LMAT - LeMaitre: Record Quarter ASPs And Volumes Ratcheting Higher Equals Qualified Growth Outlook

2023-08-24 17:31:22 ET

Summary

- LeMaitre Vascular's stock offers attractive long-term investment prospects, with recent consolidations offering an entry point for investors.

- The company reported record quarterly sales in Q2 and is expected to continue unlocking long-term value for shareholders.

- LMAT's investment in sales team expansion and continued asset growth contribute to its economic profitability and positive sentiment.

- Net-net, reiterate buy, eyeing $85 price objective.

Investment Summary

The stock of LeMaitre Vascular, Inc. ( LMAT ) continues to be a tactical source of alpha and still offers attractive long-term investment prospects in my opinion.

LMAT posted Q2 FY'23 numbers in early August and several investment updates must be unpacked as part of the broader investment thesis. Critically, the stock has consolidated off 2-year highs, thus offering an attractive entry point for those already long the stock to size up on value. For those new to the company, I would encourage you to comb through my numerous LMAT publications here on SA, dating back to 2020.

The last 3 publications can be observed here, in dated order (newest to oldest):

- Continues To Create Value, Breakout To New Highs .

- Remaining Constructive On Long-Term Valuations .

- Balance Sheet Ready To Unlock Risk Capital, Reaffirm Buy .

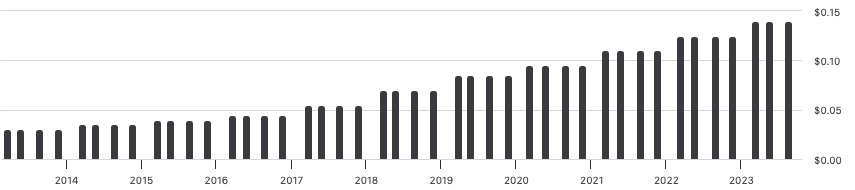

Looking to the present day, the firm continues to unlock long-term value for shareholders, with record quarterly sales in Q2, and maintaining its upsized dividend for 2023 [refer to Figure 2] . Net-net, based on the latest findings, I continue to rate LMAT a buy, eyeing an $85 price objective, the high end of the previously outlined valuation band.

Figure 1.

{kind=link}

Figure 2. LMAT 10-year dividend stream, with incremental step-ups each year. 2023 payment at $0.14/quarter, $0.56/year.

{kind=link}

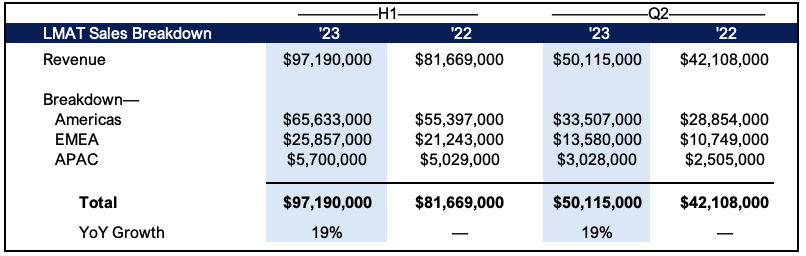

Q2 FY'23 Earnings Insights

Starting with the numbers, LMAT booked record quarterly sales of $50.1mm, up 19% YoY, with ~300bps of this attributed to the firm's non-core business. It pulled this to operating income of $9.5mm, a 63% YoY growth schedule. The growth route remains firmly on its trajectory. Management now looks to $195.4mm in full-year sales after revising forecasts higher, calling for 18% growth at the top line.

Figure 3.

{kind=link}

Higher ASPs on volume growth

Critically, average selling prices ("ASPs") maintained an upward bias, during the quarter and were up another 9%. LMAT has been employing this pricing strategy for the better part of 18 months, and it has pulled through to the top line each quarter.

More importantly, volumes on these increases ASPs have remained strong, indicating demand is resilient and LMAT is still selling at strength into its markets. Unit volumes were up 10% YoY and 6% sequentially as a testament to this. Hence, higher ASPs on higher volumes = healthy growth engine.

Just on this point:

- Underscoring the higher ASPs were valvulotomes, with prices up 14% on average, whereas shunts and artegraft sales pricing were up ~6%.

- Biologics also played a pivotal role in the record quarter and were up 23% YoY, underlined by its new distribution agreement to distribute Aziyo Biologics, Inc.'s porcine patches, with sales amounting to $1.2mm.

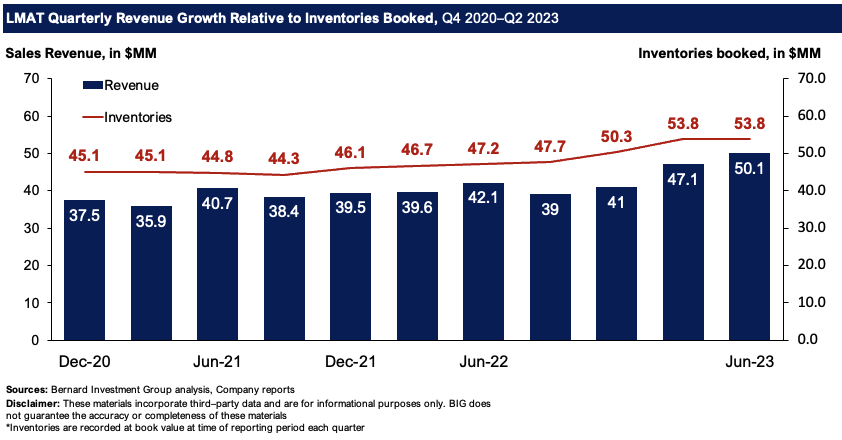

You can see these base effects in Figure 4. Quarterly revenues are plotted alongside inventories at book value as reported each quarter. Importantly, inventories on hand are consistently priced ahead of booked revenues, indicating strength in the order pipeline, and that demand is strong and thus matching order growth.

Figure 4.

{kind=link}

Moving down the P&L, it pulled the $50mm to 64% gross, and this appeared to be the major headwind in Q2 as it compressed ~200bps YoY. Surprising, given the higher ASPs and volumes listed earlier. But it was the labor costs and effect of the porcine patches impacting the product mix, as they carry a 50% gross margin vs. the company's c.65-67% longer-term averages. I'll talk more on the company's gross profitability scaled by asset growth a little later.

Investment in the rep headcount continues

Capital allocation remains a strong point for LMAT in my opinion, and we observed further investments in the sales team last quarter. It put another 22 more reps onto the books and 3 sales managers in the headcount vs. this time last year. Consider these additional points:

- Critically, it was reported a bulk of these have been on the trail for around 9 months or so, meaning they will likely be on the 'productive' side of the breakeven matrix. It finished the quarter with 133 reps (vs. 128 last quarter), thus, revenue per rep was ~$376,390 for the period, flat on Q1, and ahead of the c.$352,000 booked last year. On a simple calculus, each new rep brought on an additional $212,593 from the sequential $3.02mm gain in sales from Q1 FY'23.

- Management wants to end the year with 135-140 reps, with 3 operating in Thailand where it recently opened its first sales office. Over the next 12 months, it is eyeing Thai sales of c.$1.5mm. With the inauguration of the Thai office, it now has a presence in 13 countries, and is directly serving hospitals in 29 countries.

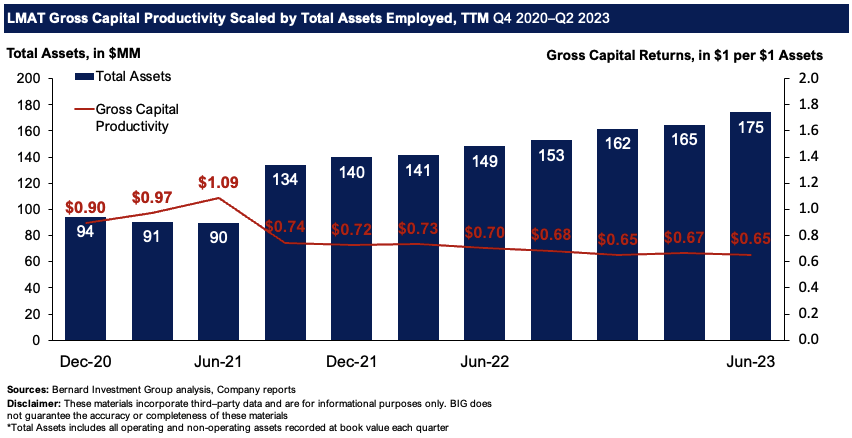

The continued investment into headcount is a critical feature of the investment debate, along with continued asset growth. Figure 5 shows the assets employed in LMAT's business, along with the gross profitability generated on these on a rolling TTM basis. Both core and non-core assets are shown. The firm is rotating back ~$0.70 in gross for every $1 tied up in company assets, a trend that's been held since 2021, despite the fact asset density is up 85% over this time. This speaks to the profitability factor, and shows the company's $175mm in assets employed return ~70% at from the top line each period.

Figure 5.

{kind=link}

Upcoming catalysts to move the needle

Recent developments in the company's APAC markets look to bear fruit into the coming periods.

For one, the company's Japan exposure has provided another positive development. Approval for its XenoSure label with an extended carotid indication has recently been secured, and it has begun moving volumes out the door already. This is potentially a bullish point, because, just as approval for XenoSure with the ephemeral indication was a key growth lever these past 3 years, the new carotid indication could possibly act in the same fashion. I'll be watching this segment very closely moving forward.

Second, in China, management's confidence of receiving a XenoSure cardiac approval in 2024 is high, followed by peripheral indications in 2025. These are two inflection points to keep an eye out for over the coming 12-24 months.

Third, in Europe, it also has expectations of gaining allograft approval either in Ireland or Germany by 2024. Additionally, plans to file for CE Mark approval of artegraft in December 2023 are in place. Regulatory costs have lifted by ~35% YoY due to ongoing efforts to secure the MDR CE mark.

Sentiment remains high

The positive sentiment in LMAT's stock is observed in two primary ways.

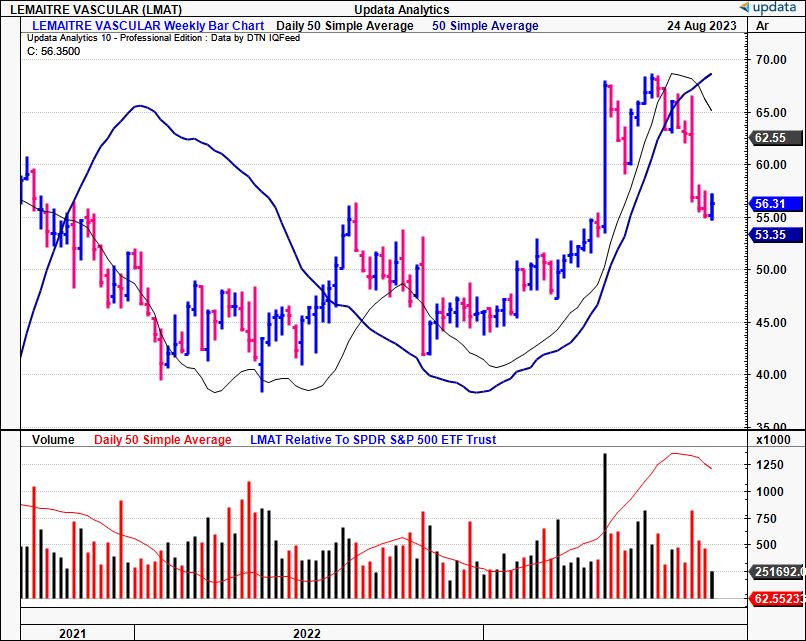

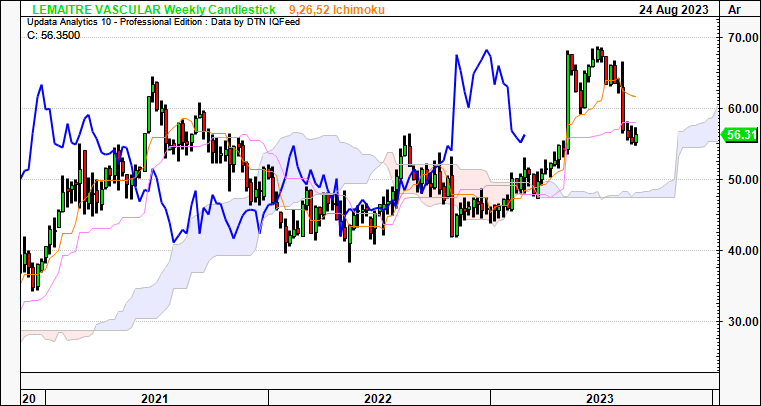

One, keeping a long-term view in mind, one can see the long-term market trend in Figure 6 (the weekly cloud chart). Both the price line and lagging line are above the cloud, indicating bullish positioning within the long-term trend. Critically, even with the sharp pullback, there is room to consolidate and remain on a bullish path. I'd be looking to support at ~$60.00 by December based on this outlook, given the weekly chart looks out to the coming months. This is bullish in my view.

Figure 6.

{kind=link}

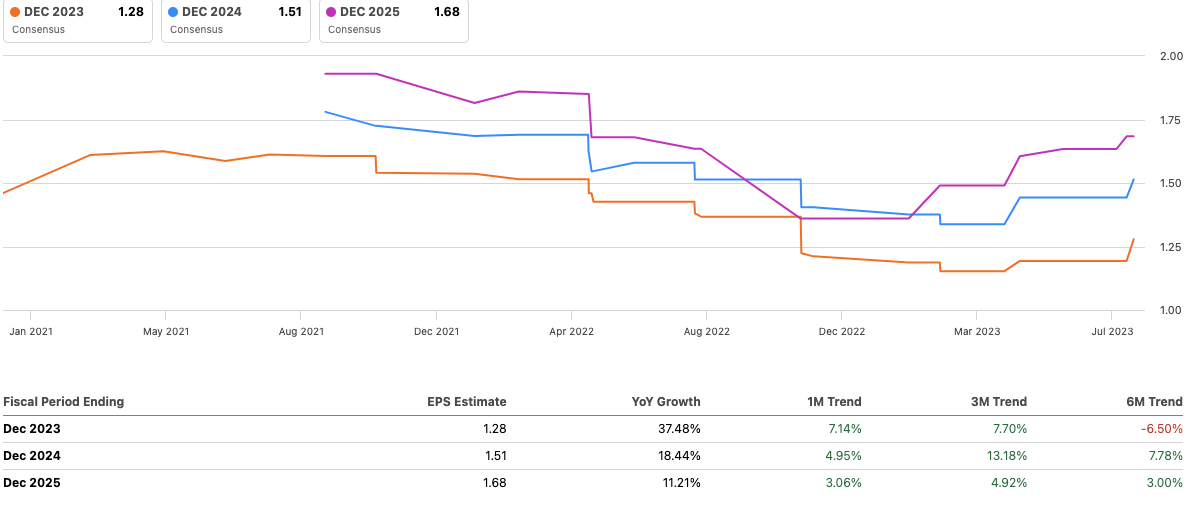

Two, there have been 7 revisions to revenue estimates and 5 upward revisions to earnings estimates from Wall Street analysts in the last 3 months. These targets represent a large subset of the market populous and thus indicate the viewpoint of a swarm of investors et al. at this point in time. I typically look for at least 3-4 upward revisions to each, so the fact there's been 5 or so is a bullish sign on the sentiment front in my opinion. The street now expects 37% YoY growth in earnings this year and another 18% at the bottom line in FY'24.

Figure 7.

{kind=link}

Valuation

In the last publication, I outlined the case for LMAT to sell at $72/share in the base case, with upsides of $85 in the more aggressive modelling. The stock still sells at a premium to peers at 25x forward EBITDA, but this is also a 13% premium to the company's 5-year average. This tells me LMAT continues to attract valuation upside and has rated higher over the 5 years to date. The market also values its net assets at a premium of $4.44 for each $1 in NAV, suggesting the capital LMAT has employed into the business is deemed as valuable and the propensity for high earnings power moving forward.

Based on the revised estimates from management and my own findings, I'm getting to $193mm in sales for FY'23, whereas I'd forecast this number not until FY'24. Hence, I'm looking more to the $85 figure and will be revising my next price objective to this mark here today. This sports a 51% value gap and more than attractive margin of safety in buying/sizing up LMAT on the long account today. The company's forward dividend shouldn't be excluded from this view either, on a forward payout of $0.56 per share.

In short

LMAT continues to present with long-term economic value for the equity risk of multi and/or single-asset portfolios going forward. The company's record quarterly sales are supported by robust economic characteristics that support earnings power and capital return to shareholders downstream. The stock continues to attract premium multiples, and trades above 5-year average multiples as I write. All roads point to the company extending this performance into the coming 12 months, with additional growth levers just activated in its APAC markets. Net-net, reiterate buy, eying $85 price objective going forward.

For further details see:

LeMaitre: Record Quarter, ASPs And Volumes Ratcheting Higher Equals Qualified Growth Outlook