KNNGF - KION: The Upside Remains And Is Still Triple Digits After Q2 2023

2023-09-13 16:00:00 ET

Summary

- KION's stock has seen a significant increase, making it no longer a bottom-fishing opportunity.

- The company has experienced a reversal in earnings and improved financial metrics.

- KION's upside potential is still intact, but at a lower level than before.

Dear readers/followers,

KION ( KIGRY ) is a company I've been bullish on, very vocally, for many months. My overall RoR is over 49% inclusive of dividends of FX, which for the time involved is of course a very solid sort of trend. When KION was at bottom-type valuations this was an almost cigar-butt type investing stock (while the company still has quality). That time is most certainly over at this point. KION is still cheap - I can still maintain that. But bottom-fishing, or cigar-butt investment? That's no longer the case.

Also, the higher the company goes, the harder it will be for the company to go even higher, given the current macro and market situation. While I maintain that KION has a triple-digit upside, I also say that some of this upside is now gone. If you didn't invest when the company traded at below €25/share, why would you buy it now?

The literal only change we've seen over the past few months and in the last quarter was something that I forecasted in my KION article when the company was extremely cheap.

I literally wrote in that article:

The time here, as I see it, is the time to really "back up the truck" on KION as an investment, so that is exactly what I intend to do here.

Current analyst estimates call for the company to deliver revenues 10% above 2021. While margins will go down, with EBIT expected to touch 6-7%, this does not to my mind justify a 50%+ price drop. Note that the margin expectations of 6-7% are still very much the same as they were in the article.

(Source: KION Article ).

I do not see how I could have been much clearer at the time. The sheer volume of articles I've put out on KION also really goes a long way to show you just how much I've expected from the business, and what it has materialized since.

Let's revisit things, and see how this might actually be one of the last times you could get a realistic triple-digit upside from KION AG.

KION's upside is very significant - even after that 40-50% climb

You know KION. World leader in industrial trucking solutions, and #1 in global supply chain solutions. It works with over €12B in annual net sales/orders, and is, outside of this situation, a qualitative and clearly profitable industrial with decades of history under its belt.

And during the last quarter, what I had been expecting for over a year finally happened.

What?

Reversal in EBIT/Earnings

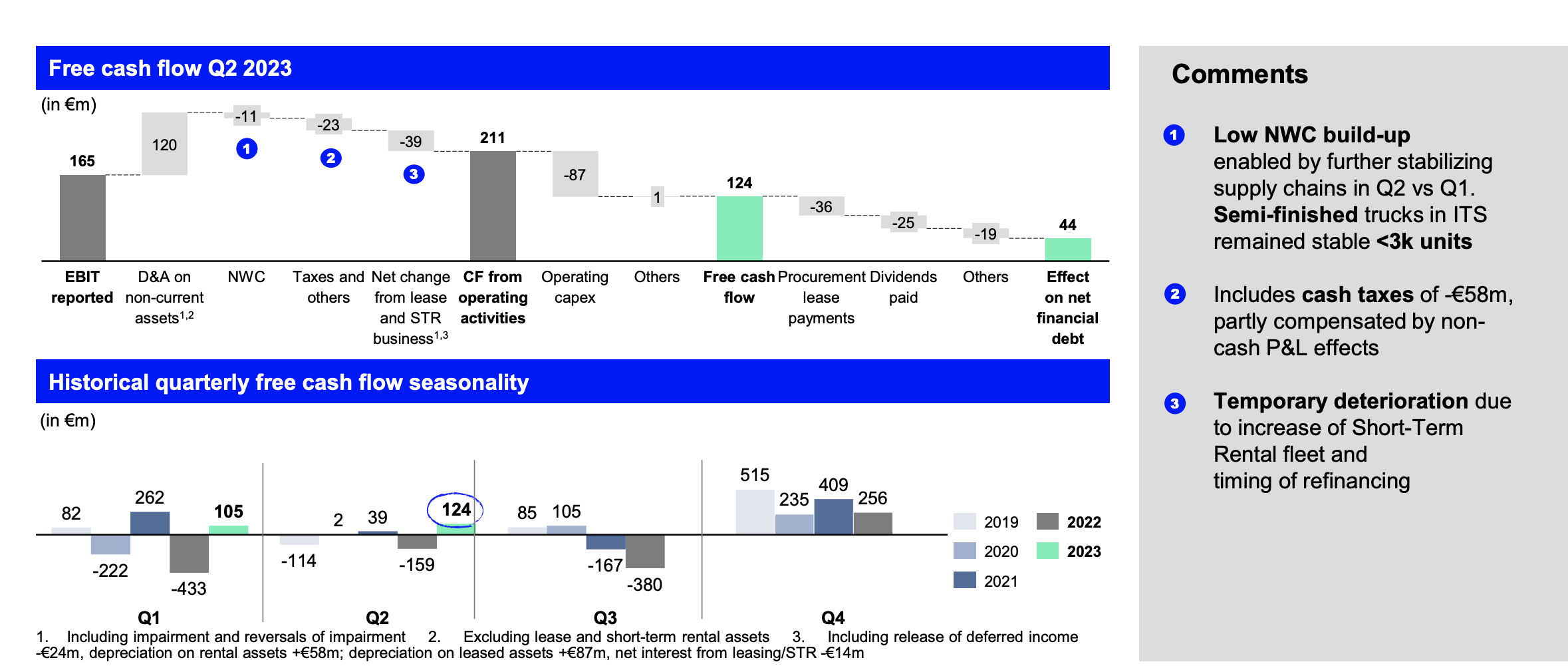

The company has been on an almost negative earnings level for many quarters prior to this. And the top-level results were actually fairly negative in 2Q23 - we saw a 24% decline in order intakes, which puts the company at just around €10B annually, and a 16% decline in the company's order book as new orders are really declining. However, earnings before taxes have recovered in a big way, as has the company's FCF.

We're up 36% in EBIT at a margin of nearly 7% for adjusted EBIT, and FCF went from negative to positive, rising over 100% YoY. EPS is still at a somewhat low level - but is stabilizing here.

What's more?

KION raised the outlook for all major KPIs for the entire group

The language and wording is clear. The turnaround is now here. What's the trajectory? We'll have to see. But ongoing company measures as well as macro trends are driving a fundamental recovery in the company's most important metrics.

Segment ITS saw the strongest intake in over four quarters, with strong services, as well as a new quarterly record in terms of revenue due to favorable input trends, higher production, and materializing price increases for products. Remember, the company had several contracts of unfavorable margins that it needed to work through. Those are declining - and inflation-adjusted sales for 2022 and 2023 are now materializing.

That's why I said that this development was very clear in my last articles. I believe it has been very easy to forecast this improvement in the company. The only thing that hasn't been easy has been to forecast the exact timing of it.

SCS is still a bit so-so. The company's second segment recovered from its very low levels but still struggles with lumpiness and hesitancy for new order signing due to macro data.

But even here, improvements are now clear. According to company IR, over 70% of contracts in SCS now have price adjustment clauses (Source: KION IR). That means the unfavorable sales and margin trends we've seen are unlikely to be repeated.

The acceleration for the company is broad-based. It reflects a fundamental restoration of demand levels in both of the company's key sales segments, following a few quarters of struggle. Despite lower intake, the company's current order book is well-filled. The split between ITS and SCS is still somewhat unfavorable, in that one segment is somewhat worse than the former - but cash flow trends have reversed, and the company's working capital on a net basis is almost completely stable.

{kind=link}

In other fundamental parts of the company, we still have a somewhat unfavorable leverage ratio, 2.7x in industrial net debt - though only 1.3x in terms of net financial debt. The company also continues to use most of its free cash flow to carve away at this mountain of debt - €1.6B sounds a lot, but remember revenues over €10B annually for the company.

Essentially, ITS is the segment that's responsible for KION being able to reset and up the guidance for the full year. The company now expects over €200M more in revenues and almost €100M more in EBIT from that segment alone - SCS is unchanged.

I would characterize the company as being in a situation where they have delivered proof of the profitability turnaround in key parts of the company - and where more improvements are expected going forward.

Things to keep an eye on going forward? Anything specific that worries me that I haven't mentioned before?

Not really. It depends on how sensitive you want to be. Remember that KION doesn't guide for order intake numbers, at all. Because they don't give us this information, this leads to potential lumpiness in forecasts compared to results.

I was also worried about the 70% price adjustment clauses, and what this would mean for the remaining 30% in terms of how "bad" things are in legacy contracts. IR/the company however guides that most of those 30%, most of the worst contracts here are things we've already seen. The company is calling an expectation of 30% being "problem contracts" both "pessimistic and inaccurate" (Source: KION IR, Earnings Call 2Q23).

The honestly biggest point of concern is SCS normalization - and because the company doesn't guide on numbers here, we're left a bit in the dark. We can look at macro trends, but this certainly doesn't give a full set of expectations or assumptions either.

The problem with SCS is structural. SCS projects are both large and capital-intensive. Lead times are very long, especially with projects only getting bigger. The bigger the project, the longer the lead time and process typically is. That's also why the segment trends are so very lumpy here.

I view it like this: You need to accept the uncertainty in SCS and depend on ITS for the underlying stability of the company. This lumpiness and uncertainty is the reason why the company, all things considered, deserves a discount, and why I am discounting it.

But beyond that, I'm fairly confident and with a high conviction in my KION investment. That's why over 2.5% of my corporate portfolio is exposed to KION's common shares at this time.

Let's look at valuation.

KION - The upside is intact, but lower

First off, S&P Global/analyst targets. I want to remind you that I've had a €75+ PT since the company traded below €25/share. It's now at €38/share.

Meanwhile, analysts following the company at one point cut their low-end targets for KION to €17/share. What should we do with those sorts of target communications? If we follow these, we would do nothing but buy and sell, especially since the higher-end target for KION only 4 months prior was €120/share. (Source: S&P Global, TIKR)

I forecast on a longer basis. I know KION is volatile. It will continue to be volatile. But have a high conviction in my ability to accurately over time, forecast where the company is likely to be valued.

The current S&P Global targets give us an average of €45.7 from a low of €23 and a high of €68. Only a year ago, the same numbers were a low of €52, a high of €120 and an average of €75. My own PT remains rock-steady at €78/share for the time being.

While KION has seen some of its potential upside materialize over the past 8 months, there's movement potential left. The reason for this is the company's sheer reversal potential. Also, you need to realize in part how high KION has traded, and just how high earnings are expected to go.

{kind=link}

In some ways, what we see here is just the beginning. The 40-45% RoR is just a beginning to what might happen in a year or three, if anything close to what you see above materializes.

But let's say you don't believe in KION's premium at all. It's BBB-, the yield is bad, and you don't believe a company, despite its estimated growth rate of 50-60% on average on a 3-year basis, can be worth that much.

Fine. 15x P/E. Then this is your RoR, even today.

{kind=link}

Do you see the potential? That's the lowest I consider possible. Anything close to normalization to a historical premium for this company would entail RoR levels upwards of 200-300%. At a 25-30x P/E, the absolute potential RoR is 82.37% per year, or 298.94% RoR in less than 3 years.

Likely?

I wouldn't personally invest with this as an expectation, as it implies a €140 share price. But I can tell you that I'm not selling my KION shares at €78. I would wait for longer to rotate, given what I see possible here.

I maintain KION as one of my higher-conviction long-term BUYs. I see a realistic potential to double your money in this investment.

I still say "BUY".

Thesis

My thesis on KION is as follows:

- KION Group is an attractive capital goods play with an emphasis on intralogistics solutions, automation, and warehouse technologies - things like forklifts, to put it simply.

- The company is undervalued and forecasts imply a significant upside over the coming 5 years, with an upside of over 100%. Even though this upside is now significantly lower than it once was, I still consider this company a massive buy. I haven't shifted my PT for a very long time, and I won't shift my PT here, over 1 year later.

- KION is a "BUY" with a price target of €78/share, and I have a high conviction and exposure to this company.

Remember, I'm all about:

-

Buying undervalued - even if that undervaluation is slight, and not mind-numbingly massive - companies at a discount, allowing them to normalize over time and harvesting capital gains and dividends in the meantime.

-

If the company goes well beyond normalization and goes into overvaluation, I harvest gains and rotate my position into other undervalued stocks, repeating #1.

-

If the company doesn't go into overvaluation, but hovers within a fair value, or goes back down to undervaluation, I buy more as time allows.

-

I reinvest proceeds from dividends, savings from work, or other cash inflows as specified in #1.

Here are my criteria and how the company fulfills them (Italicized).

-

This company is overall qualitative.

-

This company is fundamentally safe/conservative & well-run.

-

This company pays a well-covered dividend.

-

This company is currently cheap.

-

This company has a realistic upside based on earnings growth or multiple expansions/reversions.

That means that the company currently fulfills all of my criteria for attractive valuation-oriented investing.

For further details see:

KION: The Upside Remains And Is Still Triple Digits After Q2 2023