LMAT - LeMaitre: Continues To Create Value Breakout To New Highs

2023-06-14 10:14:55 ET

Summary

- LeMaitre continues to add value for shareholders on multiple fronts.

- The company's business economics support earnings and dividend growth.

- Looking ahead, the company could be worth $85 intrinsic value.

- Net-net, reiterate buy.

Investment summary

After advocating ad nauseam to allocate and size up against LeMaitre Vascular, Inc. (LMAT) over the past 3-years, the investment thesis remains unchanged, and continues to vindicate itself. Since the original buy thesis in FY'20, the company's equity stock has been valued 93% higher by the market. Critical facts underpinning the original buy thesis in FY'20 were simple:

- Consistent growth in operations since the late 1980s, balance sheet well fortified and was finally put to effective use with the Artegraft acquisition

- Eleven straight years of dividend growth , with 48.5% forward payout - that is a commitment to shareholders. In that vein, management are on our side.

- Capital structure also favours equity holders- $35mm debt used to finance Artegraft, otherwise, it is clean.

- Resilient end-markets with the company innovating around its core offerings.

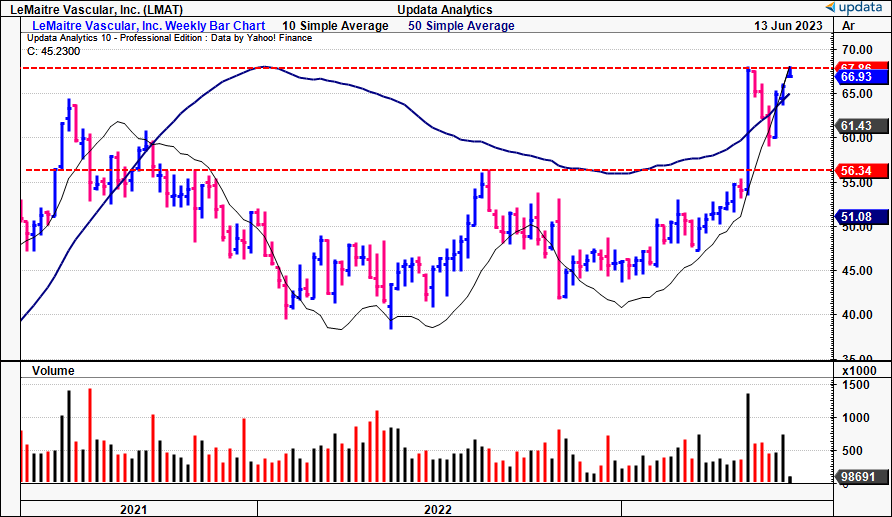

There's no major deviation from this thesis at the present day. I'll run through some additional factors pointing out why I've said to size up any LMAT positions in the long account. The stock has broken to new highs and comes out of a very attractive setup where one can observe the long-term accumulation. Net-net, I am reiterating LMAT as a buy, reinstating the $85 price target in doing so.

Figure 1. LMAY breakout to new highs

{kind=link}

LMAT revised value proposition

As a reminder, LMAT develops medical devices and human tissue cryopreservation services, selling into the peripheral vascular disease, end-stage renal disease, and cardiovascular disease markets. Since the time of its inception to now, it has built a diversified portfolio of brand-name products that enjoy high recognition among surgeons in the field.

Turning to the company's latest numbers, notable takeouts were worth discussing. These relate to the investment thesis moving forward.

One, the company booked a 13% price increase during the quarter. This was underscored by volumes of its Valvulotomes and European shunts segments. The price increase cannot be discounted and is central to LMAT's operating leverage going ahead. Thinking in first principles- revenue growth is a function of volumes and/or pricing. Therefore, LMAT's pricing gains fulfil this equation, and I would expect additional revenue growth on top of higher volumes this year. This could prove to be a meaningful tailwind over the coming 8-12 months.

Two, LMAT has been heavily investing in its sales force for the last 2 years now. It has expanded its sales to 128 sales reps as of March 31, a 14% increase from the previous year. The company plans to bolster its sales team further, aiming to reach a 135-140 headcount by year end.

By expanding its sales force, LMAT positions itself to tap into new market segments and capitalize on untapped opportunities in my view. In one light, with a bigger rep headcount, each individual rep has less area to cover, and can be more focal on penetrating one segment. Further, it reduces the amount of revenue per rep required to hit forward targets, notwithstanding the growth in turnover should they convert. In Q1, the hypothetical quarterly revenue rep was $367,968, up from $352,507 the year prior, and well up from the $296,611 in Q1 FY'20.

Three, LMAT benefited from the fact its competitors faced issues such as backorders and abandoned European MDR approvals in the quarter. While some backorders have already been resolved, several competitors have withdrawn their products from Europe due to the high costs of obtaining next-generation CE markings. Note, this is one barrier to entry in several of LMAT's end markets- something I wouldn't overlook. This presents a significant advantage for LMAT, as it can capitalize on the resulting gaps in the market and attract stranded customers looking for alternatives.

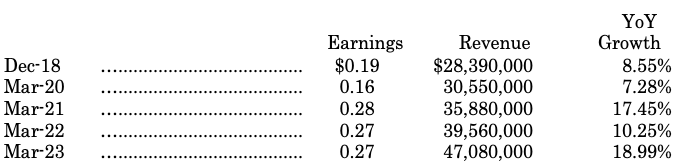

Four, LMAT's sales in Korea surpassed internal expectations, with projected 2023 revenue of $1.5mm - doubling historical sales volume relative to the ex-Korean distributor. The company's long-term record in Q1 (consolidated to 5-years in Table 1, where 2023 is shown as Q1 FY'23) speaks for itself. Earnings from $0.19 to $0.27, revenues up from $28.4mm to $47mm, with momentum building each year in growth at the top-line:

Table. 1 LMAT long-term financial statistics

Note: Figures shown as quarterly values with Q1 at each period. (Data: Author, LMAT SEC Filings)

{kind=link}

This operating performance rests abreast of an equally favourable set of economic characteristics. In that vein, LMAT's strategic initiatives extend beyond market expansion and are heavily focused on creating value for shareholders. Recently, the company agreed to acquire its Thai distributor, aiming to establish a direct presence in the Thai market by selling directly to hospitals starting in Q3 this year. Once settled, the transaction marks the 29th direct market for LMAT since it began doing business globally.

Looking ahead, there is one more catalyst that needs appreciation in my view. LMAT is set to receive Japanese approval for an additional XenoSure indication sometime this year. The label expansion is set to allow XenoSure for use in the carotid artery, starting in Q3. This approval could have a meaningful impact, given that the Q1 annual run rate for XenoSure in Japan stood at $1.9mm. By expanding the indications for use, LMAT broadens its potential customer base and total addressable market. This is definitely one way to unlock value in my opinion. Label expansions, in general, open up a higher profit pool without the investment normally required to generate growth. Hence, this adds a bullish weight to the risk-reward calculus.

Fair view of fundamentals

Financially, LMAT's performance in Q1 was impressive, with sales reaching $47.1mm, a 22% organic growth compared to Q1 FY'22. The company expects 15% organic sales growth for FY'23, (although growth rates may moderate as hospital procedure volumes normalize, as is standard in the industry). Q1 gross remained steady at 65.6%, with positive impacts of average selling price ("ASP") increases and manufacturing efficiencies. LMAT booked gross of ~65% for the entire year, with the addition of the Aziyo product line impacting the gross margin by ~half a point.

Moving down the P&L, it booked quarterly operating income of $7.9mm, clipping operating margin of 17%. OpEx rose by 28% compared to the prior year, spiked by higher selling commissions due to the significant sales overachievement in Q1. Additionally, LMAT had 16 more sales representatives in the field than the previous year, as discussed earlier. Headcount remained stable at 591 from December FY'22-March FY'23, so any additional staff above the current would be something to consider on the productivity front.

There are risks with hiring large swaths of reps as well. For one, not every rep is of the same productivity, nor is trained as easily as the other. There's also the fact of rep turnover-not revenues, but actual staff turnover. There can be a length of time to train reps as well, which can vary. Alas, LMAT projects an operating margin of 18% and 17% growth in EPS (excluding special charges) for FY'23, sensible numbers to suggest it anticipates its salesforce to be very productive.

To summarize these critical investment implications of LMAT's performance and growth prospects:

- Market expansion and challenges faced by competitors are potential tailwinds. LMAT's ability to capture market share from competitors who are undergoing challenges [such as backorders and regulatory hurdles] presents an opportunity to capture revenues and customer acquisition. Tied with its growing sales force and strategic market entry plans, LMAT could exploit these advantages well in my view.

- Geographic diversification into APAC is equally as exciting. The company's success in Korea and potentially Japan, surpassing sales expectations, and the acquisition of its Thai distributor highlight LMAT's commitment to building out its APAC markets.

- Product portfolio enhancement: LMAT's acquisition of the Aziyo product line and the potential approval of additional XenoSure indications in Japan strengthen its core portfolio offering. These additions provide opportunities for sales upside in my view and would be a net benefit to earnings and equity value.

- Long-term value-creator. The numbers around return on capital and creating value for shareholders (discussed below) don't lie.

Additional evidence of investment value

There are additional factors suggesting LMAT is well positioned to continue appreciating its market value. For one, it is fruitful to consider LMAT's long-term investment value outside of pure fundamental factors like sales, earnings growth etc. There is more at stake.

A firm is a conduit between its owners and the capital beneath its operations. Owners entrust their executives to make decisions that create value for the company's shareholders. A firm creates value for its owners (the shareholders) when it reinvests the profits it generates into new growth initiatives to generate additional profits on top. The key difference is that profits should grow faster and higher than what a hypothetical investor could generate elsewhere.

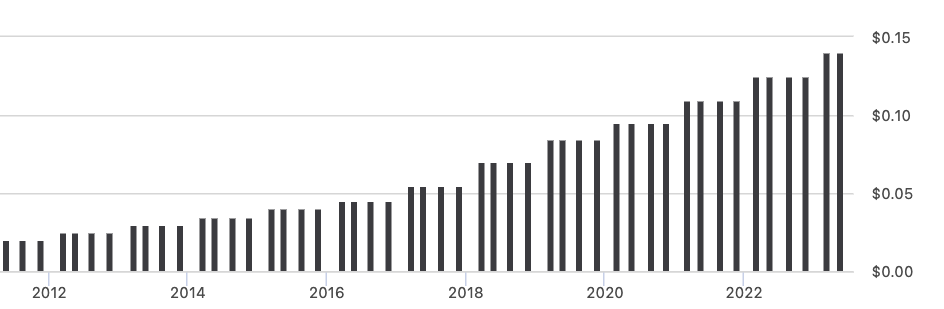

There is really no way an investor will pay a higher market value to buy a company over 5,10,15 years etc unless the firm is generating plenty of cash that it can spin off to its shareholders, either as earnings growth, dividends, or buybacks, or all three. Figure 2 also illustrates the ramp on LMAT's dividends from 2011-to date. Those with strong hands holding the stock would be pleased to have seen this kind of upside on their money.

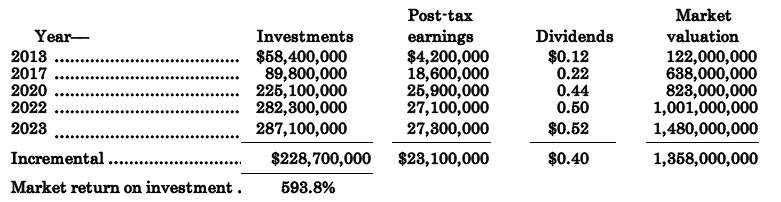

Sustaining all of this- an economically sound business engine that continues to pull the operational load up a steady incline, no matter what the conditions. Evidence of management's proficiency is observed in the same manner, in Table 2, that is. Here you're looking back to 2013 to see the progressions. It is clear to see:

- The company invested another $228.7mm to grow post-tax earnings by $23.1mm, 10.1% return on incremental investments.

- At the same time, your dividends have appreciated in the realms of 190% in the same time, $0.12-$0.54 per share ($0.40/share increase) evidencing the commitment of returning capital, and/or creating shareholder value. Note the 'step' up in each year's dividend value paid out to owners in Figure 2.

- Furthermore, the market has rewarded LMAT's investments and profit growth, prescribing an additional $1.36Bn in market value off of a $228.7mm investment, otherwise 593.8% market return on the firm's capital.

- You'll also note the company has compounded its market value each year during the testing period, not just from A to B, as investors have paid a higher valuation over time. This tells me the company's capital allocations have been successful and created value for shareholders. By my measure, these trends are poised to continue into the future as well.

Table. 2 LMAT recycling investment into additional market valuation

Data: Author, LMAT SEC Filings

{kind=link}

Figure 2. LMAT dividend growth history

{kind=link}

Valuation

There are potential concerns around the current asking valuations. The stock is priced at 56x forward earnings, 5x book value. These are nosebleed valuations that would make the deepest of 'value' players scoff in disgust. There is more to consider, and I would urge you to do so too.

A considered view, thinking in first principles, would say that investors are only accepting bids of 56x forward earnings to sell their LMAT stock. Not selling for anything below that. That would tell me of the confidence these investors have in holding LMAT, to turn down even a slightly lower bid than 56x P/E. Further, investors are happy to pay this multiple- the stock is up above all moving averages up to the 200DMA, and is trading basically at all-time highs. In the last LMAT publication, I had run through my assumptions on getting to the $85.40 equity target. Based on this information, I am maintaining this in place, noting it correlates to 74x forward earnings, above the market multiples.

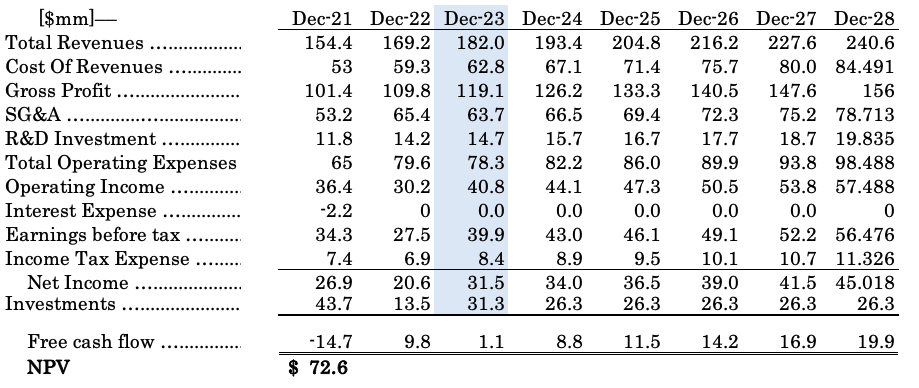

Looking forward, 8% YoY projected revenue growth gets me to $182mm in turnover for the company this year and LMAT could pull this to $78mm in operating income and $31.5mm in earnings if my assumptions pull through. I believe the company is looking attractive at a potential $72-$73 next price target, based on the projection of future estimated cash flows out to FY'28, discounted at 12% [Appendix 1]. Further out, I am getting to the $85 figure. That, and the stream of dividends adds another layer of investment income to sweeten the risk to return. As such, whilst it isn't the cheapest at the moment, I am still happy to pay the current multiples to size up against LMAT and participate in its good fortunes moving forward.

In that vein, LMAT presents with robust fundamental, market-generated, and valuation-based data to suggest it is a buy. The company's attractive business economics are exemplary of the kind of value creation I urge clients to position against in order to outperform healthcare benchmarks. Looking forward, I believe the company can do $44mm in pre-tax income in the coming year up from $30mm in FY'22, This, and the company's forward growth rate, support a buy rating in my view.

Appendix 1. LMAT Forward estimates

{kind=link}

For further details see:

LeMaitre: Continues To Create Value, Breakout To New Highs