KNRRY - Knorr-Bremse And KION GROUP AG: 2 European Industrials For Great Bottom-Fishing

2023-06-30 11:20:15 ET

Summary

- I discuss the bottom-fishing investment strategy and identify two undervalued German companies as potential targets.

- Knorr-Bremse, a leading manufacturer of braking systems, is highlighted for its solid profitability, market leadership, and potential for significant outperformance.

- I expect a 43%-80% total shareholder returns for Knorr-Bremse over the next three years, based on improving sales, cost control, and macro reversals.

- I also expect good returns for KION AG.

Author's Notice: This article was published on iREIT on Alpha in Mid-June of 2023.

Dear readers,

In this article, I'm going to be showing you two companies that I consider good targets for "bottom-fishing", meaning grabbing businesses/shares at what are essentially very low valuations both in terms of what the companies are worth, and what they have been valued at historically.

I've found over time, that such investments tend to yield incredible dividends - by which I mean not just actual dividends, but dividends in the forms of high capital appreciation/RoR.

So this is a strategy I generally am very favorable towards.

I've identified two "prime-cut" type investment targets in Germany that have been undervalued for some time.

One isn't going to be a surprise.

The other may be somewhat because I haven't given it the same sort of coverage.

Let's get going and let me show you what I have for you here.

Investing/Bottom-fishing in quality companies

So, bottom-fishing is investing in assets that have experienced a decline, essentially. Not exactly rocket science. The "science" or tricky part of the equation is figuring out just when a decline is justified and when it is not.

If you're a bottom-fishing investor like me, I would argue that you're in good company. I don't mean me - I mean investors like Warren Buffet, who are very famous bottom-fishing or value investor. We get categorized into two groups, those that use technical or fundamental analytical techniques.

Obviously, if you know my work, you know I tend toward the latter.

Bottom-fishing can be viewed as a risky strategy in the short and medium term. This is because we tend to invest in companies that are being undervalued by the market, and in my experience and analysis of the markets, most trends show us that going up takes far longer than going down. That means in order to successfully bottom-fish, or value-invest, you have to have patience.

You also need to be a bit of a contrarian. Because people are going to be calling your strategy into question - just as they did with Buffet and his bet with Occidental ( OXY ), for instance. I remember when he did the investment, and many-storied and respectable analysts called it into question.

Who's laughing now?

I've gone from using bottom-fishing and extreme value-investing in perhaps 20-25% of my portfolio to about 50% of my portfolio. My goal is that eventually, I'll "only" engage in this sort of investing activity and picks. I've had a journey from being a "Buy-and-hold-forever" dividend-oriented investor to being this.

Why am I changing up?

Because all of my highest successes and the reason I'm far more wealthy now than I was 5 years ago isn't the super-conservative, safe dividend investments I've made. Those have performed very well. But the reason I've been able to beat the market is that I have included at least a quarter of investments that are quality businesses, but that I bought at dirt-cheap levels of valuation.

The resulting outperformance is what has allowed me a 5-year TSR of over 100% portfolio-wide, in a time when the S&P500 has given around 58.9%.

Granted, this strategy requires you to be far more on your toes, because the risk is that you invest in businesses that either may take a decade or more to turn around - or businesses that despite indications of quality, fizzle out and die instead of reverting.

However, there are many safeguards I employ to prevent that - to date, I haven't had an investment go bankrupt in such a fashion.

The two companies I mean to present today are high-conviction "BUY" for me - I own non-trivial 0.7-1.2% in each, and I mean to "BUY" more.

Let's see what we have.

1. Knorr-Bremse ( KNRRY )

So, we begin with a 115+-year-old German industrial stalwart and world leader. Knorr-Bremse AG is a German manufacturer of braking systems in both rail/rolling stock systems and commercial vehicles.

It's the world's leading manufacturer of all things braking systems in key segments.

It has 31,000+ employees, and over €7B in revenues.

The company is a sector outperformer with leading, 90%+ percentile gross margins, and mid-70 percentile net margins of over 6%.

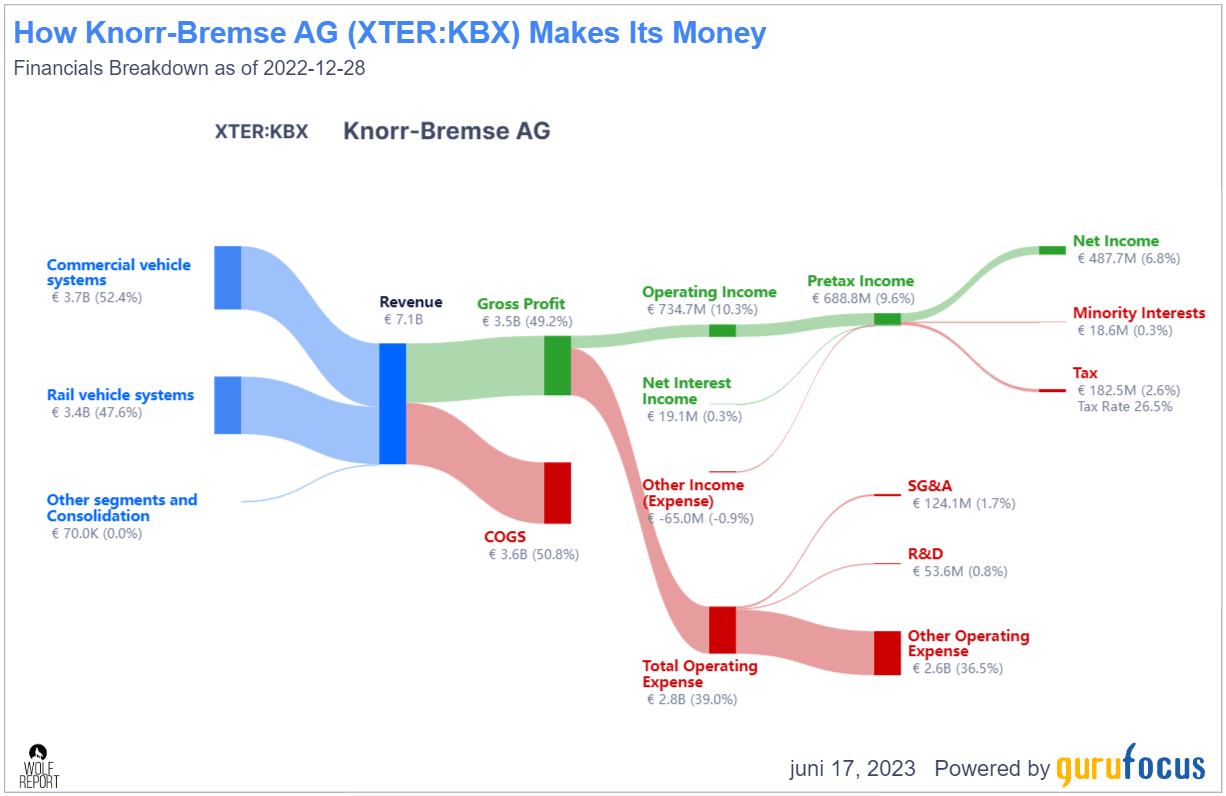

{kind=link}

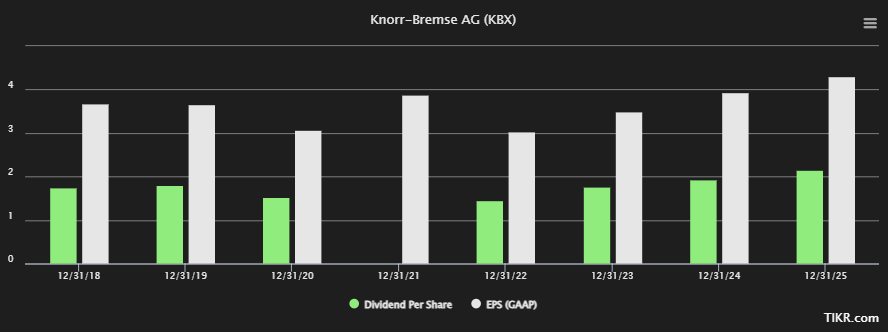

Knorr-Bremse revenue/net (GuruFocus)

All vehicles/rail need brakes - and no company comes close to even the same coverage as Knorr does. The native symbol is KBX, and this is the one I would go with if you want to invest - the ADRs are relatively illiquid for this business.

The company's profitability is solid. The company also has no net debt , so any interest rate risk is really quite moot/small. Business trends for the company are solid. Yes, inflation is putting pressure on the bottom line, but this is neither unique nor has it in any way made the company's trends unfavorable or long-term risks.

{kind=link}

KBX IR (KBX IR)

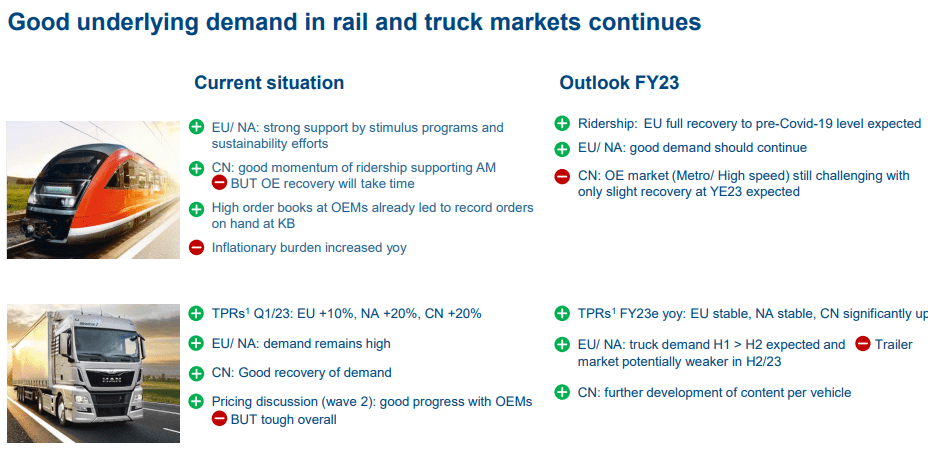

There's a strong underlying demand, which has led to a well-filled order book with over €7.1B in backlogs, and over €2.1B the latest quarter. FCF and cash flow conversion are still negative for the time being, but EBIT margins are 9-13% for the quarter. The company is continually investing around 3-4% of sales.

The main challenge at this time is inventory normalization. Due to supply constraints and market challenges, KGX has stock built-up, leading to higher net working capital, and impacting company results. Receivables are also higher due to some deferred payments from certain customers. It's "bubbling" a bit due to an unstable macro.

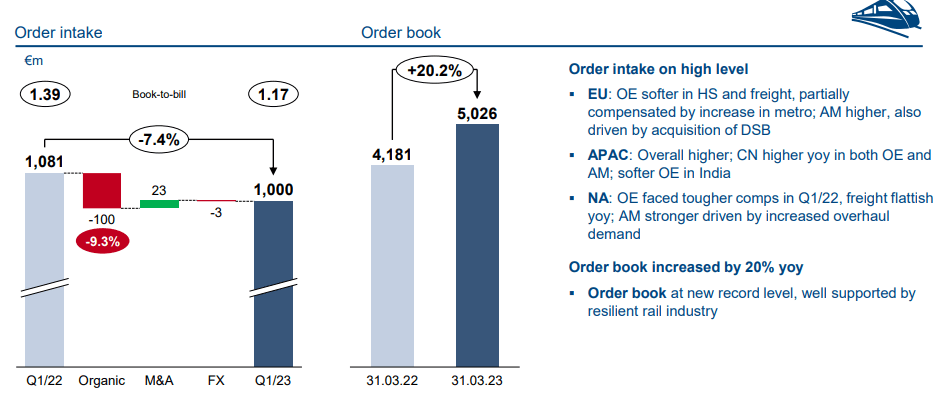

However, underlying trends in things like railway, are absolutely solid.

{kind=link}

KBX IR (KBX IR)

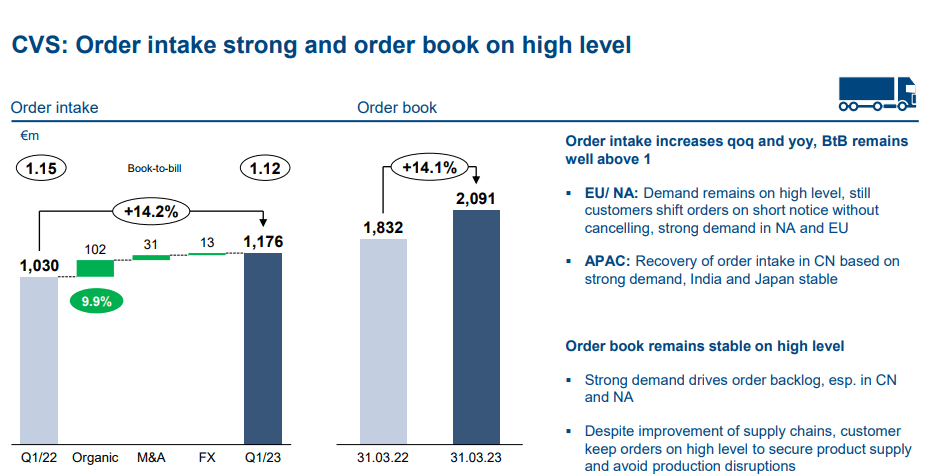

...and the CVS segment, meaning commercial vehicles, is also showing strong top-line growth and indicators.

{kind=link}

KBX IR (KBX IR)

As you can see, generally speaking, top-line trends are very much intact - and its costs and inflation that is currently, as with many industrials, causing a bit of a hiccough.

KBX has been lower. Back in October, when I started buying, we were at below €50/share for the native. However, at €66/share we're still at a level that I based on valuation trends, would consider being extremely attractive. The company has confirmed its 2023E guidance, meaning a slight revenue growth, a slight potential EBIT decline or flat EBIT margins, and significantly better cash flows on the FCF side - though these assumptions are based on no further supply chain shortages, which might or might not happen.

The company is restructuring its Chinese Segments as well as North America, and the company expects to offset all inflationary costs by price increases and cost measures , keeping margins mostly intact.

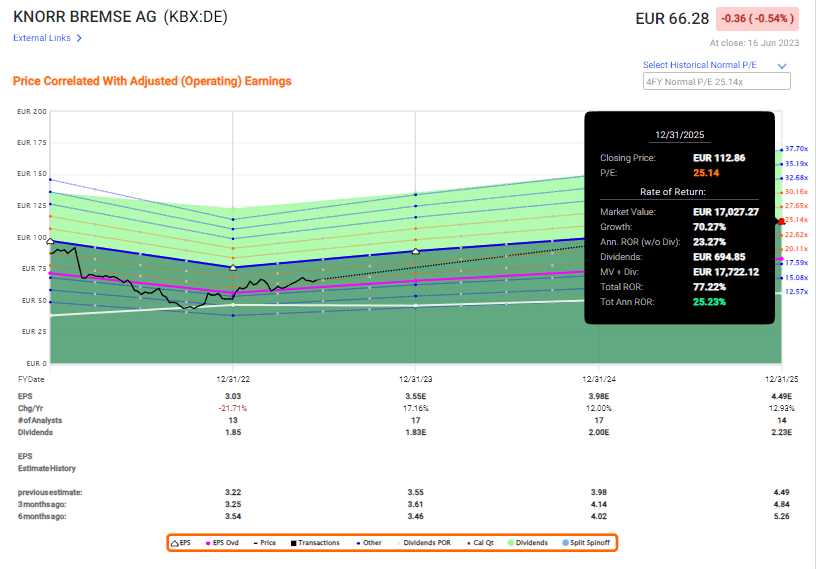

Based on an EPS growth rate of 14-15% over the next 3 years, after troughing with a negative 21.7% EPS decline in the last fiscal, I expect KBX to significantly outperform. Even if you were to only value it at 20x, compared to its 25-27x average, you're still paying 15% per year, or 43% TSR until 2025. And that is, as I see it, the bearish case.

The reason this company is so highly valued is its market leadership and its historical profitability. The company has European dividend logic, meaning annual and very much based on earnings. I believe we'll see a ramp-up in EPS in the double-digits as forecasted by S&P Global analysts we see here, based on increased sales, improving cost control, and efficiencies as well as a reversal in macro.

{kind=link}

KBX Forecasts (TIKR.com)

That is the reason why I don't just expect base or bearish-case RoR, I'm comfortable forecasting this at a potential 23-26x P/E, which caps the upside not at 45%, but at around 80% on a 3-year basis.

{kind=link}

KBX F.A.S.T Graphs (F.A.S.T graphs)

Knorr-Bremse is an A rated German industrial with a market cap, even at this level, of over €10B. It's the world leader in a key business segment. It's well-managed and forecasts solid profitability.

I see the potential for massive outperformance, and I'm already up over 20% in my position.

So, I'm adding more, and I call this my first "BUY" here. My PT for Knorr is at least €100/share.

2. KION AG ( KIGRY )

KION is likely a stock you're already more familiar with compared to Knorr. It's the world leader in industrial truck solutions in EMEA, and the global #2 in the same segment. It's #1 in global supply chain solutions and can report an annual order intake climbing toward the €13B on an annual basis.

This has seen some pressure over the past year or so, but the problem with KION and what has caused it to fall is not top-line growth or lack thereof. The company in fact has a well-filled orderbook and excellent demand trends. Still, it's down to around €11.1B in 2022, with a. new intake of slightly above that.

So both of these businesses are not unlike in size. Where KION differs is that it has seen a far deeper crash than we see in Knorr, and there is some real, meaty EPS pressure and some margin issues here.

Where I differ is that I believe these issues to be very temporary. The upside for KION is, therefore, much higher, though we forecast the companies to roughly the same premium.

KGX IR (KGX IR)

The troubles that KION faces are broad-based and not unique to KION as a company. We saw many of those issues reappear, or clear up during 1Q23. The company had a strong start to the year, with a good-sized order intake and a 2% revenue increase, but margins are anything but solved. With a -8% YoY adjusted EBIT, we're not seeing 2.6% EBIT, but we're seeing 5.6% compared to usual double digits. Still, results were up significantly quarterly, so the recovery has at the very least begun - at least that's how I see it.

We'll want to keep a very close eye on the coming quarters, but at the same time not over-interpret potential short term weakness trends that appear during those quarters. What I mean is that even if we do decline in 2Q or 3Q, that's not going to change my thesis or approach for this company, because I think 2-3 years in the future when it comes to both of these two businesses - or more.

Recover-mode companies are interesting cases. If you're at a high conviction that a recovery will take place, you're on the "ground floor" to making some incredible gains, at least potentially.

If you're also not reliant on a high dividend - as I am no longer - and can "swallow" the sentiment that you'll need to wait for your returns, well, then you're in an even better position.

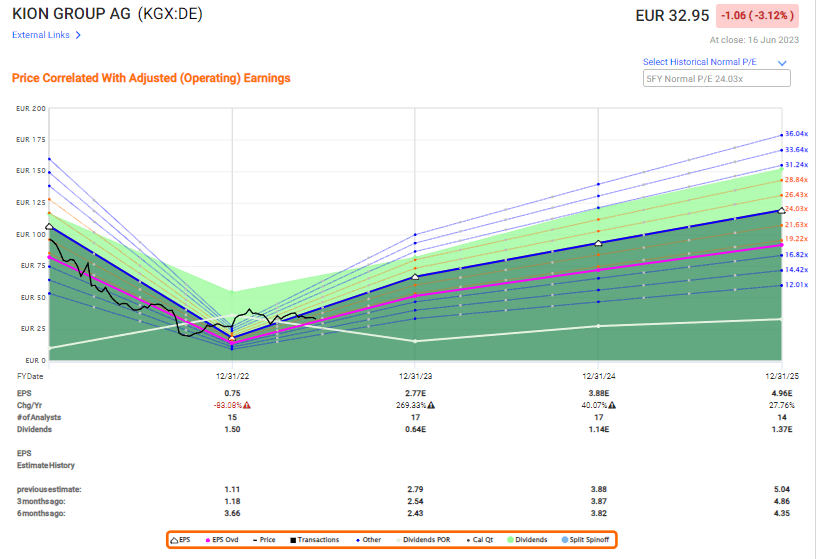

The upside forecasted for KION can be summarized in this graph.

{kind=link}

KION upside (F.A.S.T graphs)

If KION was anything except a world leader in its field, I'd be more worried. As it is though, I'm not. However, it's crucial to point out that these two companies do differ somewhat.

KION has crashed far more than Knorr, for good reason. The upside is higher, but the risk is also somewhat higher due to the timeframe involved.

Knorr has A credit rating. KION has BBB-.

Both companies have a dividend, but for KION it's actually low/cut for this year. However, neither company are yield-monsters.

Both companies have experienced significant declines - but Knorr has an easier time coming out of it because it has declined less. KION's margins have really declined to levels where they are no longer sector leaders/among leading percentiles, and this is something the company needs to revert.

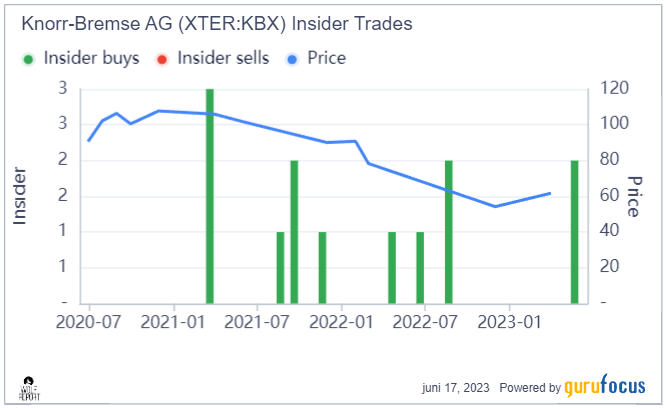

KION has seen a fair amount of insider buying, which can be a sign of faith/conviction. However, the same is true for Knorr, and even on a larger scale.

{kind=link}

Knorr Insider Buying (GuruFocus)

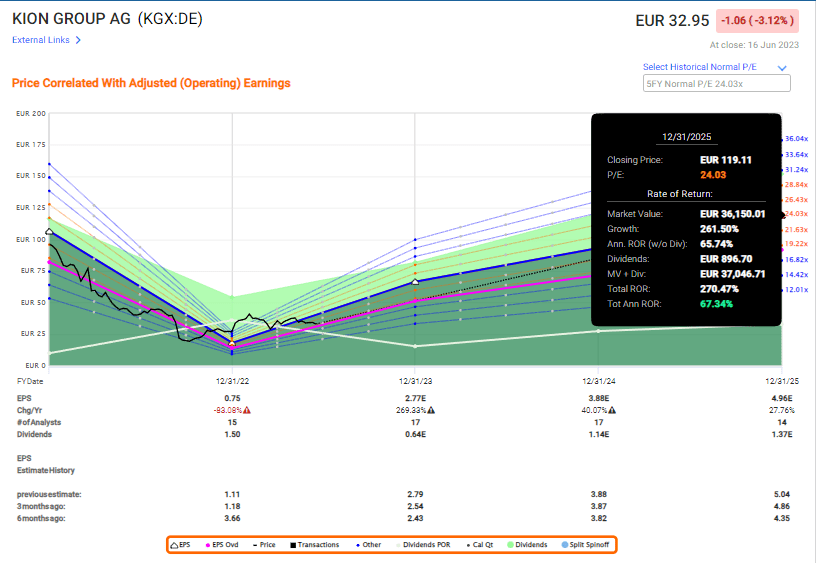

However, I still maintain that KION has the higher ultimate upside of the two investments. A normalization in KION AG will bring about returns of 270% , or 67.4% per year. Knorr is nowhere near this.

The only reason I bring this up is that I actually consider such a development to be potentially possible. But even in the case of lower multiples, if these forecasts turn out accurate, you're in the triple digits.

{kind=link}

KION AG Upside (F.A.S.T Graphs)

Wrapping Up/Stances

My firm conviction is that both of these companies will be in substantially better positions in 2-3 years than they are today. If you do not share this conviction, I'd be curious to hear your case against it - just remember what you're in that case arguing against, and the arguments that you base such a stance.

If you're in agreement with this stance, then the only question I view as relevant is "how high" things will go from there. That's a different question.

Perhaps we'll only see the companies barely make double-digit valuation jumps. Perhaps they'll perform less than advertised or forecasted. However, even in the case of "only" 15-20x P/E, these businesses will outperform market averages as they typically trade and are forecasted.

Another way to put this is that the likelihood of losing your capital is low - that's my view, not an official recommendation. But I do view both of these companies, based on what they actually do and what we can expect from them going forward, as extremely safe investments despite what can be seen as very volatile trends.

KION is a "BUY" for me, and I currently have a PT of €78/share.

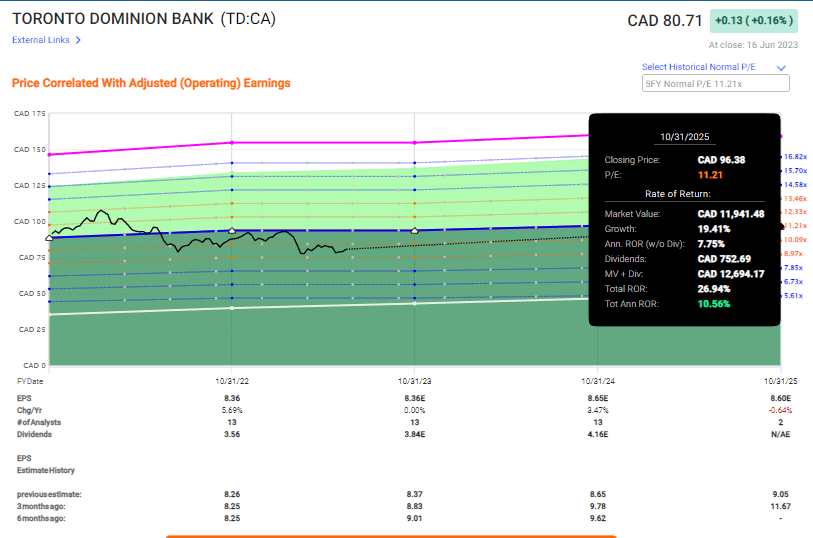

Different investments have different upsides. These companies have a different upside and investment profile than say, Toronto-Dominion Bank ( TD ), which is another company I recently purchased shares in. Here, I don't expect anything beyond a double-digit RoR and a good yield. I do buy for yield, and this is an example of that.

{kind=link}

TD Upside (F.A.S.T graphs)

I believe a linchpin to your success is a well-diversified, both in currencies and investments, portfolio of stocks, and other investments.

These two companies are good examples of how I think about this.

Questions?

Let me know.

For further details see:

Knorr-Bremse And KION GROUP AG: 2 European Industrials For Great Bottom-Fishing