KIO - KIO: A 12.15%-Yielding Dynamic Income Fund Worthy Of Purchase

2023-11-30 17:30:38 ET

Summary

- The KKR Income Opportunities Fund specializes in generating a high level of income for shareholders, with a current yield of 12.15%.

- The KIO closed-end fund has performed well over the past few years, with a 12-month return of 21.88% and a three-year return of 17.36%.

- The fund invests in a portfolio of debt securities, including senior loans and high-yield bonds, and employs leverage to boost its effective portfolio yield.

- The fund's balance between junk bonds and floating-rate securities gives it a degree of neutrality between rising and falling interest rates.

- The fund is fully funding its distribution out of NII and trades at a discount.

The KKR Income Opportunities Fund ( KIO ) is a closed-end fund, or CEF, that specializes in generating a very high level of income for its shareholders. The fund certainly manages to accomplish this task fairly well, as its 12.15% current yield is very competitive with similar funds offered by other alternative asset managers:

| Fund |

| Current Yield |

| KKR Income Opportunities Fund |

| 12.15% |

| Ares Dynamic Credit Allocation Fund ( ARDC ) |

| 11.00% |

| Apollo Tactical Income Fund ( AIF ) |

| 11.66% |

| Carlyle Credit Income Fund ( CCIF ) |

| 15.65% |

| Blackstone Strategic Credit 2027 Term Fund ( BGB ) |

| 11.19% |

These funds are all offered by sponsors who tend to be very well known for their private funds, but they certainly do not have the name recognition of PIMCO or another fund house that has run open-ended mutual funds for an extended period of time. However, many of these alternative asset managers are very competent investment houses and as we can see just by looking at the yields of these funds, their strategies appear able to provide investors with a very high level of current income.

The KKR Income Opportunities Fund has performed exceptionally well for a debt fund over the past few years. As we can see here, the fund’s shares are up 7.99% over the past twelve months. However, investors in the fund have actually done even better than that, as the fund has returned 21.88% over the past twelve months when we consider the impact that its distributions have had on its returns:

{kind=link}

The fund’s return over the trailing three-year period is comparably respectable, as it managed to deliver a 17.36% total return to its shareholders despite the share price declining by 12.65% over the period:

{kind=link}

While the three-year return may not impress everybody, when we consider all the market turbulence that has occurred over the period in question, we can clearly see that the fund has managed to hold out very well. This speaks volumes about the overall quality of the fund’s management, and while past performance is no guarantee of future returns, right now there appears to be some reasons for us to investigate further and see if purchasing this fund could make sense today.

About The Fund

According to the fund’s webpage , the KKR Income Opportunities Fund has the primary objective of providing its investors with a very high level of current income. This makes a certain amount of sense, as the fund’s name alone suggests that it is trying to provide its investors with a high level of income. In a few previous articles, I pointed out that many funds that have the provision of income as their primary objective invest in fixed-income securities to achieve that goal. This fund is no exception to this rule, as the description of the fund’s strategy on its website specifically states that it aims to achieve its objectives by investing in a portfolio of debt securities. Here is the description:

KKR Income Opportunities Fund seeks to allocate across credit instruments to capitalize on changes in relative value among corporate credit investments and manage against macroeconomic risks.

The website goes on to state that this fund targets its investments towards both senior loans and high-yield bonds (“junk bonds”). The fact that this fund is investing in junk debt is probably no surprise for those who are somewhat familiar with KKR’s history. Regardless, the fact that this fund invests in both senior loans and junk bonds makes it very similar to a fund like the Ares Dynamic Credit Allocation Fund or the Apollo Tactical Income Fund. I discussed both of these funds in a few recent articles:

- AIF: This 11.33%-Yielding Alternative Credit Fund Is A Winner

- ARDC: A Lot To Offer Income Investors, Regardless Of Interest Rate Direction .

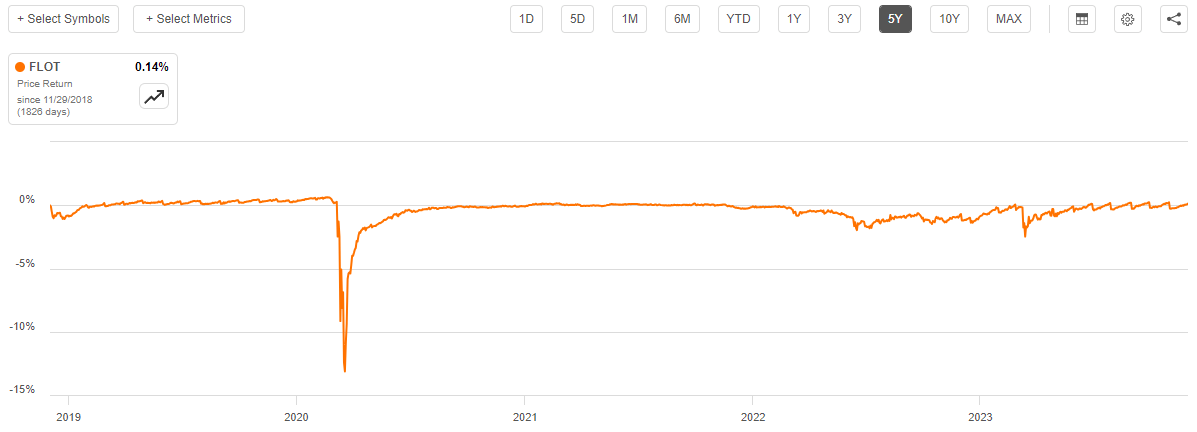

There are some advantages to this strategy of combining senior loans with junk bonds. Perhaps the most important advantage is that it allows the fund to be somewhat interest-rate neutral. After all, floating-rate loans tend to remain relatively stable in terms of price, regardless of any changes in interest rates. We can see this quite clearly by looking at the iShares Floating Rate Bond ETF ( FLOT ), which tracks an index of floating-rate securities. As we can see here, the fund’s share price has not really varied much over the past several years despite the fact that interest rates were all over the place during the period:

{kind=link}

Senior loans are almost always floating-rate securities, so we should expect that the senior loans held by this fund will deliver a similar price performance to what we see in the above chart. This overall stability regardless of changes in interest rates is largely caused by the fact that these securities will always deliver a competitive yield relative to brand-new securities and the market interest rate. This is quite different from ordinary bonds, which see their prices decline when interest rates rise.

According to the website, just under half of the fund’s assets are invested in senior loans and similar assets:

KKR

As we can see, 41.5% of the fund’s assets are invested in leveraged loans. In addition, we see a 5.9% allocation to collateralized loan obligations. Both leveraged loans and collateralized loan obligations are usually floating-rate assets. As such, it appears that approximately 47.4% of the fund’s assets are invested in floating-rate securities. These securities not only exhibit price stability regardless of interest rate changes, but also see their yields increase when interest rates do. As a result, these securities will provide the fund with a rising level of income when interest rates go up. That is something that undoubtedly benefited this fund over the past two years. It will also provide the fund with protection against future interest rate increases, as there are still some people in the market who expect that interest rate increases are much more likely than decreases over the next year, assuming that the economy manages to avoid a recession.

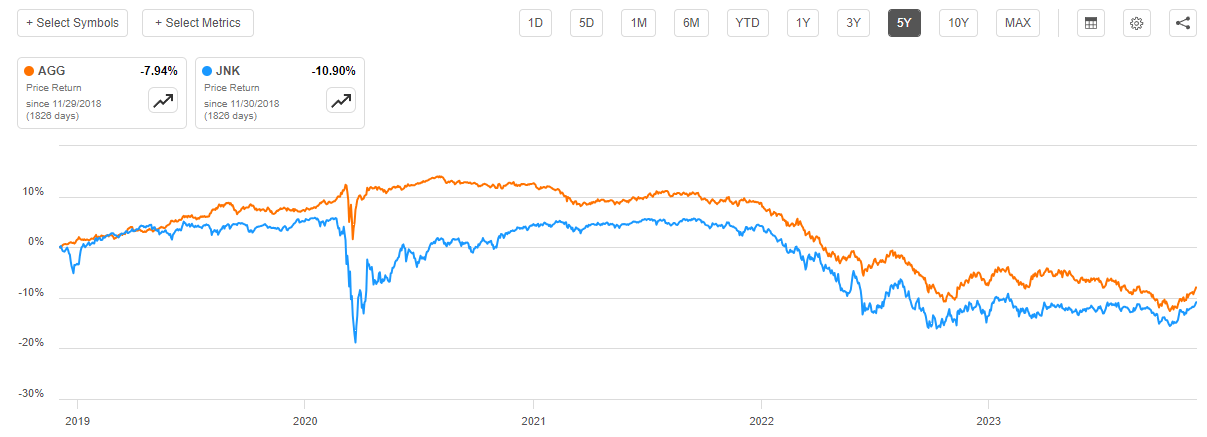

We also see that 51.3% of the fund is invested in high-yield bonds, and another 0.1% of its assets are invested in preferred stock. These two securities will benefit from price appreciation if interest rates decline over the next year, as the market currently expects. After all, we can see here that the Bloomberg U.S. Aggregate Bond Index ( AGG ) and the Bloomberg High Yield Very Liquid Index ( JNK ) were generally increasing over most of 2020 and 2021 as the Federal Reserve kept interest rates low:

{kind=link}

It was not until the central bank began raising interest rates in earnest starting in early 2022 that we really started to see bond prices decline. We can also see that both of these indices have started to rise again over the past few weeks. That is being caused by the market’s expectation of lower interest rates in 2024. The KKR Income Opportunities Fund should be able to benefit from falling interest rates if indeed they do decline significantly over the next year (the market is currently expecting 125 basis points of cuts by the end of 2024).

The future outlook for interest rates is quite uncertain right now. The most recent minutes from the Federal Reserve seem to imply that there is no real chance of 125 basis points of cuts unless the economy enters a severe recession by March. However, the median prediction being put forward by the members of the Federal Open Market Committee is a single 25-basis point cut to the federal funds rate by the end of 2024. In such an uncertain environment, it could help investors to sleep better knowing that they are reasonably well-positioned regardless of what happens with interest rates. As is the case with both the Ares Dynamic Credit Allocation Fund and the Apollo Tactical Income Fund, the KKR Income Opportunities Fund appears to be positioned to perform well regardless of what direction and magnitude the changes of interest rates in 2024 actually are. That is a pretty good position to be in right now.

As I have pointed out in various previous articles, both senior loans and junk bonds tend to be backed by companies with less-than-stellar credit. In the case of junk bonds, this should be fairly obvious as a company with a stronger balance sheet and overall financial profile would carry an investment-grade rating. In the case of senior loans, which are typically floating-rate securities, the interest rate risk is on the issuing company and not on the purchaser of the security. It is unlikely that companies that are capable of issuing investment-grade credit would willingly take on that interest rate risk themselves. After all, it is much better for long-term financial planning for debt to be at a fixed rate so that the company knows well in advance how much it will have to send out in debt payments during a certain period of time. As a result of this, we can expect that most of the securities held by the KKR Income Opportunities Fund will be speculative-grade securities. This is indeed the case, which we can clearly see here:

KKR

An investment-grade security is anything rated BBB- or higher. As we can see, that only describes 2.5% of the fund’s assets. The rest of the securities in this fund’s portfolio are junk bonds of various types and degrees. This is something that may concern those investors who are seeking a safe investment to put into their portfolio. After all, we have all heard about how junk bonds have a much higher risk of losses due to defaults than investment-grade securities. Indeed, Moody’s Investor Service expects that the default rate for American junk bond issues will be 5.6% in January 2024 before falling to 4.6% in August of the same year. That is substantially higher than the default rate of investment-grade securities. Investors who are worried about the preservation of principal, which is a category that likely includes many retirees, will probably be concerned about this as they do not want to suffer from the potential losses that could accompany such a situation.

However, we can see above that 48.3% of the fund’s assets are invested in securities that are rated either BB or B by the major credit agencies. According to the official bond ratings scale , companies whose debt offerings carry one of these two ratings do have sufficient financial strength to carry their current outstanding debt and will likely be able to continue to carry such debt even in the event of a short-term economic shock. As most economic shocks are relatively short-term, this should mean that the fund is unlikely to suffer too much from defaults, but it will certainly not be immune considering that this fund does have higher exposure to CCC and lower debt than some of the other junk bond funds that we have discussed in previous articles. Fortunately, though, the KKR Income Opportunities Fund has 146 current holdings, which should mean that the fund does not have an outsized portion of its portfolio exposed to any individual asset.

That is indeed the case, which we can see by looking at the largest positions in the fund. Here they are:

KKR

This fund is certainly a bit more concentrated in its largest positions than some of the other fixed-income funds that we have discussed in the column over the past year or so. However, we can still see that no individual asset accounts for an excessive proportion of the fund’s assets. As such, any default will probably not have a large enough impact on the fund as a whole for us to even notice the losses, particularly when we consider that both junk bonds and floating-rate securities are yielding a lot more than 3.8% right now. As such, we probably do not need to worry too much about the losses that the fund could suffer in the event of a default. The fact that it does have its ten largest issuers accounting for 26% of the fund’s assets does unfortunately mean that we cannot be too cavalier about its default risk either, though. In particular, investors may want to keep an eye on some of these companies so that they can be sure that they are comfortable with their finances before making an investment in the fund.

Leverage

As is the case with most closed-end funds, the KKR Income Opportunities Fund employs leverage as a method of boosting its effective portfolio yield beyond that of the underlying assets in the fund. I have discussed how this works in various previous articles. To paraphrase myself:

In short, the fund is borrowing money and using that borrowed money to purchase floating-rate loans and other fixed-income assets. As long as the purchased assets have a higher yield than the interest rate that the fund has to pay on the borrowed money, the strategy works pretty well to boost the effective yield of the portfolio. As this fund is capable of borrowing money at institutional rates, which are considerably lower than retail rates, that will usually be the case.

However, the use of debt in this fashion is a double-edged sword. This is because leverage boosts both gains and losses. As such, we want to ensure that the fund is not employing too much leverage, as that would expose us to too much risk. I generally do not like to see a fund’s leverage exceed a third as a percentage of its assets for this reason.

As of the time of writing, the KKR Income Opportunities Fund has leveraged assets comprising 31.93% of its portfolio. That is a very reasonable level of leverage that is either in line with or better than the fund’s peers. It is also below the one-third level that I normally like to see, although a fund like this can probably carry a higher level of leverage due to the lower volatility of its assets relative to an equity closed-end fund. Overall, the risk-reward balance here is probably fine and we should not really need to worry about this fund’s leverage too much.

Distribution Analysis

As mentioned earlier in this article, the primary objective of the KKR Income Opportunities Fund is to provide its investors with a very high level of current income. In order to achieve this goal, the fund purchases a variety of floating-rate leveraged loans and junk bonds, both of which tend to have high-interest rates in the current market environment. The fund collects all the money that it receives from the debt securities in its portfolio and even uses leverage to purchase more securities than it otherwise could based on its assets. That leverage effectively boosts the yield that the fund is able to generate from its net assets. The fund then pays out all of the money that it generates through these operations to its shareholders, net of the fund’s expenses. When we consider the nature of the securities that are providing income for the fund, we can expect that this will result in the fund’s shares having a very high yield as well.

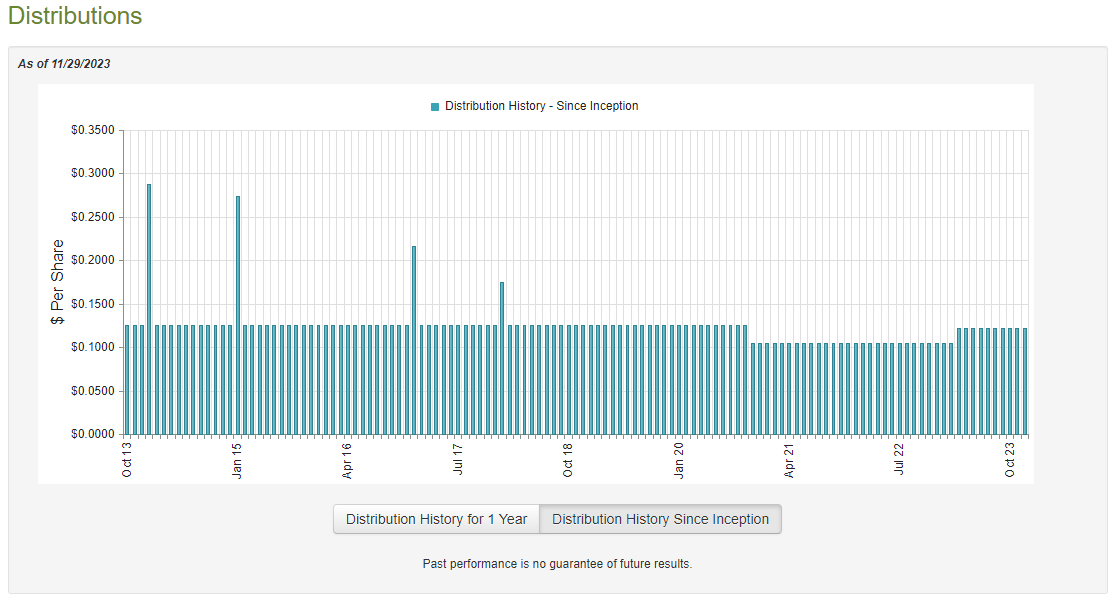

This is certainly the case, as the fund currently pays a monthly distribution of $0.1215 per share ($1.4580 per share annually), which gives it a 12.15% yield at the current price. This fund has generally been pretty consistent with its distribution over the years, although it has not been perfect as it was forced to cut the payout in response to the pandemic:

{kind=link}

This actually makes this fund one of the few debt funds that was actually forced to cut its payout in response to the COVID-19 pandemic and the incredibly low-interest rates that dominated in 2021. After all, that incredibly low interest-rate environment was quite good for the value of most fixed-income assets. We did see a number of fixed-income funds cut their distributions in 2022 due to the rising-rate environment, but as we have already seen, this fund should not be as adversely affected by a rising rate regime as those funds that invest solely in fixed-rate securities.

With the exception of this brief period of paying out a lower distribution, the KKR Income Opportunities Fund has proven to be remarkably consistent over the past decade and it will probably still be reasonably appealing to those investors who are seeking to earn a high safe and secure level of income that can be used to pay their bills or finance their lifestyles.

As I have pointed out a few times in the past though, the fund’s past history is not necessarily the most important thing for anyone who is considering purchasing the fund’s shares today. After all, anyone who is buying the fund right now will receive the current distribution at the current yield and will not be affected by any actions that the fund has had to take in the past.

Unfortunately, we do not have an especially recent document that we can consult for the purpose of our analysis. As of the time of writing, the fund’s most recent financial report corresponds to the six-month period that ended on April 30, 2023. This is a bit disappointing because this report will not include any information about how the fund’s portfolio has performed over the past six months. This is a period that has included a very euphoric market in which investors were aggressively bidding up both stocks and bonds in anticipation of rate cuts later this year. Obviously, those rate cuts never transpired, but the fund may have still had the opportunity to make some profits if that caused the prices of its junk bonds to go up. The past seven months also included a period of time during which interest rates were rising rapidly and bond prices were generally falling. As such, the past seven months have certainly tested the fund’s ability to handle itself in any interest-rate environment, which is exactly the reason why we are considering purchasing its shares. It would have been nice to see how well it actually performed.

During the six-month period, the KKR Income Opportunities Fund received $22,378,386 in interest from the assets in its portfolio. When we combine this with a small amount of income that was received from other sources, the fund reported a total investment income of $23,086,014 during the period. The fund paid its expenses out of this amount, which left it with $16,263,936 available for shareholders. That alone was sufficient to cover the $15,133,194 that the fund paid out in distributions during the period. As such, it appears that this fund is simply distributing its net investment income to its shareholders, which is what we normally like to see with any closed-end fund that invests in debt securities. Overall, this fund’s distribution should be reasonably dependable as long as it can keep its net investment income at the current level.

Valuation

As of November 29, 2023 (the most recent date for which data is available as of the time of writing), the KKR Income Opportunities Fund has a net asset value of $12.90 per share but the shares only trade for $12.02 each. This gives the fund’s shares a 6.82% discount on net asset value at the current price. This is a discount, but it is much worse than the 10.06% discount that the shares have had on average over the past month. Thus, it may be possible to obtain a more attractive entry price by waiting a bit before buying in. With that said though, this fund is still trading at a discount, so the current price is not horrible.

Conclusion

In conclusion, the KKR Income Opportunities Fund appears to be a good alternative to an ordinary fixed-income closed-end fund. As is the case with some of its peers, this fund is fairly well positioned to take advantage of both rising and falling interest rates, which is desirable right now considering that nobody can predict with any degree of accuracy where interest rates are heading. The fund’s distribution is fully covered by net investment income and its valuation is reasonable, so overall it could be worth considering for purchase.

For further details see:

KIO: A 12.15%-Yielding Dynamic Income Fund Worthy Of Purchase