RA - KKR Income Opportunities Fund: An Opportunity To Add Income To Your Retirement Portfolio

Summary

- KIO trades at a discount to NAV of -11% and offers a forward annual yield of 12.5% with monthly distributions.

- After a poor return in 2022, this taxable fixed-income fund is shaping up nicely in 2023 with a recently raised distribution.

- The fund is in the midst of a rights offering, which could offer shareholders an opportunity to add shares at a lower price.

As I pass another birthday and get closer to my own retirement, I am constantly on the lookout for opportunities to increase my future income stream in retirement. In my article published earlier this month, I describe my income compounder approach to building a retirement income stream in more detail. With that background in mind, I would like to share with my readers and followers a unique opportunity to add some shares of an income fund from KKR and Co, Inc. ( KKR ). Not surprisingly, the name of the fund is the KKR Income Opportunities Fund ( KIO ).

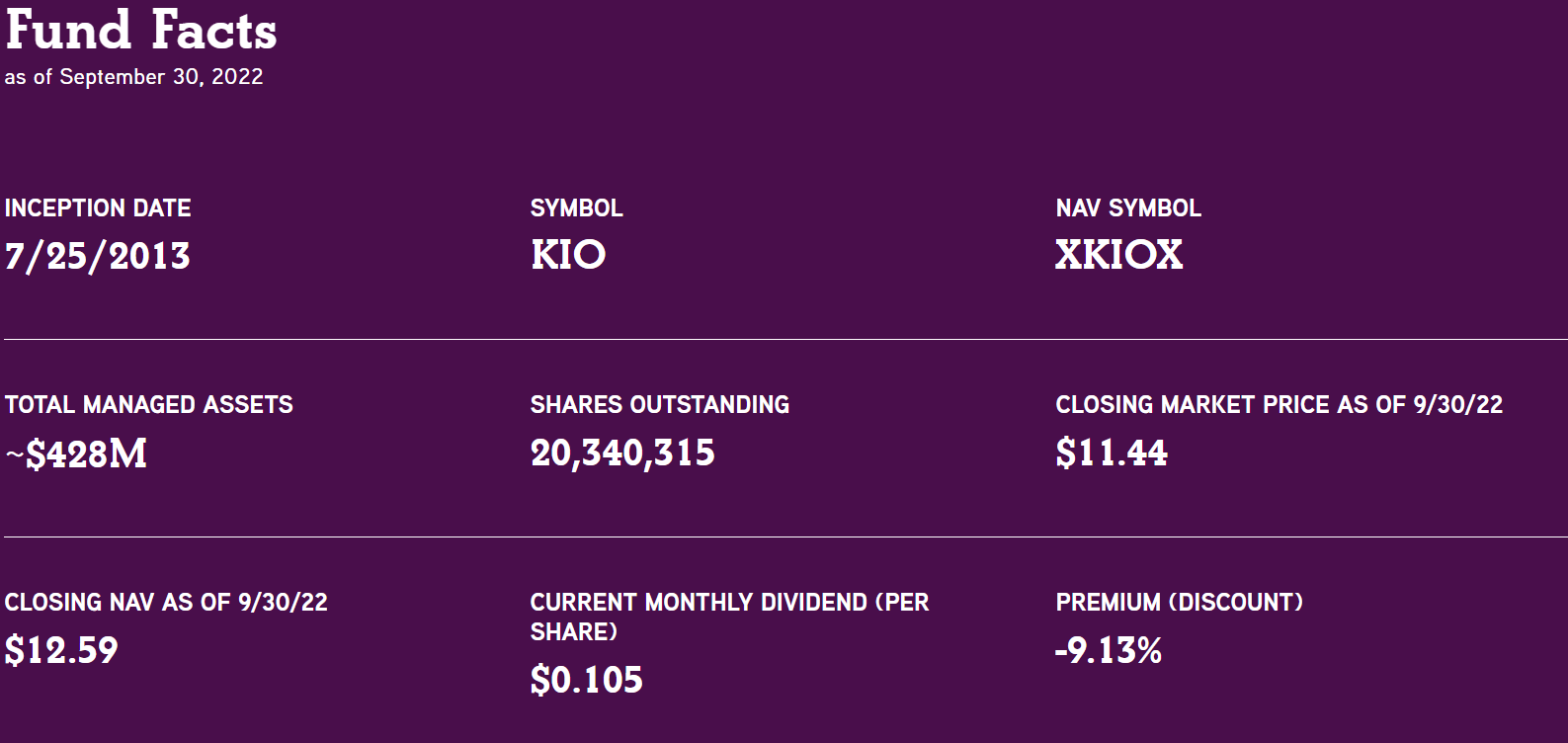

Instead of using a lot of words, here is a snapshot of fund facts from the fund website:

{kind=link}

The fund has been around for a while (almost 10 years) and trades at a discount to NAV (although both NAV and the discount are now higher), and pays a regular monthly dividend, which was $0.105 for quite a while until it was recently raised by 15% to $0.1215 per share starting in March. This fund, which now trades at a discount of -11.3% as of 1/26/23, pays a monthly distribution that amounts to a forward annual yield of about 12.5%, and is already a good value at the current price of $11.50. I rate the stock a Strong Buy, but with one caveat.

Rights Offering Announced

On January 12, the fund announced a rights offering for existing shareholders who owned shares as of January 23. The offering is a transferable offering, meaning that shareholders who are issued rights can trade those rights on the open market if they wish to (under the symbol KIORT). The offering will expire February 16, unless extended. It is likely that the RO will dilute the value of existing shares due to the new shares being sold below NAV, and that may in turn have the effect of driving the price down.

The details of the rights offering are spelled out in the press release:

Record Date Common Shareholders will be entitled to purchase one new Common Share for every three Rights held (1 for 3).

The subscription price per Common Share (the "Subscription Price") will be determined on the Expiration Date, and will be equal to 92.5% of the average of the last reported sales price of a Common Share of the Fund on the NYSE on the Expiration Date and each of the four (4) immediately preceding trading days (the "Formula Price"). If, however, the Formula Price is less than 82% of the Fund's net asset value ("NAV") per Common Share at the close of trading on the NYSE on the Expiration Date, the Subscription Price will be 82% of the Fund's NAV per Common Share at the close of trading on the NYSE on that day. The estimated Subscription Price has not yet been determined by the Fund.

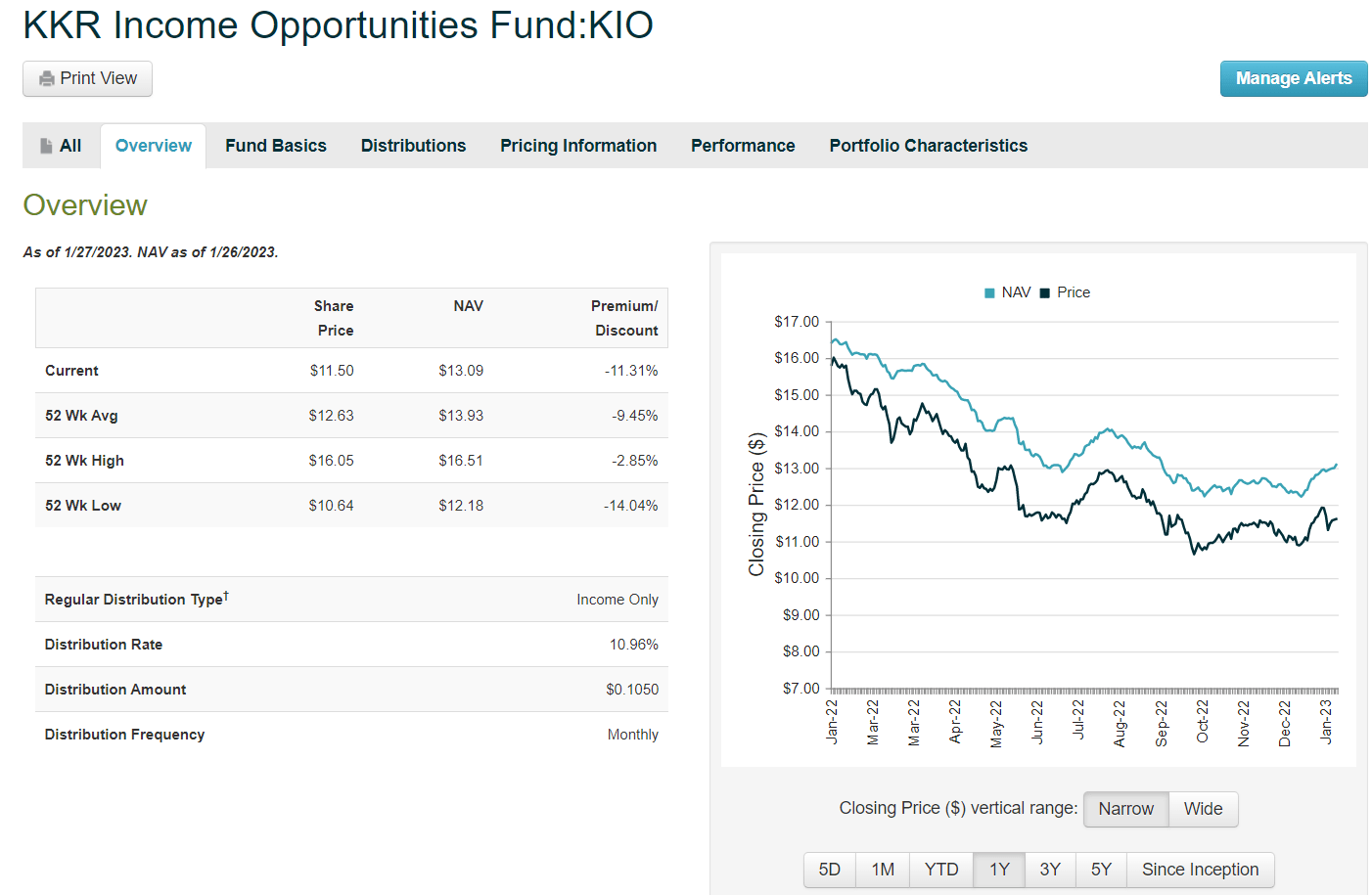

The impact on the fund's share price immediately after the announcement of the RO was not what I had expected would happen and that may have simply been due to the timing of the press release. The announcement came out on January 12 and instead of the price dropping immediately, the price rose to a high of $11.91 on 1/18 before dropping again to around $11.30 on January 20, and now back up to $11.50. Meanwhile, the NAV of the fund has risen steadily since that time, creating an even wider discount and a better buying opportunity now. That trend can be easily seen on this fund pricing chart from CEFconnect, where it appears NAV hit a near-term bottom right around the beginning of the year and has been trending steadily upward since then.

{kind=link}

In addition, the fund has yet to go ex-dividend for February, so investors who buy shares of KIO before February 2 will also receive the $0.105 dividend for February. After that date, the fund NAV will drop by the amount of the dividend, and the share price may drop even further due to the upcoming rights offering and fears of dilution which could cause some investors to sell their shares after collecting the next month's dividend.

Just to help investors understand how the pricing of the RO could work, if the NAV and price remain the same between now and Feb. 16 (which they most likely will not), the formula would be calculated as:

0.82 * NAV of $13.09 = $10.73*

.925 * Price of $11.50 = $10.64

* Shareholders who wished to exercise the rights they own would be able to buy one share for $10.73 for every 3 rights they hold.

Of course, the expiration of the RO is still 2 weeks away so it is quite likely that things will change. My expectation is that NAV will continue to increase so the offering subscription price is likely to go up more than what it would be if the offering had expired Friday 1/27 as in the above example. Will the subscription price be lower than the current market price? That is the question that rights holders need to ask themselves.

For others who do not own rights, the question to ask is whether the price will drop after the expiration of the RO, and if so, by how much? In my experience with other funds that have held ROs the price often drops more than the final subscription price after the expiration of the offering, so it is better to wait and buy on the open market after the RO expires. I am not sure that will be the case with KIO.

My suggestion for investors new to the fund, and what I have done in my own portfolio, is to buy a tranche of shares (50 or 100) now that you are comfortable with to establish an initial position, collect the February dividend, and then consider adding more if the price drops in another couple weeks. Meanwhile, keep an eye on the NAV of the fund and see if the trend continues in a positive direction, which I believe it will as the market seems to be in a bullish mood for the past few weeks.

Who Should Buy KIO?

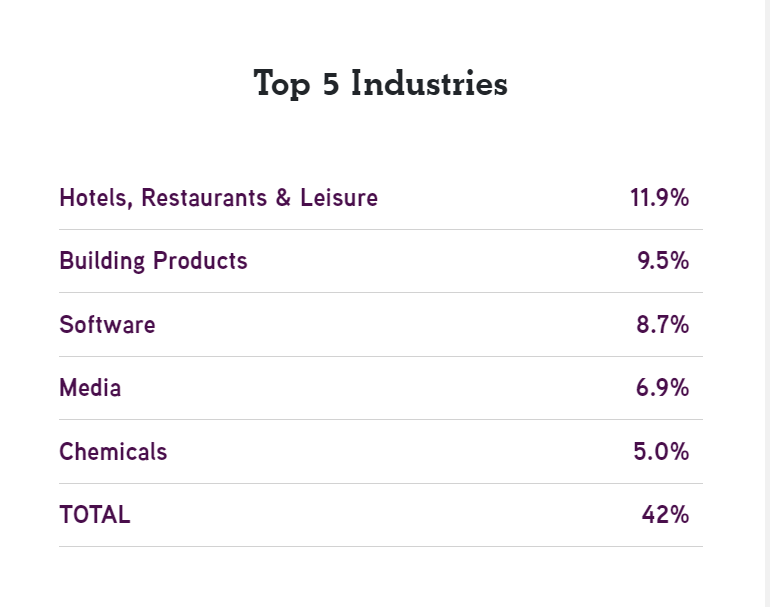

This income fund from KKR is not for everyone, especially those who are more conservative in their risk profiles and who fear a major recession in the next six months to a year. KIO owns about 50% high yield securities and about 45% leveraged loans. The credit quality consists primarily of "junk" rated credit instruments. The fund holdings are more than 93% US based with about 6.5% European based (as of 9/30/22). The top 5 industries make up 42% of the total portfolio and the fund holdings are diverse with the biggest majority in Hotels, Restaurants and Leisure (as of September 30, 2022).

{kind=link}

The fund's objective and strategy is described on the fund website :

KKR Income Opportunities Fund ("KIO" or "the Fund") seeks to allocate across credit instruments to capitalize on changes in relative value among corporate credit investments and manage against macroeconomic risks.

They use a targeted portfolio of mostly bank loans and high yield securities such as corporate bonds to achieve attractive levels of income offering monthly distributions. The fund managers attempt to adapt credit strategies to macroeconomic and current market conditions.

The fund breakdown of credit quality and portfolio composition is illustrated on the fund fact sheet (as of 9/30/22):

{kind=link}

KKR Credit Advisors LLC is the fund's adviser and is a subsidiary of the global asset management firm, KKR. In a recent positive discussion of KKR, this SA article from fellow contributor The Value Puzzle suggests that KKR could be a surprise winner in 2023 and holds $110 billion in "dry powder". The relationship between KKR Credit Advisors and the parent company KKR is described on the KIO fund website to help clarify the benefits from such an arrangement:

KKR Credit Advisors (US) LLC (the "Advisor") serves as the Fund's investment advisor. Launched in 2004, the Advisor is a subsidiary of KKR & Co. Inc. (together with the Advisor and its other affiliates, "KKR"), a leading global investment firm with more than a 44-year history of leadership, innovation and investment. The Advisor's investment teams, which are organized by industry, invest across the capital structure with the goal of protecting capital and achieving attractive risk-adjusted returns.

That makes me feel more comfortable investing in KIO just knowing that it has the backing of this very large and successful global investment firm with many years of experience and oodles of resources to bring to the table. The fund managers, Chris Sheldon and Jeremiah Lane , also have excellent track records in credit investing.

Fund Distributions

Another very appealing aspect of the fund is the distribution history. Although it did cut the distribution once in its nearly 10-year history, the monthly distribution has been held steady for most of the duration of the fund since inception as shown in this snapshot from the SA Dividend History page. And now, with the most recent increase to $.1215, the monthly amount is nearly back to the original monthly distribution of $.1250 that it started with in 2013.

{kind=link}

Fund Prospects and 2023 Outlook

From the fund's annual report, I am including a snapshot of the fund managers' commentary to provide some perspective. The date of the Annual Report is October 31, 2022, so it may be wise to consider what has happened since that time, but I believe that this commentary offers some good food for thought:

For yield-hungry investors the traded credit market buffet is open…just not all you can eat. After more than a decade of extremely low interest rates, the leveraged credit markets in the United States and Europe are awash in yield and present an interesting opportunity for investors willing to take a longer-term view on credit markets. Rising interest rates and the retreat of traditional lenders set the table for the current smorgasbord of yield options. For years, interest rates were artificially low, and prices fell quickly as those artificial supports disappeared. But banks have also stepped back from the capital markets and loan origination due, in part, to the waning risk appetite of investors and also to rising rates; as rates rise, so do the regulatory capital requirements imposed on banks. Financing is now both expensive and very difficult to source, hence the higher yields we are seeing today.

Also from the Annual Report is a summary of the fund holdings:

As of October 31, 2022, the Fund held 71.5% of its net assets in first and second-lien leveraged loans, 88.1% of its net assets in high-yield corporate debt, 2.8% of its net assets in equities and other investments. KIO's investments represented obligations and equity interests in 139 positions across a diverse group of industries. The top ten issuers represented 49.3% of the Fund's net assets while the top five industry groups represented 67.7% of the Fund's net assets. The Fund's Securities and Exchange Commission 30-day yield was 16.43%

The fund expenses amount to 3.56% with 1.77% management fees, and the remaining 1.8% in interest and other expenses. The current leverage used (as of 10/31/22) is about 39%, which is on the high side for a leveraged fixed income fund, but understandable given the market conditions in 2022. I would expect the fund advisors to consider deleveraging a bit in 2023 as the economy recovers from the effects of rising interest rates and ongoing inflation.

Comparison to Other High Yield Funds

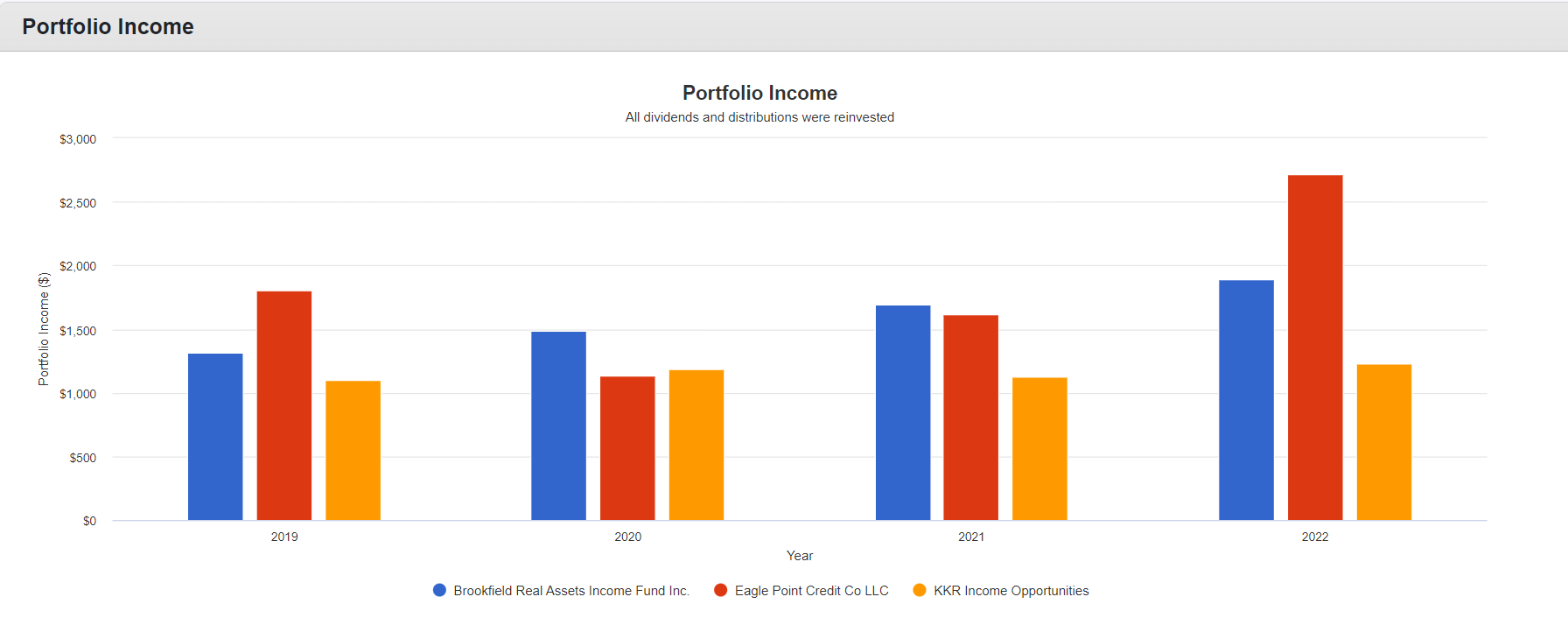

I decided to compare the total return, income generated, and max drawdown of KIO compared with two other popular high yield funds, which I also own and have large positions in. Those two funds include Eagle Point Credit ( ECC ), which I have previously covered , and Brookfield Real Assets Income fund ( RA ). Each of these 3 funds invests in different asset classes with very different strategies and fund holdings, but all offer high monthly income and reasonable total returns over the past 4 years despite the 2020 Covid-19 recession and 2022 bear market. I used Portfolio Visualizer to capture some of the statistics.

{kind=link}

And the income generated (with dividends reinvested) as I would expect, was slightly lower in most cases for KIO, however, the inclusion of all 3 funds indicates that holding them all through different periods would likely smooth out the results with a steady and rising flow of income overall.

{kind=link}

Concluding Remarks

If you are an investor with a long-term horizon, meaning that you plan to create a future income stream that will endure for 20 or 30 years in retirement, you may wish to consider adding shares of KIO. As with my other income holdings that offer high yield monthly income, there is a level of risk to consider, so I would suggest that you may wish to consider including additional positions in different asset classes to offset the risks. For example, ECC and RA offer more opportunities to generate a high yield income stream from CLOs and real assets like energy and infrastructure holdings, which will all perform differently during different time periods.

KIO, like many other fixed income funds and leveraged loan funds, had relatively poor performance in 2022. So far, 2023 is shaping up to be a better year for the fund, and with the opportunity that presents itself with the increased distribution plus the upcoming rights offering, I believe that now is a good time to either start a new position in the fund, or add to existing shares if you are already a shareholder, either via the RO or by waiting for the price to drop after the RO expires.

If you have additional information to add to the discussion, please do so in the comments section. I welcome any feedback or dialog regarding KIO or other funds that I have mentioned.

For further details see:

KKR Income Opportunities Fund: An Opportunity To Add Income To Your Retirement Portfolio