LNXSF - Lanxess: Global Specialty Chemicals Player With Turnaround Potential

2023-12-06 03:44:54 ET

Summary

- Lanxess has experienced a slump in demand for specialty chemicals, resulting in profit warnings and a significant decrease in market cap.

- However, even without any increase in demand in 2024, management expects EBITDA to increase by around EUR 180 million following the implementation of a restructuring.

- The current valuation of Lanxess does not account for a potential demand normalization, making it an attractive investment opportunity.

Editor's note: Seeking Alpha is proud to welcome NHM Capital as a new contributor. It's easy to become a Seeking Alpha contributor and earn money for your best investment ideas. Active contributors also get free access to SA Premium. Click here to find out more »

Summary

Following a slump in global demand for specialty chemicals in 2023 German specialty chemicals company Lanxess ( LNXSF ) had to post two profit warnings and lost more than 50% of its market cap within the last 9 months trading currently around a ten year low.

But customer destocking and reduction of high cost inventory should come to an end in 2023 and even at current historic low utilization rates of 55% for its production facilities the company expects EBITDA to increase by around EUR 180 million in 2024 following the implementation of a restructuring plan.

The current valuation does not give any benefit for a potential demand normalization and could offer an attractive entry point as the company's profitability will benefit significantly from any increase in utilization. Hence, the risk reward profile looks to be skewed to the upside from here.

Background Of 2023 profit warnings

Lanxess' stock price has been hit by two profit warnings this year trading currently around EUR 23 compared to its 2023 high of EUR 47.63 reached in February.

The company, which makes high-end speciality chemicals such as additives, lubricants, flame retardants and plastics is suffering from inflation and rising interest rates that have triggered a global downturn and resulted in weak demand for its products. Full year 2023 EBITDA guidance that was initially set at EUR 850-950 million had to be reduced to EUR 600-650 million in June followed by another reduction to EUR 500-550 million in November of this year.

However, in its Q3 results conference call management indicated that both the reduction of own excess inventories and customer destocking in all industries except Agrochemicals should be completed within FY 23. The company also posted strong cash flow in Q3 by working capital management reducing net financial debt by round EUR 300 million. A EUR 500mm bond coming due in 2025 has already been refinanced by a bilateral loan agreement and management could disperse concerns about the need for a capital raise to reduce leverage.

Business Overview

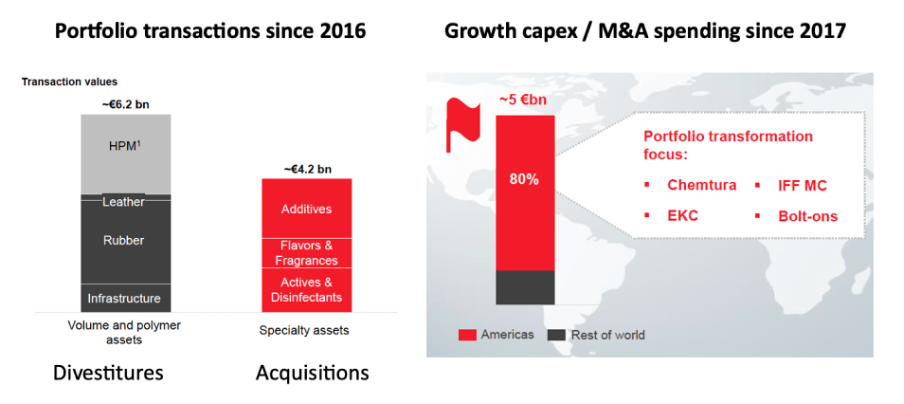

Management has repositioned the company in recent years divesting business in the more asset intensive and less profitable business lines like Polymer (HPM) and Rubber business while adding in the specialty segments.

Source: Company Q3 results presentation

{kind=link}

The acquired business are characterized by a higher profitability and cash generation as well as lower asset intensity and cyclicality compared to the divested businesses. At the same time the company has strengthened its asset footprint in the Americas while reducing the German exposure further.

In its latest divestment Lanxess contributed its High Performance Materials business ((HPM)) into a joint venture with Advent effective April 1, 2023. Lanxess' stake in the joint venture called Envalior is 40.94% and it received a cash consideration from Advent in the amount of around EUR 1.3 billion that was used to reduce net financial debt. Starting in the second quarter of 2023, the minority interest in Envalior is included in the LANXESS consolidated financial statements using the equity method. Lanxess expects a hit in its financial income of approximately EUR 50mm per quarter going forward due to the high level of Envalior debt and associated interest costs. However, these are non-cash items for Lanxess. Lanxess has the option to sell its remaining stake to Advent in 2026 at a pre agreed EBITDA multiple. As of September 30, 2023 the remaining stake was value at around EUR 1bn in the financial statements of Lanxess.

Following its portfolio transformation Lanxess is now a global chemical player with strong market positions in markets with oligopolistic structures. The company is a top #3 player in all of its business segments Consumer Protection, Specialty Additives and Advanced Intermediates. (A comprehensive overview of their business strategy and business lines was provided at last year's capital markets day ).

Financials

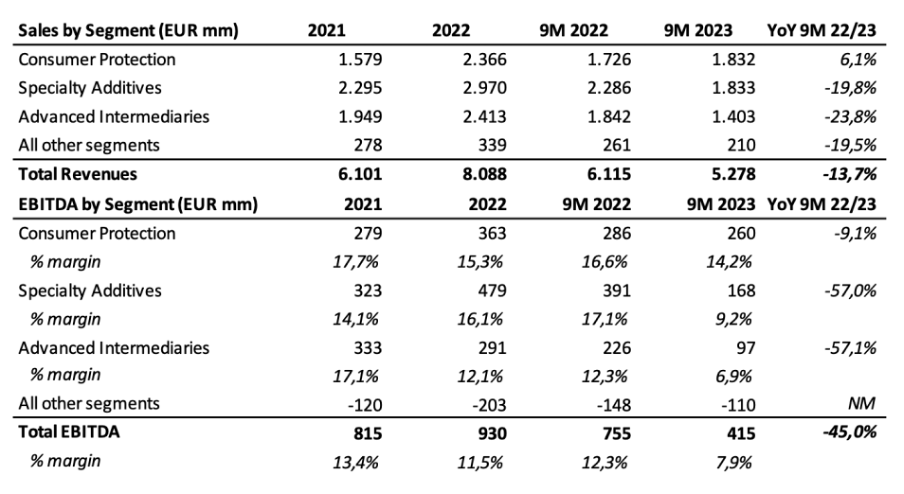

Demand for the company's products has remained weak in 2023 following customer destocking across construction, electronics, and consumer-related products, with a corresponding impact on volumes and operating leverage. Revenues in the first 9 months have been down more than 13% (EUR 5.3 bn vs. EUR 6.1bn) and with utilization at a historic low of 55% EBITDA margins have deteriorated significantly falling from 12.3% in the first nine months of 2022 to 7.9% by September 2023. Management does not expect any uptick in underlying demand in the fourth quarter and is now guiding for a full year EBITDA between EUR 500 and 550 million.

Source: Company 2022 AR, Q3 results

{kind=link}

Valuation Considerations

With a share price of around EUR 23 Lanxess' current market cap stands at roughly EUR 1.99 billion adding financial debt including pension liabilities as of September 2023 of 2.86 billion results in an enterprise value of 4.85 billion. While the midpoint for this year's EBITDA guidance stands at EUR 525mm the company has identified a number of drivers that will improve next year's EBITDA even without any improvement in demand / increase in factory utilization.

2023 EBITDA has been hit by EUR 100mm that will not reoccur in 2024 from reducing the company's inventory and sweating out the high-priced costs. The restructuring program FORWARD! implemented in 2023 will result in additional cost savings of EUR 40 million in the next year on top of EUR 50 million realized in 2023. There is currently a temporary supplier bottleneck causing a EUR 10 million hit to EBITDA in the last quarter of 2023 that is expected to be solved by year end. On top of this, there has been a long persisting limitation in chlorine supply that had roughly an impact of around EUR 15 million and should not impact the company in 2024 any longer. Finally, the company expects synergies from their M&A integration coming on top in the magnitude of EUR 15 million.

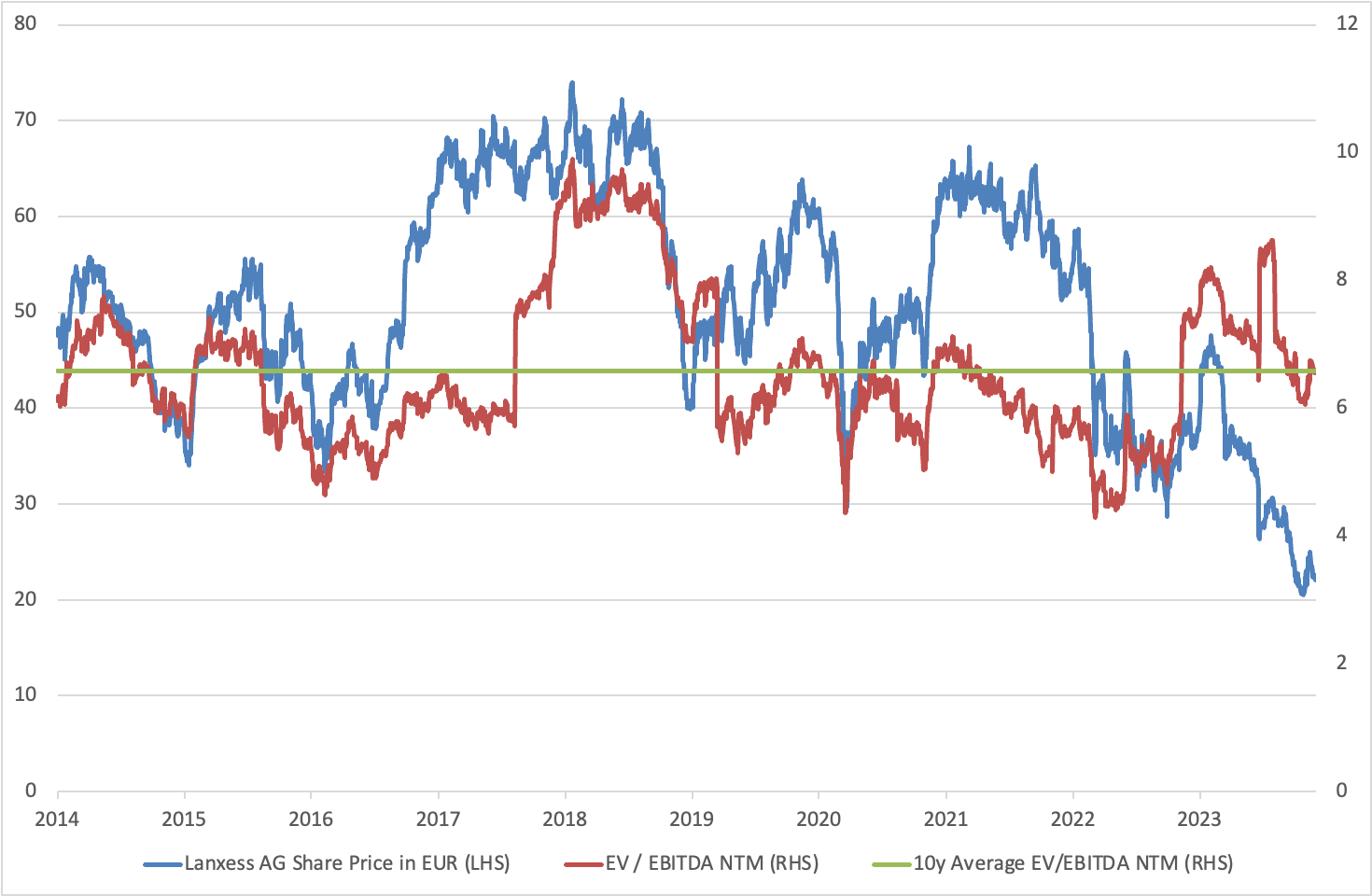

Adding this all together should improve EBITDA by around EUR 180mm in 2024. Hence, base case EBITDA for 2024 should be in the region of EUR 700 million which is still very depressed in historical terms but results in an EV/EBITDA multiple of around 6.9x slightly above the 10y average of 6.6x the company has been trading at. Research consensus as per Reuters Refinitiv expects 2024 EBITDA also in the region of EUR 700mm implying that the market does not expect any improvement in profitability through higher demand / utilization.

{kind=link}

Following its portfolio transformation with the focus on three business segments the company had provided the market with long term EBITDA margin potential of more than 20% for Consumer Protection, up to 20% for Specialty Additives and between 16 and 18% for Advanced Intermediates. Using the lower end of those ranges and applying a sales split of 40/30/30 would result in a blended EBITDA margin potential of 19%. Adjusting for overhead expenses included in "all other segments" corresponding historically to 2-3% p.a. would reduce this margin potential by another 2-3% to roughly 16%.

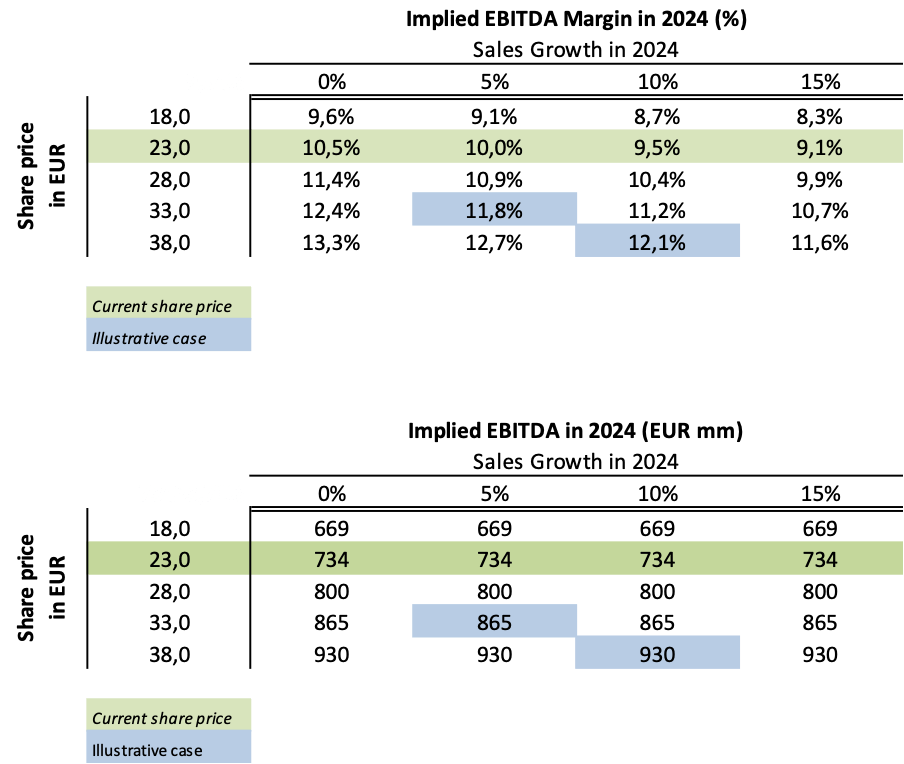

Now, rather than predicting what the EBITDA margin will be the following sensitivities show the implied EBITDA margins and absolute EBITDA levels in EUR the company needs to achieve in 2024 to justify the shares prices shown based on a 6.6x EV / EBITDA multiple assuming constant net debt.

{kind=link}

Hence, to justify a share price of EUR 33 assuming 5% sales growth in 2024 the company would need to achieve an EBITDA margin of 11.8% or an EBITDA of around EUR 865 million in 2024 which does not look impossible given the EBITDA and margins the company generated in the past. Assuming 10% sales growth and an EBITDA margin of 12.1% the company's shares would need to trade at EUR 38 to keep the EV/EBITDA multiple at 6.6x.

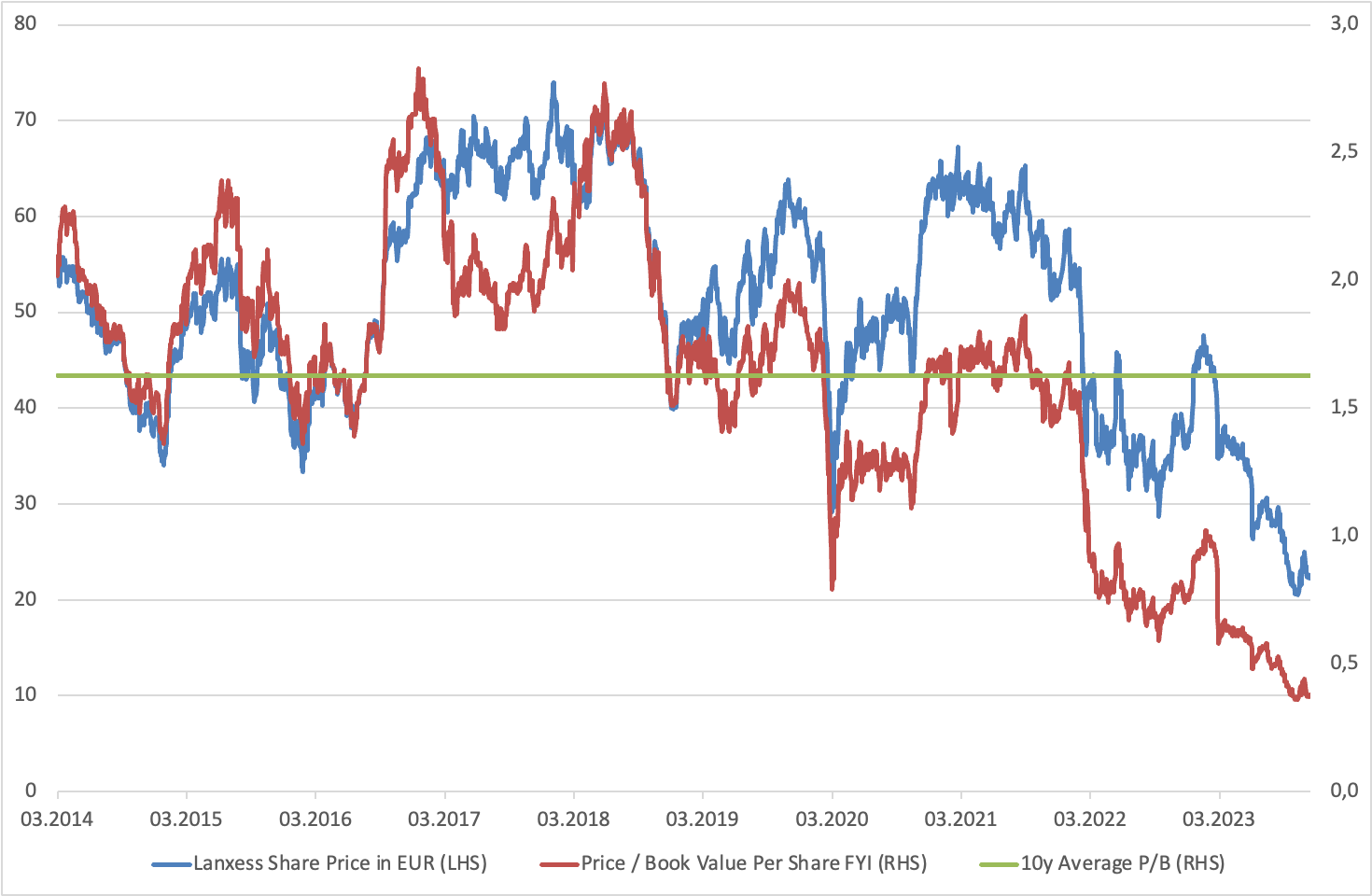

Another way to look at the company's valuation is its book value vs market value. As of September 30, 2023 the company's equity had a total book value of EUR 5.6bn. Conservatively deducting the book value of its Envalior stake of EUR 1bn fully still implies a Price to Book Value of 0.4x which is also at a historic low compared to a 10-year average of around 1.6x.

{kind=link}

Risk Considerations Or Where Could We Be Wrong

The 2024 EBITDA might turn out to be lower than currently guided by the management if demand weakens even further or some of the items identified by management are not realized (M&A synergies, end to limitation of chlorine supply, persistent issue with supplier). Also, while the company clearly stated that it does not see any structural changes in its end markets that should reduce their business potential there could be more competition e.g. from Chinese players impacting their ability to regain their footing. Since Lanxess operates a majority of its production sites in Germany it has been hit by the high energy prices following the Russian invasion of Ukraine. While it has been able to pass on these higher energy prices to its customers there is a risk of market share losses to Asian suppliers that operate at lower energy prices.

The company's leverage has increased as EBITDA fell off a cliff in 2023. At the midpoint of the 2023 EBITDA guidance of EUR 525 million net debt to EBITDA stands at 5.5x and assuming EUR 700 million of EBITDA for 2024 would still imply leverage factor in excess of 4x. The company's credit rating was just downgraded to Baa3 by Moody's on November 21 with the rating agency maintaining a negative outlook.

Additionally, the Envalior joint venture is highly levered and operates in a difficult environment. The book value of Lanxess' stake will be reduced over time as the JV is expected to incur losses in the foreseeable future. While this has no cash effect for Lanxess there is a risk that new equity financing needs to be provided to the JV if it does not perform according to plan. This would most likely dilute Lanxess' ownership assuming it would not participate in any capital raise and would also reduce the probability that Lanxess can exit the remaining stake at an attractive price in 2026.

Conclusion

At 6.9x 2024 expected EBITDA, Lanxess is valued slightly above its historical average but at still depressed profitability levels. The current 2024 EBITDA forecast assumes no pick-up in demand and a utilization of its productions sites of 55% or its absolute low. On a Price to Book multiple the company trades around the ten year low.

Lanxess has significant operating leverage and the potential to increase profitability again in the coming years. However, there could be further short term headwinds. The management has indicated that Q4 will remain challenging not only on profitability metrics but also on the company's cash flows as there will be some seasonal working capital additions. The company is dependent on a normalization of specialty chemicals demand and with the Chinese economy still not showing signs of returning to growth and the debate about a potential recession in the US it could take time until this materializes. However, medium term we expect the company to return to higher levels of profitability and regard the current valuation as an attractive entry point as it appears that the downside is largely priced in. BUY.

As US OTC market liquidity is very poor in Lanxess shares, we would encourage to execute any trading in the name on its German home exchange Xetra where trading is denominated in Euro.

For further details see:

Lanxess: Global Specialty Chemicals Player With Turnaround Potential