LPSN - LivePerson Could Be Poised For A Turnaround

2023-10-27 09:46:56 ET

Summary

- LivePerson's stock has plummeted, but it has the potential for a turnaround play.

- LivePerson faces risks and competition in the AI space, but its focus on core B2B solutions and new AI products could drive growth.

- The ousting of its former CEO should be good for the company.

- Given past valuations in the space, the stock has a lot of potential upside.

While LivePerson ( LPSN ) has been a disaster, the stock could have the recipe to be a nice turnaround play.

Company Profile

LPSN operates a cloud-based platform that allows consumers to interact with organizations through conversational interfaces, such as in-app and mobile messaging. One of the company's solutions main focuses is to route voice calls to messaging and other digital channels, saving its customers money in the process.

The company's Conversational Cloud platform helps organizations best connect with their customers through a combination of human agents, chatbots, and Conversational AI. The platform works through a variety of voice and messaging channels, including SMS, WhatsApp, voice, Facebook Messenger, in-app, and other channels to reach the customers where they prefer to connect.

The company also owns some other businesses that it has acquired over the years. This includes German conversational AI company e-bot7; real-time speech recognition and conversational analytics firm VoiceBase; and Tenfold, which integrates communication systems with CRM platforms. Last year it bought WildHealth, which looks to give people a blueprint for optimal health by combining machine learning with DNA analysis, biometrics, microbiome testing, and phenotypic data.

Opportunities and Risks

With its stock down over -75% year to date and -88% over the past five years, a lot of things have obviously not been going LPSN's way recently.

The company will have a new CEO for the first time after founder Robert LoCascio stepped down, while CFO John Collins was named interim CEO. LoCascio was a brash visionary CEO, but one who turned a lot of people off, leading to a lot of executive turnover at the company over the years. He also seemed to get distracted by a lot of non-core ventures. With the company in complete disarray the past couple of years, getting new leadership should be a positive. However, it still hasn't named a permanent CEO, so we'll have to see who it can attract to help turn the ship around.

That said, the company has a well-respected activist in the name of Starboard. If the company works with the firm, it should be able to get someone who can help the company in its turnaround efforts. It's also notable that two main competitors have been acquired in the past couple of years, with Microsoft ( MSFT ) buying Nuance and an investor group taking Zendesk private.

When looking at themes, AI is probably both the biggest opportunity and risk for the firm. The company is a leader in conversational AI and earlier this year launched new generative AI products and platforms.

Discussing its new offerings in its Q2 earnings call , CFO and interim CEO John Collins said:

"Last quarter, we launched an expansive set of generative AI-powered products across the Conversational Cloud. These products provide a significant uplook to agent efficiency, and enable automation to operate on the long tail of consumer intent. Using generative, we are also automating previously manually intensive labor, to accelerate time to value for customers. We also launched voice AI, which meaningfully extended LivePerson's automation products to the voice channel, opening the door to approximately 70% of the conversations currently taking place between consumers and brands. This significantly expands our serviceable market. The intent of voice AI, is not to compete with incumbent voice solutions, which focus on the needs of agents and synchronous contact center operations, but instead to shift traditional voice calls, including those trapped in the IVR into an AI-powered automation flow, which we see as the future of customer service. …Voice AI, for us, again, is opening up a new channel for the first time for LivePerson to deploy automation where the vast majority of the conversations are taking place today. And I think what differentiates LivePerson is this enterprise readiness. It's existing back-end integrations, the flows for the contact center operation that have been honed over decades and installing the voice AI within that wider ecosystem is what makes it a powerful solution, much more powerful than simply tapping an API from OpenAI without all of that other infrastructure behind it."

Most of LPSN's AI capabilities have been in the messaging realm, so extending it into areas like voice, virtual assistants, automation, and analytics represents a nice opportunity. The company has a lot of conversational data sets built up over the years, so should be able to translate that into some nice new capabilities.

At the same time, the pace of AI advancement also leaves the space becoming more competitive and open to commoditization. The company saw this with chatbots many years ago, and some experts are already predicting that large language models will become commoditized in the not-so-distant future. So while LPSN should be able to benefit from new products, how long these stay at the cutting edge is a risk. The company also faces plenty of competition from some big pocket competitors as well, including the likes of Amazon ( AMZN ) and Salesforce ( CRM ), among others.

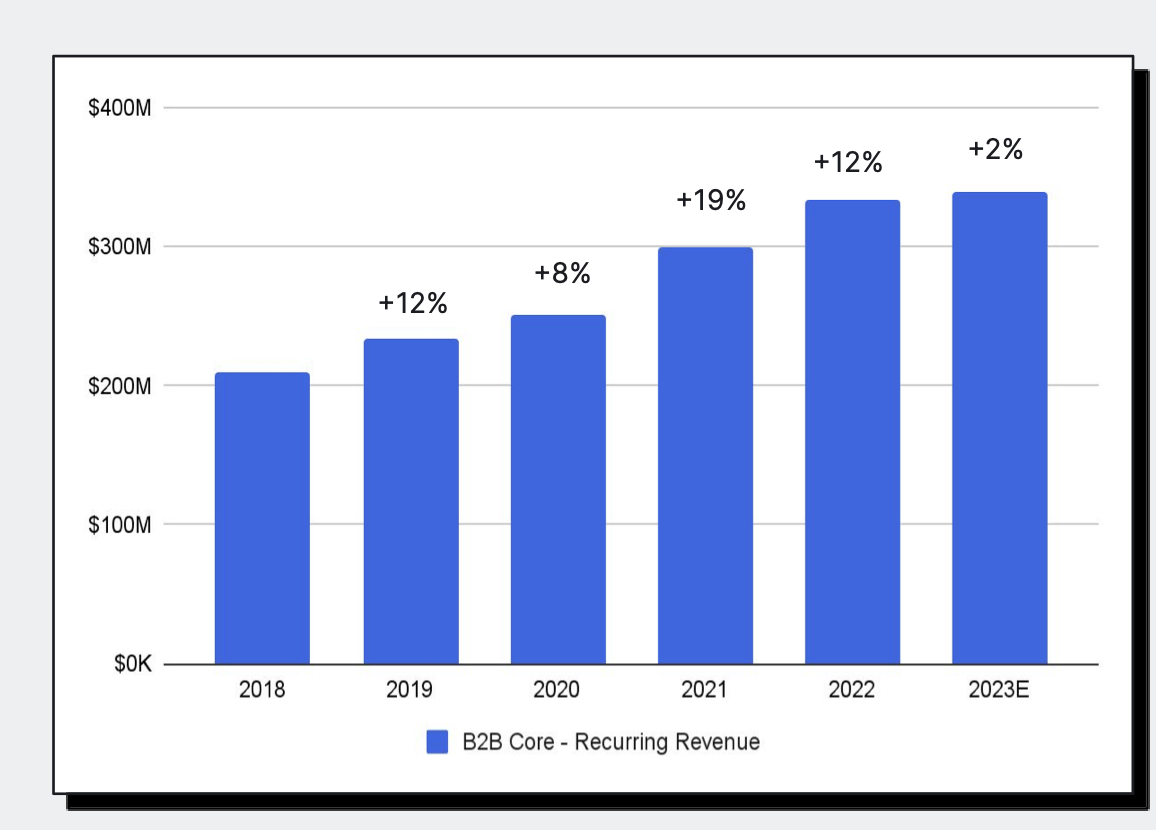

LPSN has also been undergoing a restructuring of its business that will have it focus on its core B2B solutions. It divested Kasamba in Q1, which was an odd business that connected people to psychics for online psychic readings. It also took out $200 million in costs and eliminated about $70 million in low-margin, non-core revenue.

Its B2B business has been pretty solid, growing core revenue every year since 2018. Core B2B revenue includes recurring revenue, professional services, one-time charges, and overages. While it is experiencing a more difficult 2023, the segment is still projected to see core revenue up 2%.

{kind=link}

When looking at additional risks, the company has been burning cash, generating -$46.5 million in free cash flow through the first six months of 2023. It also has $582.6 million in convertible debt on its balance sheet against $214.8 million in cash. The bulk of these are notes that mature at the end of 2026. They carry 0% interest and have an initial conversion price of approximately $75.23 per share. It also has $120 million in potential payments to WildHealth investors if certain milestones are met.

Valuation

LPSN trades at an 11.8x EV/EBITDA multiple based on the 2023 EBITDA consensus of $28.1 million. Based off of the 2024 EBITDA consensus of $43.3 million, it trades at around 10.4x.

On an EV/S multiple, it trades at 1.4x 2023 revenue of $399.5 million and 2024 revenue of $404.7 million.

The company is projected to see revenue decline nearly -22% this year, in part due to its divestiture of Kasamba, and grow 1% next year.

Two of its closest public peers were bought out in 2022. Nuance was bought out at over 14x revenue multiple with little growth, and Zendesk was acquired at a 7.6x multiple with growth of over 25%.

Conclusion

While obviously a risky bet given its struggles over the past several years, LPSN could be set up to be a turnaround play next year. The company has gotten rid of its reckless CEO and turned its focus to its core business. It's improved its cost structure and has gotten rid of some weak business lines, while it is looking for new AI products to help spur growth.

Despite its struggles, the company is still winning new customers in its core business, which is still growing. With peers getting some pricey multiples in buyouts and Starboard behind it, it could be a potential buyout candidate itself down the line.

All in all, LPSN is a speculative idea, but given its valuation, Starboard's involvement, and the ousting of its CEO, I think the stock is an interesting speculative "Buy" candidate, that could see a nice January Effect rally next year. The stock has an upside to $15-20 in a turnaround or buyout scenario, representing a 2-3x revenue multiple. While that seems like a crazy jump, it is worth noting that Starboard was buying shares at over $33 .

For further details see:

LivePerson Could Be Poised For A Turnaround