RILYN - KKR Says Buy High Yield Bonds As Interest Rates Peak

2023-11-24 07:35:00 ET

Summary

- Global alternative asset manager Kohlberg Kravis Roberts & Co. L.P. is loading up on high-yield bonds and asset-based loans.

- We present our top picks in this asset class, up to 11% yields.

- The current rate cycle is almost over; is your portfolio ready to face rate cuts?

Co-authored with "Hidden Opportunities."

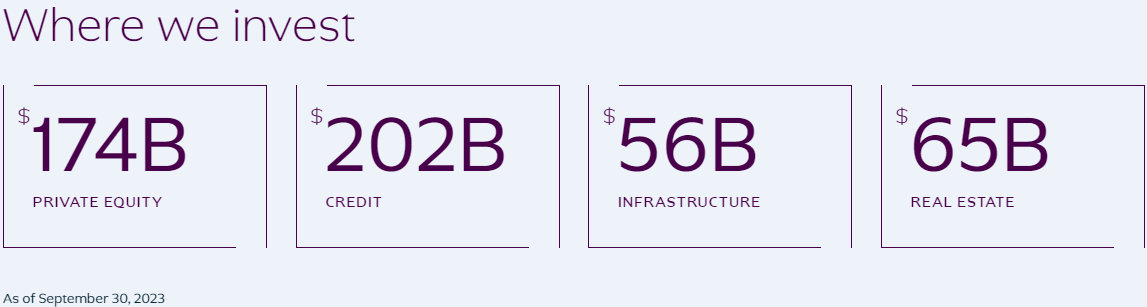

Kohlberg Kravis Roberts & Co. L.P. (KKR) is widely known as one of the largest global asset managers and a very successful one. It is also known as KKR & Co. Inc. and manages multiple alternative asset classes, including private equity, energy, infrastructure, real estate, and credit assets. Source - KKR.com.

{kind=link}

The firm, which manages over $500 billion in AUM (Assets Under Management) with more than $ 200 billion in credit assets, recently said that rates have peaked and that high-yield bonds are a steal. This is enormous! In recent months, the firm has been loading up fixed-income investments.

"We don't believe that the Fed is going to raise rates significantly higher from here." - Jeremiah Lane, KKR's head of US leveraged credit.

With high yields well above their historical averages, KKR expects fixed income to outperform as the tightening cycle is close to its end, and is loading up on this deeply discounted class of securities. Source .

kkr Website

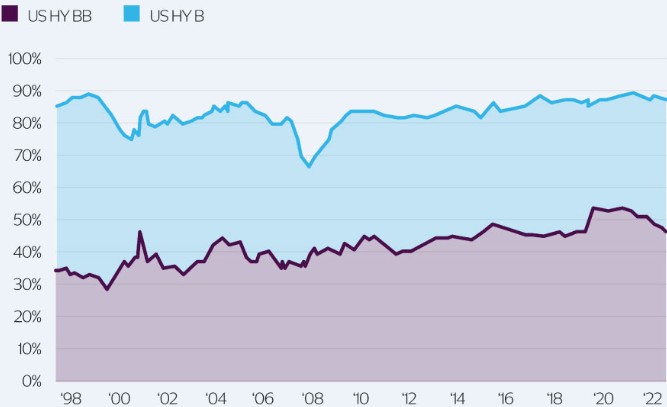

According to KKR's research, over 50% of the high-yield benchmark comprises BB-rated bonds (vs ~29% at its lowest point in early 2001), and over 85% of the asset class is rated B or better.

{kind=link}

Through Quantitative Tightening, our Investing Group has emphasized building a rate-agnostic portfolio. No one can realistically predict where interest rates will be five years from now, but you will still need income for your everyday needs.

"Alan Greenspan (former Chair of the Federal Reserve Board) is a very honest guy. He would tell you that he can't predict interest rates. He can tell you what short rates are going to do in the next six months. Try and stick him on what the long-term rate will be three years from now. He'll say, "I don't have any idea." So how are you, the investor, supposed to predict interest rates if the head of the Federal Reserve can't do it?" - Peter Lynch on interest rates.

Today's elevated rate environment has created a selloff in the high-yield camp, and we are buying with both hands. The fixed-income camp remains explicitly very attractive for high yields now, and for massive capital gains when the rates begin to drop. Preferred stocks and baby bonds are a safer asset class, with better income reliability and price upside possibilities than common stock, and we are loading up. Here are our top picks:

1) Runway Growth Baby Bonds

Runway Growth Finance Corp. ( RWAY ) is a BDC (Business Development Company) providing flexible capital solutions to late-stage and growth companies seeking alternative ways to raise equity.

RWAY's debt portfolio is 100% floating-rate, and the Weighted Average Borrower Loan-To-Value at origination is an impressive 17.6%. The BDC's realized loss rates are minuscule compared to the broader venture debt industry. RWAY lends to more established firms with proven cash flows and avoids risky startups. 80% of the BDC's borrower base is technology and healthcare companies.

We like RWAY's bonds that offer up to 8% yields with CD-beating returns until 2027.

-

Runway Growth Finance Corp. 7.50% Notes Due 7/28/2027 ( RWAYL )

-

Runway Growth Finance Corp. 8.0% Notes due 12/31/2027 ( RWAYZ )

2) B. Riley Baby Bonds

B. Riley Financial, Inc. ( RILY ) is a leading financial services firm specializing in various services associated with Wall Street's day-to-day affairs. RILY's diverse business segment enables the firm to cater to the needs of companies in sickness (liquidation, bankruptcy proceedings) and in health (M&A activity, IPO, debt offerings).

RILY has an impressive insider ownership of over 33% , indicating a solid alignment of management decision-making with the interests of the shareholders. And the company's baby bonds present spectacular income opportunities:

-

5.0% Senior Notes Due 12/31/2026 ( RILYG )

-

5.5% Senior Notes Due 3/31/2026 ( RILYK )

-

6.375% Senior Notes Due 2/28/2025 ( RILYM )

-

6.5% Senior Notes Due 9/30/26 ( RILYN )

-

6.75% Senior Notes Due 5/31/2024 ( RILYO )

-

6.0% Senior Notes Due 1/31/2028 ( RILYT )

-

5.25% Senior Notes Due 8/31/2028 ( RILYZ ).

All of the RILY bonds saw Yields-to-Maturity over 20% recently, and still hold exceptional yields today with a variety of maturities to choose from. We notably like RILYZ, which matures in 2028, offering an 8.8% current yield and ~70% upside to par.

3) OXLC Baby Bonds

Oxford Lane Capital Corporation ( OXLC ) is a CEF (closed-end fund) that primarily invests in CLO (Collateralized Loan Obligations) equity tranches. CEFs are inherently designed to distribute all NII (Net Investment Income) to shareholders, making their bonds and preferred securities safer asset classes. Due to strict regulatory limits on their borrowings and the nature of their business model, the preferreds and baby bonds from CEFs provide very reliable income.

We like OXLC's growing common distribution, backed by its floating-rate portfolio, and see terrific fixed-income opportunities in their baby bonds.

-

Oxford Lane Capital Corp., 6.75% Notes due 2031 ( OXLCL )

-

Oxford Lane Capital Corp., 5.00% Notes due 2027 ( OXLCZ ).

OXLCL matures in 2031 and offers a 7.3% current yield, 8.3% YTM, and ~8% upside to par.

Asset Based Financing

Despite rapidly cooling down, inflation remains above the Fed's target levels, traditional lenders are scaling back aggressively in response to higher rates, and there is high volatility in the banking system. All these factors have increased the need for private ABF (Asset-Based Financing), and KKR is bullish on this segment.

At the end of 2022, the private ABF asset class was 67% larger than in 2006 (and 15% bigger than in 2020). This segment is an attractive way to diversify across the credit universe that is snowballing.

-

Cash flow with collateral backup : Loans are backed by hard and financial assets that generate contractual cash flows. As such, ABF strategies offer compelling risk-adjusted returns relative to other credit asset classes. The collateral both discourages defaults and provides a tangible asset that can be taken and monetized if a default happens.

-

Intra-asset diversification : ABF investments range from residential mortgages to aircraft leases. It also is extended to financial assets like accounts receivable. These are loans that are collateralized by things that can be seized and monetized. This diversification reduces overall risk exposure to a specific asset subcategory.

-

A natural inflation hedge: The value of the collateral strengthens along with the CPI.

KKR expects to see continued demand growth in ABF and sees private capital playing a critical role as banks are increasingly pulling back from consumer and commercial lending and divesting non-core loan portfolios.

"The asset-based lending business is always more active in times of economic stress, such as the present. There are many transactions out there that are better suited for private lenders than banks. And they pay very high returns - such as SOFR plus 600 to 700 basis points." - Dan Pietrzak, KKR's global head of private credit.

Our top pick in this segment is SLR Investment Corp. (SLRC), a unique BDC specializing in sponsor financing, equipment financing, and asset-based lending. Of SLRC's loans, 99.4% are senior secured, and 65.7% carry floating interest rates. From Q4, SLRC will pay quarterly dividends at an 11% annualized yield. The BDC trades at a whopping 20% discount to book value, making it a solid bargain during these uncertain times.

Conclusion

At our service, we don't gamble on predicting future interest rates. Our mission is to construct a dependable income-generating machine to meet and exceed our financial needs across economic cycles. With a diverse portfolio of over 45 carefully selected securities, we aim for an overall yield of +9%. Our income, derived from these deeply discounted securities, will remain robust even in the face of a hawkish monetary policy, and our portfolio is strategically positioned to capitalize on significant upside potential. We are unwavering in our commitment to being buyers of quality income.

Our approach currently resonates with that of global alternative asset leader KKR, which is strategically acquiring fixed-income securities such as high-yield bonds and asset-based loans. KKR believes that interest rates have peaked and is actively positioning itself to benefit from the anticipated decline in rates. With a solid portfolio of discounted high-yield assets, we are ready to ride the wave of capital appreciation alongside KKR, emerging stronger with a wealthy income stream.

For further details see:

KKR Says Buy High Yield Bonds, As Interest Rates Peak