KHC - Kraft Heinz: The Risks Of A Narrative-Driven Share Price Rally

2023-12-13 09:40:14 ET

Summary

- Kraft Heinz stock has been on a tear in recent months, after sell-side analysts have rushed to upgrade their forecasts.

- Free cash flow upside for 2024, however, remains limited and this limits any potential upside from current levels.

- Topline growth is also likely to continue on its downward trajectory over the coming months which creates additional risks for shareholders.

Kraft Heinz ( KHC ) stock has been on a tear recently after the company reported slightly better than expected results in early November.

{kind=link}

As a result, the huge performance gap between KHC and Consumer Staples Select Sector SPDR® Fund ETF ( XLP ) has closed in a matter of weeks.

Even though pricing remained strong during the past quarter, the company does not offer anything fundamentally different from what we have seen over the past few years. Margins have improved slightly, but as we will see later on, this is also nothing to get excited about provided that you have a medium to long-term investment horizon.

The main reason for the sharp increase in KHC share price, however, has been linked to the flurry of sell-side analysts who rushed to upgrade the stock.

{kind=link}

These upgrades have gravitated around Kraft Heinz valuation, market share and improving efficiency within the company.

... gaining market share, improving efficiency, and has a healthier balance sheet

Source: Seeking Alpha

Although all these are positive signs, they do not justify a buy rating over the medium or long-term. As we will see later on, the gains in market share are in certain product categories and overall volume declines will remain a headwind for KHC.

In terms of how the stock is priced, the current free cash flow yield of 5.6%, is hardly attractive given how direct competitors are priced. For example, peers like J. M. Smucker ( SJM ) and Kellanova ( K ), which are experiencing similar troubles with their capital allocation processes (see here and here ) are trading at much higher free cash flow yields. At the same time the high quality businesses of General Mills ( GIS ) comes at an even lower price tag than KHC.

{kind=link}

Cash flow estimates for the next year are quite optimistic and this results in a significantly higher forward free cash flow yield of 7.8%.

Seeking Alpha

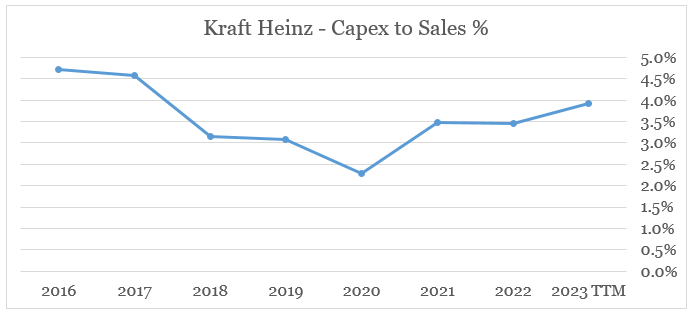

Although profitability could improve slightly in FY 2024, topline growth is likely to slow down (more on that later). In terms of capital expenditure, Kraft Heinz currently spends around 4% of sales on capex which is roughly in-line with the historical average.

{kind=link}

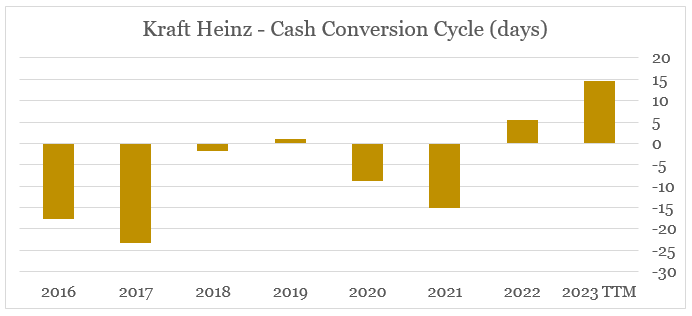

The one key area where we could see an improvement is working capital improvements. After years of negative cash conversion cycle, Kraft Heinz experienced a sharp increase in its working capital requirements over the course of FY 2022 and 2023.

{kind=link}

The key driver of this increase has been the falling inventory turnover which to an extent has been in response to the increased volatility.

(...) we do have, compared to historical levels, higher inventory coverage in average in raw and package materials, also, which is normal because we're also trying to build the buffers given all the volatility and uncertainty.

Source: Kraft Heinz Q4 2022 Earnings Transcript

In recent quarters, Kraft Heinz has also experienced a mix change towards higher gross margin products in taste elevation which usually require higher levels of inventory.

{kind=link}

Having said all that, Kraft Heinz ability to sustainably improve its free cash flow going forward appears limited and given the optimistic analyst estimates for FY 2024 there is a significant risk of worse than expected results for next year.

Lower Growth Rates Ahead

In terms of topline growth, we have seen a gradual decline in Kraft Heinz organic revenue growth throughout 2023 as the dynamic between pricing and volume growth has worsened.

Growth in the International segment has remained strong, but the relative size of the business unit is small when compared to North America.

prepared by the author, using data from quarterly presentations

The impact of pricing within North America has also fallen sharply in recent months and in Q3 2023 stood at slightly above 5%, down from 13% in Q1 of the same year.

prepared by the author, using data from quarterly presentations

The volume/mix dynamic has stabilized somehow as the year progressed, but it remains in negative territory.

prepared by the author, using data from quarterly presentations

When we compare all these metrics in North America to the one we saw in 2022 (see below), we could see the degree to which pricing and volume have deteriorated.

Kraft Heinz Investor Presentation

During the last conference call, Kraft Heinz management did not provide any solid guidance on volumes but reiterated that it should turn positive at some point next year.

So we said, and it happened that volume would improve in Q3 sequentially to Q2, and it did. It improved in Q4 versus Q3. And at some point in 2024, the volumes will turn positive .

Source: Kraft Heinz Q3 2023 Earnings Transcript

Therefore, should pricing continue on its current trajectory, organic growth is highly likely to turn negative in the first half of 2024. The likelihood of this happening should not be underestimated as Kraft Heinz management has also made clear that they will prioritize profitability.

(...) we are not going to just be chasing volume , we are going to be looking for what is the way for us to drive profitable volume (...)

Source: Kraft Heinz Q3 2023 Earnings Transcript

The lower amount of products sold on promotion is also a clear indication that the focus is on brands with high price premium that require less incentives for continued customer purchases.

{kind=link}

All that makes sense, if a company wants to move up on the value-added chain and gradually improve margins. In the case of Kraft Heinz, however, the company's brands portfolio is not as strong to make this strategy a viable one beyond the short-term. In order to do that sustainably, the company would need more truly international brands that are leading in high margin segments of the Packaged Foods sector. In my view this significantly increases the probability KHC making a large acquisition in 2024 which will be a clear indication of the inferiority of the company's current brand portfolio and strategic positioning among the other large cap names in the sector.

Conclusion

The recent rally in Kraft Heinz share price could easily prove to be unsustainable as it was largely driven by sell-side analysts. The stock is priced for perfection as far as free cash flow growth in 2024 is concerned and this limits any potential upside. At the same time, the challenges for the long-term business strategy have not gone away. With all that in mind, I still see Kraft Heinz as one of the least attractive picks within the large cap Packaged Food space.

For further details see:

Kraft Heinz: The Risks Of A Narrative-Driven Share Price Rally