KC - Kingsoft Cloud Reduces Major Customer Dependence Pursues Quality Revenue Growth

2023-10-13 17:45:08 ET

Summary

- Kingsoft Cloud Holdings Limited provides cloud-based services to Asia-based companies.

- The company's revenue continues to decline and operating losses remain high despite efforts to grow AI capabilities and reduce customer dependence.

- The global cloud services market is expected to reach $2.5 trillion by 2031, driving the potential for growth in Kingsoft Cloud.

- I remain Neutral [Hold] on Kingsoft Cloud Holdings Limited stock for the time being.

A Quick Take On Kingsoft Cloud

Kingsoft Cloud Holdings Limited ( KC ) provides Asia-based companies with a variety of cloud-based service offerings.

I previously wrote about KC with a Neutral Hold outlook due to continued operating losses and declining revenue.

While the firm is working to grow its AI system capabilities and is reducing its major customer dependence, revenue continues to decline and operating losses remain high.

Until we see a return to topline revenue growth and a substantial reduction in operating losses, I remain Neutral [Hold] on KC.

Kingsoft Cloud Overview And Market

Hong Kong, China-based Kingsoft was founded to provide Asia-Pacific based organizations with a suite of complementary cloud services as an alternative to their on-premise information technology systems.

The company is led by Vice Chairman and Chief Executive Officer Mr. Tao Zou, who was CEO of Seasun Holdings and has been responsible for the firm's entertainment software business since 2004.

The company's primary offerings include:

-

Compute.

-

Networking.

-

Storage & CDN.

-

Database.

-

Data Analysis.

-

Security.

According to a 2023 market research report by Allied Market Research, the global market for cloud services of all types reached a value of $553 billion in 2022 and is expected to reach $2.5 trillion by 2031.

This represents a forecast of 16.6% from 2022 to 2031.

The primary reasons for this expected growth are the ongoing transition by organizations worldwide from on-premise systems to public, private and hybrid cloud environments and ongoing innovation in cloud system offerings by service providers.

A Frost & Sullivan report paid for by Kingsoft estimated the expected growth of various cloud services sectors in China as shown in the chart below:

Allied Market Research

Kingsoft Cloud's Recent Financial Trends

Total revenue by quarter has continued to drop; Operating income by quarter has remained heavily negative but has improved slightly over the past year.

Seeking Alpha

Gross profit margin by quarter has trended higher, as has Selling and G&A expenses as a percentage of total revenue, although management continues to focus on cost control measures.

Seeking Alpha

Earnings per share (Diluted) have remained materially negative but have come off their worst performance in the middle of 2022.

Seeking Alpha

(All data in the above charts is GAAP).

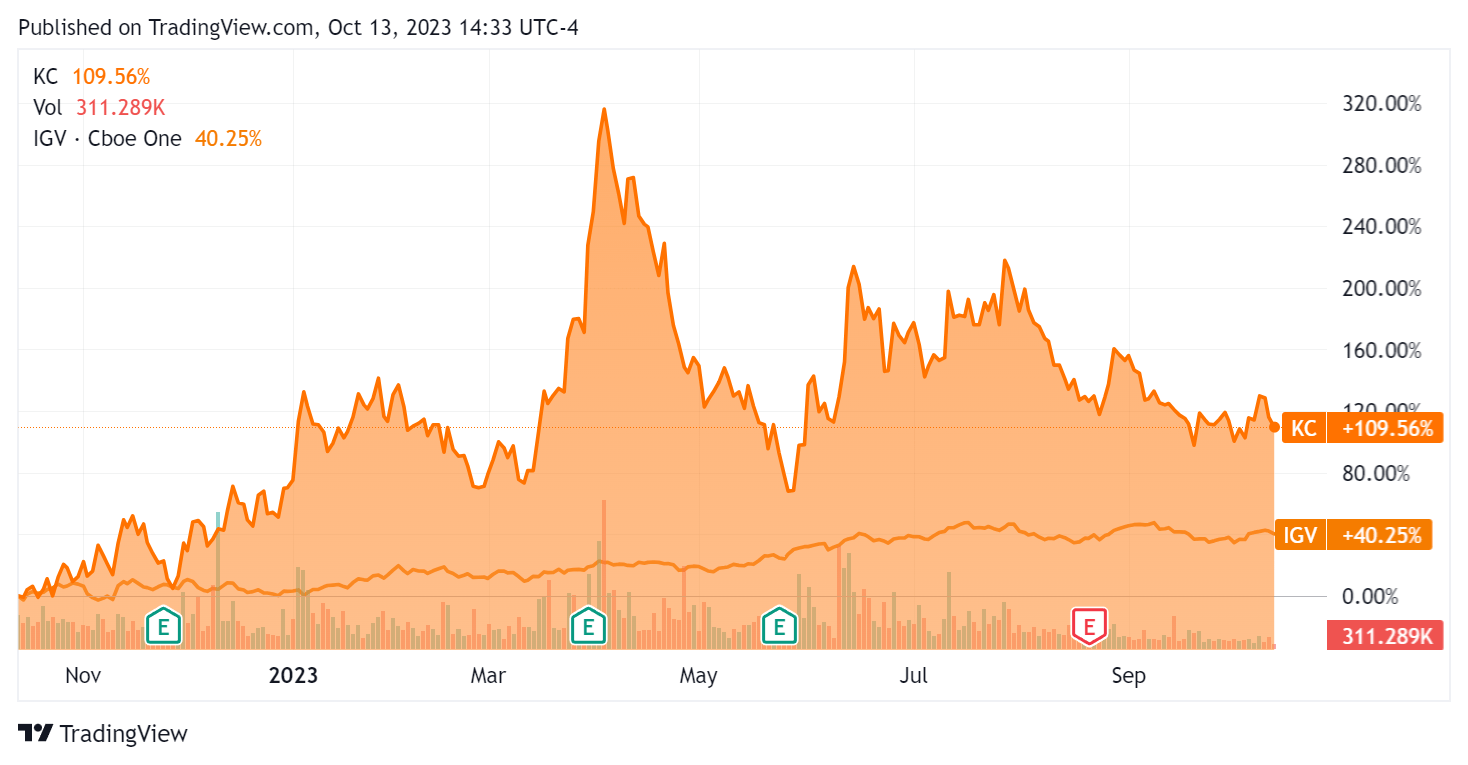

In the past 12 months, KC's stock price has risen 109.56% vs. that of the iShares Expanded Technology-Software ETF's ( IGV ) rise of 40.25%:

{kind=link}

For balance sheet results, the firm ended the quarter with $590.8 million in cash, equivalents and short-term investments and $231.2 million in total debt, of which $195.3 million was categorized as the current portion due within 12 months.

Over the trailing twelve months, free cash used was ($158.9 million), during which capital expenditures were $195.5 million. The company paid $49.6 million in stock-based compensation in the last four quarters.

Valuation And Other Metrics For Kingsoft Cloud

Below is a table of relevant capitalization and valuation figures for the company:

| Measure [TTM] |

| Amount |

| Enterprise Value / Sales |

| 0.8 |

| Enterprise Value / EBITDA |

| NM |

| Price / Sales |

| 1.1 |

| Revenue Growth Rate |

| -14.8% |

| Net Income Margin |

| -30.9% |

| EBITDA % |

| -10.9% |

| Market Capitalization |

| $1,180,000,000 |

| Enterprise Value |

| $897,680,000 |

| Operating Cash Flow |

| $36,550,000 |

| Earnings Per Share (Fully Diluted) |

| -$1.43 |

| Free Cash Flow Per Share |

| -$0.68 |

| SA Quant Score |

| 2.94 - Hold |

(Source - Seeking Alpha).

KC's most recent unadjusted Rule of 40 calculation was negative (25.7%) as of Q2 2023's results, so the firm has performed poorly in this regard, per the table below:

| Rule of 40 Performance (Unadjusted) |

| Q4 2022 |

| Q2 2023 |

| Revenue Growth % |

| -9.7% |

| -14.8% |

| EBITDA % |

| -13.4% |

| -10.9% |

| Total |

| -23.1% |

| -25.7% |

(Source - Seeking Alpha).

Commentary On Kingsoft Cloud

In its last earnings call (Source - Seeking Alpha ), covering Q2 2023's results, management's prepared remarks highlighted its proactive embracing of the AI era in its operations management.

The company has also dropped long-term unprofitable customers.

It has continued to optimize its customer mix, with the signing of "more than 20 new medium-sized customers," so that its largest customer now accounts for only 16% of total revenue.

Total revenue for Q 2023 fell by 11.1% year-over-year, while gross profit margin rose by an impressive 7.9%.

Management didn't disclose any customer or revenue retention rate metrics.

Selling and G&A expenses as a percentage of revenue dropped by 0.3% YoY and operating losses were reduced by 39.3% over the same period.

The company's financial position is only moderate with plenty of liquidity, some debt, but large use of cash in the last four quarters.

KC's Rule of 40 performance has been poor, with revenue decline compounded by high operating losses.

Looking ahead, consensus revenue estimates for full-year 2023 suggest a potential decline of (15.1%) versus 2022's revenue.

If achieved, this would represent a higher revenue decline rate versus 2022's decline rate of (13.74%) over 2021.

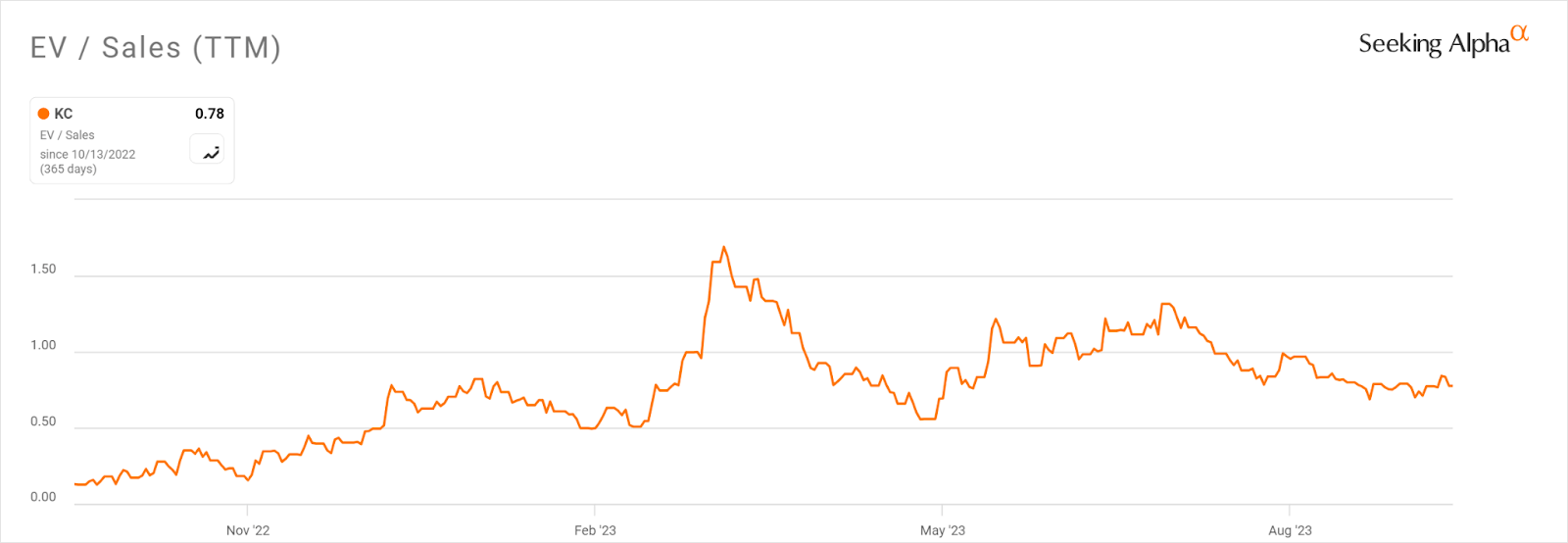

In the past twelve months, the firm's EV/Sales valuation multiple has increased by 5x, as the chart from Seeking Alpha shows below:

{kind=link}

A potential upside catalyst to the stock could include attracting more customers to its various AI initiatives.

The company is working on its ability to assist businesses in AI training and inference business deployment.

However, the timing of generating material revenue from its AI initiatives is likely to be slow in its development.

Until we start to see revenue growth again and a meaningful move toward operating breakeven, I'm Neutral [Hold] on Kingsoft Cloud Holdings Limited shares for now.

For further details see:

Kingsoft Cloud Reduces Major Customer Dependence, Pursues Quality Revenue Growth