KIO - KIO: The 13.49% Yield Is Fully Covered But The Fund Is Cheap

2023-05-17 17:05:45 ET

Summary

- Investors are in desperate need of income today due to the rapidly rising cost of living.

- KKR Income Opportunities Fund invests in a portfolio of floating-rate securities and junk bonds in order to provide investors with a very high yield.

- The KIO closed-end fund has underperformed most bond indices over the past year.

- The 13.49% is fully covered by net investment income.

- The fund is currently trading at an incredibly large discount to the net asset value.

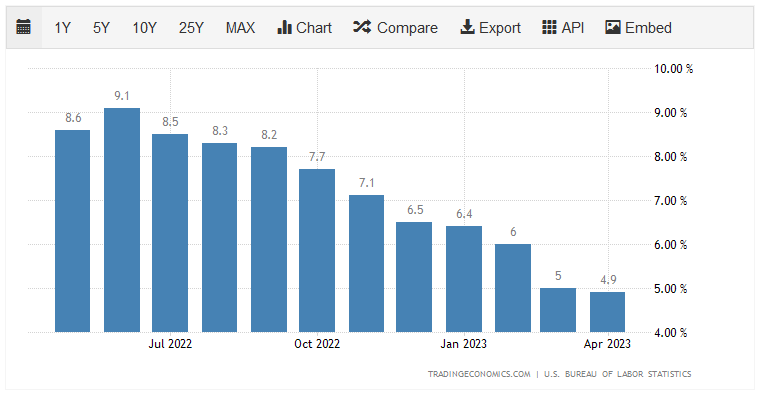

There can be very little doubt that one of the biggest problems facing average Americans today is the incredibly high inflation prevailing throughout the economy. This is clearly evidenced by the consumer price index, which theoretically measures the changes in the prices of goods purchased by an average person. As we can see here, there have been only two months out of the last twelve in which the consumer price index did not increase by at least 6% year-over-year:

{kind=link}

While the reported inflation rate has been coming down in recent months, this is somewhat misleading as it is caused mostly by falling energy prices. I pointed this out in a recent blog post . As inflation has been primarily centered on food and energy, which are generally considered to be necessities, people cannot simply avoid it by postponing or canceling planned purchases. Thus, this inflation has had a very devastating effect on people of lesser means, who have been forced to take on second jobs or enter the gig economy in order to obtain the extra money that they need to keep their families fed and warm.

As investors, we are by no means immune to this, as we need to buy various goods and services too. Thus, we need extra income to maintain our lifestyles, which have already taken a hit from the challenging market conditions over the past eighteen months. We do not necessarily have to resort to taking on a second job in order to obtain this extra money, though. After all, we have the ability to put our money to work for us to earn an income. One of the best ways to accomplish this is to purchase shares of a closed-end fund, or CEF, that specializes in the generation of income. These funds are unfortunately not very well-followed in the media, so it can be difficult to obtain information on them. This is a shame as they have a number of advantages over more familiar open-ended and exchange-traded funds. One of these advantages is that they can employ certain strategies that allow them to earn a higher yield than any of the underlying assets.

In this article, we will discuss the KKR Income Opportunities Fund (KIO), which is a closed-end fund that can be used to earn an income. As of the time of writing, the fund yields a whopping 13.49%, which will undoubtedly appeal to any income-seeking investor. Generally, anything that achieves a yield this high is perceived by the market as being in danger of a near-term distribution cut though, so we will want to pay special attention to this. Thus, let us investigate the fund and see if it could be a worthy addition to an investment portfolio today.

About The Fund

According to the fund's webpage , the KKR Income Opportunities Fund has the objective of capitalizing upon changes in relative value among corporate credit opportunities and managing macroeconomic risks. This is a very unique objective, but in reality, this is an income-focused debt fund. We can see this quite clearly in the fact that the fund's portfolio consists almost entirely of bonds and convertible securities, with only a very small allocation to common stocks:

CEF Connect

The bonds in the fund's portfolio are not exactly what most readers are likely to think of when picturing a bond fund, however. The fund specifically states that it invests in bank loans and high-yield securities (colloquially called "junk bonds.") Thus, many of these are not traditional bonds that simply pay a fixed coupon to their investors on a regular basis with the face value coming due at maturity. This is because corporate bank loans do not work that way. Rather, these are floating-rate securities that pay a coupon that adjusts to the prevailing interest rate in the economy.

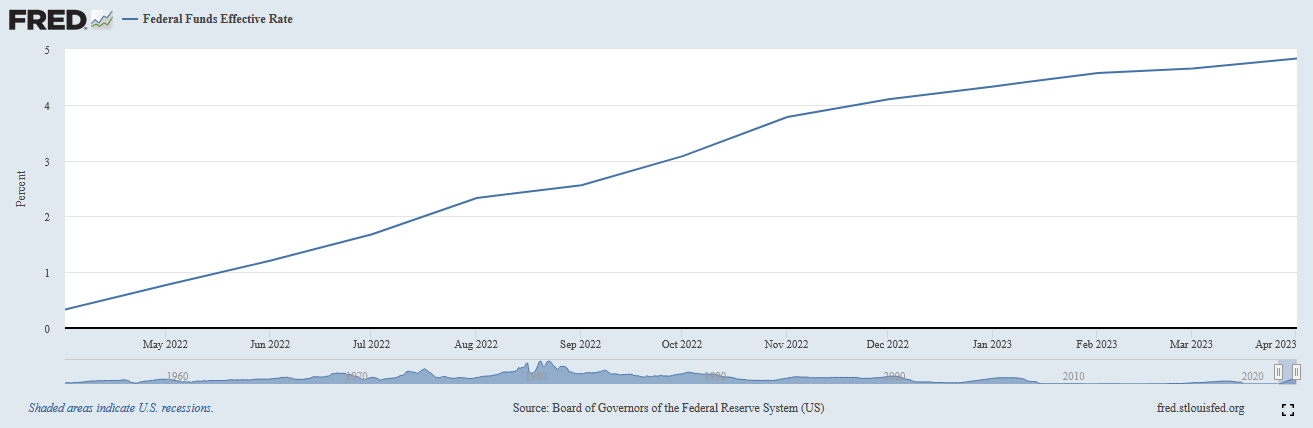

As I have pointed out in various previous articles, these securities have a substantial advantage over traditional bonds in today's environment. This is because the Federal Reserve has been aggressively raising interest rates over the past year in an effort to combat inflation. We can see this in the federal funds rate, which is the rate at which the nation's commercial banks lend money to each other on an overnight basis. As we can see here, the effective federal funds rate has gone from 0.33% a year ago to 4.83% today:

{kind=link}

The reason that I bring this up is that bond prices move inversely to interest rates. In short, when interest rates go up, bond prices go down, and vice versa. This is because a newly issued bond will have a yield that corresponds to the market interest rate at the time that it is issued. Thus, when interest rates are rising, brand-new bonds will have higher coupon rates than existing bonds. In that scenario, nobody will buy an existing bond because they could get a brand-new one with a higher yield. Thus, the price of the existing bond has to fall until it delivers a similar yield-to-maturity as an otherwise identical brand-new bond. This is the reason why so many bond funds have fallen in price over the past year.

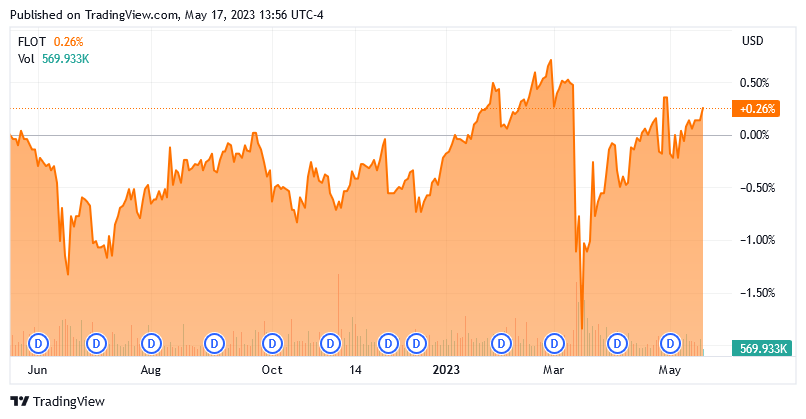

The bank loan securities held by the KKR Income Opportunities Fund should hold their value much better when interest rates rise. This is because the coupon rate of these debt securities goes up when interest rates do. This is the reason why the Bloomberg US Floating Rate Note Index (FLOT) has been almost perfectly flat over the past twelve months despite the substantial increase in interest rates:

{kind=link}

As of today, 46.2% of the securities in the KKR Income Opportunities Fund are floating-rate securities like the ones just described:

KKR

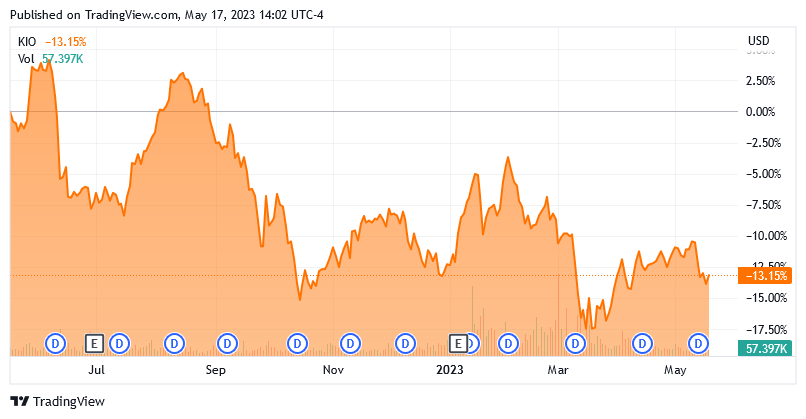

Leveraged loans and collateralized loan obligations are both floating-rate securities, which is where the above number comes from. Some preferred stocks are also floating rate securities, but the fund does not specify what exact preferred stocks it has in its portfolio today so we cannot be certain what percentage of those securities are floating rate. Regardless, preferred stock in total is only 0.1% of the portfolio, so it does not really affect the fact that just under half of the portfolio appears to consist of floating-rate securities. As such, we can expect that this fund should have held its value reasonably well over the past year. However, that is not the case as the fund is down 13.15% over the trailing twelve-month period:

{kind=link}

This is worse than both the floating-rate index and the junk bond index used by iShares iBoxx $ High Yield Corporate Bond (HYG), but the fund has a much higher yield than both of these indices. That helps to offset the decline significantly since anyone that reinvested the fund's distribution over the past year would not have lost anywhere close to 13.15% in value. I searched the fund sponsor's documentation for information about how well its portfolio performed over the period, but there is no information available. That is disappointing, since these funds frequently underperform the portfolio itself, especially in periods of market volatility as we have seen over the past year. The fund states that its portfolio delivered a -19.08% total return over the one-year period that ended on October 31, 2022, but that is the most recent data that the sponsor has provided. This is very disappointing, especially given that other fund sponsors provide daily performance updates.

As just mentioned, only a bit less than half of this fund consists of floating-rate securities. The remainder consists of junk bonds. That is something that might concern some investors, particularly those that are concerned with the preservation of principal. After all, we have all heard about how junk bonds have an especially high risk of losses due to defaults. Fortunately, we can alleviate these concerns somewhat by looking at the credit ratings that have been assigned to the securities in the fund's portfolio. Here is a high-level summary:

KKR

An investment-grade security is anything rated BBB or higher. As we can see, that is only 0.6% of the bonds in the portfolio. Everything else is considered a junk bond. Please note that I am considering the 12.8% of the portfolio that is invested in unrated securities to be junk bonds. This is logical as any company with a sufficiently strong balance sheet to achieve an investment-grade credit rating will almost certainly opt to have its securities rated due to the money that it will save from the higher credit rating. However, we can see that 42.95% of the portfolio is invested in securities that carry either a BB or a B credit rating. Those are the two highest ratings for junk bonds and according to the official bond rating scale , any company whose securities are assigned these ratings has sufficient financial capacity to carry its existing debt even through a short-term economic shock. While it is comforting that a reasonable proportion of the securities appear to be reasonably safe, this fund's allocation to such securities is somewhat less than most junk bond closed-end funds. Thus, the KKR Income Opportunities Fund does have a higher risk of default losses than most other funds. It also only has 146 current positions, so it does not make up for this by having such a large portfolio that a single default will go largely unnoticed. Thus, there may be some valid concerns here from those investors that are worried about default risk.

Leverage

As stated in the introduction, closed-end funds like the KKR Income Opportunities Fund have the ability to employ certain strategies that boost their effective yields well beyond that of any of the underlying assets. One of the strategies that this fund uses to accomplish that is the use of leverage. In short, the fund borrows money and uses this borrowed money to purchase junk bonds, floating-rate securities, and other high-yielding debt securities. As long as the yield on the purchased assets is greater than the interest rate that the fund has to pay on the borrowed money, the strategy works pretty well to boost the effective yield of the portfolio. As this fund is capable of borrowing money at institutional rates, which are substantially lower than retail rates, this will usually be the case.

However, the use of debt in this fashion is a double-edged sword. This is because leverage boosts both gains and losses. The fund's use of leverage might be one reason why it declined much more than the index over the past year. Thus, we want to ensure that a fund does not employ too much leverage because this would expose us to too much risk. I generally do not like to see a fund's leverage exceed a third as a percentage of its assets for this reason. As of the time of writing, the KKR Income Opportunities Fund has levered assets comprising 33.73% of its portfolio, so it is slightly over this one-third level. As this is not very much over the one-third limit, the fund is probably okay here as its leverage will fluctuate with the market prices of its assets and it could very easily drop under the limit on any market strength. Thus, the balance between the risk and reward with respect to leverage appears acceptable with this fund.

Distribution Analysis

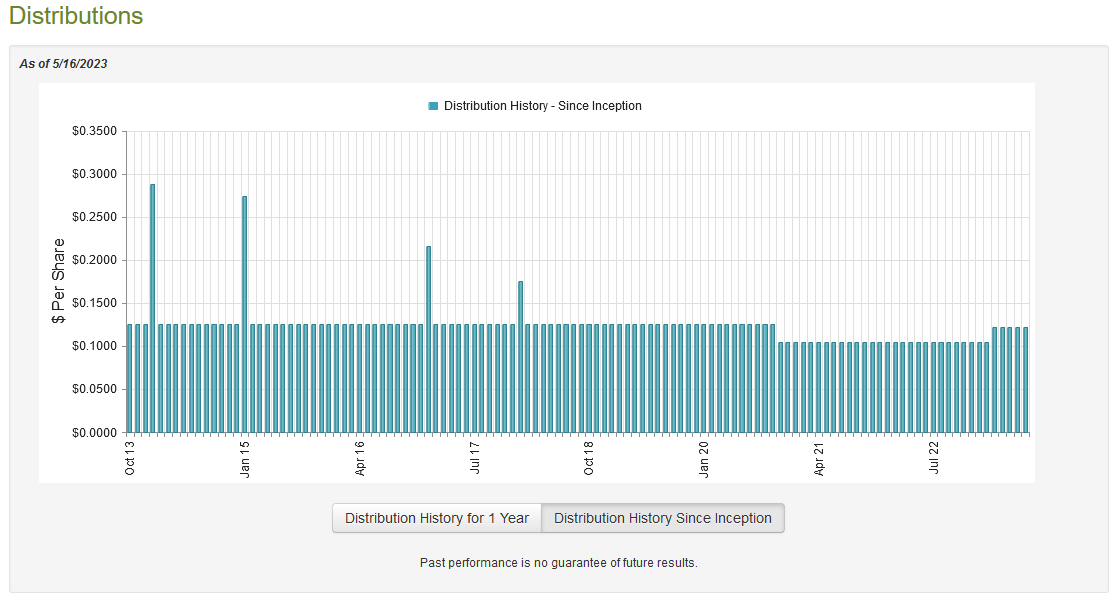

The general goal of any closed-end fund is to maintain a relatively stable portfolio value and pay out all its capital gains and other investment profits to the shareholders. This one invests in a portfolio of high-yield bonds, levered loans, and similar high-yielding assets, and then applies a layer of leverage to boost its effective portfolio yield further. As such, we might assume that the KKR Income Opportunities Fund has a very high yield itself. This is certainly true as the fund pays a monthly distribution of $0.1215 per share ($1.458 per share annually), which gives it a whopping 13.49% yield at the current price. The fund has been reasonably consistent with its distribution over the years, but it is not perfect as it did cut the payout back in late 2020, although it has increased it since then:

{kind=link}

The distribution is currently slightly below the $0.1250 per share monthly that the fund paid prior to the late 2020 cut, but it is better than it was during 2021. For the most part, this fund's track record will probably be reasonably attractive to anyone that is seeking a safe and secure source of income to use to pay their bills or finance their lifestyles. After all, it seems to make an effort to pay a reliable distribution through various market conditions and anyone purchasing the fund today will receive the current distribution and the current yield. As such, let us investigate the fund's ability to cover its distribution.

Unfortunately, we do not have an especially recent document that we can use for our analysis. The fund's most recent financial report corresponds to the full-year period that ended on October 31, 2022. As such, it will not include any information about the fund's performance over the past six months. This is unfortunate because the market has improved quite a bit since then, so the fund is probably in a stronger place financially right now than will be reflected in this report. During the full-year period in question, the KKR Income Opportunities Fund received $37,994,968 in interest, both as cash and payment-in-kind. When combined with a small amount of income from other sources, the fund reported a total investment income of $38,238,244 over the course of the year. The fund paid its expenses out of this amount, which left it with $27,468,926 available for the shareholders. This was enough to cover the $25,628,796 that the fund actually paid out in distributions. The fund paid its entire distribution out of net investment income during the prior-year period as well.

The fund did see its total asset base decline by $87,669,954 after accounting for all inflows and outflows during the period. This is concerning, but it appears that all this fund is doing is paying out the interest payments that it receives net of expenses. That is sustainable for extended periods. Thus, as long as the fund can maintain its net investment income, it should be able to maintain its current distribution. When we consider that bonds are currently boasting the highest yields that we have seen in over a decade, that is quite possible. We should not lose sleep over a distribution cut here.

Valuation

It is always critical that we do not overpay for any asset in our portfolios. This is because overpaying for any asset is a surefire way to earn a suboptimal return on that asset. In the case of a closed-end fund like the KKR Income Opportunities Fund, the usual way to value it is by looking at the fund's net asset value. The net asset value of a fund is the total current market value of all the fund's assets minus any outstanding debt. This is therefore the amount that the shareholders would receive if the fund were immediately shut down and liquidated.

Ideally, we want to purchase shares of a fund when we can obtain them at a price that is less than the net asset value. This is because such a scenario implies that we are acquiring the fund's assets for less than they are actually worth. This is, fortunately, the case with this fund today. As of May 16, 2023 (the most recent date for which data is available as of the time of writing), the KKR Income Opportunities Fund had a net asset value of $12.45 per share but the shares only trade for $10.90 each. That gives the shares a 12.45% discount on the net asset value. This is quite a bit better than the 11.59% discount that the shares have averaged over the past month, so the price certainly looks reasonable today.

Conclusion

In conclusion, the KKR Income Opportunities Fund looks a bit concerning in terms of risk, as the fund is more heavily invested in low-quality junk bonds than most other funds and the fund's shares have declined substantially over the past year. However, its total returns are not that bad and the 13.49% yield is fully covered by net investment income. When we consider that this fund is also trading at a large discount, KKR Income Opportunities Fund is worth recommending for a portfolio today.

For further details see:

KIO: The 13.49% Yield Is Fully Covered, But The Fund Is Cheap