USAC - Kodiak's Weak IPO Is Our Opportunity

2023-07-25 07:38:36 ET

Summary

- Kodiak's IPO was weak due to being released just before a major summer holiday.

- Yet, the firm is in a strong business that produces solid ongoing cash flows.

- Near-term expected drivers include positive coverage from major Wall Street firms and declaration of a dividend.

Kodiak's IPO was a Dud

Kodiak (KGS), is North America's third largest compression company.

Company Roadshow Presentation

That they just held their initial IPO on July 3rd, the day before the July 4th holiday, was probably poor timing. The 16.5 - 18.4 million share IPO went off at only $16 per share instead of the $19 - $22 originally estimated by management. It also closed the day down in price with less than 800k shares having traded hands. This was a bad kickoff for KGS, but a potentially good opportunity for us.

The previous estimated $20.50 midpoint, resulted in shares being priced at about 8.1x EV run rate EBITDA, and $1,342 - $1,415 / HP. That made sense as it was about the same as AROC's current EV/EBITDA valuation (8.1x EV/run rate EBITDA) but higher than their $899/HP (as you will see, KGS is a bit less risky). At $1.64 estimated dividend (40% of expected DCF) KGS would have also offered a reasonable 8% dividend yield at that price. Instead, Kodiak's poor initial showing, combined with our analysis preparation prior to IPO, is giving us the chance to pick up shares at a relative bargain.

Yet Kodiak has a Good Business with a Strong History of Producing Solid Cash Flows:

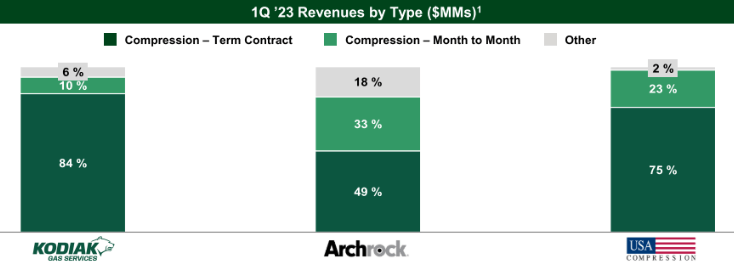

Kodiak's strategy of leasing large horsepower compression units (81% >1,000 HP) in ancillary gas regions like the Permian is similar to Archrock ( AROC ) and USA Compression Partners ( USAC ). It tends to mean gas keeps getting produced, and their units keep getting utilized, even if the price of gas falls. This is because producers still value the oil being produced, and thus also continue to produce ancillary gas even when gas prices make its production less economical.

Additionally, Kodiak contracts contain meaningful cancel/move charges just like USAC and AROCs, albeit with a meaningfully higher proportion of multi-year contracts (84%).

{kind=link}

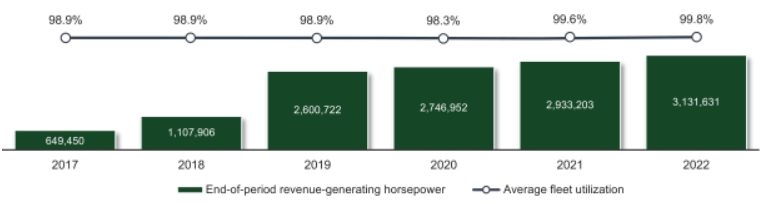

The net result is Kodiak has enjoyed a significantly higher fleet utilization than either AROC or USAC.

{kind=link}

AROC's fleet utilization for 2020 - 2022 averaged about 85%. USACs was about 86%. As you can see above, KGSs never dipped below 98%.

This higher utilization results in more stable revenue and discretionary cash flow 'DCF' during downturns. It is a significant benefit that reduces risk.

KGS Adj EBITDA average 2021-2022 Adj EBITDA margin of 58% was in between AROCs relatively poor 48% (they used to have a greater proportion of smaller HP units and more on spot) and USACs stronger 62%. However, what matters most to the investor is the per share bottom line.

{kind=link}

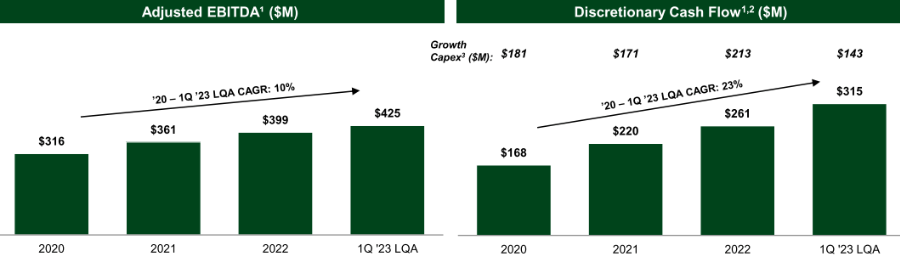

In the roadshow slide above, KGS indicates a $315 million run rate DCF. This equates to $4.10 per share (=$315 million / 76.7 million shares). Which in turn implies a quite interesting 24% forward DCF yield at today's $17 price (= $4.10 / $17 offering price). If as indicated verbally in the roadshow, 40% of DCF is paid out as a dividend, that also implies $1.64 being paid out to shareholders annually (a 9.6% dividend yield on cost 'YoC' at $17 per share). That dividend declaration would be a driver as it is a pretty attractive dividend relative to AROCs 6%. It would also be comparable to USACs 10.9%, even though USAC pays out almost 100% of DCF whereas KGS is much less risky with an expected to pay out only 40%.

Kodiak's Debt is also Reasonable:

Kodiak proforma leverage ratio post IPO is going to be similar to USACs without their preferred, about 4.6x (note the management roadshow slide below assumes the $20.50 IPO price. At a $16 IPO less debt gets paid off, so I estimate Kodiak's Net Debt / EBITDA should be revised to about 4.6x).

Company Roadshow Presentation

Trading Considerations:

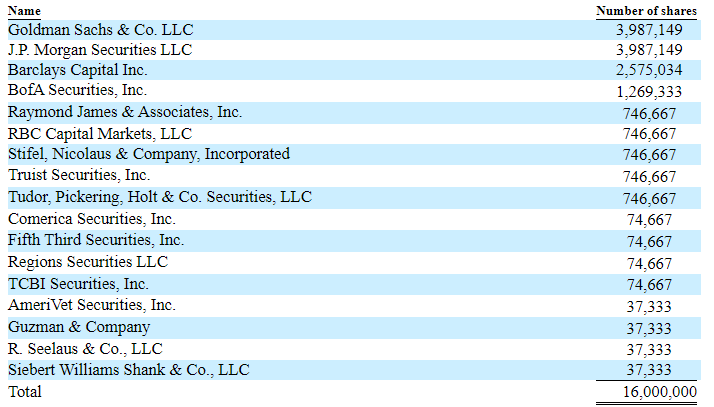

The underwriters (Goldman Sachs, JPMorgan, Barclay's, BofA, etc.) net cost for the shares after discount was $15.10. Predictably they stopped selling at a small spread above their cost ($15.30) and then the stock started to rise. The underwriters needed to unload 16 - 18.5 million shares and typically seek to do so in the first month. Volume indicates they should have been able to have done so by now. The rise from the $15.30 initial IPO selling pressure created low, to the current price of $17+ also indicates this underwriter selling pressure is likely over. Yet the stock remains a deal that investors should seriously consider.

{kind=link}

The underwriter list above is a who's who of large, well known investment banks. Thus, over the coming weeks I expect various large, well known Wall Street firms to initiate positive coverage. This IPO is under the radar right now, but it probably won't be a month from now.

Management Alignment and Insider Ownership:

EQT, a private equity firm which specializes in infrastructure, will remain a major >70% holder of KGS post IPO. Senior management consist of Robert McKee, the CEO and 2011 founder of Kodiak, Ewan Hamilton the CFO, and Chad Lenamon the COO. All three got class B shares (23.8k, 3.3k, 1k respectively) through their compensation arrangements which vest at 20% per year. These B shares are convertible to common. Based on the $4.4 million which was booked as expense for these units, each unit is probably convertible into 10 shares of the common. Most management also purchased shares at $16 with their own money in the IPO.

{kind=link}

Take Away

Bottom line, what we investors should care about the most is first what we benefit from ($4.10 DCF) vs. what we have to pay ($17 stock price). Second we want to know how likely we are to continue to benefit (cash flow stability). On that front, with KGS we are looking at a firm that is likely to enjoy more stable revenue than either USAC or AROC, similar debt, and pay a high USAC like dividend yield, despite a low AROC like payout %. Near term drivers include Wall Street initiating positive coverage, and the KGS declaring a dividend.

For further details see:

Kodiak's Weak IPO Is Our Opportunity