KIO - KIO: Fully Funded 12.4% Yield But Shrinking NAV

2023-07-28 08:01:43 ET

Summary

- KKR Income Opportunities Fund offers a generous 12.4% distribution yield, funded by net investment income.

- KIO invests in risky credit markets, leading to perennial losses on its portfolio and reducing average annual total returns to only 7.2% and 3.2% over 3 and 5 years.

- The author would avoid investing in 'return of principal' funds like the KIO.

The KKR Income Opportunities Fund ( KIO ) is one of KKR's offering in the closed-end fund ("CEF") space. KIO's main attraction is a very generous 12.4% distribution yield that is fully funded by net investment income.

At first glance, KIO's value proposition is very attractive, especially for retirees who like to invest for yield. However, looking under the surface, we see that the KIO fund, like peer funds offered by other private equity sponsors, invests in the riskiest corners of the credit markets in order to generate those high NIIs. This often leads to the KIO fund suffering perennial realized and unrealized losses on its portfolio, which reduces average annual total returns to a more pedestrian 7.2% and 3.2% over 3 and 5 years, respectively.

In the long run, investors in amortizing 'return of principal' funds like the KIO may end up with losses in both principal and income. If it sounds too good to be true, it probably is. I would personally avoid the KIO.

Fund Overview

The KKR Income Opportunities Fund is a closed end fund ("CEF") that focuses on delivering high current income from a portfolio of high-yield bonds, leveraged loans, and other credit instruments.

The KIO fund has $335 million in net assets as of March 31, 2023 and charged a 3.56% net expense ratio in fiscal 2022.

Portfolio Holdings

Figure 1 shows the sector allocation of the KIO fund. The fund has 52.4% invested in high-yield bonds, 44.1% invested in leveraged loans, and 2.1% invested in collateralized loan obligations ("CLOs") as of March 31, 2023.

Figure 1 - KIO sector allocation (kkrfunds.com)

KIO's investments are primarily on the lower-end of the credit quality spectrum, with the biggest weights around single-B credits (37.8% across B-, B, and B+), and CCC credits (42.2% across CCC-, CCC, and CCC+). The KIO fund also has a sizeable allocation to unrated securities (Figure 2).

Figure 2 - KIO credit quality allocation (kkrfunds.com)

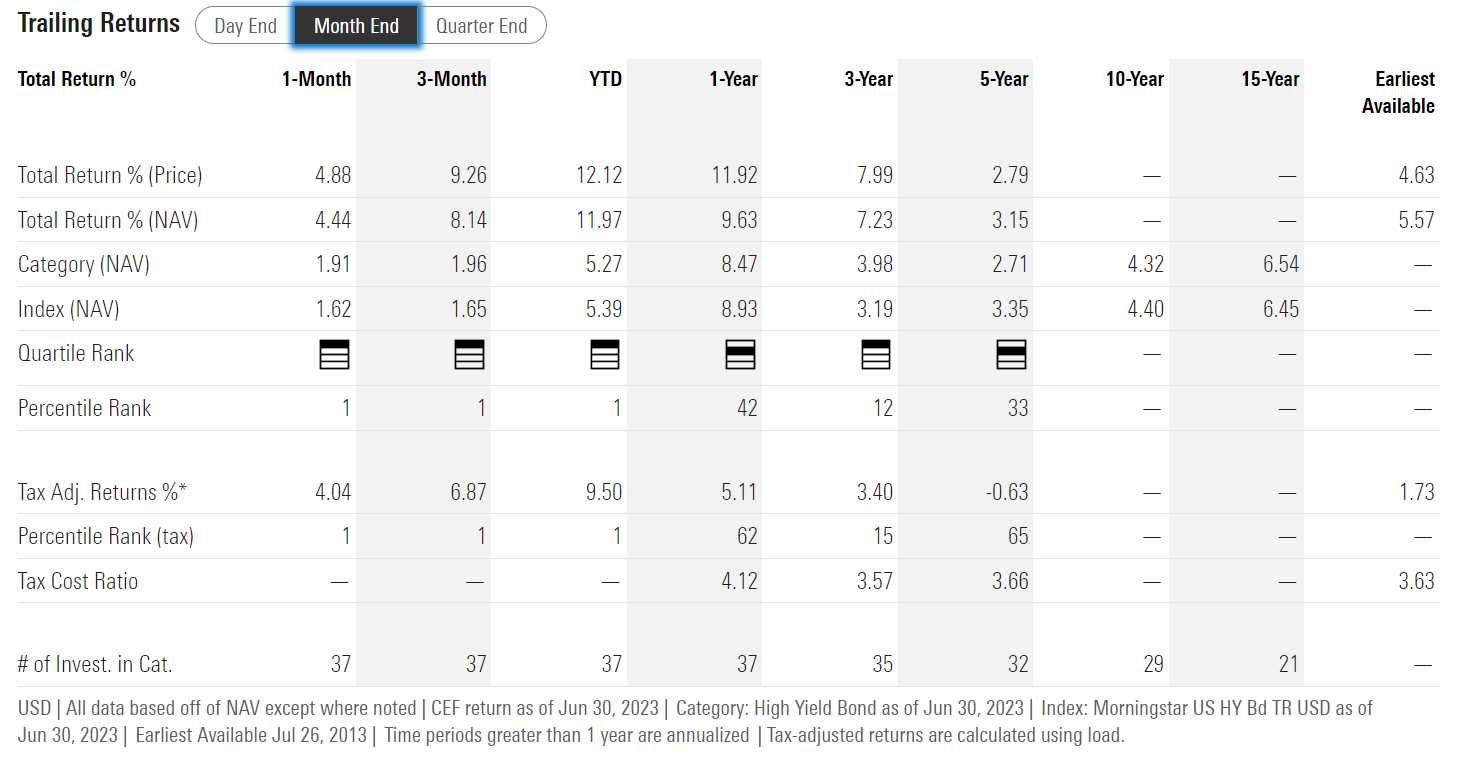

Returns

Figure 3 shows the KIO fund's historical returns. The KIO fund has generated modest long-term returns, with 3 and 5Yr average annual returns of 7.2% and 3.2% respectively to June 30, 2023. Since inception, average annual returns have been better, at 5.6%.

Figure 3 - KIO historical returns (morningstar.com)

{kind=link}

Distribution & Yield

The KIO fund pays a high monthly distribution, with the current monthly distribution set at $0.1215/share. This implies a forward yield of 12.4% on market price or 11.8% on its most recent March 31, 2023 NAV of $12.38 (Figure 4).

Figure 5 - KIO has a 12.4% distribution yield (Seeking Alpha)

{kind=link}

KIO's distribution has been raised recently in March 2023 to reflect higher investment income from the floating rate leveraged loans in its portfolio. (Figure 5).

Figure 5 - KIO historical distributions (Seeking Alpha)

{kind=link}

Generous Distribution Well Funded From NII

Historically, KIO has funded its distributions from net investment income ("NII") (Figure 6). There is no reason to believe that will not be the case going forward.

Figure 6 - KIO distribution funded with NII (KIO annual report)

{kind=link}

While Distribution Is Fully Funded, Something Doesn't Add Up

While KIO is able to fully fund its distribution via NII, sharp-eyed readers should have noticed a discrepancy between the fund's distribution yield (>12%) and its historical average annual return of 7.2% and 3.2% over 3 and 5 years.

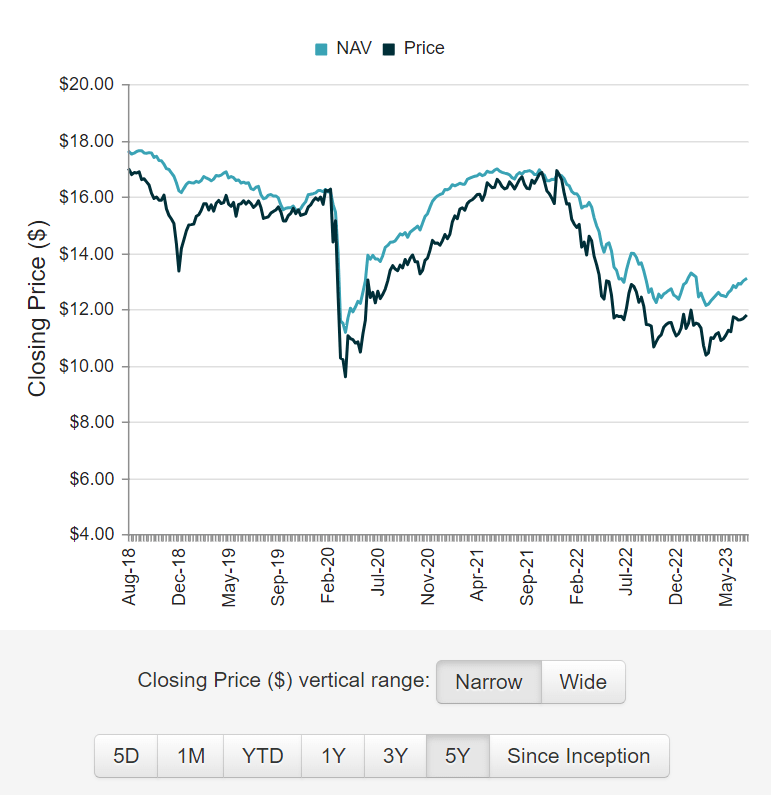

Funds that pay distribution yields higher than total returns are called ' return of principal ' funds. These funds are characterized by a declining NAV, as they generally pay out more than they earn (Figure 7).

Figure 7 - KIO has a declining NAV profile (cefconnect.com)

{kind=link}

What is tricky about the KIO fund and private-equity sponsored peers like the Apollo Tactical Income Fund ( AIF ) and the Blackstone Strategic Credit Fund ( BGB ) is that it is not apparent at first glance that there is anything amiss. These funds earn NII well in excess of their distributions, so from a tax accounting perspective, these funds are not return of capital ("ROC") funds.

However, if we think about the nature of credit investments, a portfolio of prudently selected credit investments should pay out at par less any defaults if it is held to maturity. However, if we study the financial statements of the KIO fund (Figure 6 above), we see that the fund has suffered cumulative realized/unrealized losses of $4.95/share from fiscal 2018 to fiscal 2022. The string of realized/unrealized losses is the primary driver of the KIO fund's decline in NAV shown in Figure 7.

So although the KIO fund was able to generate sufficient NII to cover its distribution, the NII came at the expense of portfolio losses. This leads me to suspect the investments used to generate these high investment yields were very speculative and may have led to permanent losses of capital.

Note credit losses do not have to be solely from a company going bankrupt. A credit investment can suffer credit losses if the credit rating is downgraded (i.e., credit spread widens). Since the KIO fund primarily invests in the riskiest corners of the credit markets (single-B, CCC, and unrated credit investments), there is a very high likelihood of the fund suffering large credit losses even during normal market environments.

Conclusion

The KKR Income Opportunities Fund pays investors a very high distribution yield from a portfolio of speculative leveraged loans and high-yield bonds. The KIO fund is currently yielding 12.4% on market price.

Although the KIO fund's distribution is very attractive and is fully funded from NII, investors need to be cognizant of the fact that the KIO fund has a long-term average annual return of only 7.2% and 3.2% over 3 and 5 years respectively. This suggests that in order to generate the high portfolio NII, KIO's portfolio suffers high realized/unrealized losses.

Investors should look beyond the large headline distribution yield and consider whether the returns profile, high yield but large NAV losses, is what they are comfortable with.

Over the long run, investors in amortizing 'return of principal' funds like KIO tend to suffer both a loss of principal (since market price tracks the decline in NAV) and a loss of income (with less NAV/unit, eventually the fund cannot sustain its high distributions). I would personally avoid the KIO.

For further details see:

KIO: Fully Funded 12.4% Yield But Shrinking NAV