KTB - Levi Strauss & Co.: Still Worth Trying On

2023-03-24 08:26:17 ET

Summary

- Levi Strauss & Co. has failed to live up to my previous bullish stance on the firm, largely because of temporary weakness on its top and bottom lines.

- This is disappointing, but shares look attractively priced right now, and investors need to pay attention to the long run.

- Management has mixed expectations for 2023, but they continue to focus on growing the company at a nice clip over the next few years.

As an investor, I do my best to focus on the long run. That does not mean that the short run doesn't bother me. From time to time, short-term results can reduce my optimism regarding an opportunity. But at the end of the day, you need to step back and evaluate the entirety of the picture, including the long-term potential of what it is that you are buying shares in. Although I do not own shares in this particular firm, one company where I think this is important right now is Levi Strauss & Co. ( LEVI ). The most recent financial data provided by management has shown weakness on both the top and bottom lines for the business. Even so, the outlook for the company for the next few years looks positive and shares are priced at attractive levels that indicate upside exists around the corner. So although things might not be going exactly as planned, I do still think that the company warrants a 'buy' rating at this time.

Short-term pain

Back in July of last year, I found myself taking a bullish stance on Levi Strauss & Co. Up to that point, the company had fared quite poorly for a number of months, with shares following the broader market lower. This was in spite of the fact that both top line and bottom line numbers reported by the company were coming in incredibly strong. That performance, combined with how cheap shares became, ultimately led me to rate the business a 'buy' to reflect my view that the stock should outperform the broader market moving forward. Unfortunately, since then, things have not played out exactly as I thought they might. While the S&P 500 is up 6.3%, shares of Levi Strauss & Co. have seen an upside of only 1.8%.

{kind=link}

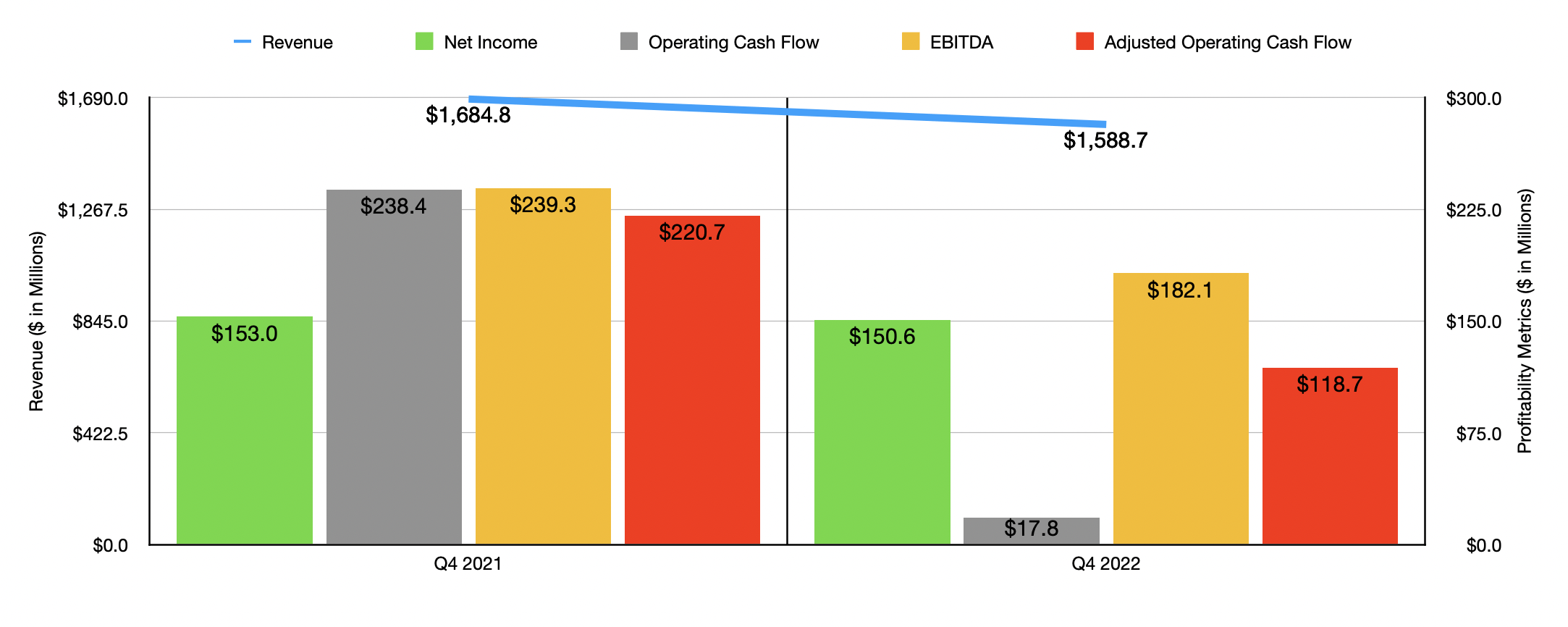

To understand why recent performance has been lackluster, I think we need only point to the most recent data offered up by management. This data includes results for the final quarter of the company's 2022 fiscal year. During that time, revenue for the business came in at $1.59 billion. This is actually down about 5.7% compared to the $1.68 billion reported one year earlier. Digging deeper, we find that all of this pain was driven by foreign currency fluctuations. On a constant currency basis, revenue would have been flat year over year. Even so, this is not great for a company that's pushing for long-term growth. The biggest weakness for the company involved its wholesale activities. Even on a constant currency basis, wholesale revenues were down about 4% year over year. In terms of specific geographic area, the greatest weakness was in Europe, with revenue dropping around 8% on a constant currency basis. Macroeconomic issues, combined with the suspension of the company's operations in Russia, resulted in this pain. But in the Americas, sales also took a beating, with constant currency revenue down 5%, largely in response to supply chain challenges and the decision by retailers to rebalance inventory levels because of changing market conditions.

{kind=link}

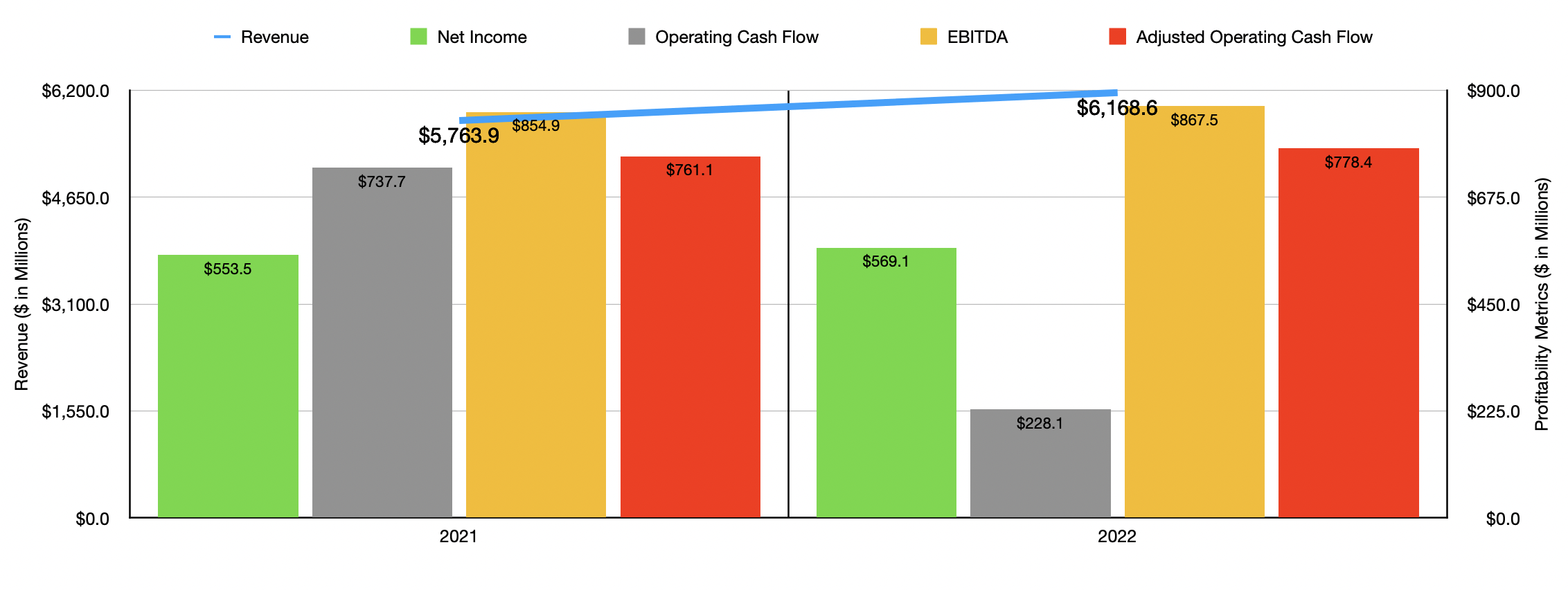

The drop in sales for the company brought with it a decline in profits. Net income, for instance, dipped from $153 million to $150.6 million. Operating cash flow fared worse, plunging from $238.4 million to $17.8 million. If we adjust for changes in working capital, we would see that metric decline from $220.7 million to $118.7 million. Meanwhile, EBITDA for the company shrank from $239.3 million to $182.1 million. Despite these troubles, the 2022 fiscal year as a whole was actually quite positive compared to 2021. These results can be seen in the chart above.

{kind=link}

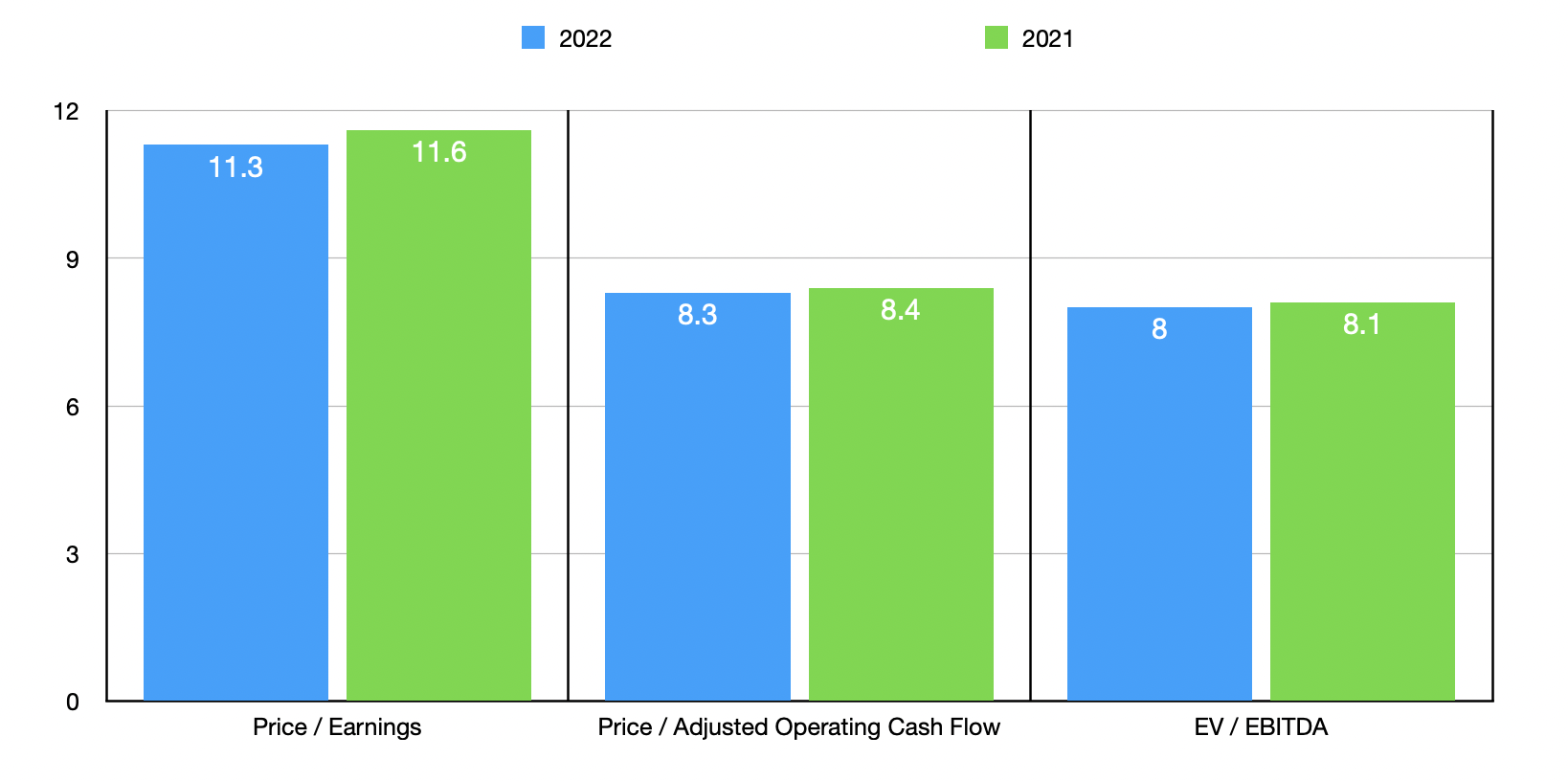

When it comes to valuing the company, it is worth noting that shares look quite affordable at this time. Using data from 2022, I calculated that the company is trading at a price-to-earnings multiple of 11.3. That's down from the 11.6 reading that we get using data from 2021. The price to adjusted operating cash flow multiple should be 8.3 compared to the 8.4 we get using data from the year prior. And the EV to EBITDA multiple will have dropped from 8.1 to 8. As part of my analysis, I did compare the company to five similar firms. On a price-to-earnings basis, the company is rather lofty, with four of the five firms trading cheaper than our prospect. On a price to operating cash flow basis, only one of the companies was cheaper than our target, while using the EV to EBITDA approach, we get three of the five firms cheaper than it.

| Company |

| Price/Earnings |

| Price/Operating Cash Flow |

| EV/EBITDA |

| Levi Strauss & Co. |

| 11.3 |

| 8.3 |

| 8.0 |

| G-III Apparel ( GIII ) |

| 4.5 |

| 7.3 |

| 4.8 |

| Capri Holdings Limited ( CPRI ) |

| 8.4 |

| 10.2 |

| 6.1 |

| Gildan Activewear ( GIL ) |

| 11.0 |

| 14.4 |

| 8.9 |

| Delta Apparel ( DLA ) |

| 6.8 |

| 99.2 |

| 6.2 |

| Kontoor Brands ( KTB ) |

| 11.6 |

| 34.0 |

| 8.9 |

The future looks brighter

What we have so far is a company that looks more or less fairly valued compared to similar businesses, but that does look, in my opinion, cheap on an absolute basis. However, recent performance suggests that the firm is definitely susceptible to pain, with declining revenue pulling back on profitability. Because of the economic environment that we are dealing with right now and the uncertainty that it brings to the table, I can understand why investors might be a bit cautious at this moment. However, the data moving forward still looks very positive.

For starters, when it comes to the 2023 fiscal year, management expects revenue to come in at between $6.3 billion and $6.4 billion. That represents a year-over-year growth rate of between 1.5% and 3%. Which really impressive is that this growth is after factoring in a roughly 2% negative headwind anticipated by foreign currency fluctuations and the suspension of business operations in Russia. Earnings per share, meanwhile, should come in at between $1.30 and $1.40. At the midpoint, that would translate to net income of $540.3 million. That would be down slightly from what the company saw in 2022 when it reported profits of $569.1 million. Of course, this does not factor in what might happen with the number of shares the company has outstanding. Last year alone, management repurchased 8.7 million shares of stock for $176 million. A change in share count could definitely impact net profits.

{kind=link}

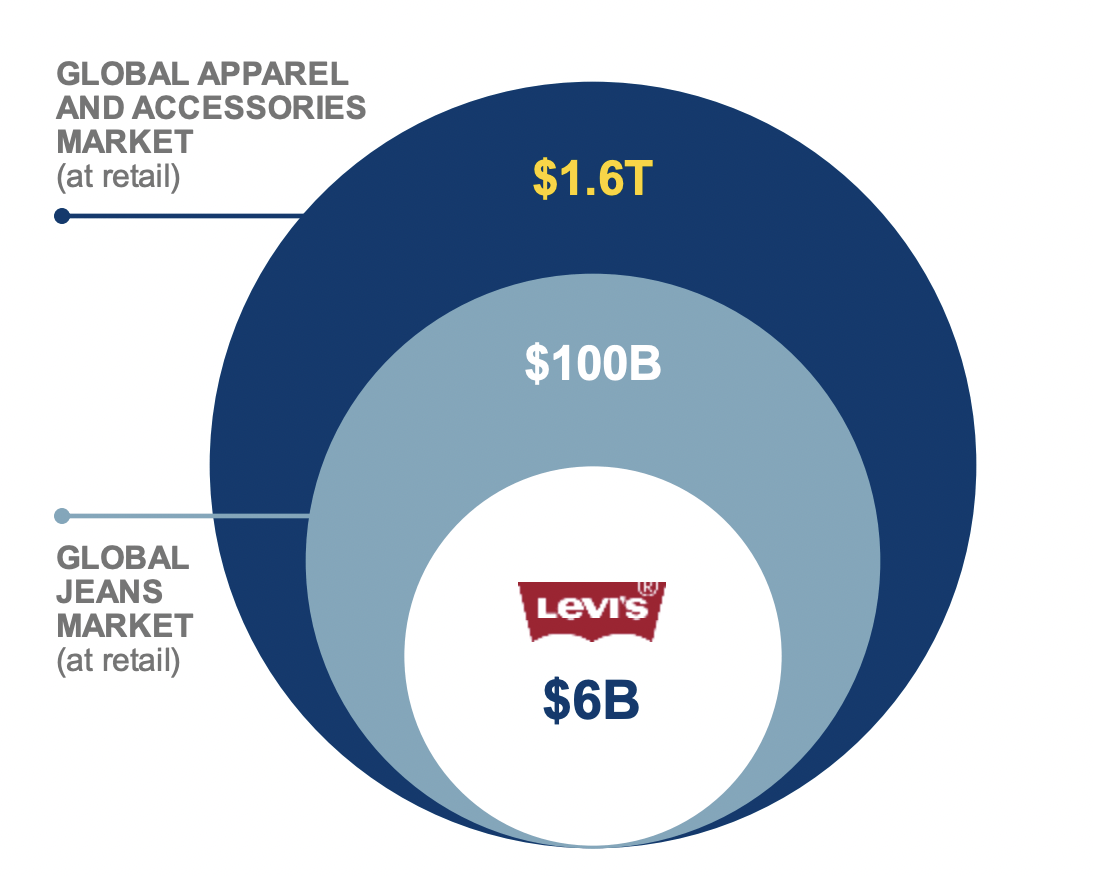

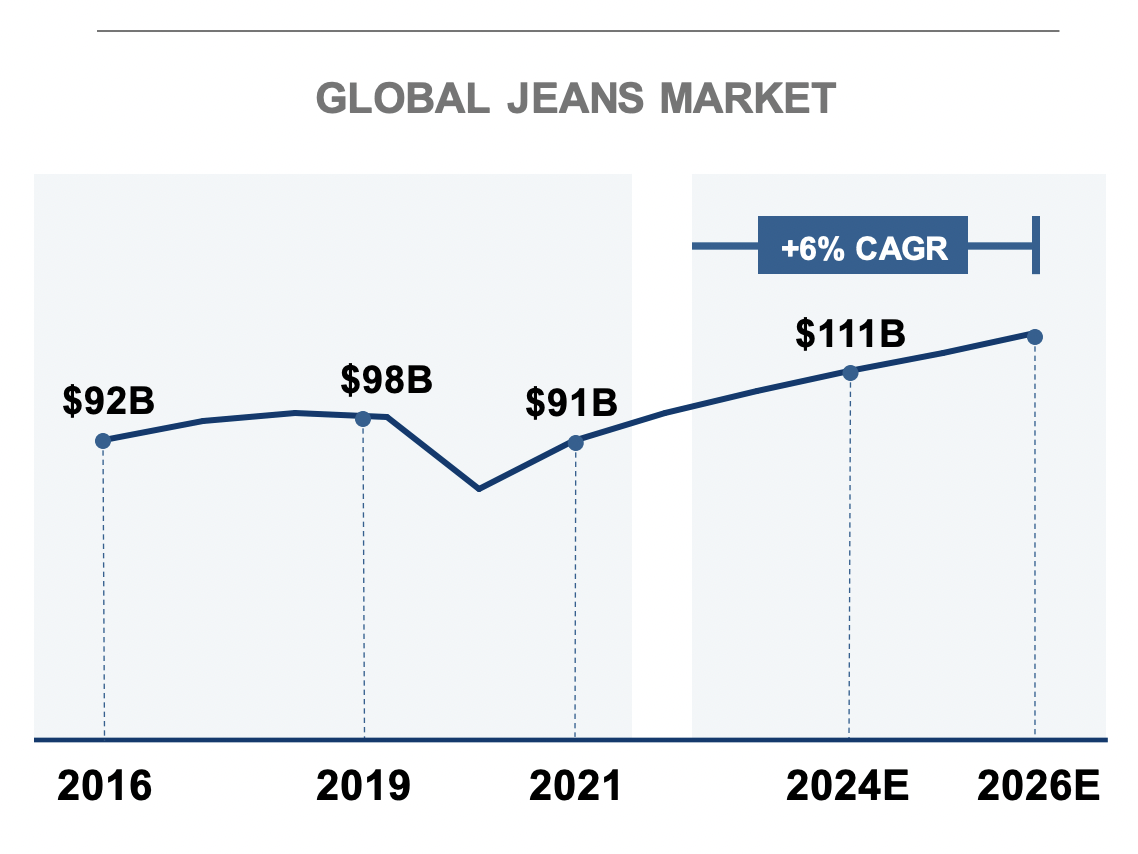

What we have on the top line is a scenario where growth looks set to continue. But on the bottom line, it does look as though 2023 might be a bit problematic. But when we step back even further and focus on the long term , the picture does look more appealing in my view. You see, management has provided some good details about the market in which they operate. The global apparel and accessories market has been estimated to be worth around $1.6 trillion. The global jeans market is a fairly sizable chunk of that, valued at roughly $100 billion. That means that Levi Strauss & Co. has a roughly 6% stake in the global market. While that does make the company a rather big player, it does also mean that significant growth potential exists. This is especially true when you consider that the market for jeans is expected to continue growing for at least the next few years. By 2024, the market should be worth around $111 billion before ultimately hitting $124.7 billion in 2026.

{kind=link}

By focusing on its e-commerce operations, as well as by continuing to cater to its core brands, the management team at Levi Strauss & Co. hopes to grow revenue to between $9 billion and $10 billion by 2027. Earnings per share, meanwhile, are forecast to decline to around $2.70. This growth will be driven by a number of factors. For starters, the company is hoping to grow its international footprint such that, by 2027, around 57% of its revenue comes from overseas. That's up from the 47% reported for 2015.

{kind=link}

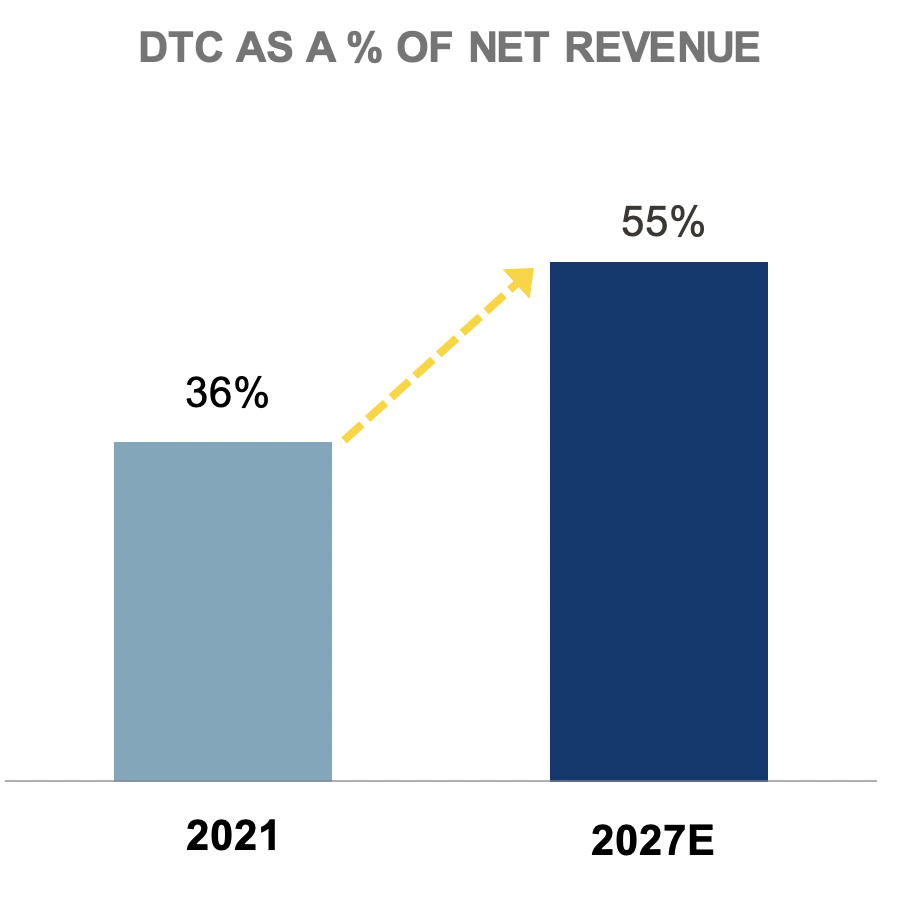

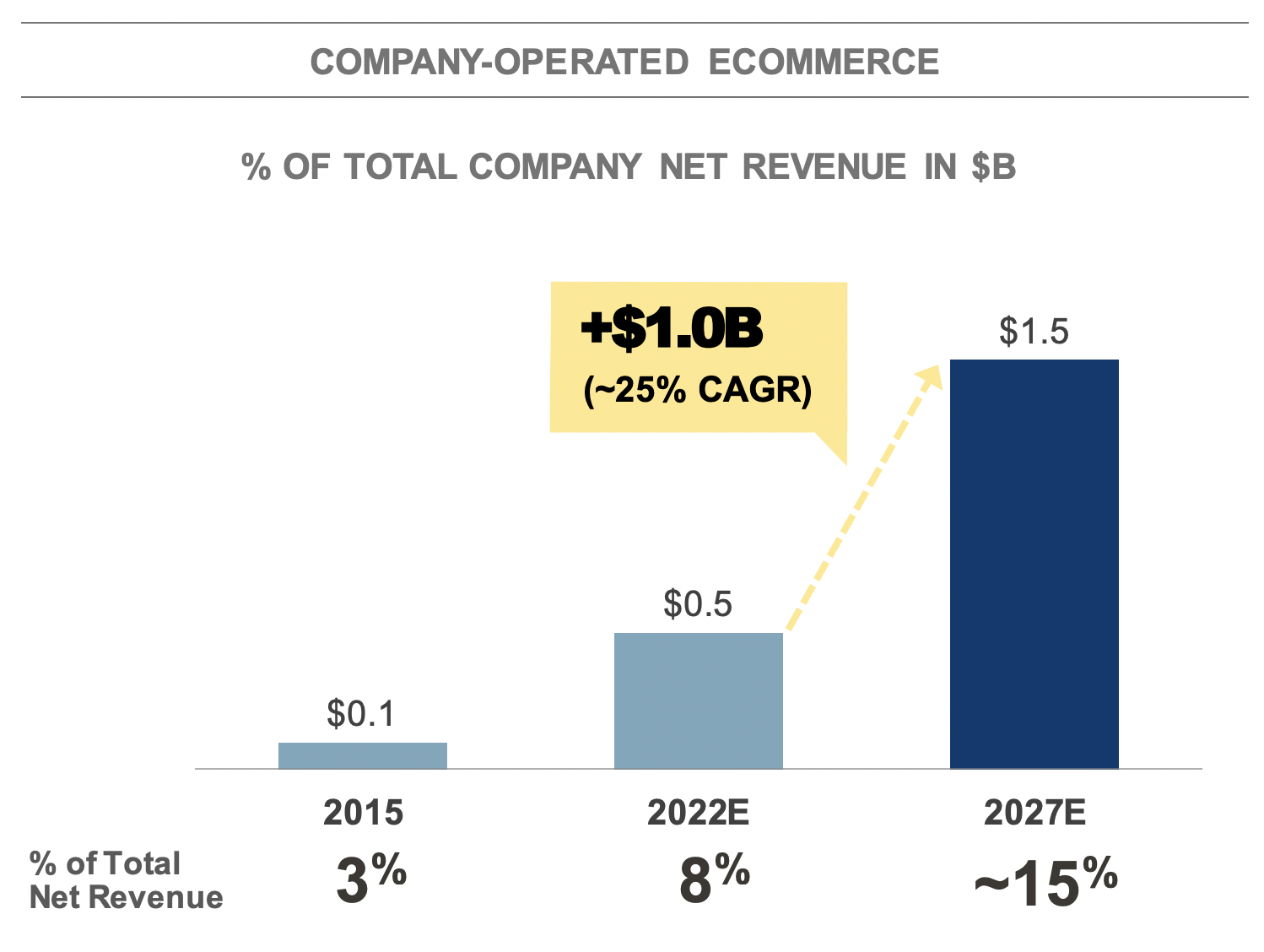

During this same time, the company also hopes to grow its direct-to-consumer operations from 36% of overall sales to 55%. A big part of this will be a push for the e-commerce portion of the company to roughly 15% of sales by 2027. That's roughly triple the amount of revenue the company got from these activities back in 2022. The direct-to-consumer side of the business also includes the company's operated stores. While continuing to leverage its franchised and licensed stores and shop-in-shop setups to grow, particularly overseas, the company does also plan to grow its number of operated stores from 1,089 to 1,550 by 2027. If management does turn out to be accurate and their forecasts, the price of the company should become even more appealing as time goes on. After all, using the earnings forecast for 2027 would yield us a price-to-earnings multiple today of 6.1 compared to the 11.3 reading that we get using data from 2022.

{kind=link}

Takeaway

Operationally speaking, Levi Strauss & Co. seems to be doing quite well in the grand scheme of things. Recently, financial performance has pulled back some. Some of this is because of foreign currency fluctuations, but it is clear that bottom line issues will continue through at least this year. Even so, shares of the company look attractively priced on an absolute basis, even while being perhaps fairly valued compared to similar firms. Add on top of this management's growth plans, and what that means for the company's valuation moving forward, and I do believe that enough upside potential exists here to warrant the original 'buy' rating I previously assigned the business.

For further details see:

Levi Strauss & Co.: Still Worth Trying On