KNNGF - KION: The Upside After Q1 2023

2023-05-13 04:46:27 ET

Summary

- I've reviewed KION and invested into the company for some time. While KION is facing some serious near-term pressure, I believe the medium and long term looks good.

- KION is, by all appearances, a company set to revert significantly. The share price/valuation result in some calling it a "value trap".

- I am not one of those investors, and I consider KION good enough to invest in. Here is why.

Dear readers/followers,

KION (KIGRY) is one of those companies that I invest in, and that I believe will revert in the next 12-24 months or so. I believe they will revert because their earnings will take a massive step upward once the current pressures on the bottom line start disappearing, and the normalization of supply chains and various operational improvements come online.

It's my view that since my last article on KION and since the company reported 1Q23, this has become more clear. I believe it's becoming clearer and clearer that there will be a near-term reversal. My case for this article is presenting to you why I believe this will happen, and why I would be interested in buying more KION at this time.

Also, why you should be buying more KION at this time?

Let's look and see what we have going for us here.

KION - An update is warranted after 1Q23 because things are looking good

So, the 1Q23 is why we're here, to begin with. We have negative numbers on a lot of KPIs, but also positives in some others. First off, Order intake is down 16% YoY. The macro continues to be difficult, and customers are careful with their spending.

Top-line sales were up - though mostly due to pricing, not due to volume. The pre-tax profit was down, but only 8%. The margin is inching back up, with a margin on an EBIT basis of 5.6%. Also, that EBIT improvement marks a 91% quarter-on-quarter improvement , which is absolutely solid on a comparative basis. Free cash flow was positive as well - up half a billion from negative YoY. EPS is also positive, which means a 100%+ improvement from the negative YoY EPS level.

The improvements came from fundamental trend improvements in ITS. We're talking about improved supply chains and benefits from the commercial and operational measures taken by KION, which resulted in the company beating estimates. The way up back to profitability and market-beating RoR is still far. Look at my recent set of articles on the company and you'll see why I'm in the green - look at my valuation later and you'll see why I expect to be significantly in the green going forward.

Seeking Alpha KION article (Seeking Alpha)

Some highlights from 1Q include new agreements with Li-Cycle to form a JV/partnership regarding battery recycling, with a 95%+ recovery rate for Li-ion batteries. The company's own fuel cell system production in Hamburg is expected to start in 2023. This is in turn giving KION a significant competitive edge in the market.

Aside from that, the company's global segment is launching a value platform going live with about 30 multi-brand model launches in -23 alone, with more than 25 for export markets from China.

{kind=link}

The company also went some ways in its sustainability/ESG work - but this is not that interesting to me as an investor. We know the company has targets in terms of emissions, and I can mention that the share of electrified new trucks has gone up to 88% as of 2022 - but I'm more interested in underlying profitability, as opposed to platinum sustainability ratings, ISO 14001/45001 increases and emissions targets. These may dictate investability to some, but I am not one of them.

I like hard data.

Like the ITS segment. 45% quarterly order intake improvements, beating my own expectations, and over 50% improvements in YoY EBITD margins, with margins back up over 8.5% on an EBITD level. Revenue in the core ITS segment remains at elevated levels, and the segment is really "humming", as far as both expectations and forecasts go.

SCS isn't as good. It's improved - 250 bps margin improvements on a quarterly basis, but most everything else remained negative. The positive that can be said is that the segment is pre-tax positive at €7M and that margins are back into positive at 0.9%. But this is neither impressive nor desirable in the long run. The kitchen-sink quarter seems past for SCS as a segment, but now we're looking for improvements beyond expectations, and SCS doesn't yet deliver this.

The problem?

The current macro is causing order postponements reflecting the overall uncertainty. This leads also to slower decision-making processes on new orders. The company has visibility due to its order book, but improvements may be some time coming, unfortunately.

However, thanks to the ITS segment, things are actually going well. Here are the trends/results.

{kind=link}

The company is far from out of the woods yet. Moving from EBITDA to EPS, we find substantial and non-trivial increases in financial expenses, almost twice that of 4Q, due to increased interest rates, lower net results from leasing, and changes in derivatives.

There were also positives in the quarter in the FCF due to how almost no net working capital, or NWC was built up during the period - less than €15M, which came from improved supply chain trends. Other than that, inventories improved as well, and semi-finished trucks were reduced to less than 3,000 units.

Things are still somewhat rocky in terms of company fundamentals. Leverage remains well above the company's usual level. Industrial net debt is at 2.8x, and net financial is at 1.3x. This isn't worrying to a massive degree, but it's certainly above where things usually are.

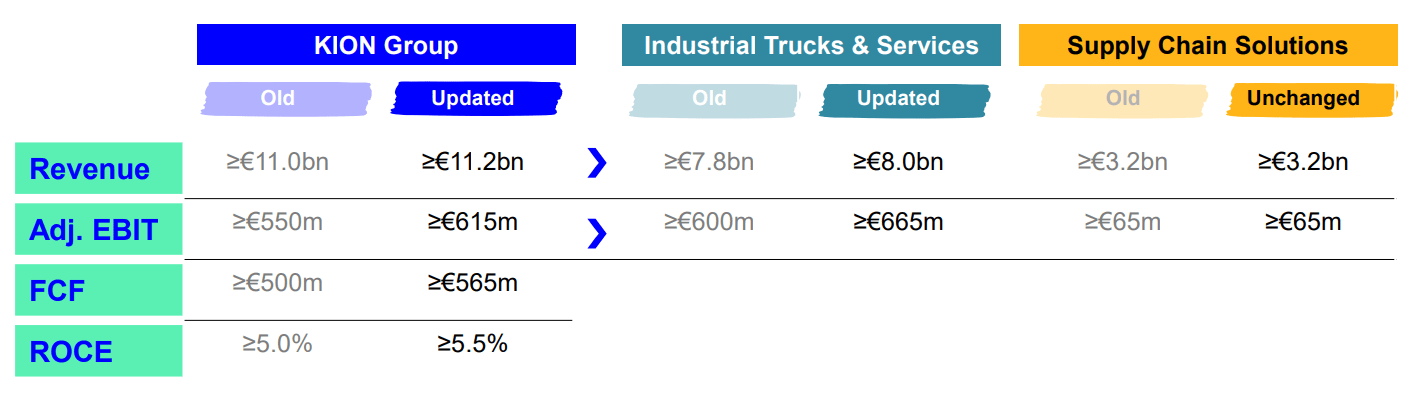

The company actually increased its guidance quite a bit. We're now up over €200M in annual revenues, nearly €70M more in EBITDA on an adjusted level, and over €60M in FCF, according to these specifics, coming mostly (or rather, all of it) from industrial trucks & services, or ITS - the company's core segment.

{kind=link}

So how could this be?

Well, fairly simple - the improvements from the supply chain are significantly higher than expected. Normalization is happening faster than the company forecast, due to its own improvement programs. The company is also more agile in its ITS segments. Contracts in the ITS segments are easier to adjust in terms of pricing - or rather, contracts are more flexible and quicker in terms of delivery. The SCS contracts are usually done years in advance, and they suffer from some of the "legacy" characteristics you'd find in certain infrastructure companies, where businesses went "into" projects and agreements that turned out to be incredibly unprofitable at rates and profits levels "today" then when they were signed. Also, a surprising number of businesses, KION included, have traditionally not used clauses to safeguard against changes in inflation or inputs. This is not easy to do, but it's something companies across Europe now are doing to a higher extent (see my articles on Alstom ( OTCPK:ALSMY ) as an example).

So, as long as legacy is weighing down SCS, not much improvement there, and margins will continue to lag in 2Q23. I don't expect a marked or clear improvement until we enter 4Q23 or even 1Q24.

That's my forecast, at least.

Moving to valuation.

KION valuation - A lot to like still

If you believe that KION is eventually moving up, you're still in for a massive, triple-digit upside. Only if you believe that KION's current valuation marks an overall paradigm shift relative to its historical performance, can it be justified to be negative on the company's long-term prospects here.

KION may currently be below average in terms of profitability. But this is entirely due to the recent few years. Looking beyond current SCM trends, the company is an above-average business in terms of profitability as well as returns.

What's more, even with these relatively terrible numbers, the company is still profitable in 1Q. The company's relative amount of debt is something to keep looking at, but much of those KPIs will reverse when earnings normalize.

There are two reasons why profit will go up as we move forward into 1Q and 2Q into 2H23.

First, the continued normalization of supply chains and macro, which is currently ongoing. While slow, it surprised in 1Q and might surprise going forward once more.

Second, the working through of unprofitable, lower-margin legacy contracts on the company's SCS segment. Once these are out of the way, I have no doubt the company's margins will bounce back up - and the resulting increase in valuation/share price move should reward investors very nicely.

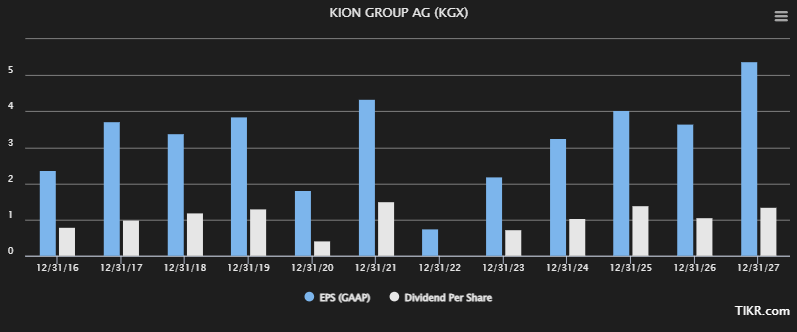

Here is where S&P Global forecasts currently are for KION.

TIKR.com KION forecast (S&P Global/TIKR.com)

{kind=link}

Any negative outlook for this particular company needs to explain how the above-mentioned trends would not result in a significant reversal of the company's fortunes. KION remains a market leader in key segments. These latest few months have done little to dent the company's international reputation or its expertise in its core segments. The current revenue-net flows do not look all that attractive, but it's really a non-recurring event - at least that's how I see it.

It's not that drops in this company's fortunes haven't happened before. They have, but recovery has always been there. And if even anything close to these current trends is true, then you're looking at an upside of no less than 115%. 115% marks the 14.68x 2025E P/E for KION AG at these forecast numbers. The company currently trades at a native average weighted (for the German ticker KGX) P/E of 23.9x, though impacted by low earnings. The straight current, non-weighted P/E is closer to 50x. A 5-year normalized P/E comes to around 24x. An upside to those earnings by 2025E implies an upside of 250% in 3 years, or 60% annualized RoR.

KION is by far one of the highest-potential investments I currently invest in outside of office REITS. I view it as an incredibly solid company - at least fundamentally. The fact that it needs to recover only means I can buy it cheap, and my only current regret is not buying more at below €20/share.

That less than 0.6% yield is not attractive is nothing that needs be argued with. It's an unattractive yield to be sure - but it's also momentary, as I see it, and closer to 4%+ if we normalize the future yield.

Because I believe the next few years of outsized growth in earnings will do much to catapult this company upward in terms of valuation - as will the increases we're likely to see in dividends. This coupled with the continued, low valuation we're seeing for what I see as a qualitative albeit historically somewhat cyclical company, means that my current thesis continues to almost write itself as I finish up an article like this.

The current S&P Global average for KION AG is almost €45/share. That is, mind you, up from a low of €36/share average back in December. Out of 18 analysts, 14 are either at a "BUY" or outperform for this company.

Analysts at €45/share - and me?

I never shifted my target from €78/share. I'm still not shifting my target from that level. KION continues to be attractive, and I continue to put money to work.

Thesis

My thesis on KION is as follows:

- KION Group is an attractive capital goods play with an emphasis on intralogistics solutions, automation, and warehouse technologies - things like forklifts, to put it simply.

- The company is undervalued, and forecasts imply a significant upside over the coming 5 years, with an upside of at least 80-110%, but potentially as much as 250%+

- KION remains a "BUY" with a price target of €78/share.

Remember, I'm all about:

-

Buying undervalued - even if that undervaluation is slight, and not mind-numbingly massive - companies at a discount, allowing them to normalize over time and harvesting capital gains and dividends in the meantime.

-

If the company goes well beyond normalization and goes into overvaluation, I harvest gains and rotate my position into other undervalued stocks, repeating #1.

-

If the company doesn't go into overvaluation, but hovers within a fair value, or goes back down to undervaluation, I buy more as time allows.

-

I reinvest proceeds from dividends, savings from work, or other cash inflows as specified in #1.

Here are my criteria and how the company fulfills them (Italicized).

-

This company is overall qualitative.

-

This company is fundamentally safe/conservative & well-run.

-

This company pays a well-covered dividend.

-

This company is currently cheap.

-

This company has a realistic upside based on earnings growth or multiple expansion/reversion.

That means that the company still fulfills all of my criteria for attractive valuation-oriented investing. I'm still at a "BUY".

For further details see:

KION: The Upside After Q1 2023