SRVR - Land REITs: Disinflation Headwinds

2023-07-12 10:00:00 ET

Summary

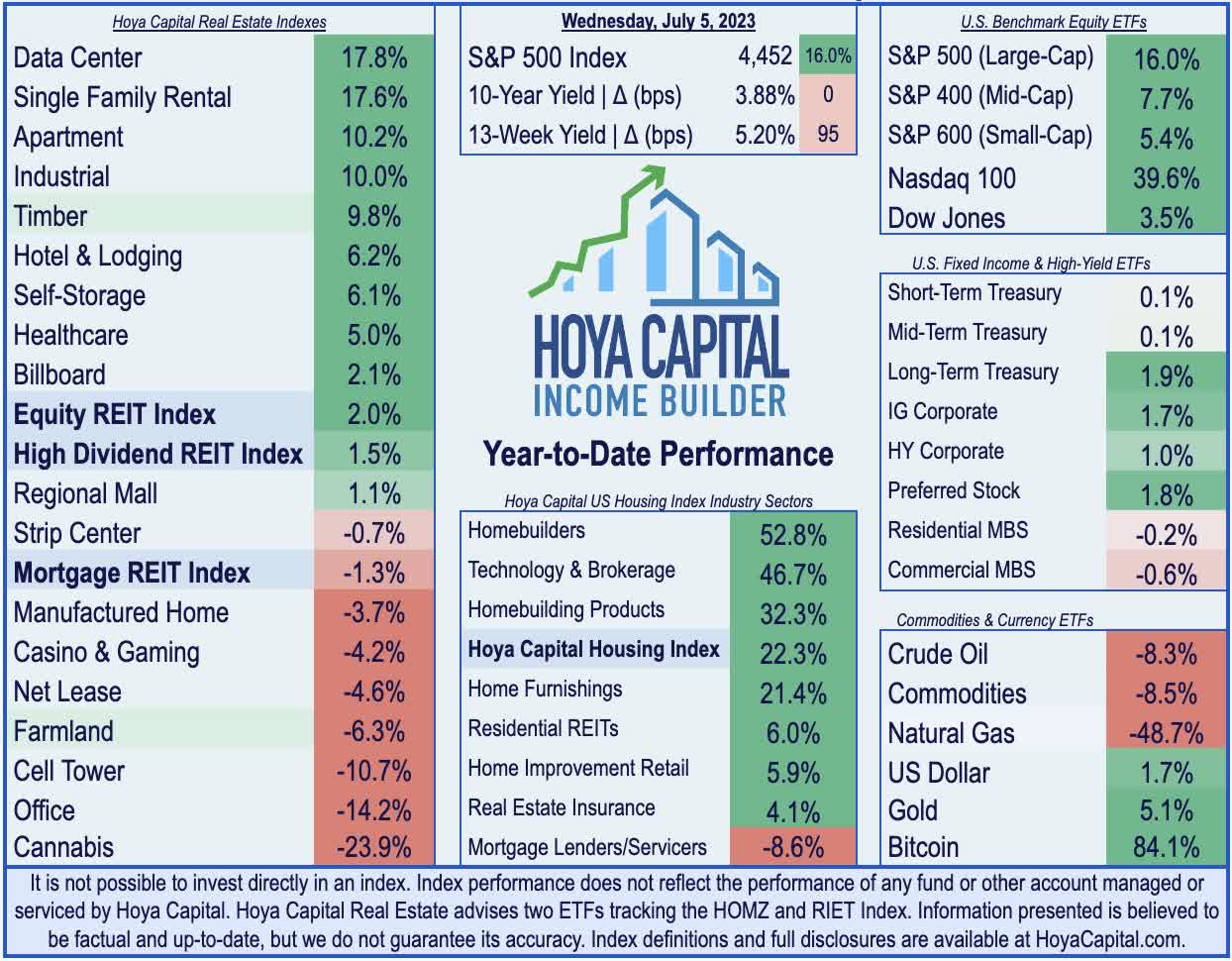

- One of the hottest "inflation hedges" during the pandemic, land REITs have fallen out-of-favor as rising rates and normalizing supply chains have created disinflationary - and even deflationary - headwinds for commodities.

- While services sector inflation remains sticky, goods-related inflation has fallen dramatically over the past nine months, with some inflation reports now showing goods deflation levels typically seen only in recessions.

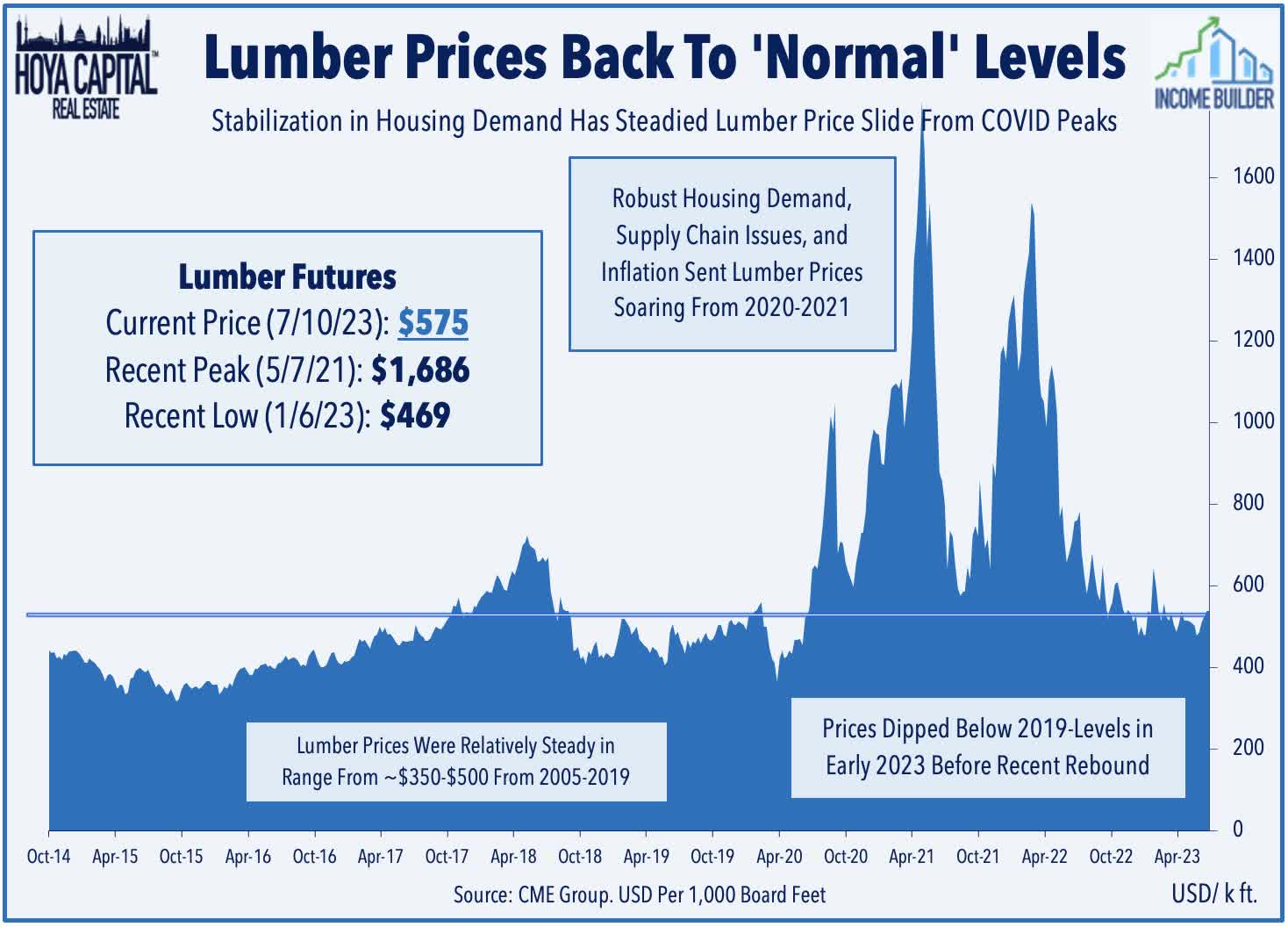

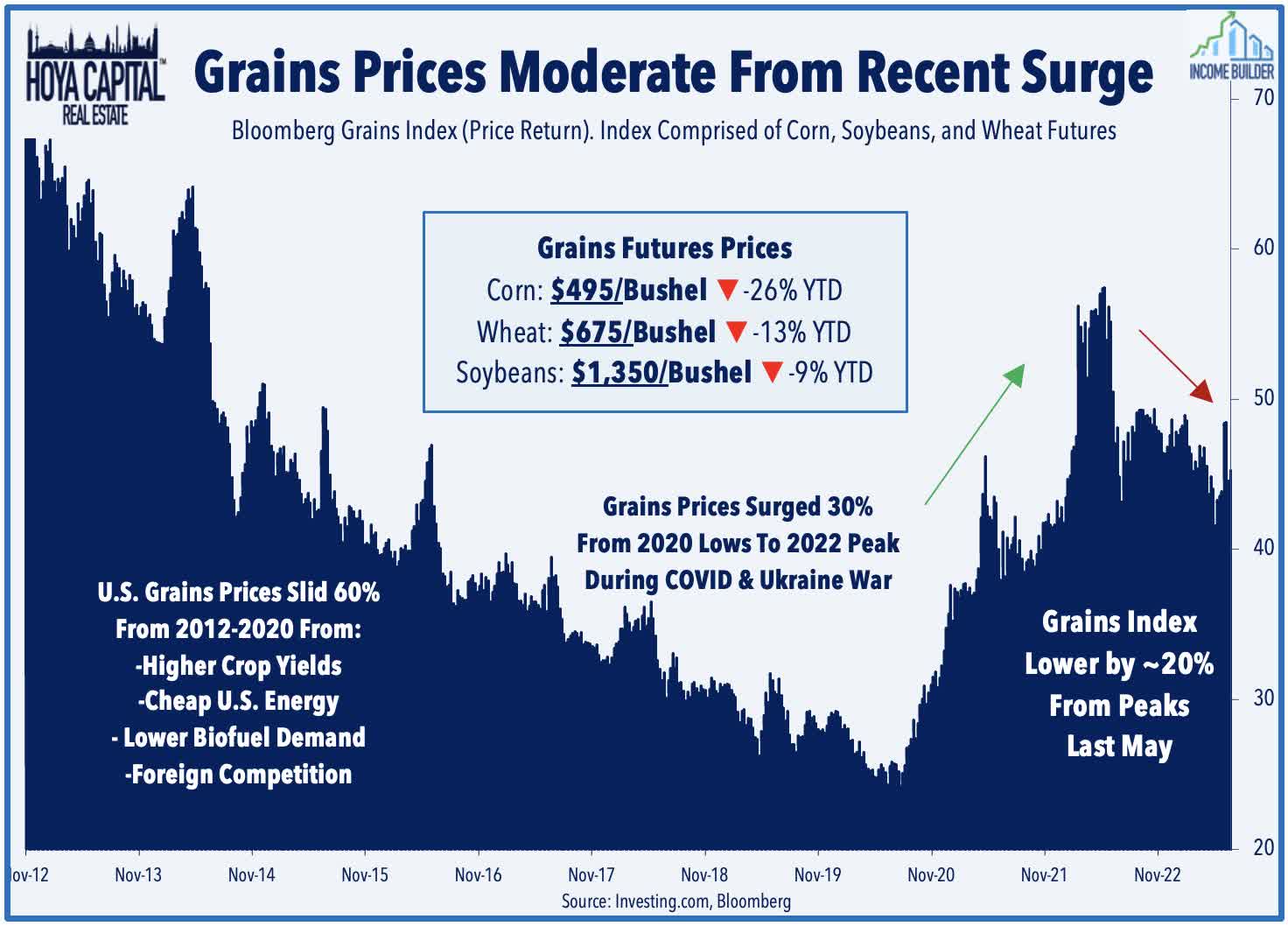

- Grains prices have declined 25% from their 2022 peak despite the ongoing Russia/Ukraine War, but remain 50% above 2019-levels. Lumber is lower by more than 50% from their pandemic-era highs.

- Farmland REITs have been pressured by a "triple whammy" of headwinds - lower crop yield due to extreme weather, lower crop prices, and significantly higher interest rate expense - but the selloff has brought valuations to reasonable levels.

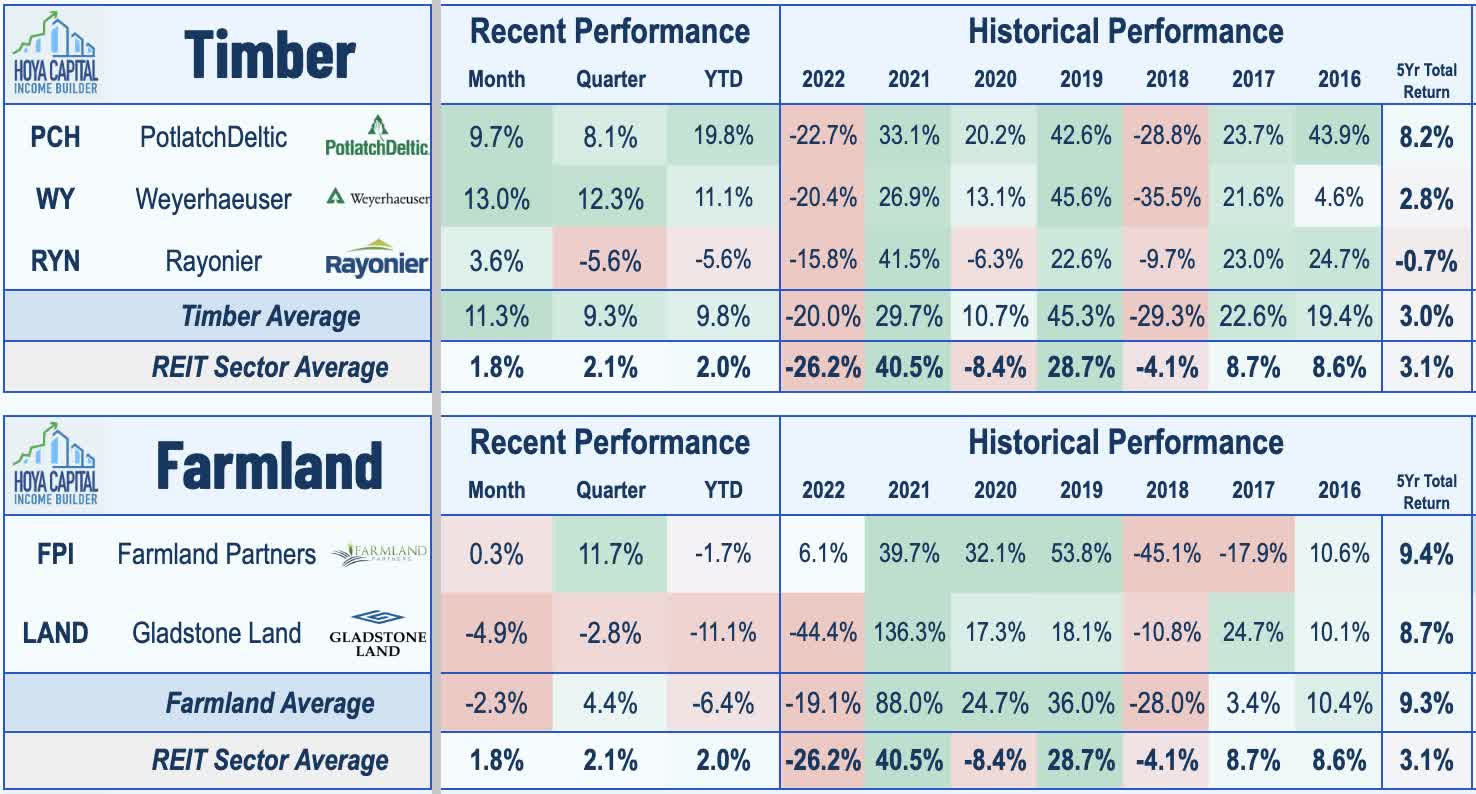

- Timber REITs have surged 20% since May as the U.S. housing industry emerged from its year-long recession. Long-term fundamentals remain attractive given pent-up housing-related demand, but near-term upside now appears limited.

REIT Rankings: Timber & Farmland REITs

{kind=link}

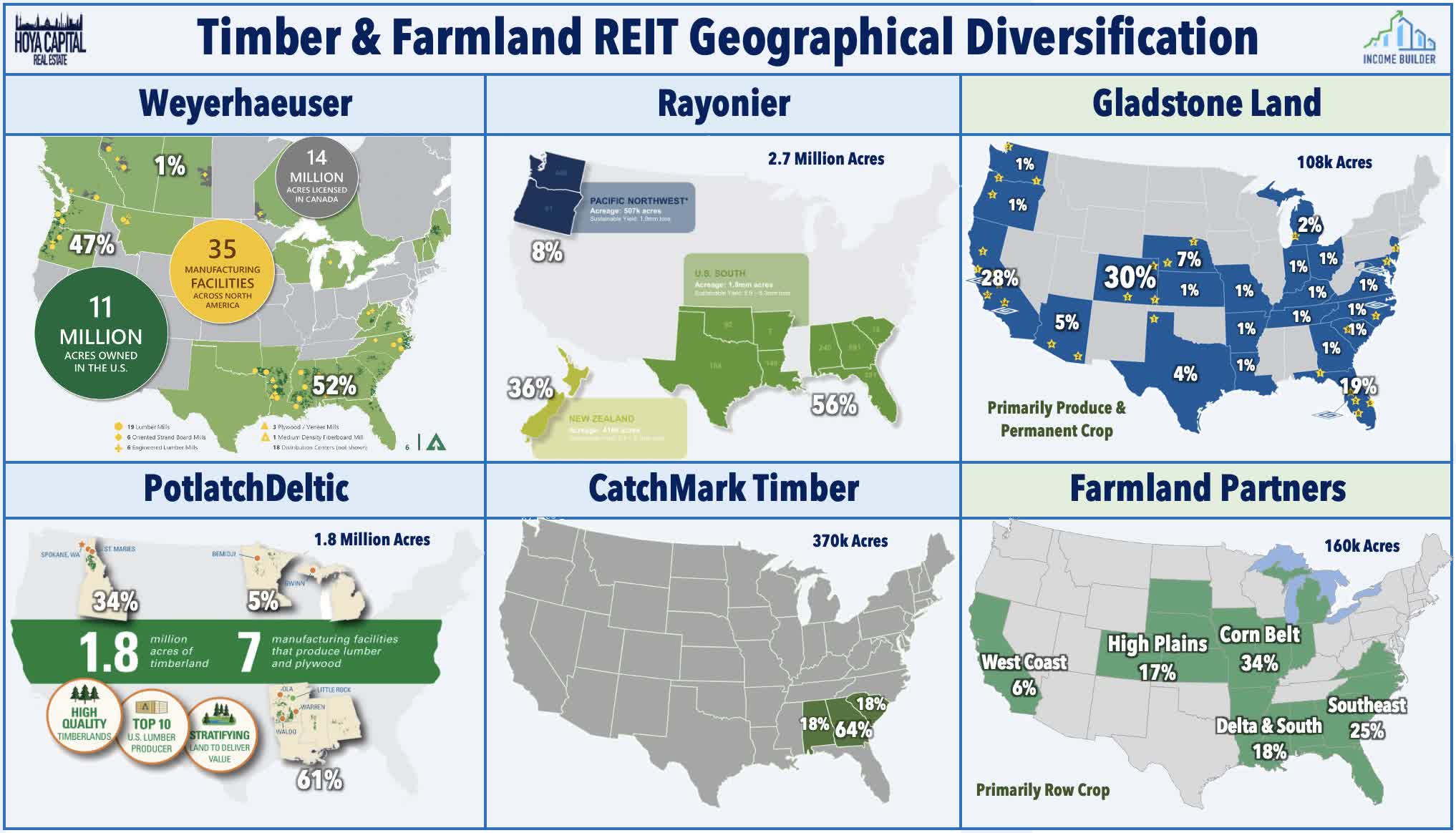

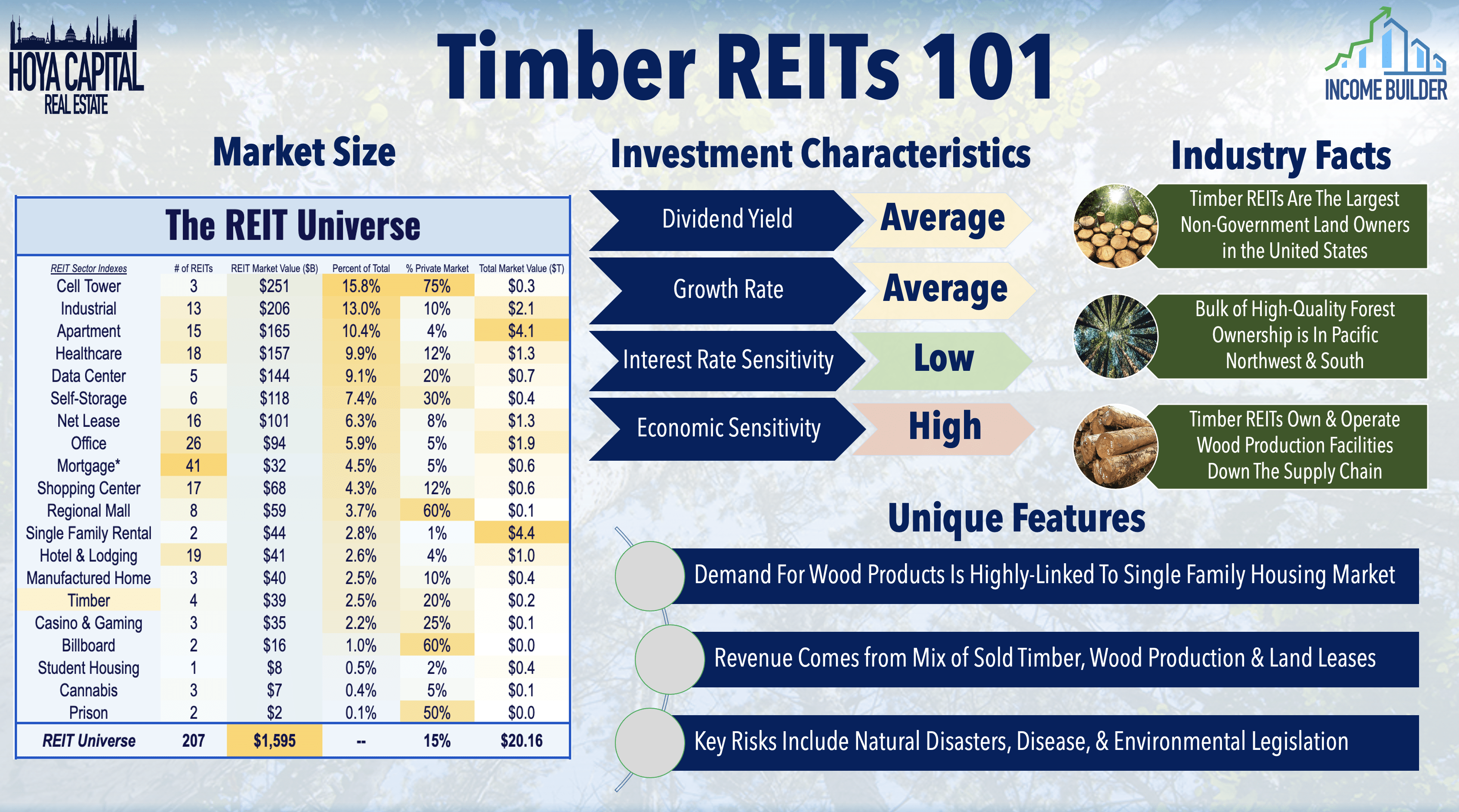

One of the hottest "inflation hedges" during the pandemic, land REITs have fallen out of favor of late as higher interest rates and normalizing supply chains have created disinflationary - and even deflationary - headwinds for commodities. Grains prices have declined 25% from their 2022 peak despite the ongoing Russia/Ukraine War but remain 50% above 2019-levels, while lumber is lower by more than 50% from their pandemic-era highs. In the Hoya Capital Timber REIT Index , we track the three timber REITs which account for roughly $35 billion in market value and collectively own 16 million acres: Weyerhaeuser ( WY ), Rayonier ( RYN ), PotlatchDeltic ( PCH ), and CatchMark Timber ( CTT ). We also track the two farmland REITs in the Hoya Capital Farmland REIT Index , which account for roughly $1.2 billion in market value: Gladstone Land ( LAND ) and Farmland Partners ( FPI ).

{kind=link}

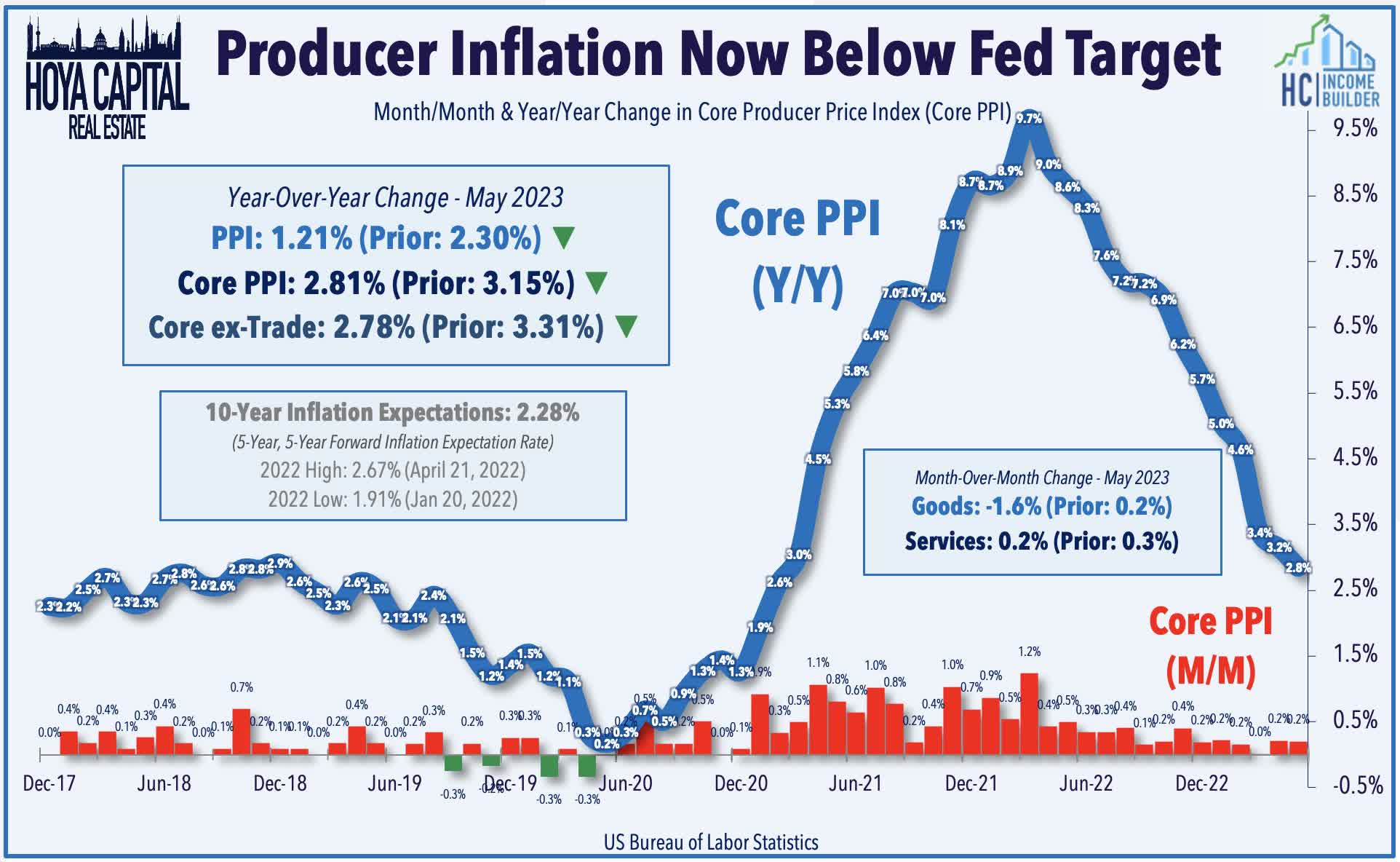

While services sector inflation remains sticky - due in large part to the delayed recognition of record-high rent inflation from mid-2021 through mid-2022 - goods-related inflation has fallen dramatically over the past nine months, with some inflation reports now showing goods deflation levels typically seen only in harsh recessions. Last month, the headline Producer Price Index declined 0.3% in May - the fourth monthly decline in six months - dragging the annual increase to just 1.1%, its lowest reading since December 2020. We observed similar trends of cooling price pressures in recent PMI data with both the ISM Services and Manufacturing PMI showing that inflationary pressures declined to the lowest-levels in more than three years in June to levels that are now below that of the 2016-2019 average - a period in which CPI inflation averaged less than 2%. S&P highlighted one survey respondent who commented, "In this environment, pricing power is fading rapidly. Prices charged for inputs by suppliers are now falling at a rate not seen since 2009."

{kind=link}

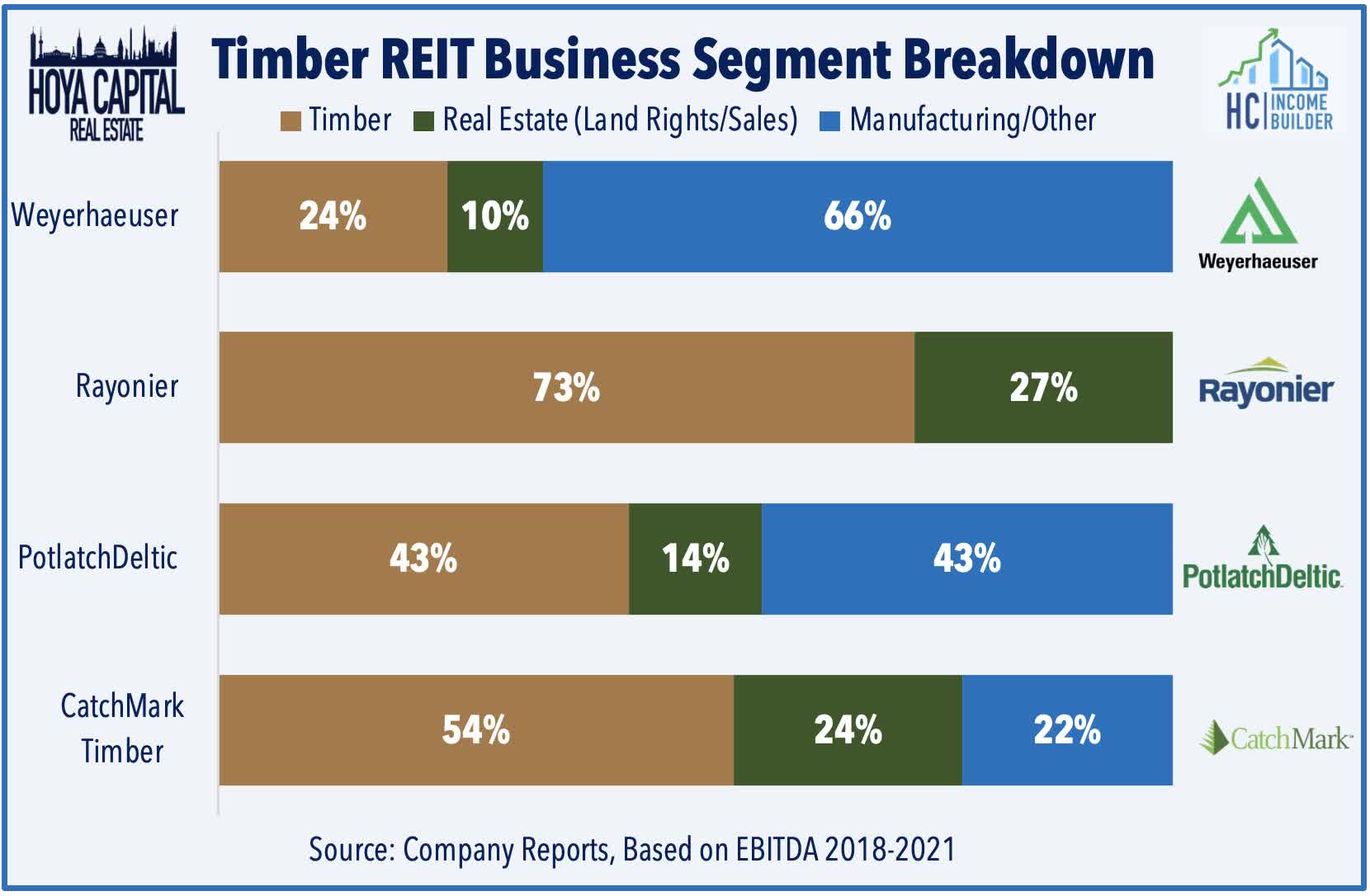

While both lumber and grains prices have retreated significantly from their pandemic-era highs, both commodities remain well above the pre-pandemic levels, faring better than energy and industrial-related commodity groups amid generally favorable supply-demand conditions for North American agricultural commodities. Timber REITs own and/or manage over 30 million acres of US timberlands - more land than the smallest five states in the US combined. Notably, Weyerhaeuser and PotlatchDeltic are considered to be more "vertically integrated" timber REITs as they each have significant business operations along the lumber supply chain - not only timberland ownership but also in lumber production and manufacturing - transforming the raw timber into usable construction materials. As a result, these REITs tend to be more sensitive to changes in lumber prices and short-term fluctuations in demand. Rayonier and CatchMark , on the other hand, are more "pure-play" timberland owners and as a result, have seen more muted effects - both on the upside and downside - from volatility in lumber prices.

{kind=link}

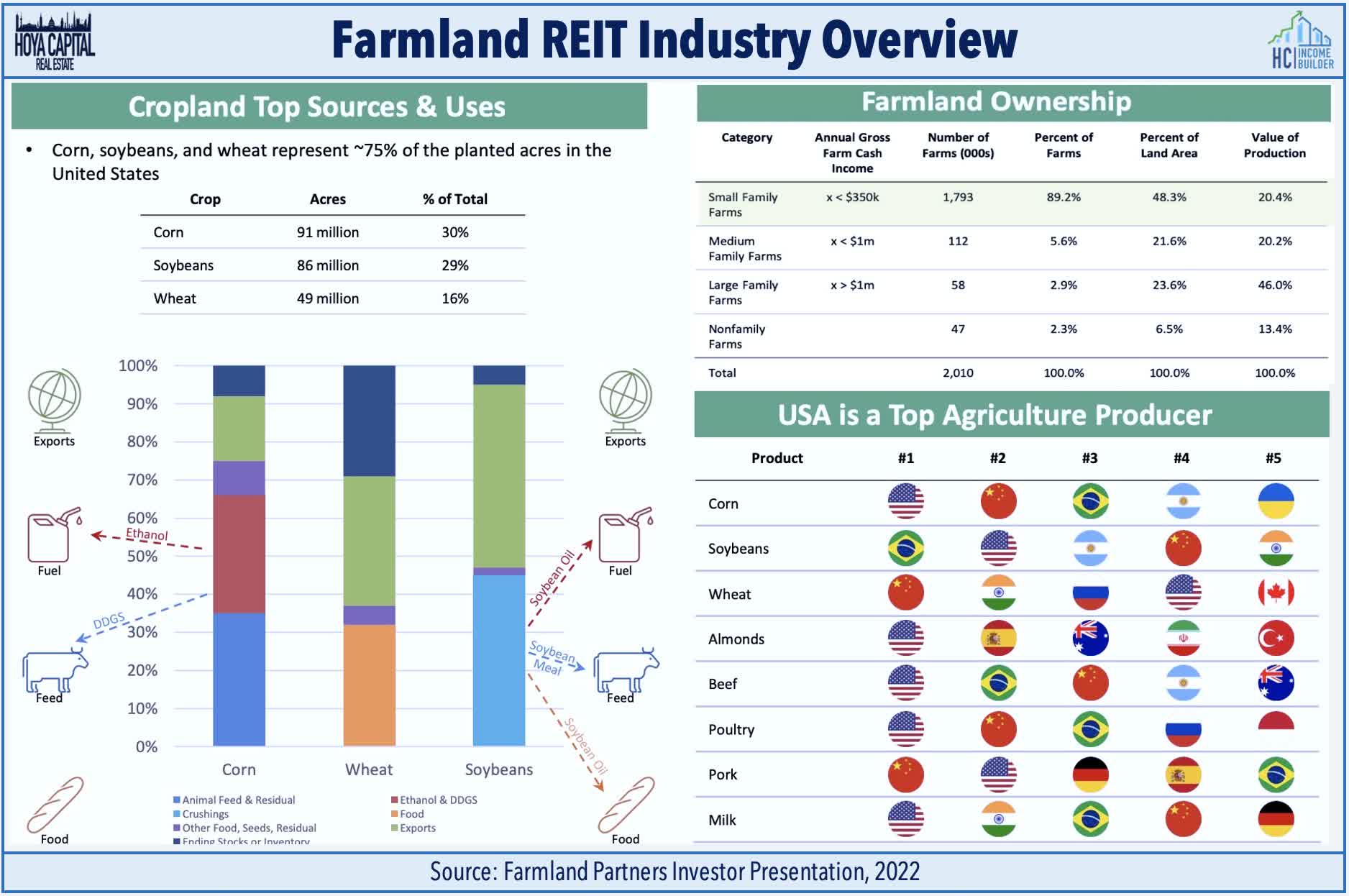

U.S. Farmland, meanwhile, is one of the largest commercial real estate sectors valued at roughly $2.5 trillion, comprised of roughly two million farms - 90% of which are considered small family-operated farms. Farmland consists of row crops (e.g., corn, wheat, soybeans) - which is the focus of Farmland Partners - and permanent crops (e.g., fruits, nuts, berries) - which is the primary focus of Gladstone Land . Increased demand for food globally has been met with a shrinking supply of available agricultural land, but the productivity of this land has increased substantially in recent decades, roughly doubling in output every 20 years. Farmland leases generally have a 1-3 year term for row crops and a 5-10 year term for permanent crops, and leases are primarily fixed-rate, but some have a revenue-share component. Weather patterns - and access to water for irrigation - have remained a persistent concern for farmers over the millennia, and these REITs are certainly no exception. Farmland Partners' regional focus is on the U.S. Midwest and Southeast - areas that are currently experiencing moderate-to-extreme drought conditions - while Gladstone Land has a major presence in California and the U.S. West, which is recovering from drought conditions last year.

{kind=link}

Land REITs' inflation-hedging attributes and portfolio diversification attributes are among the most appealing investment characteristics. Consistent with its historical inflation-hedging attributes, timberland values averaged roughly $1,970 per acre in 2022, an increase of 12.9% from 2021. The Western U.S. - home to higher-valued timber species such as Douglas Fir - has the highest value-per acre at $3,300/acre followed by the U.S. South - home to the relatively cheaper Southern Pine species - at $1,800/acre, while the Northern US timberlands are valued at $800/acre. Per the US Dept. of Agriculture, farmland values averaged $3,800/acre for 2022, up 12.4% ($420/acre) from 2021. On a per-acre basis, crop and farmland in California is the most valuable at over $10k/acre, followed by the Midwest at $6-8k per acre and the Southeast at $4-5k/acre.

{kind=link}

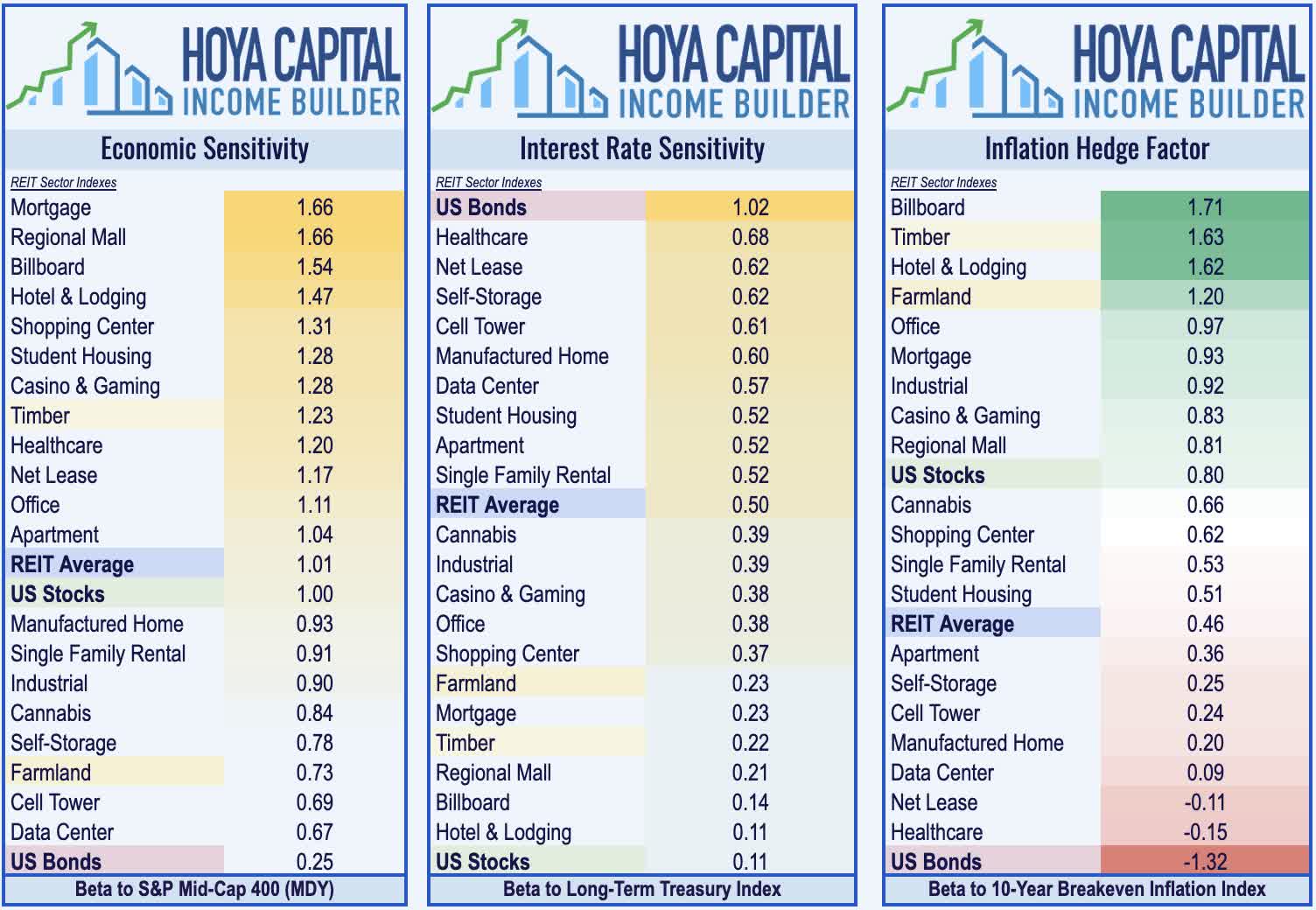

Historically, timberland and farmland have exhibited low correlations to other asset classes and both timber and farmland REITs exhibit some of the lowest levels of interest rate sensitivity within the real estate sector. Investors should note that while timber REITs are quite economically-sensitive due to their high correlation with wood products demand and lumber prices, farmland REITs exhibit limited sensitivity to economic growth expectations, as food demand tends to be far less cyclical. As it relates to inflation-hedging, however, timber REITs reign supreme in the REIT sector, exhibiting one of the strongest upside correlations to inflation expectations, but farmland REITs are close behind.

{kind=link}

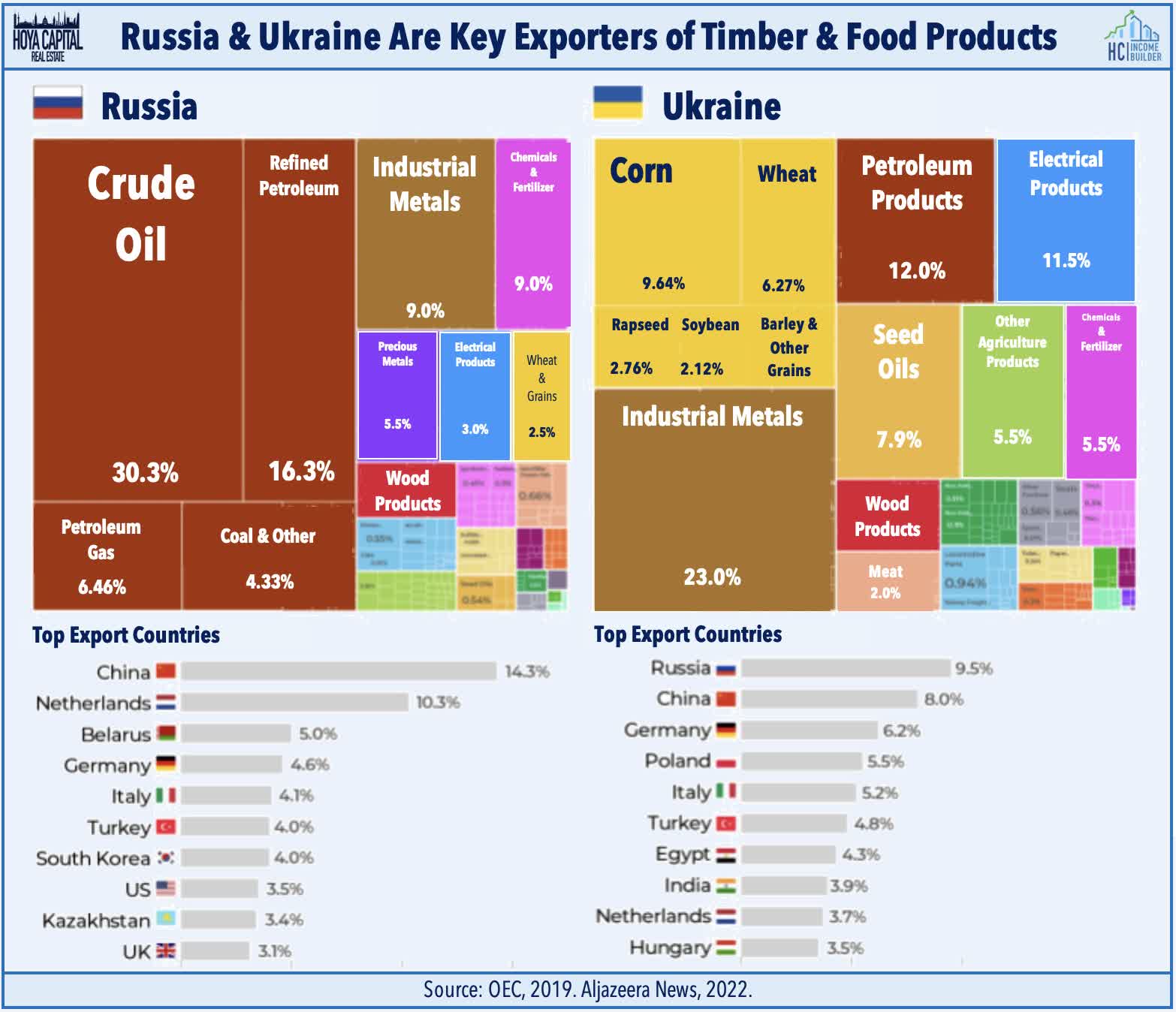

As noted previously, beyond their utility as the most direct "land play," we remain optimistic about the long-term value-creation for both timber and farmland REITs on the expectation of continued global market share gains for North American agricultural commodities producers given the lingering disruptions from the Ukraine/Russia conflict and strained trade relations with China. While the significance of Russian oil and natural gas production has been the key focus of politicians and consumers alike, Russia is also the world’s largest exporter of lumber - primarily softwoods - and the seventh-largest exporter of forestry products. Ukraine, meanwhile, is responsible for more than a quarter of the world’s wheat exports, a fifth of corn exports, and nearly 30% of barley exports. With indications that the conflict may drag on indefinitely, we expect continued global market share gains for North American producers of the disrupted agricultural products.

{kind=link}

Timber Industry Overview & Update

Lumber prices have been on a wild ride since the start of the pandemic with prices peaking at record-highs above $1,600 per thousand board due to soaring demand for homebuilders, robust DIY home renovation activity, and supply chain issues stemming from the pandemic - but have since dipped back towards "normal" levels by the rate-driven cooldown in new home construction activity and the easing of supply chain bottlenecks. As noted in our recent Homebuilder report, to the surprise of countless pundits, the U.S. housing industry has quietly started to emerge from its year-long recession, thawing from a deep freeze induced by historically aggressive monetary tightening and helping to put a floor in timber prices. The near-term outlook for home construction activity remains very-much rate-dependent, but the longer-term demand outlook remains quite favorable following a decade of historic underbuilding of single-family homes.

{kind=link}

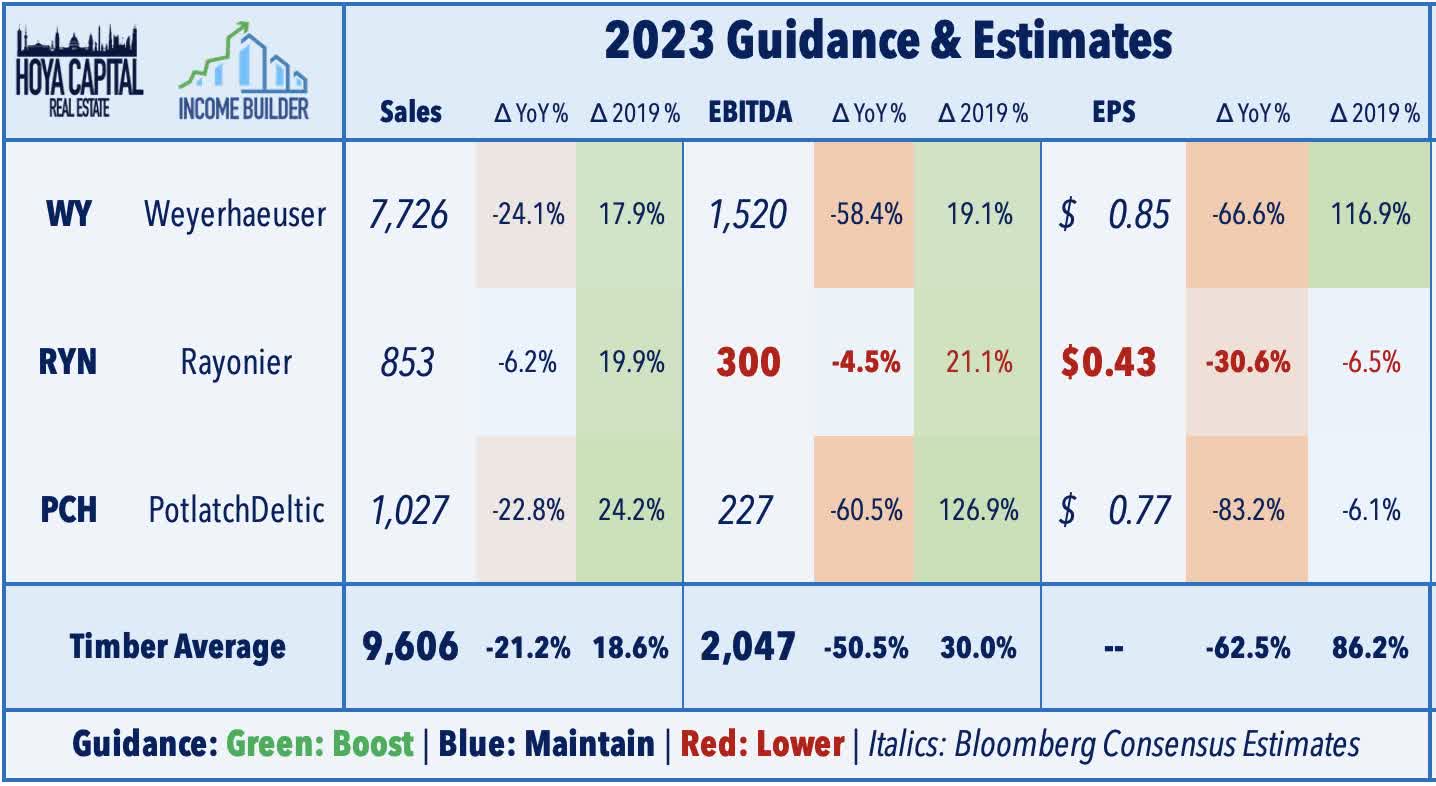

Lumber sawmills - the source of much of the supply chain bottlenecks and the resulting surge in lumber prices - are finally beginning to catch up and address the supply/demand imbalance as producers have invested heavily into building immediate and long-term capacity over the past several quarters. As discussed in our REIT Earnings Recap , timber REITs reported results that were roughly in line with estimates in the first quarter with EBITDA and EPS metrics reflecting the slowdown in volumes following the record years in 2021 and 2022, particularly from Weyerhaeuser and PotlatchDeltic which have more direct exposure to lumber prices. Rayonier - the lone timber REIT that provides full-year EBITDA and EPS guidance - continues to project double-digit EBITDSA growth this year after a modest downward revision in its outlook. Based on Bloomberg consensus estimates, timber REITs are expected to report total sales that are roughly 20% lower from last year, but these levels remain nearly 20% above 2019 levels.

{kind=link}

Farmland Industry Update

Grains prices have been on a similar trajectory, and the Russia/Ukraine conflict came as global wheat and corn stockpiles were already shrinking after a below-average growing season in 2021 and lingering supply chain issues, resulting in significant food price inflation over the subsequent several quarters. The Russia/Ukraine conflict sent prices of corn, wheat, and soybeans higher by 10-20% last year in the U.S. - and at a far faster pace in Europe - but crop prices have retreated rather significantly after a decent growth season in 2022 and amid a broader cooling of inflationary pressures. The Bloomberg Grains Index is now lower by about 20% from last year and is now slightly below the average from 2015-2020.

{kind=link}

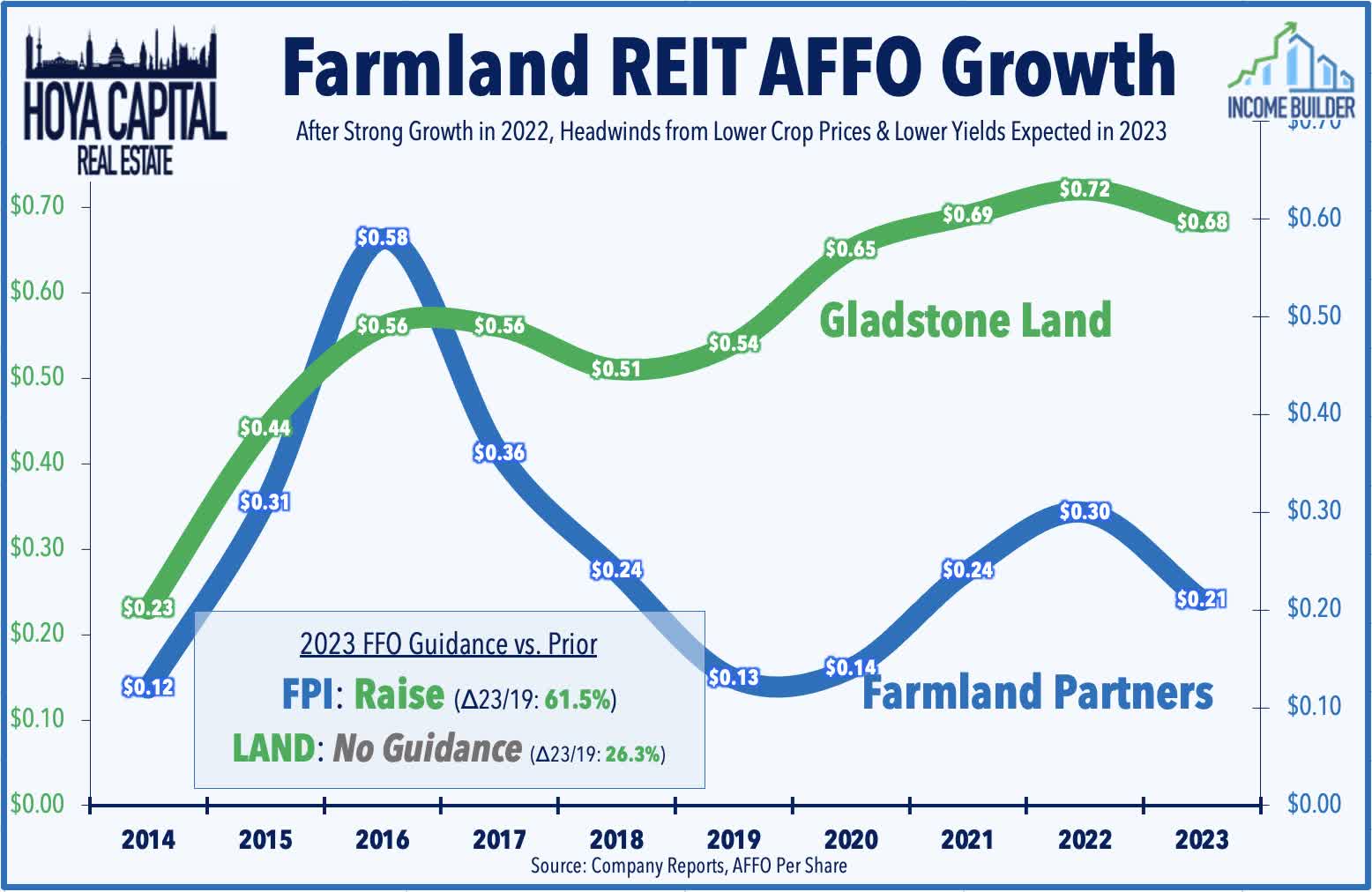

As noted, Farmland REITs have been pressured by a "triple whammy" of headwinds - sluggish crop yields in some regions due to extreme weather, lower crop prices, and significantly higher interest rate expense. As discussed in our REIT Earnings Recap , Farmland Partners ( FPI ) reported mixed results, noting that it still expects its FFO to decline 30% this year driven primarily by significantly higher interest rate expense due to FPI's elevated level of variable rate debt exposure. Even with the rate-driven decline, however, FPI still expects its FFO to be 60% above 2019-levels. Gladstone Land ( LAND ) reported mixed results, noting that its tenant rent collection issues have persisted amid headwinds from lower crop prices and the impacts of flooding in California. LAND reported rent collection issues from 3 of its 90 tenants - one of which was evicted - while the other two are late in their rent payments. While LAND doesn't provide guidance, consensus estimates call for FFO to be about 26% above 2019-levels for full-year 2023.

{kind=link}

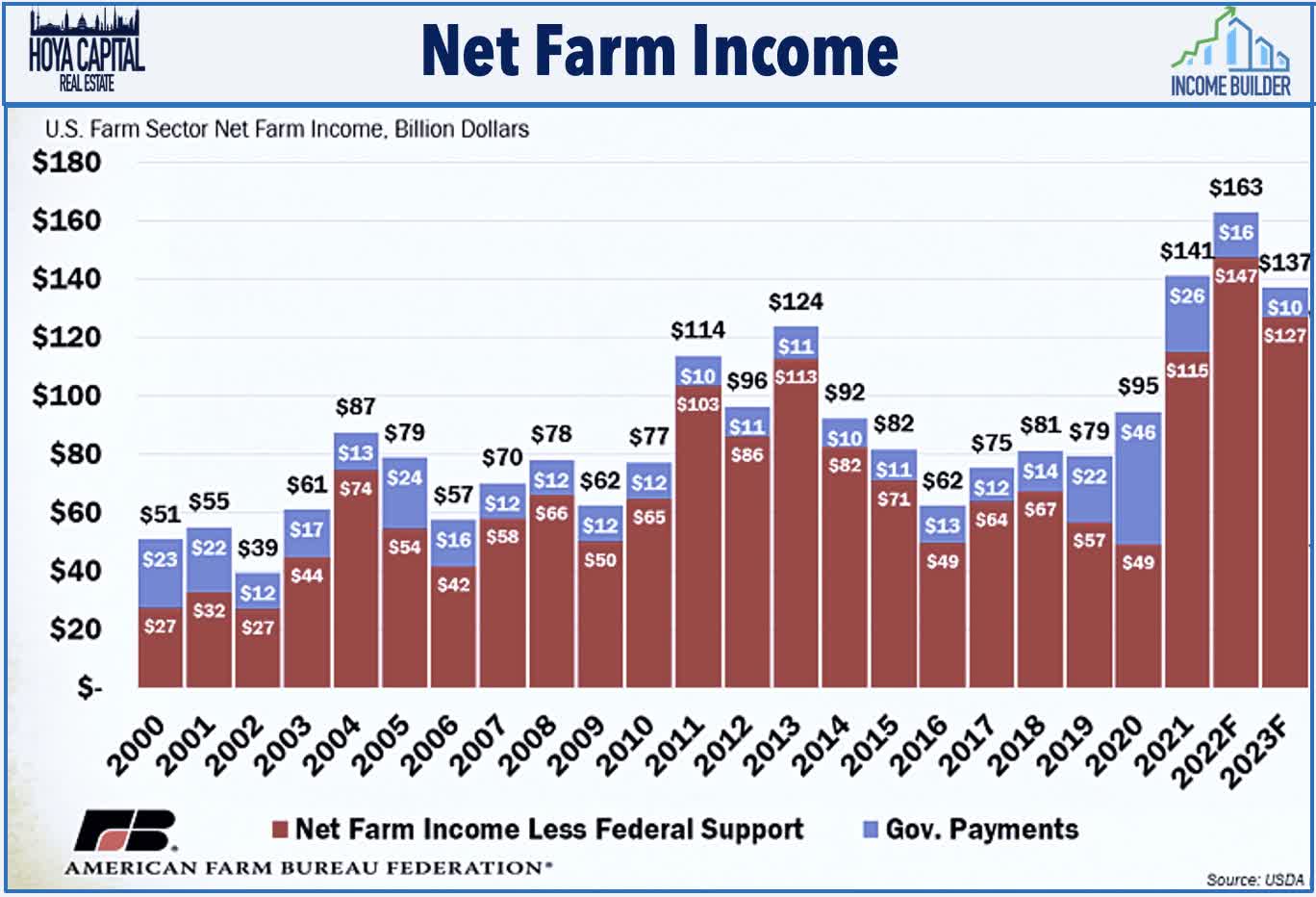

Farm incomes climbed to record-highs last year, but are expected to erase some of these gains this year, per the most recent USDA Farm Sector Income Forecast. U.S. net farm income, a broad measure of farm profitability, is currently forecast at $136.9 billion, down 15.9% from 2022’s $162.7 billion. This $25.9 billion decline erases the $21.9 billion increase that was forecast between 2021 and 2022 but is smaller than the gain between 2020 and 2021 of $46.5 billion following the COVID-19 pandemic. When adjusted for inflation, 2023 net farm income is expected to decrease $30.5 billion (18.2%). The report expects farm and ranch production expenses to continue to increase by $18.2 billion (4.1%) in 2023 to $459.5 billion, following a record increase of $70 billion in production expenses in 2022.

{kind=link}

Farmland & Timber REIT Performance

Among the best-performing real estate property sectors last year, Timber and Farmland REITs have posted mixed performance this year on cooling inflation expectations, slumping global commodity demand, and regional weather complications, pulling valuations of several of these REITs back towards more compelling levels. After lagging for much of the first half of 2023, Timber REITs are now higher by nearly 10% this year following a sharp rebound since the start of May driven by an improving single-family housing market outlook. Farmland REITs, however, remain lower by about 6% this year, which compares to the 2.0% increase from the Vanguard Real Estate ETF ( VNQ ) and the 16.0% gain on the S&P 500 ETF ( SPY ).

{kind=link}

PotlatchDeltic has led the gains this year as it completed its acquisition of CatchMark Timber in a roughly $600 million all-stock deal. The combined company now owns 2.2 million acres of timberlands, including 626,000 acres in Idaho and over 1.5 million acres in the U.S. South and have a market valuation of roughly $4 billion. PCH paid a 55% premium to its most recent close - which is roughly at the levels that CTT traded in late 2021 before running into a myriad of issues with its now-exited Triple T joint venture. PotlatchDeltic shareholders own 86% of the combined company. Gladstone Land ( LAND ) has been the laggard over the past two years, but valuations now look quite compelling as the most immediate extreme-weather-related headwinds have improved in recent months.

{kind=link}

Deeper Dive into the Timber Industry

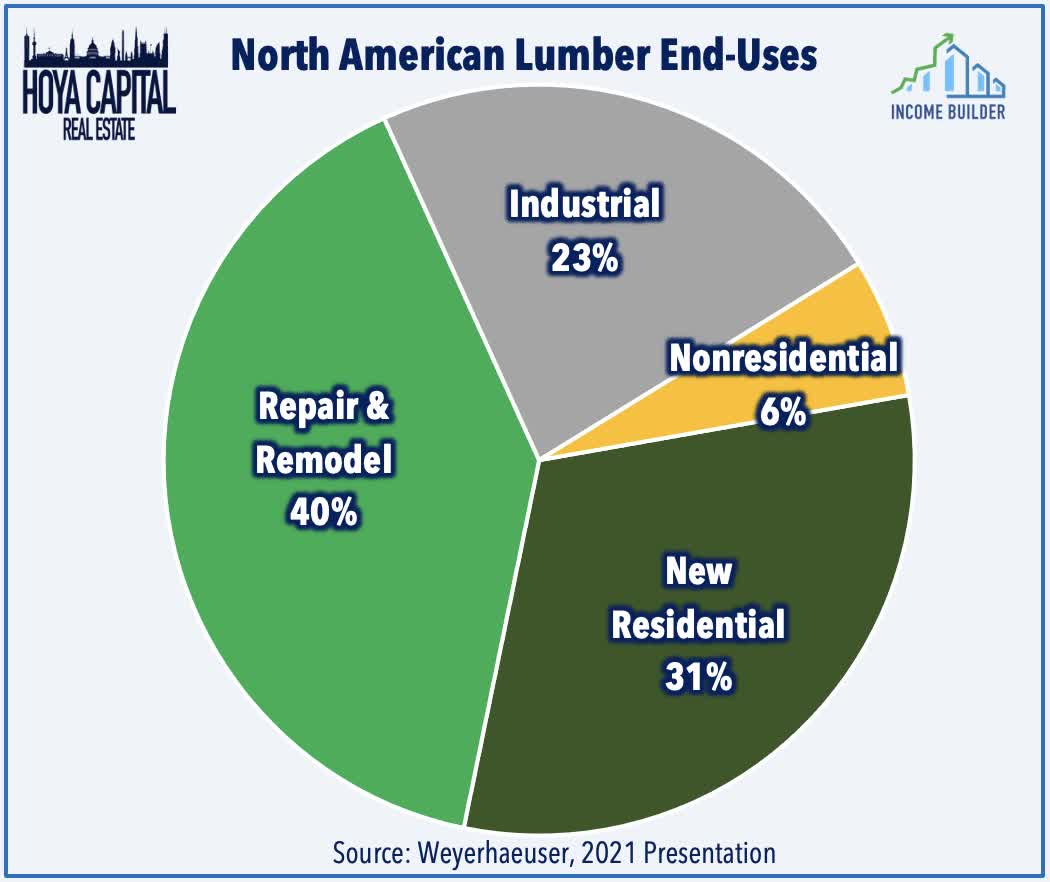

Wood is arguably the most important natural and renewable resource on Earth. A highly versatile and cost-effective material with applications across all industries from paper to fuel, residential construction accounts for the majority - roughly two-thirds - of wood demand. The vast majority of single-family homes in the US are built primarily with wood products, and wood has been increasingly used as a primary structural material in larger multi-family or commercial structures. Wood products account for more than a third of total construction materials cost inputs in the typical single-family home, and the average-sized home requires between 150 and 300 trees to construct.

{kind=link}

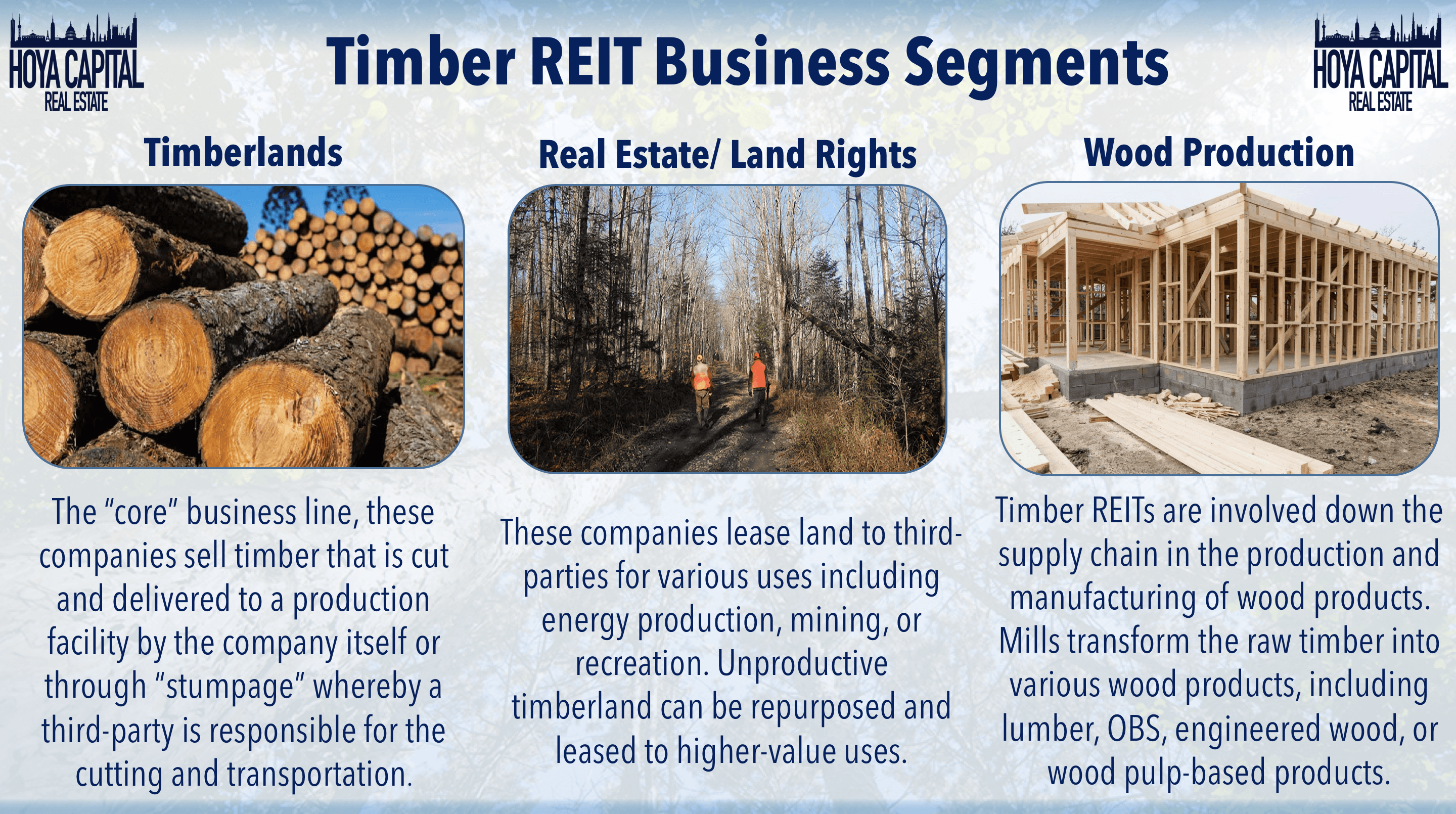

While they've been around for two decades, Timber REITs are still considered a "specialty" REIT sector that straddles the line between the REIT and building materials industries. Real estate ownership is only part of the business for Timber REITs, which take on quite a bit more operational responsibilities than other REIT sectors. There are three primary business lines for timber REITs:

| 1) Timberland - The "core" business line. These companies sell timber that is cut and delivered to a production facility by the company itself or through "stumpage," whereby a third party is responsible for the cutting and transportation. A true commodity, prices of timber are determined by prevailing supply and demand conditions. Usage of timber products for biomass-fueled energy production falls into this category as well. |

| 2) Real Estate - These companies lease land to third parties for various uses, including energy production, mining, or recreation, and also market land for sale to homebuilders or other developers. This business line encompasses about 20% of total EBITDA, and Timber REITs have special exemptions under the tax code to qualify as REITs despite operating outside of the traditional definitions of "real estate." |

| 3) Wood Production - To varying degrees, these companies are involved down the supply chain in the production and manufacturing of wood products. Mills transform the raw timber into various wood products, including lumber, OBS, engineered wood, or wood pulp-based products such as paper. Production facilities are generally located in close proximity to timberlands. |

{kind=link}

An old forestry maxim is "the forest that pays, stays." Timber REITs are among the leaders in sustainable foresting, with all four timberland REITs having 100% of their land third-party certified as sustainable either by the Sustainable Forestry Initiative ((SFI)) or the Forest Stewardship Council ((FSC)). Due to responsible foresting of privately-owned land and growing demand for wood products (including lumber, paper, and biomass) and despite several years of above-average incidences of wildfires , primarily on federally-owned land on the West Coast, there are actually more trees now than there were 100 years ago, according to the Food and Agriculture Organization .

{kind=link}

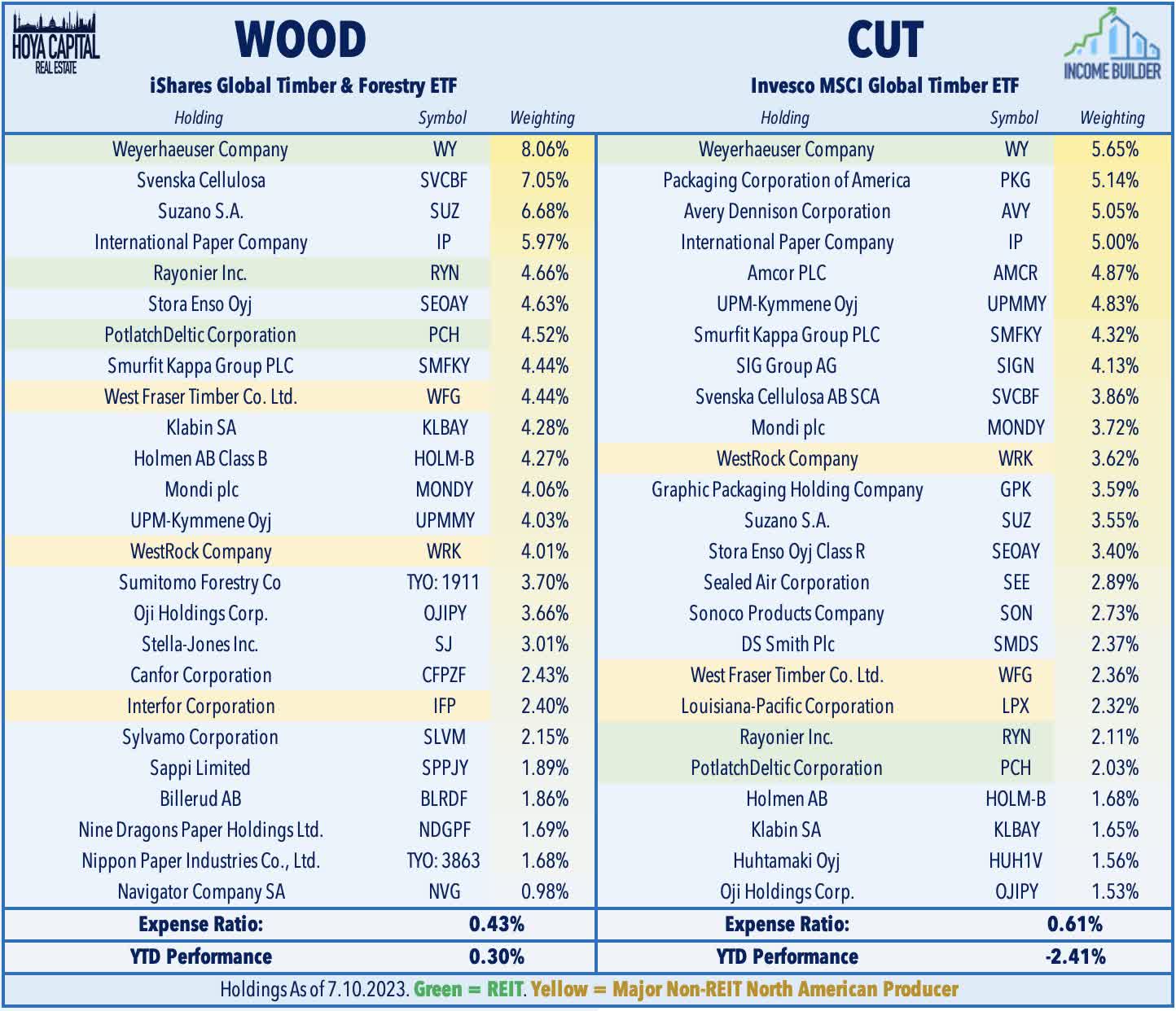

Primarily concentrated in the Pacific Northwest and the Southern US, there are roughly 200 million acres of commercially forested timberlands in the United States. Timberland ownership, while still a highly fragmented industry comprised of thousands of individual landowners, has undergone a continued wave of consolidation and institutionalization over the past four decades. The first Timber REIT was established in 1999 with the conversion of Plum Creek from an MLP into a REIT. Rayonier and Potlatch followed in the early 2000s. Weyerhaeuser converted to a REIT in 2010 and merged with Plum Creek in 2016 to form the largest Timber REIT. CatchMark Timber went public in 2013, and most recently, Potlatch and Deltic Timber merged in 2018. Two ETFs track the broader Timber and Foresting sector: the iShares S&P Global Timber & Forestry Index ETF ( WOOD ) and the Invesco MSCI Global Timber ETF ( CUT ). Other major publicly traded companies in the lumber production industry besides these REITs include Canadian firms West Fraser Timber, Interfor, and Canfor, as well as Georgia-based Louisiana-Pacific ( LPX ). Private players include Georgia Pacific Company, Sierra Pacific, and Hampton Affiliates.

{kind=link}

Timber & Farmland REITs Dividend Yields

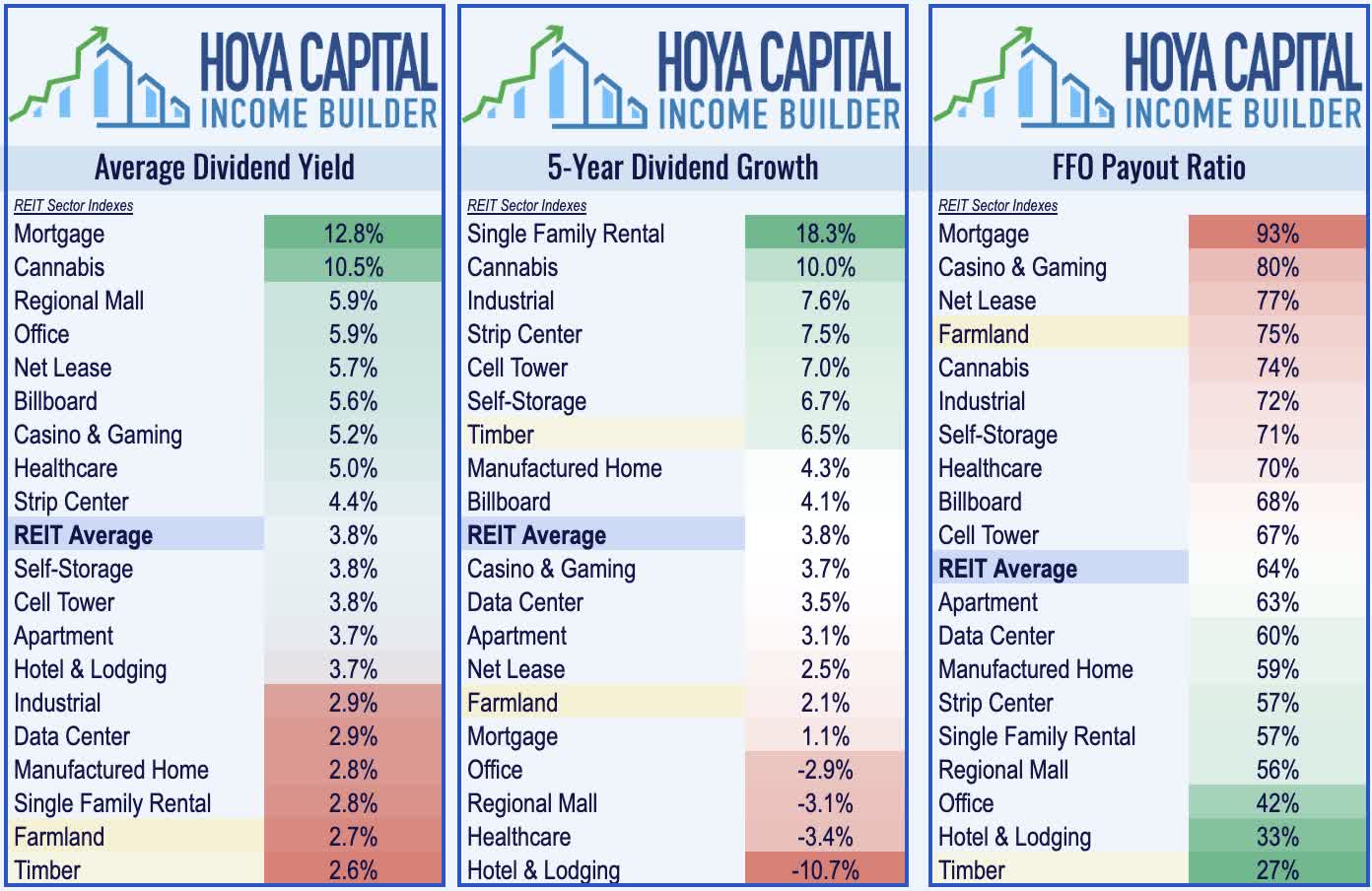

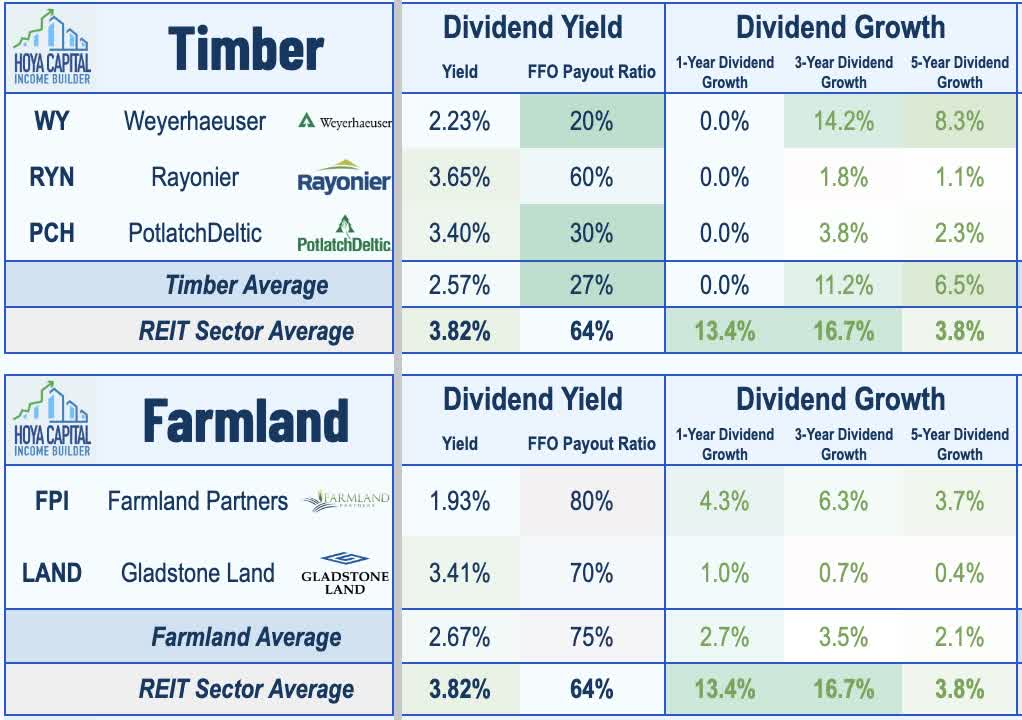

Timber REITs pay an average dividend yield of 2.7% while farmland REITs pay an average dividend yield of 2.6%, each below the REIT sector average dividend yield of 3.8% Timber REITs pay out just 25% of their available free cash flow, however, leaving ample capital available for future dividend growth while farmland REITs payout roughly 75% of their normalized FFO.

{kind=link}

Record profitability during the pandemic translated into significant dividend growth for each of these five REITs over the past several years. Both Weyerhaeuser and PotlatchDeltic utilize a similar "base plus variable supplemental" dividend framework whereby these REITs pay a relatively conservative quarterly dividend with the expectation of paying a special dividend at the end of each year to achieve a full-year targeted payout ratio of 75-80% of Adjusted Funds Available for Distribution. Including its $0.45 special dividend last year, PCH has a sector-leading trailing twelve-month ("TTM") dividend yield of 5.1%, followed by WY with a TTM yield of 4.8% when including its $0.90 special dividend. RYN , along with the FPI and LAND, employ a more conventional dividend framework.

{kind=link}

Takeaways: Buying Land At A Discount

One of the hottest "inflation hedges" during the pandemic, land REITs have fallen out-of-favor as rising rates and normalizing supply chains have created disinflationary - and even deflationary - headwinds for commodities. Beyond their utility as the most direct "land play," however, we remain optimistic about the long-term value-creation for both timber and farmland REITs on the expectation of continued global market share gains for North American agricultural commodities producers. The three timber REITs and two farmland REITs also collectively comprise about 40% of our Landowner Portfolio , which targets exposure to publicly-traded companies that own or control significant acreage of land across North America, diversified across regions and across distinct productive uses. Designed to "isolate" the benefits of land ownership, the portfolio has significant inflation-hedging characteristics, low correlations to stocks and bonds, and a healthy dividend yield and an evident "quality" tilt.

{kind=link}

For an in-depth analysis of all real estate sectors, check out all of our quarterly reports: Apartments , Homebuilders , Manufactured Housing , Student Housing , Single-Family Rentals , Cell Towers , Casinos , Industrial , Data Center , Malls, Healthcare , Net Lease , Shopping Centers , Hotels , Billboards , Office , Farmland , Storage , Timber , Mortgage , and Cannabis.

Disclosure : Hoya Capital Real Estate advises two Exchange-Traded Funds listed on the NYSE. In addition to any long positions listed below, Hoya Capital is long all components in the Hoya Capital Housing 100 Index and in the Hoya Capital High Dividend Yield Index . Index definitions and a complete list of holdings are available on our website.

{kind=link}

For further details see:

Land REITs: Disinflation Headwinds