LEGH - Legacy Housing: Attractive Positioning In Turbulent Housing Market

2023-11-15 23:52:40 ET

Summary

- Legacy Housing Corporation is positioned well in the entry-level housing market with affordable prices and has demonstrated a track record of stable growth, particularly post-COVID.

- The company has a strong margin profile and has shown the ability to pass on any increase in input costs to consumers.

- We believe the strong earnings momentum, robust margin profile, and opportunity to capitalize on its entry-level positioning provide favorable risk-reward for the long-term investors.

Investment Thesis

We ascribe Legacy Housing Corporation ( LEGH ) with a Buy rating on the back of

1) Attractive positioning within the entry-level housing with retail home prices under $180,000

2) Growth opportunity as the company is largely based in Southern US and had about 3,000+ average home sales historically and the current challenges in housing market could propel growth as consumers chase affordability

3) Robust margin profile relative to peers driven by tight cost control and its ability to pass on any jump in input costs to its end consumers

4) Strong growth in its loan book which is largely derisked as a result of its lower exposure to consumer loan book which has also shown a growth amidst mortgage applications declining to decadal lows.

Company Background

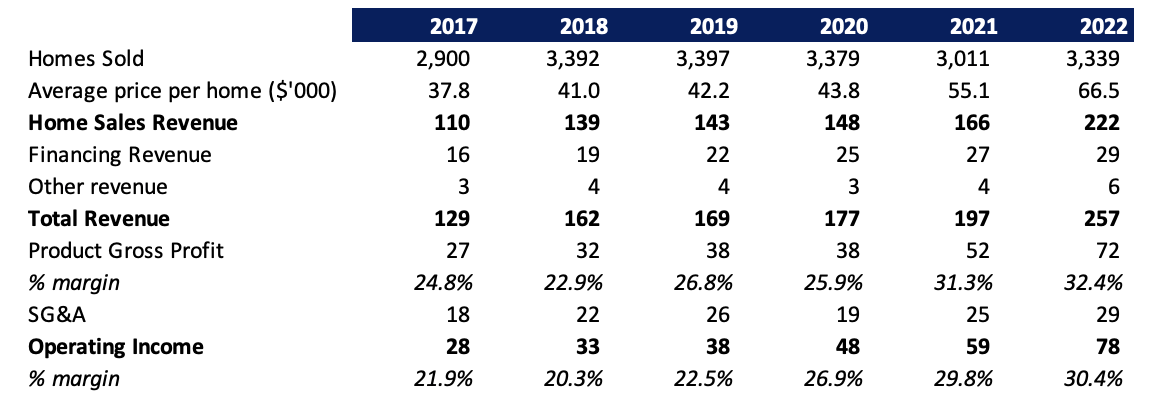

Legacy Housing Corporation is the 5th largest home builder specializing in entry level tiny houses under its 'Legacy' brand distributed through its network of independent retailers and company-owned stores as well as directly to manufactured home communities. Its operations are primarily within the Southern US offering customers wide range of small housing options ranging from 395 to 2,700 sq. feet with home prices ranging from $33,000 to $180,000. The company sells about 3,400 homes annually with Texas contributing more than 50% of the total homes sold. The company also provides financing to consumers and manufactured home communities which in turn leases to end consumers. In addition, the company also provides inventory financing to a wide range of its independent retailers.

Historical Track Record

Legacy Housing had a flattish track record in new homes sold annually with a historical average trending around the 3,300 mark in the last several years. However, the revenue growth was aided by a jump in average prices post-pandemic as a result of supply-side constraints which enabled them to post a revenue growth of 12% and 34% in 2021 and 2022 respectively. Financing revenue continues to grow in low double digits as the management continues to be prudent in growing its loan portfolio. The company has been largely able to sustain its strong gross margins as it passes on the majority of the input cost inflation throughout its history. The company also managed to sustain during the COVID downturn and rebounded strongly post driven by record-low interest rates which spurred new home sales. In 2021 and 2022, a significant jump in prices along with the passing of its cost inflation helped them generate record margins at 40%+. This coupled with tight cost control and operational efficiency helped them to post robust operating margins which hovered around the 30% mark.

{kind=link}

Strong Q3 Earnings

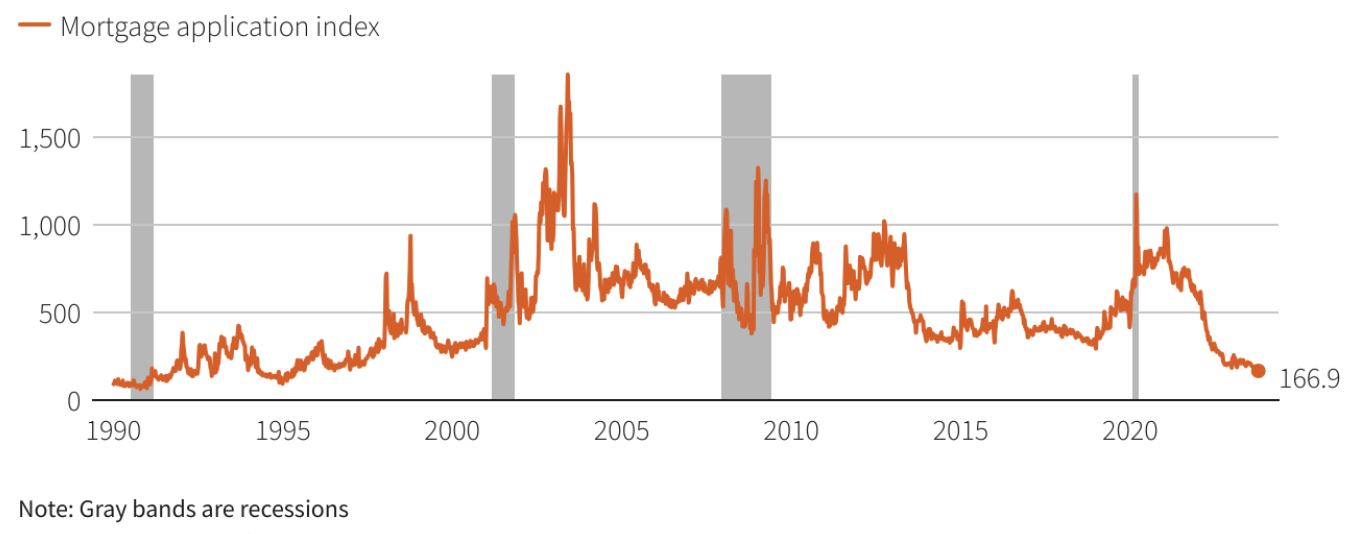

The company reported strong Q3 with revenues down 13% YoY at $50 mn, slightly below the consensus expectations pegged at $53 mn. Volumes declined 23% YoY to 582 homes sold as a result of the overall decline in industry volumes, however, the decline was sharper than the 15% and 14% decline in Q2 and Q1 respectively. Revenue per unit sold came in at $63.6k, down by ~2% YoY, but slightly higher on a sequential basis ($62.4k in Q2 and $63.0k in Q1). Product revenues declined by 24% YoY primarily driven by lower volumes along with slightly lower unit realization prices. Interest income grew by 26% YoY primarily due to an increase in both its MHP note portfolio (up 26% on YTD basis) as well as consumer loan portfolio (up 9% on YTD basis). This also comes at the time when mortgage applications are at three decadal lows as a result of a significant rise in mortgage rates, teasing the 8% mark, along with crippling housing affordability. The relative growth demonstrates the company's ability to expand its loan portfolio while also managing the risk appropriately as the demand for affordable homes continues to grow.

Mortgage Bankers Association, Reuters

{kind=link}

Gross product margin improved by 100 bps YoY to 32.9% driven by lower construction costs with persistent wage inflation and labor pressures serving a testament on the company's ability to manage expenses despite lower volumes. SG&A dollars declined 9% YoY as a result of lower warranty costs along with other miscellaneous costs. SG&A expenses deleveraged by 60 bps YoY as a result of tight cost control which were partially offset by sticky fixed costs amidst a decline in revenue. This led to operating profits jumping by 13% YoY with margins expanding strongly by almost 9 percentage points. In all, the company reported an EPS of $0.66, up 10% YoY, and beating consensus estimates pegged at $0.58.

We expect Q4 volumes to be down largely by 15% YoY, in line with declines observed during the past few quarters after the company received stronger follow-through on dealer financing sales in October along with a strong response on the Fall roadshow. We expect gross product margins to be around 33%, flat sequentially, on the back of stable volumes and no material impact on labor and cost deflation on QoQ basis. We expect SG&A expenses will continue to be flattish on YoY basis, but up sequentially as revenue declines and SG&A spending largely remains in line. This will boost the operating margins on YoY basis as well as sequentially and we further expect EPS to be $0.72, slightly higher than consensus expectations at $0.67.

Balance sheet remains flexible with the company ending with cash balance of $0.5 mn along with $13 mn drawn from credit facilities. In addition, it closed another RCF facility with Prosperity Bank for $50 mn secured by consumer receivables which will further provide additional flexibility.

Valuation

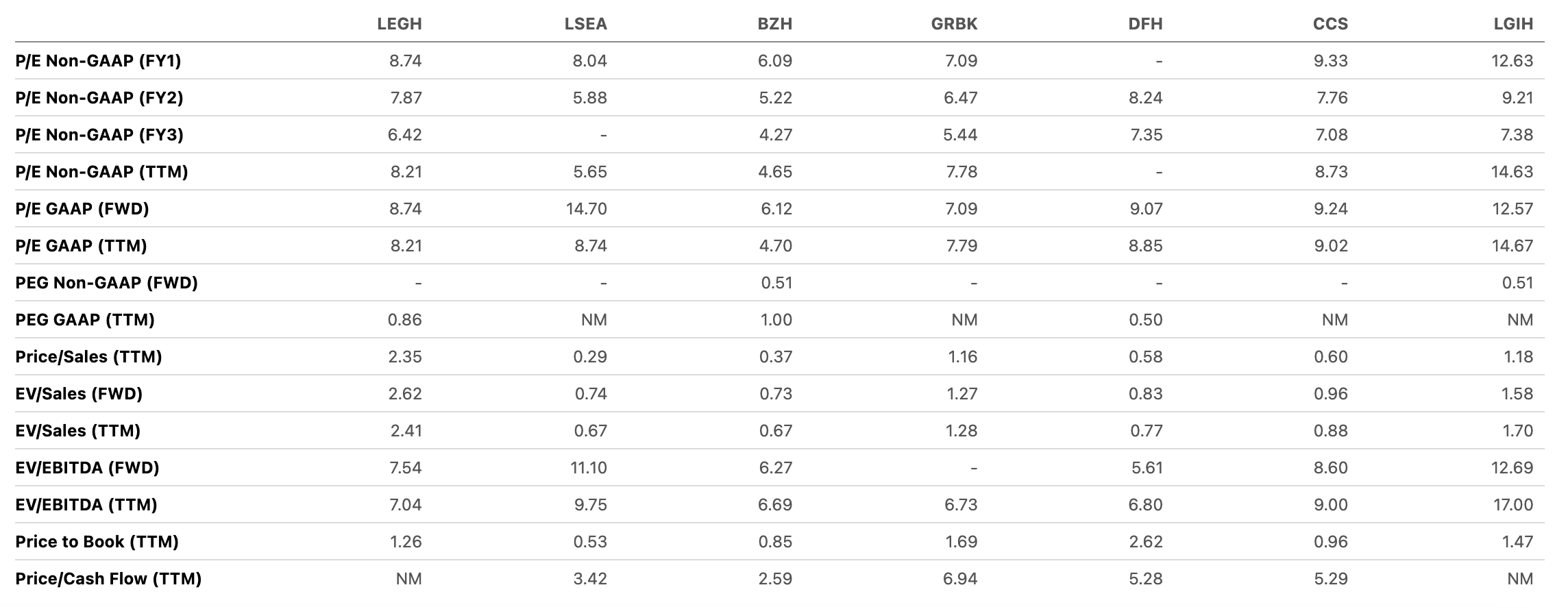

LEGH trades at 8.7x Fwd P/E which is at a discount to its long-term average of over ~10x. However, on a relative basis, the company largely trades in line with its peer average of 8.6x. Also, on Price to book basis, the company trades at a slight discount to its peer average (1.3x vs 1.4x).

{kind=link}

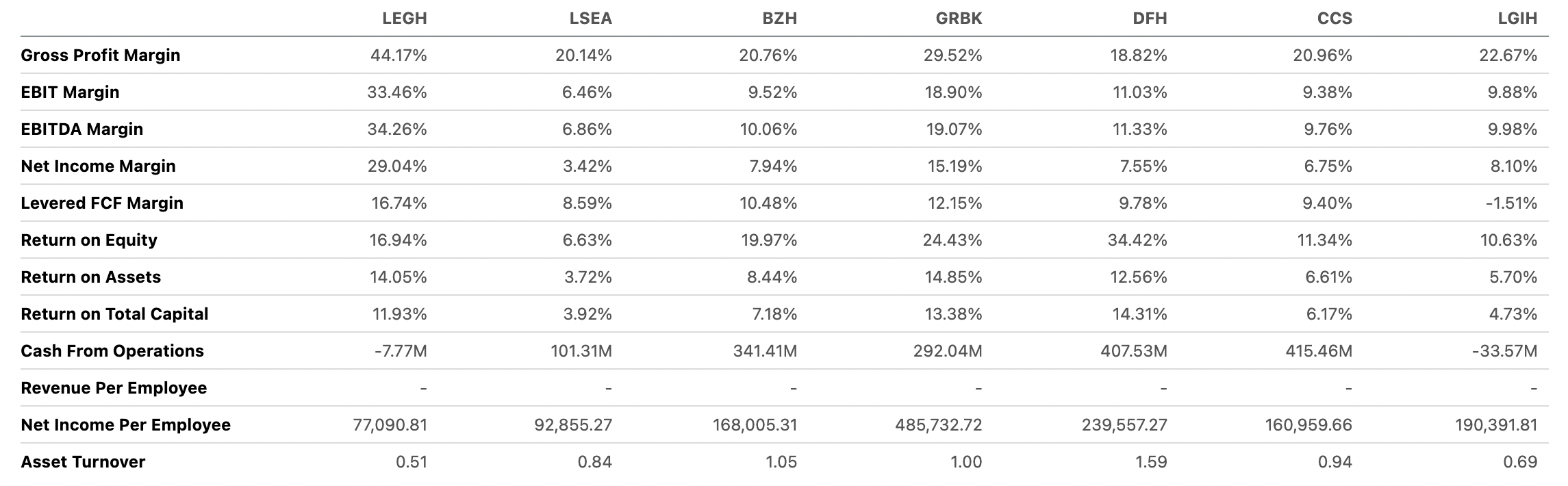

However, the company has significantly strong operating margins and net margins compared to its peers.

{kind=link}

We believe given the stronger operating margins, the company warrants a premium relative to its peers. We ascribe a 20% premium to the target multiple and value LEGH at 10.3x Fwd P/E and thereby ascribe a target price of $30. Initiate at Buy.

Seeking Alpha's Quant rating also ascribes a 'Buy rating' on the back of robust earnings momentum, positive price action as well as relative undervaluation.

Risks to Rating

Risks to rating include

1) Prolonged economic slowdown as a result of persistently higher mortgage rates can lead to significant worsening of demand

2) Gross margins can be adversely impacted as a result of higher construction costs and labor costs

3) Financing segment can have an adverse impact in case of a spike in default rates amidst current economic downturn

Final Thoughts

We believe LEGH is perfectly positioned to grow in the affordable housing space providing entry-level homes as record mortgage rates and low resale inventory continue to cripple housing affordability. Despite the near-term uncertainty in the housing market, we believe the company is perfectly positioned with its value offering and capitalize on its growth entering 2024 through the completion of its Del Valle or Bastrop County community offerings as well as a rebound in its product sales through independent retailers and expected to rebound to 3,000+ levels in 2024. In addition, its robust operating margin profile relative to peers, scale opportunity and attractive positioning provide a favorable risk reward to long-term investors. Initiate at Buy.

For further details see:

Legacy Housing: Attractive Positioning In Turbulent Housing Market