GLD - KMLM: December Futures Rolled Out Analyzing The Changes

2023-12-18 20:03:46 ET

Summary

- KMLM is an ETF that follows a systematic trend-following, volatility-weighted futures strategy in commodities, currencies, and fixed income.

- The ETF has made changes in its exposures and positions this month, including reducing short exposure to currencies by 25% and raising net commodity exposure to 9%.

- KMLM is still fully short bonds despite the Fed, ECB, and BOE all hinting at or calling out "peak rates."

- These changes show how technical trends can diverge from macro trends and could be a short-term pitfall before trends reverse.

Introduction

For the uninitiated, the KFA Mount Lucas Index Strategy ETF ( KMLM ) employs a trend-following, volatility-weighted futures strategy to follow commodities, currencies, and fixed income.

From KFA's website :

KMLM is benchmarked to the KFA MLM Index, which consists of a portfolio of twenty-two liquid futures contracts traded on U.S. and foreign exchanges. The Index includes futures contracts on 11 commodities, 6 currencies, and 5 global bond markets. These three baskets are weighted by their relative historical volatility, and within each basket, the constituent markets are equal dollar weighted.

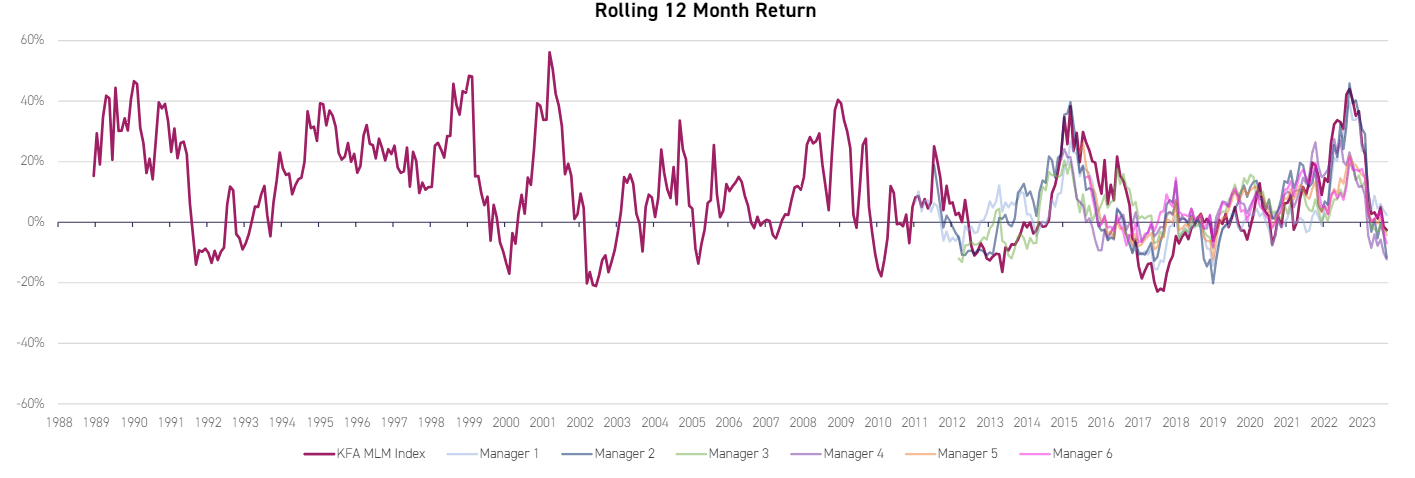

Since its launch in late 2020, KMLM has been providing very impressive returns. It has had a low correlation with other traditional investments, making it an appealing alternative to hold alongside stocks and bonds.

In this column, I am going to analyze the changes in trends that KMLM has identified, how exposures have changed, and which positions have increased or decreased in exposure with the roll to the March expiration futures.

Note: the annual ex-dividend date for KMLM is on 12/28. It will be paying $2.48 per share , establishing a yield of 8.64% at current prices.

Trend-Following

The MLM Index, the underlying instrument KMLM replicates in ETF form, weighs index components by their historic volatility in order to come to a total expected volatility of 15% p.a.

Components are then evaluated by their technical outlook and based on the asset's trend, a position is taken, either long or short. These are re-evaluated periodically and adjusted as trends change.

KMLM is particularly fascinating because it uses the leverage futures provide to give more than 100% exposure to its assets.

These exposures change over time and can change dramatically. Exposure to commodities in November was at 66% and is now at 61% as of December 18th .

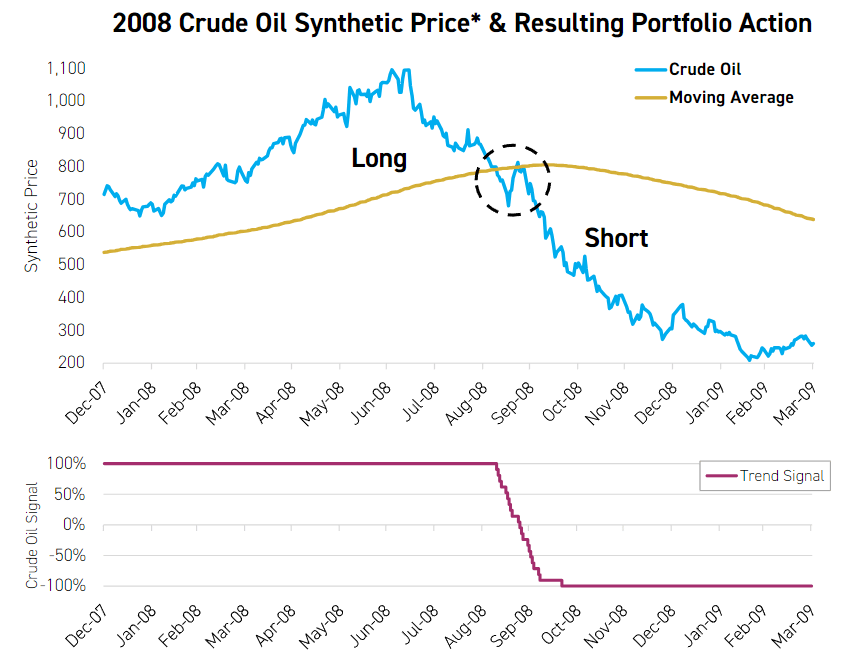

KFA provides a good example of how its trend signal algorithm works to identify when to be long or short an asset.

{kind=link}

If you're interested in learning more about their strategy, they have a presentation that covers it very well here .

Competitors

It is to note that there are several other managed futures funds that compete with KMLM. They all perform differently and are worth checking out independently since they do not follow the same index KMLM does.

The MLM Index itself has been operating since 1988.

{kind=link}

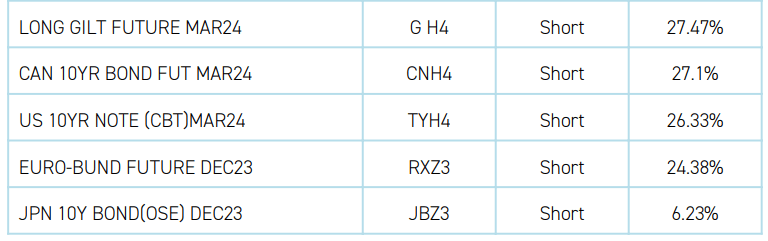

Past Holdings, December Expiration

As mentioned earlier, KMLM has rolled its futures contracts to the March expirations, which means it has had an opportunity to re-adjust its holdings.

Here is how the exposure looked leading into November:

10/31/23 Commodities Exposure

{kind=link}

10/31/23 Currency Exposure

{kind=link}

10/31/23 Fixed Income Exposure

{kind=link}

10/31/23 Top Cash Holdings

{kind=link}

Macros vs. Technical

The macro outlook of bonds and the technical outlook of bonds have diverged in the last two months.

On the Treasury side of the trade, the Fed left rates unchanged in their November and re-affirmed that in their meeting this month as well, even going so far as to being talking of rate cuts next year. US bonds are not expected to continue their downward trend, all else being equal.

I covered how I'm playing "peak rates" with corporate bonds and the 10yr treasury here .

On the Euro-Bund side of the trade, the ECB has signalled that they are still on the "higher for longer" train. They are tempering expectations for rate cuts, just like the Fed is.

The Gilt is no different, with the Bank of England halting rates for the third time in a row recently, holding steady and calling a hold off on future rate cuts as well, but no talk of raising rates at all.

This is the biggest shift that I would want to see in the new rollovers. This kind of shift is macro-based and not technical, so there is no guarantee that KMLM will fall in line. As the technicals shift, KMLM will fall into the trend. The only question is how long it will take.

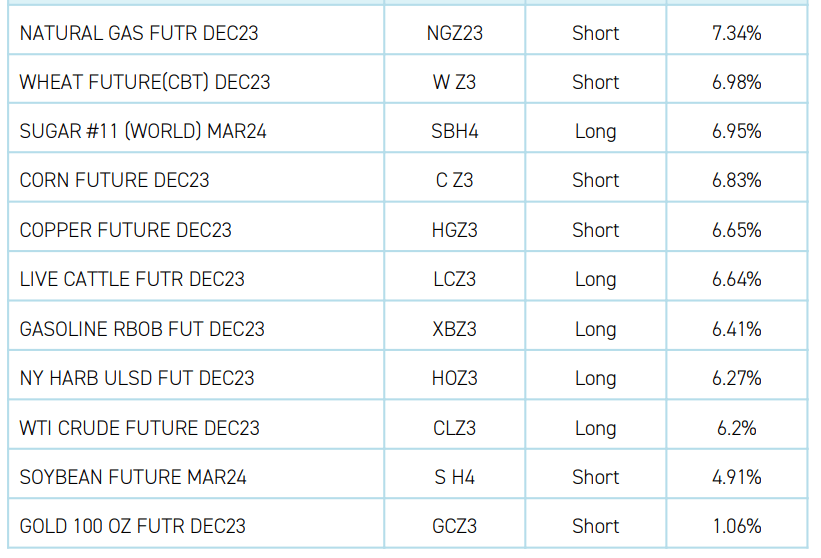

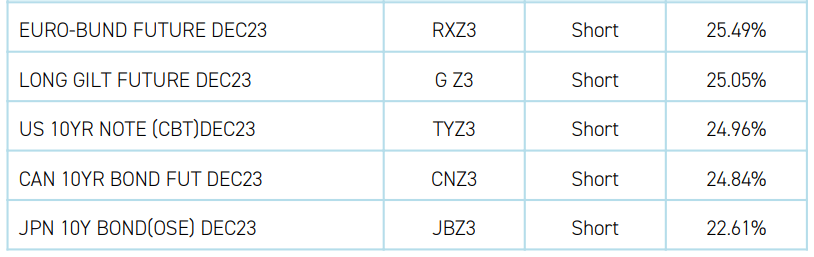

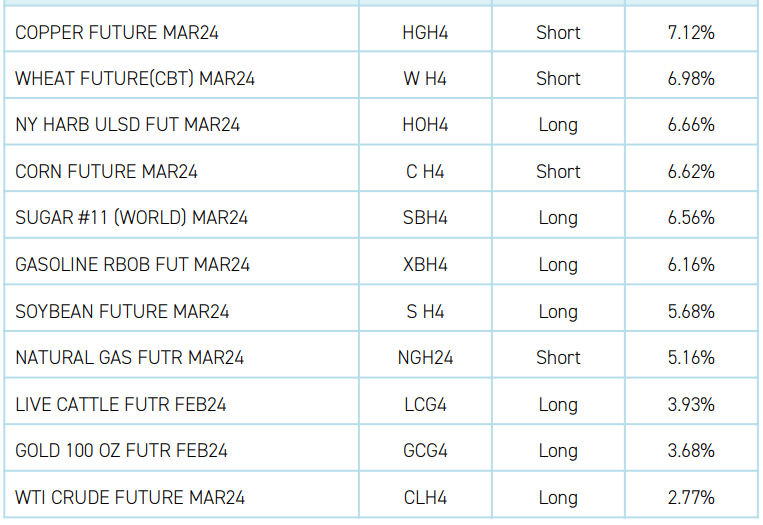

Current Holdings, March Expiration

Without further ado, here is the exposure heading into the new year:

11/30/23 Commodities Exposure

{kind=link}

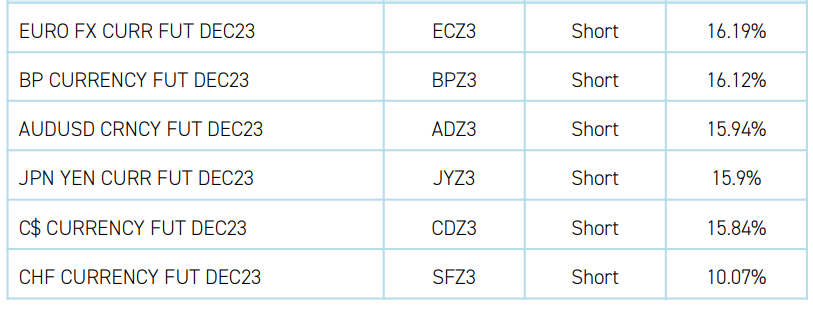

11/30/23 Currency Exposure

Note that these have not been rolled out beyond December yet, although these are not necessarily the same contracts as before and there are allocation changes.

{kind=link}

11/30/23 Fixed Income Exposure

{kind=link}

Major Changes

Long to Short:

- None

Short to Long:

- Soybeans

- Gold

- Swiss Franc

- British Pound

The trend signals have indicated that we are in a trough for some of these markets, and KMLM has not changed any of its long positions to short positions.

The most stark shift is in currencies, which were fully short as an asset class in the previous holdings. That short exposure has decreased by over 25% since.

Conclusion

KMLM has positioned itself to be net long in commodities by 9%, has reduced its short exposure to currencies by 25%, and has remained short bonds across the board despite changing macro conditions.

This disconnect between macro and technical indicators could prove to be a pitfall for investors, but reversing trends can be caught quickly and it may be temporary. One of the advantages of KMLM being passively indexed is that it will catch the trend without having to predict or follow macro trends.

Thanks for reading. If you want to see how I would implement KMLM in a portfolio meant to yield 8% p.a., see my article here .

For further details see:

KMLM: December Futures Rolled Out, Analyzing The Changes