FLKR - Korea Fund: Brighter Skies Ahead

2023-12-24 22:09:48 ET

Summary

- After a topsy-turvy year, Korean stocks are ending 2023 on a high.

- The 2024 micro/macro setup looks interesting as well, particularly at current valuations.

- Playing Korea through an active fund like KF has its drawbacks, but there are mitigating factors worth considering.

The JPMorgan-managed ( JPM ) Korea Fund's ( KF ) two key tech names, SK Hynix ( HXSCF ) and Samsung Electronics (SSNLF), have extended their stock price rallies into the back half of the year on the back of a cyclical memory semiconductor (DRAM and NAND) rebound. Helped by a tech upcycle, Korea's exports are similarly gaining steam in both value and volume terms – despite ties to a slowing Chinese economy. Beyond tech, other Korean equity themes also screen quite attractively. Most notably, electric vehicle ('EV') battery manufacturers, the key KF performance drag this year, remain poised to benefit from market consolidation as EVs move further down the battery cost curve and increasingly penetrate the mass market. Higher up the value chain, Korean auto manufacturers also continue to deliver healthy bottom lines and are well on track with their long-term EV roadmaps – positives that don't seem to be reflected in their current valuations.

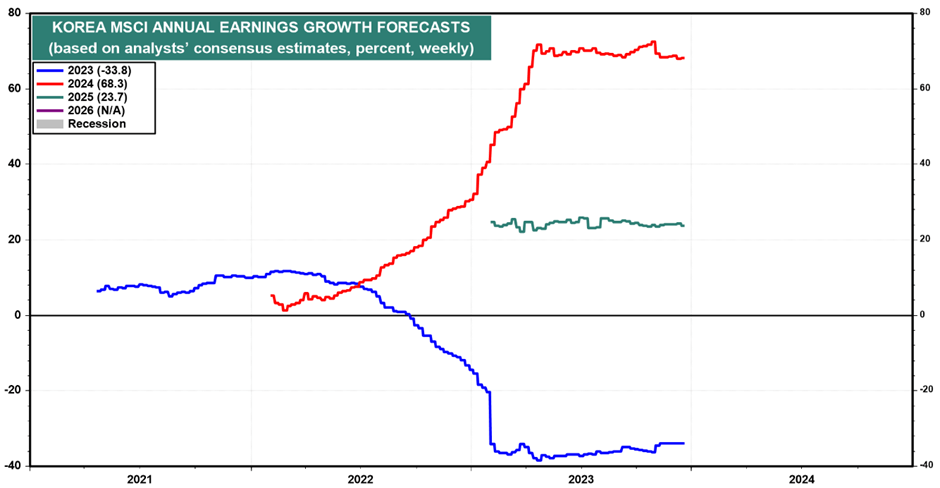

Even in a worst-case scenario where KF's export-oriented stock portfolio gets dragged down by external headwinds next year, there's ample buffer on the valuation side. For one, the KF portfolio is currently priced at 8.6x earnings and a ~20% book value discount – very reasonable relative to consensus expectations for 2024/2025 earnings to rebound by +68%/+24% (albeit off steep earnings declines in 2023). US Treasury yields are also down and the Fed has effectively committed to a pivot, so currency pressures from capital outflows are less of a risk; in turn, the central bank ('Bank of Korea') has its all-clear to ease. A potential index inclusion catalyst for government bonds is also worth watching out for ahead of the next FTSE World Government Bond Index (WGBI) review early next year; approval could mean significant passive inflows and a structurally lower Korean risk-free rate (also higher equity valuations).

{kind=link}

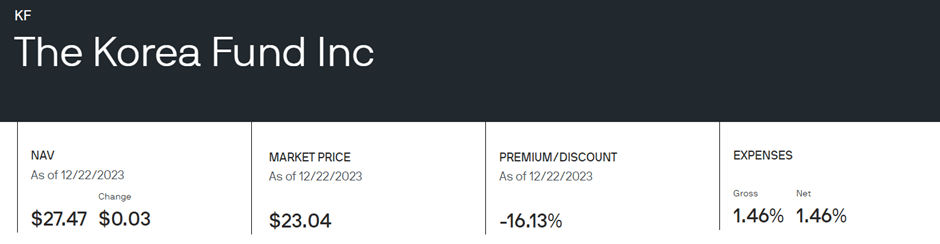

Low-cost passive funds like the Franklin FTSE South Korea ETF ( FLKR ) or the iShares MSCI South Korea ETF ( EWY ) remain the lowest risk ways to capture Korean upside, but those willing to take the current expense ratio/NAV discount tradeoff on offer with KF could also come out ahead. For now, the manager has made little effort to lower its expense ratio or step up distributions, and its steep mid-teens % net asset value [NAV] discount, while slightly lower than when I last covered the fund, reflects this. That said, a buyback commitment, should the fund underperform its benchmark, offers some welcome support. Long-term-oriented investors also get 'free' optionality as rising closed-end fund activism could eventually put pressure on the discount down the road. Either way, I remain upbeat on KF heading into an action-packed 2024.

Korea Fund Overview – Tech Concentration Moves Higher; Pricey Expense Ratio Intact

At the manager level, not much has changed for the actively managed Korea Fund relative to last quarter. This remains a bottom-up fund targeting long-term capital growth (vs its benchmark MSCI Korea 25/50 Index) via a concentrated portfolio of high-conviction names. Assets have risen in recent months to $134m, helped by a rebound in late Q4, though the expense ratio remains high at ~1.5% (up from ~1.1% last year). Given passive alternatives like EWY and FLKR charge ~0.6% and ~0.1%, respectively, the current fee structure is a concern.

{kind=link}

The KF portfolio has narrowed slightly to 55 holdings and, as a result, also features higher sector concentrations. Information Technology has seen its allocation increased by about three percentage points to 38.4%, while Materials exposure is further cut to 12.4% after a particularly dismal year-to-date performance. Financials (12.4%) is now the joint second-largest allocation, followed by Consumer Discretionary (down to 10.9%) and Communication Services (8.4%). With the cumulative top-five sector contributions rising to ~83% of the overall portfolio, KF's fortunes remain closely tied to a handful of key sectors.

{kind=link}

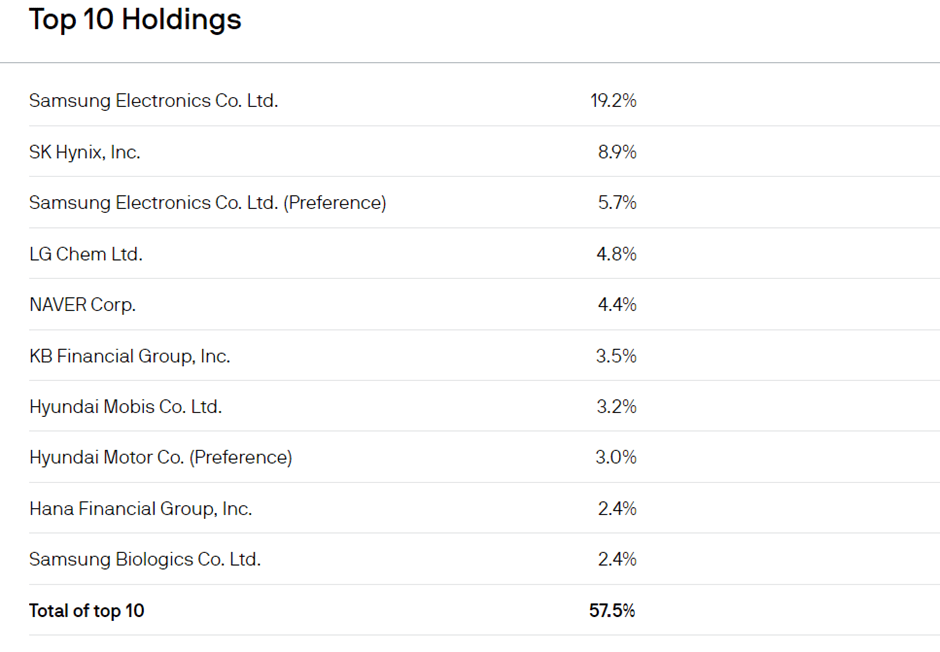

KF's single-stock allocation is still dominated by semiconductor/mobile leader Samsung Electronics, with the common stock and preferred stock holdings increasing to 19.2% and 5.7%, respectively. Korea's other tech major, SK Hynix (HXSCF), also gains a bigger slice of the portfolio at 8.9%. Other major holdings include LG Chemical (LGCLF), internet company NAVER Corp (NHNCF), and KB Financial Group (KB). While KF isn't as top-heavy as it used to be, the ~58% portfolio contribution from its top ten holdings means investors should still be mindful of the concentration risks here.

{kind=link}

Korea Fund Performance – Narrowing Performance Gap; Mind the Volatile NAV Discount

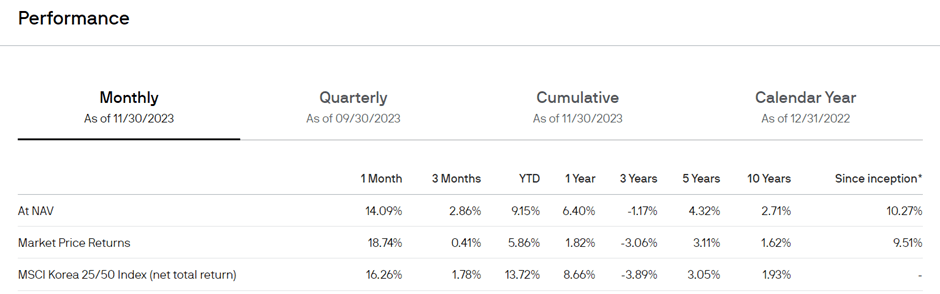

Following a challenging start to H2 for Korean stocks, a steep decline in US Treasury yields has triggered a November/December rally, keeping KF well on track for a YTD gain. Relative to the benchmark MSCI index, on the other hand, KF has begun to make inroads. While the fund's overweights in materials stocks like LG Chemical remain a drag on its near-term performance, its outsized exposure to memory chips (via Samsung and Hynix) has allowed its NAV to outperform over the last three months. In turn, KF has narrowed its YTD underperformance slightly (+9.2% vs +13.7% for MSCI Korea 25/50) and widened its annualized three-year performance gap (-1.2% vs -3.9% for MSCI Korea 25/50).

{kind=link}

In contrast with a relatively decent NAV performance, the fund's widening market price discount means investors have underperformed over most timelines. The one-year gap is particularly striking at +1.8% vs. +8.7% for MSCI Korea 25/50, while over the last decade, investors have realized ~30bps of annualized underperformance in market price terms (vs ~80bps of outperformance in NAV terms).

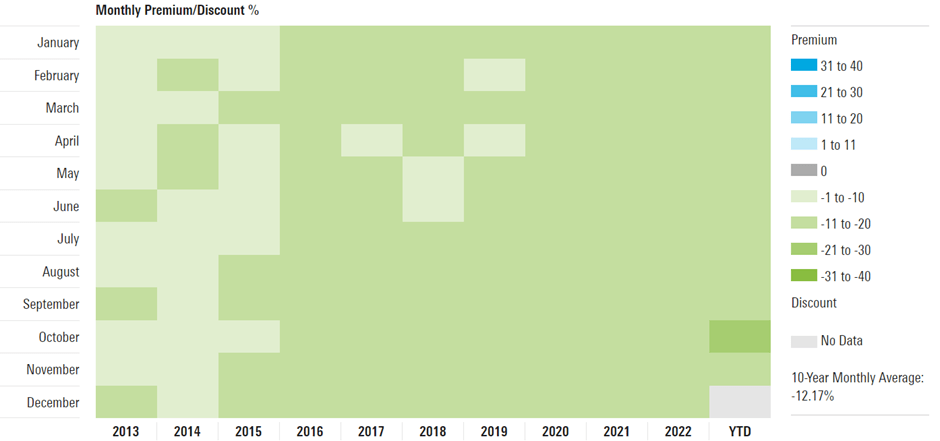

Of note, the NAV discount has been particularly choppy in Q4, widening to >21% at one point before narrowing back to the mid to high teens %. The culprit was likely technical (rate differentials vs. US) rather than fundamental, though longer-term, more subpar performance will be an issue, along with the fund's overly high expense ratio.

{kind=link}

For now, there isn't a clear catalyst for the NAV discount to narrow outside of the manager's commitment to a performance-linked buyback (up to 25% of outstanding shares). Yet the Board's recognition of its high fee % is a positive step ( "your board monitors the Fund's total expense ratio closely" per the 2023 annual report ). Plus, with activist activity also increasing across the closed-end fund universe and plenty of low-hanging fruit available to address the discount (e.g., fees and distribution), investors get essentially 'free' optionality at current prices.

Brighter Skies Ahead

It's been a mixed year for Korean stocks, but following a Q4 resurgence, KF, alongside the broader Korean market, now looks poised to end the year firmly in the green. Heading into 2024, the fundamental and technical setup remains compelling. The all-important tech sector is on track for a cyclical rebound, while decelerating inflation and a dovish Fed mean valuations may also be set for a boost from rate cuts later next year.

The risk here is Korea's exposure to external headwinds, given its economy and large caps are heavily export-oriented. Yet, the negatives are already in the price – relative to MSCI Korea consensus estimates for high-double-digits % earnings growth in 2024 and low-double-digits % in 2025, the current ~8x forward earnings multiple for KF's portfolio seems very reasonable. Plus, there's the prospect of additional upside surprises from a potential sovereign bond inclusion catalyst and potentially even fiscal loosening ahead of parliamentary elections next year.

{kind=link}

While KF has its drawbacks (high expenses, low distributions), there's still interesting value at the current mid to high-teens % NAV discount - particularly given the performance-linked buyback 'floor' and potential activist optionality longer-term. For patient, longer-term-oriented investors interested in Korea exposure, this fund is still worth a look.

For further details see:

Korea Fund: Brighter Skies Ahead