that I would have sold my entire position if the stock reached $35 (US$26) and might have changed my stance to a buy rating if the stock dropped toward $25 (US$18.60).

Since my initial article, Keyera beat the S&P500 by around 210 basis points on a total return basis, as can be seen in the snippet below:

KEY:CA - Performance since last article (Seeking Alpha)

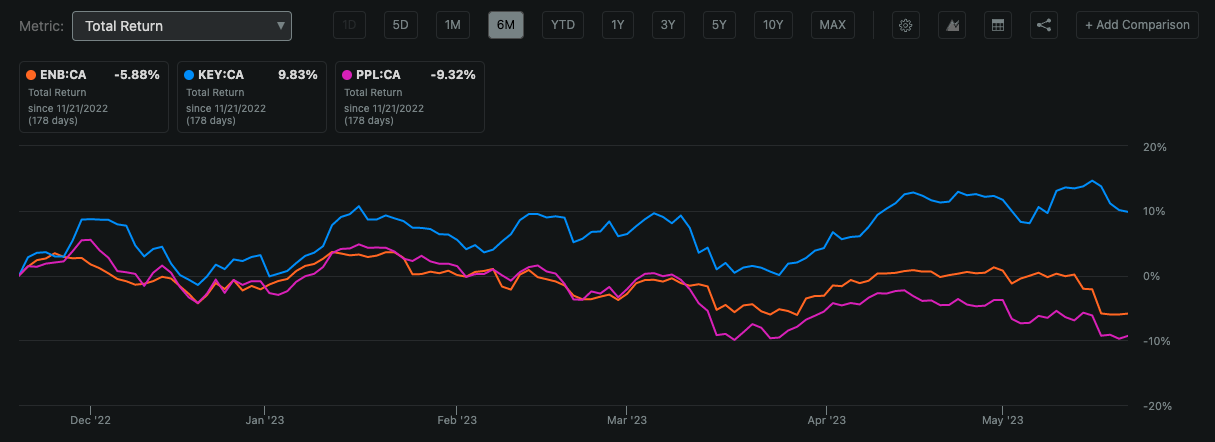

With this performance, Keyera outperformed Canadian peers Enbridge Inc. ( ENB ) ( ENB:CA ) and Pembina Pipeline Corporation ( PBA ) ( PPL:CA ) over the past six months:

Total Return 6M (Seeking Alpha Charting)

{kind=link}

Note that these numbers don't take into account currency effects.

Seeking Alpha Analysts and Wall Street are bullish on Keyera (Keyera isn't covered by SA Quant), as can be seen in the following snippet from Seeking Alpha:

KEY:CA - Seeking Alpha ratings (Seeking Alpha)

Earnings Update

There have been two earnings releases since my last article so I will just throw them together and give an earnings update for the last six months (October 2022 - March 2023) compared to the same period one year ago. I will solely focus on distributable cash flow ((DCF)) because this is the main metric we have to look out for. If we look at it very simplified, DCF is operating cash flow less maintenance capital expenditures ((CAPEX)).

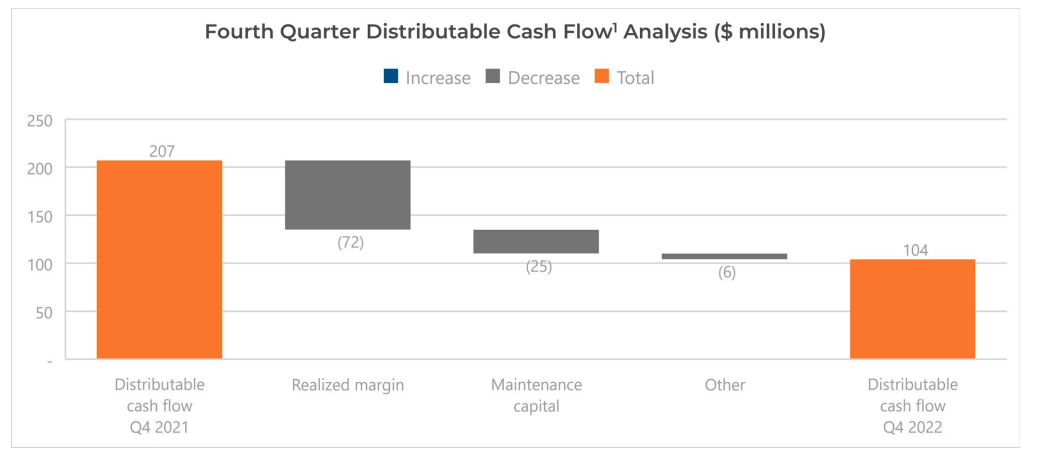

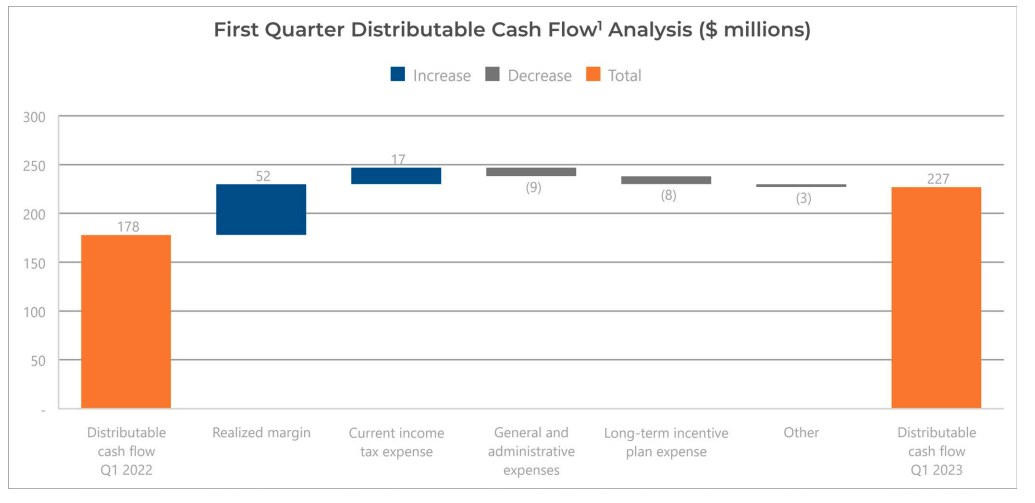

DCF for the past six months amounts to $332 million. In the year-ago six months period, DCF came in at $385 million. So DCF declined by around 14%. Let's see where this decline came from. Here are two charts from the past two earnings reports:

Q4 2022 DCF (Keyera - 2022 Year-End Report) Q1 2023 DCF (Keyera - Q1 2023 Report)

{kind=link}

{kind=link}

We can see that the main changes came from slightly higher maintenance CAPEX and changes in what Keyera calls "Realized margin". Realized margin is defined as operating margin excluding unrealized gains and losses on commodity-related risk management contracts. So realized margin is basically a sort of adjusted EBIT.

In Q1 2023, realized margin grew in all business segments. Gathering & Processing grew by $24 million, Liquids Infrastructure by $14 million and Marketing by $13 million.

In Q4 2022, Gathering & Processing and Liquids Infrastructure were flat while Marketing realized margin declined by $75 million. Here is what I wrote in my initial article regarding Keyera's Marketing segment:

Keyera also purchases and sells products associated with their own facilities. They buy products from their customers through supply arrangements and deliver these to end markets (propane, condensate) or use them on their own in the production of iso-octane at their Alberta EnviroFuels facility (butane). The earnings from the marketing segment depend on commodity prices between the purchase price from the arrangements and the selling prices. Therefore, the marketing segment is much more volatile than the other two segments.

Source: Initial article

Gathering & Processing and Liquids Infrastructure are very stable business segments. If Keyera's earnings are volatile, this volatility likely results from the Marketing segment. This is the nature of the business and as long as declining DCF is only a result of a decline in the Marketing segment's realized margin (as is the case here), I am not concerned at all.

On a trailing twelve ((TTM)) basis, DCF stands at $702 million compared to $756 million at the time of my last article. As I described above, the decline is solely attributable to the marketing segment, partly offset by some growth in the other two segments.

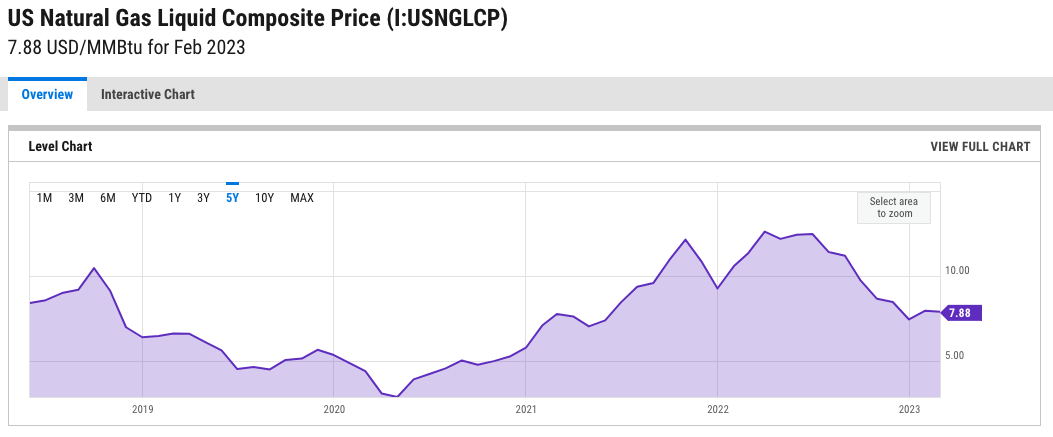

In FY2022, realized margin for the marketing segment came in at a record high of $397 million. In the Q1 2023 report, Keyera guided for FY2023 realized margin for the marketing segment of $350 million at the midpoint. If we take into account that realized margin grew by $13 million as I stated above, there should be some more headwinds ahead for the marketing segment in the upcoming quarters. This makes sense when we look at this chart:

US Natural Gas Liquid Composite Price (YCharts)

{kind=link}

Keyera's marketing segment earns more money when they can buy products for low prices and sell them for a higher price. In our case, Keyera bought at good prices at the end of 2020 and all through 2021 and was able to sell at even better prices in 2022, resulting in a record-high realized margin in the marketing segment. Now that prices are declining, the marketing segment is suffering.

As I stated earlier, this doesn't concern me at all. As long as the other two segments are growing nicely, volatility in the marketing segment is not a problem.

KAPS Pipeline Update

I warranted an extra section for the KAPS Pipeline in my initial article. Here is what I wrote back then:

Keyera describes the KAPS pipeline project as a game changer for the company. KAPS will connect the three northern gas plants (Pipestone, Wapiti and Simonette) to the Fort Saskatchewan area (as can be seen in the above illustrations) and allow Keyera to serve the whole value chain from the gathering systems to the delivery to end markets. More importantly, it will operate on a Take-or-Pay basis, which will make Keyera's cash flows more stable.

Source: Initial article

I also complained that Keyera couldn't conservatively calculate the project's costs because they had to revise estimated costs upwards several times over the past few quarters. In the Q1 2023 report, Keyera announced that the pipeline is now nearing completion. The condensate pipeline system started operations in April and the NGL pipeline is expected to be operational by the end of June. The estimated costs didn't change and remained at $1 billion net to Keyera (50% ownership).

The main thing to look out for is how the KAPS pipeline will affect DCF growth in the upcoming quarters.

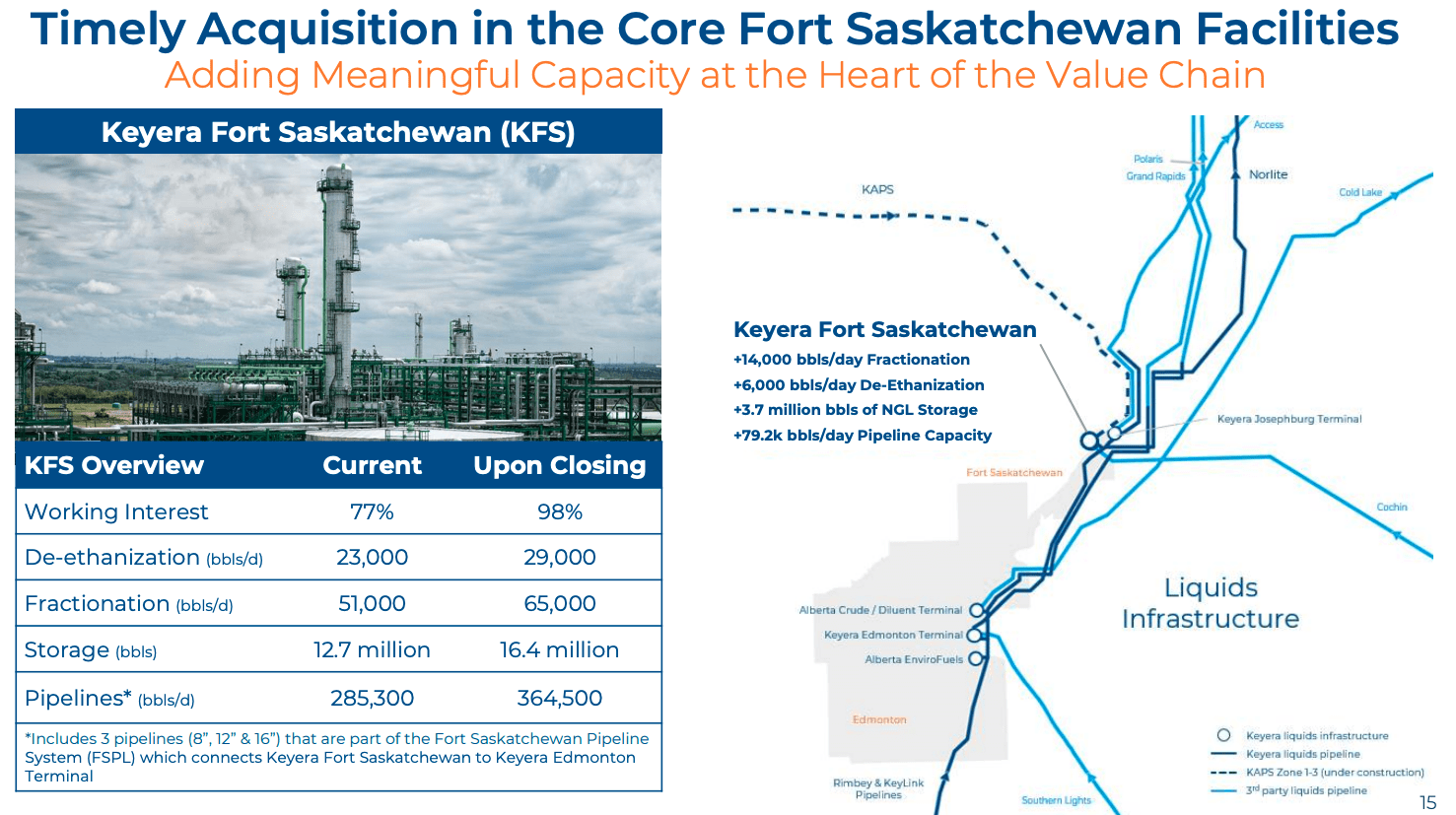

Fort Saskatchewan Transaction

Another deal I want to highlight is the acquisition of 21% additional interest in Keyera Fort Saskatchewan . Keyera bought that interest from Plains All American ( PAA ). Before the deal, Keyera had a 77% interest in KFS. They now upped that interest to 98%. This slide from the current investor presentation shows an overview of the transaction:

KFS Acquisition (Keyera Investor Presentation)

{kind=link}

I like transactions like this because buying additional equity interest when you already own 50%+ (and thus are like to operate the facility) usually comes at low to no additional general and administrative expenses. That makes it more likely that the deal will be accretive.

Keyera paid $365 million and funded the transaction with cash-on-hand, credit facilities and the issuance of 7,070,000 new shares. I would have liked Keyera to fund this without issuing new shares but so be it.

According to Keyera, the price represents around 11x the expected 2023 operating margin and a 9.5x operating margin thereafter. This could be an early hint that Keyera expects strong growth for KFS in FY2024.

Change in dividend policy

This is not important for overall returns but might disappoint income investors. Up to March 2023, Keyera paid a monthly dividend. On February 14, 2023, Keyera announced the transition to a quarterly dividend . From now on, Keyera will pay a quarterly dividend of $0.48 (US$0.36) at the end of March, June, September and December.

Valuation and What to look out for

I will keep this section short. In my last article, I concluded that Keyera was fairly valued and should be able to generate around 11% long-term returns (7% dividend yield + 4% potential earnings growth). Updating the DCF valuation I used in my last article will result in the company looking overvalued at the current price. This is because (a) TTM DCF declined from $756 million to $702 million and (b) the share price increased a bit.

That DCF valuation would be a shot in the dark though because we need to see how the KAPS pipeline going into operation in the second quarter of FY2023 will affect DCF. Another uncertainty is the realized margin for the marketing segment. If we look at the YChart I highlighted earlier, we can see that current NGL prices are at the 5-year average. Assuming that FY2023 should be a weak year because Keyera bought at higher prices at the end of 2021 and throughout 2022, the contribution from the marketing segment should be below average in FY2023 (as Keyera indicated with the marketing segment's guidance range).

As I will reiterate my hold rating on Keyera, I will just state that the company isn't more appealing than at the time of my last article. We will have to wait and see how the KAPS pipeline and NGL prices affect earnings over the next few quarters. Especially the contribution of the KAPS pipeline in Q3 2023 (when the pipeline should be fully operational) will be something to look out for.

Risks

One risk remains unchanged and another risk just came along in the recent past. The unchanged risk is one of higher refinancing costs. I won't repeat myself here and will just refer to my initial article.

The newly arising risk is the possible effect the Alberta wildfires might have on Keyera's business. According to this article from Reuters , the amount of gas flowing from Canada to the U.S. dropped to a 25-month low of 6.4 billion cubic feet per day because wildfires disrupted production. While this shouldn't hit Keyera directly, lower production will affect Keyera's Fee-for-Service cash flows.

I want to highlight that Enbridge lists the "Alberta Forest Fires" from 2017/2018 as one of the big four crises over the past two decades to highlight their low-risk business model, as can be seen in the following snippet from the Q1 2023 earnings presentation:

Highlighted crises (Enbridge Q1 2023 earnings presentation)

Here is Keyera's statement regarding the wildfires in the last Q1 2023 report:

As a precaution, the company proceeded with the safe and orderly shut-in of six gas plants between Thursday, May 4 and Friday, May 5. These are the Brazeau River, Pembina North, Zeta Creek, Cynthia, Nordegg and Wapiti gas plants. All Keyera employees and their families in the affected areas are safe and accounted for.

At this time, the company does not believe the outages will have a material financial impact. Keyera is prepared to restart operations as soon as conditions allow. At the Wapiti gas plant, regulatory approval has been received to restart and the plant is commencing its start-up process.

Source: Keyera Q1 2023 report

While Keyera expects no material financial impact at the time of this report, further comments regarding this topic in the upcoming reports and earnings calls should be closely monitored.

Conclusion

Since my last article, Keyera's TTM DCF declined from $756 million to $702 million. The decline is solely attributable to the marketing segment which is more volatile by nature as I described in this article. The growth in the Gathering & Processing and Liquids Infrastructure segments offset some of the marketing segment's decline. Meanwhile, the share price increased a bit. With the volatility of the marketing segment, the main cash flow drivers for Keyera are the other two segments (Gathering & Processing and Liquids Infrastructure).

For this reason, I decided against updating my DCF valuation because I want to wait and see how the KAPS pipeline which should be fully operational in Q3 2023 will affect the DCF of these two segments.

Besides the impact of the KAPS pipeline on DCF, the potential for higher refinancing costs and the possible financial impacts of the Alberta wildfires are two more of my concerns. There are just too many uncertainties at this point.

With Keyera maybe being fairly valued at best (if we include possible DCF growth from KAPS), I reiterate my hold rating on Keyera. The company's quality is just not high enough to warrant a buy rating when it is not clearly undervalued. I also reiterate my stance regarding potential actions with my own shares: I would probably sell the whole position at around $35 (US$25.93) and might change my stance to a buy rating at around $25 (US$18.52).

For further details see:

Keyera: Earnings And KAPS Pipeline Update