LYG - Lloyds Banking: Sticky Interest Rates Support Recovery Though Risks Remain

2023-07-17 05:40:26 ET

Summary

- Despite economic challenges in the UK, Lloyds' operational diversification strategy, undervaluation, and expansion to mass affluent consumers support long-term growth.

- LYG's long-term strategy includes scale growth, diversification, and digital access to reach a larger number of consumers.

- The bank has reported Q1 revenues of $11.31bn, a 105.12% YoY increase, and a net income of $1.83bn, up 13.63% YoY.

The Lloyds Banking Group ( LYG ) is a London, England-based multinational financial services firm, with operations across retail banking, commercial banking, corporate banking, life insurance and pensions through its subsidiaries, Lloyds Bank, Halifax, the Bank of Scotland, and Scottish Widows.

{kind=link}

{kind=link}

Through its activities, Lloyds has seen Q1 revenues of $11.31bn, a 105.12% YoY increase, alongside a net income of $1.83bn, up 13.63% in the same time frame.

Introduction

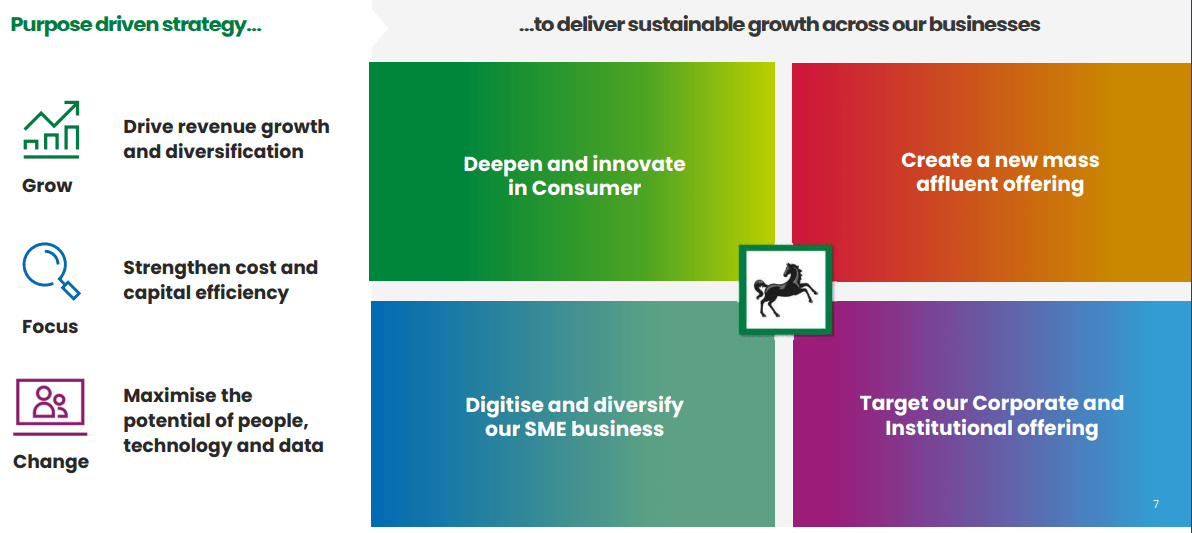

At the heart of Lloyds' long-run strategy remains the threefold objectives of scale growth and diversification, to ultimately drive stability, develop into a more capital-effective organization- preferably with a less debt-driven cap structure, and maximize productivity and accessibility to a more significant number of consumers through talent retention, digital access, and data analytics.

Over the coming strategic timeframe, Lloyds aims to implement its strategy through innovations and operational efficiencies across its consumer division, targeting the higher-end of mass market banking consumers, as to boost profitability, diversification within Lloyds' commercial banking, and increased exposure to institutional and corporate offerings.

{kind=link}

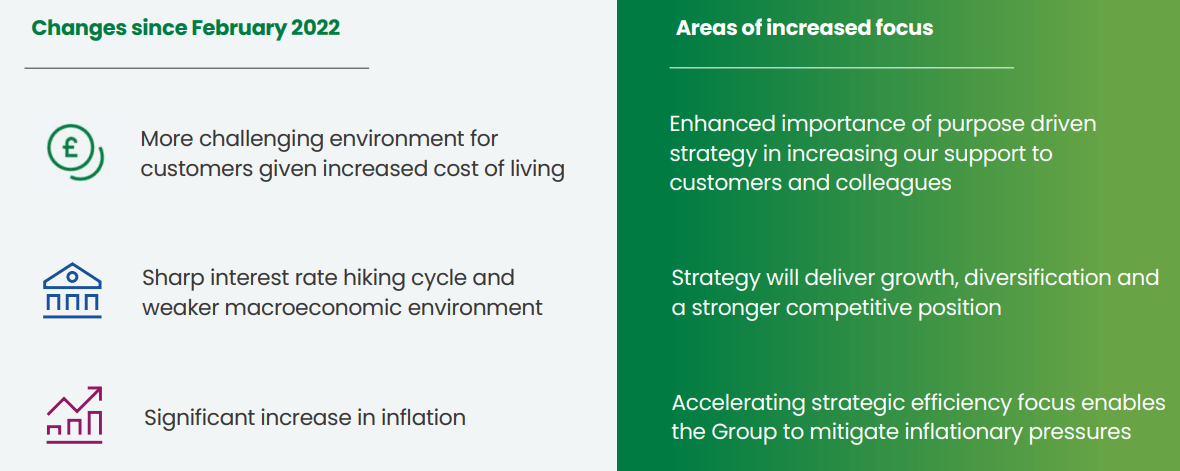

All this works within the macro-financial environment, which is becoming increasingly hostile to lower-end mass market consumers, is seeing increasing and sticky interest rates- particularly in the inflation-ridden UK- as a long-term theme, and said inflationary pressures impacting third-party demand and capital supply for Lloyds.

{kind=link}

Therefore, although the UK is facing significant economic headwinds, I believe Lloyds' operational diversification strategy works alongside its undervaluation, and mass affluent expansion to support long-run growth, leading me to rate the firm a 'buy'.

Valuation & Financials

General Overview

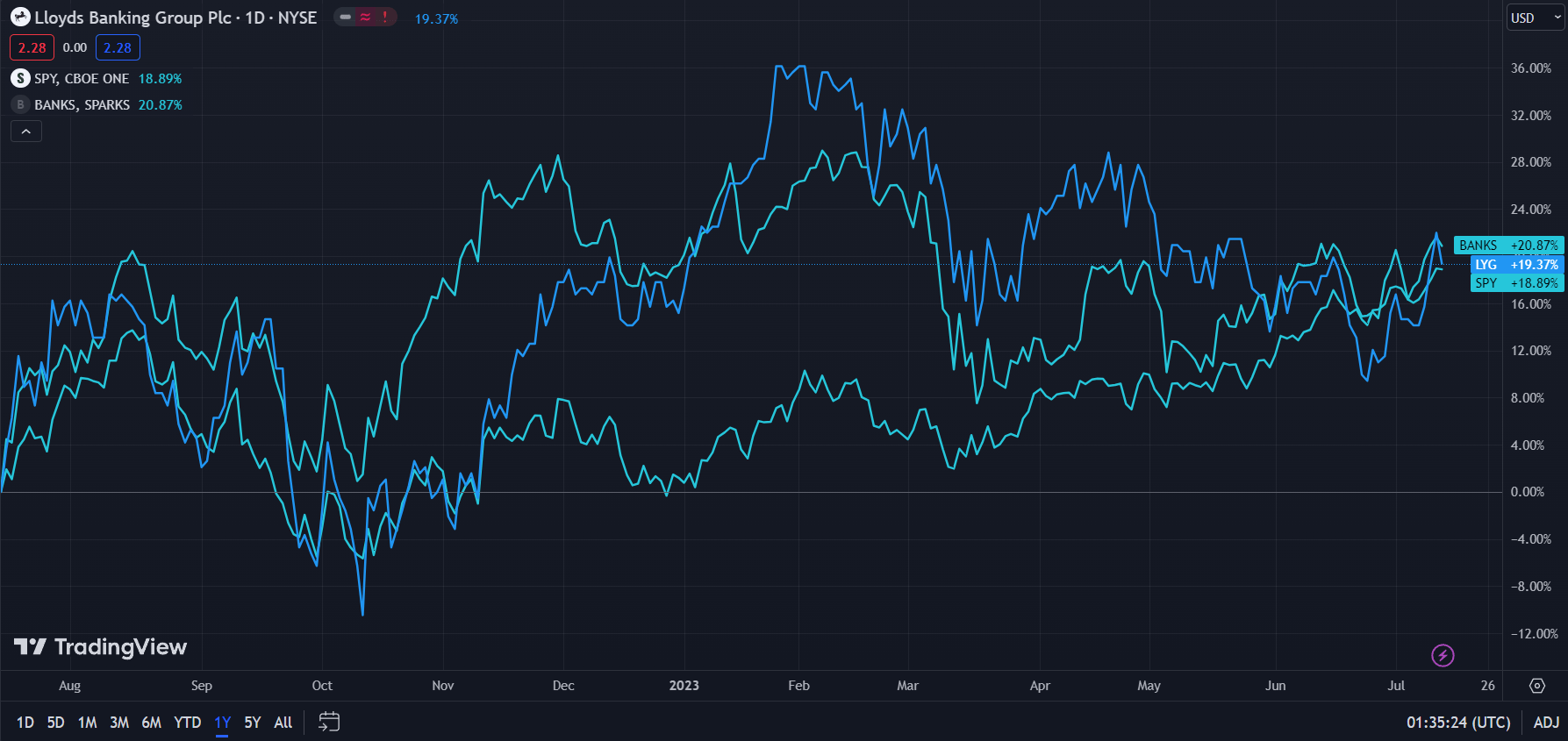

In the TTM period, Lloyds' stock- up 19.37% for the year- has experienced middling, but similar, growth between the TradingView Banking Index- up 20.87%- and the general market, as represented by the S&P 500 ( SPY ) - up 18.89%.

{kind=link}

Despite stronger relative growth in terms of earnings and revenues, as I will further discuss, Lloyds has experienced similar growth to that of TradingView's banking index, exemplifying how the firm has been unfairly punished by the market for headwinds in the broader national economy rather than intrinsic difficulties.

Comparable Companies

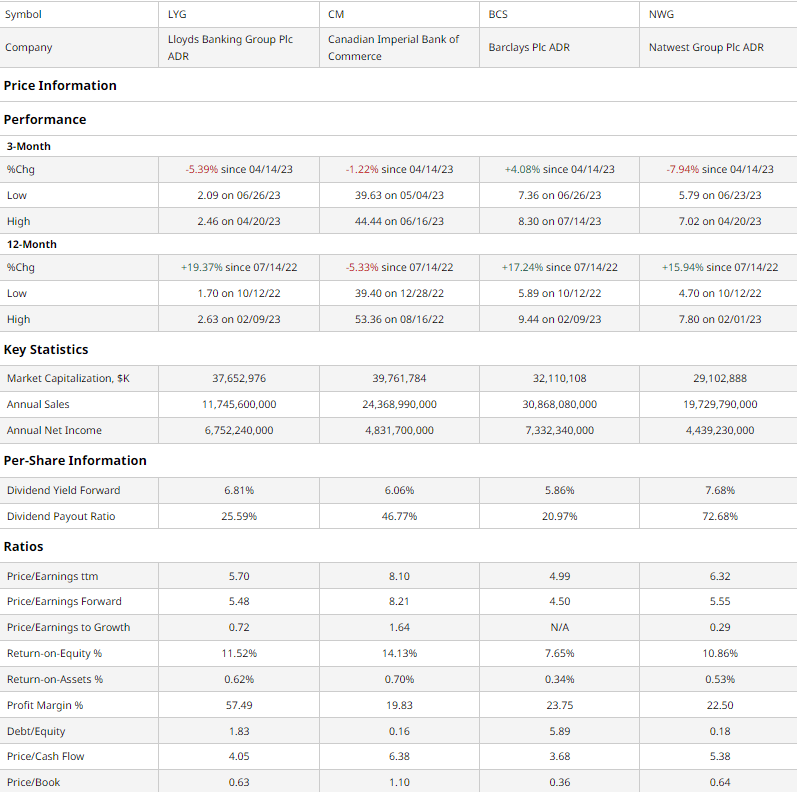

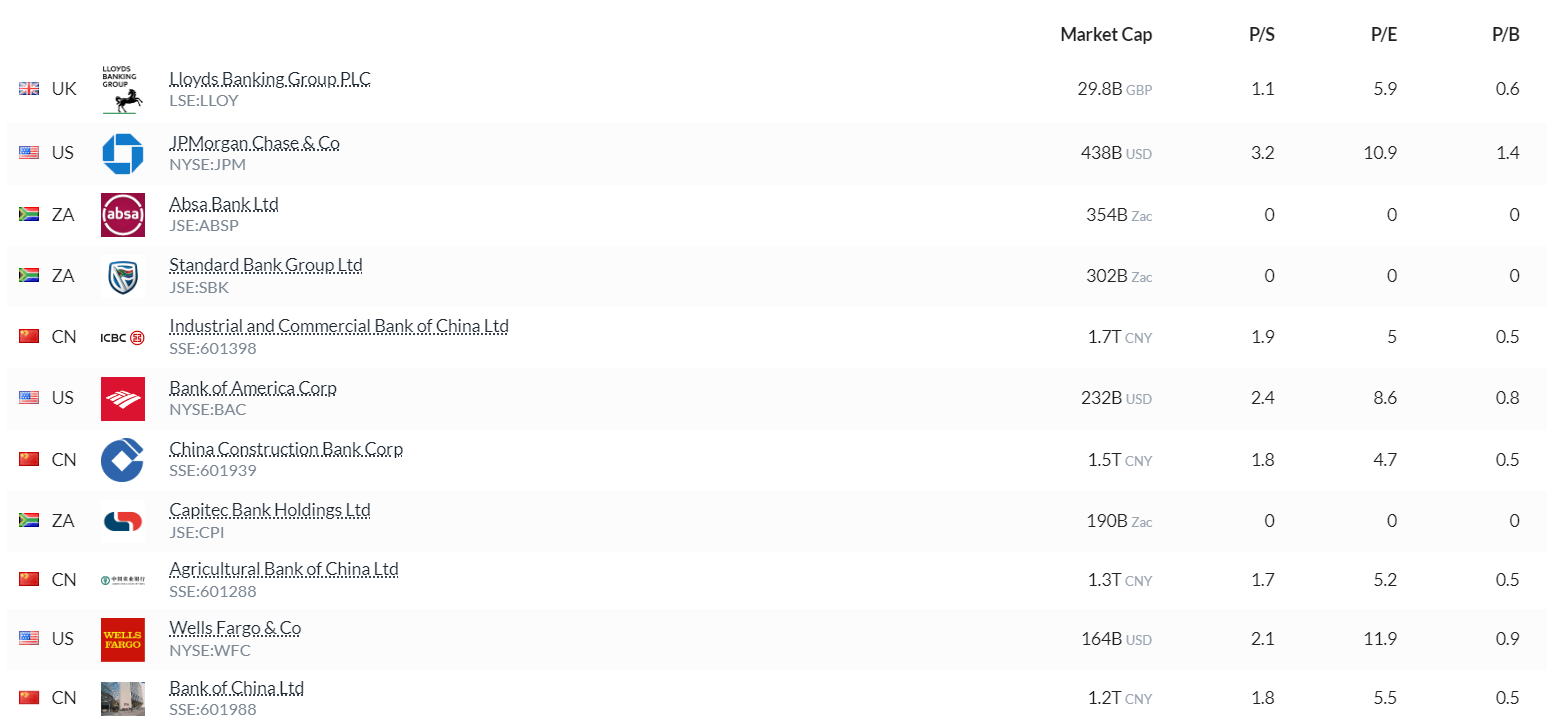

The British banking industry remains highly consolidated, with a small number of major financial institutions. Lloyds thus remains most comparable to these institutions, such as universal banking major, Barclays ( BCS ), and Edinburgh-based universal bank, the NatWest Group ( NWG ). And to provide a broader perspective, I also sought to compare Lloyds' financials to the Canadian Imperial Bank of Commerce ( CM ), which also operates across all major banking verticals and is similarly sized.

{kind=link}

As demonstrated above, Lloyds has experienced the second-worst quarterly price action, largely a reversion from Lloyds' peerless YoY stock rally. Despite this, Lloyds' strong multiples-based valuation, alongside the firm's growth capabilities, and shareholder returns necessitate a higher price.

For instance, Lloyds maintains the second-lowest trailing and forward P/E ratios, running alongside the second-lowest P/CF and P/B to demonstrate the firm's strength across all three financial statements.

Additionally, with the second-lowest PEG, ROE, and ROA, Lloyds demonstrates the capability to sustain its high, 6.81% dividend, which is paid out on the back of a 25.59% payout ratio.

All this comes at the price of a 1.83 debt/equity ratio, the second-worst of the group, though I believe Lloyds is more than capable of reducing that figure over the long run.

Valuation

According to my discounted cash flow analysis, at its base case, the true value of Lloyds should be $2.74, meaning, at its current price of $2.28, the stock is currently undervalued by ~16%.

My model, calculated over 5 years without perpetual growth, assumes a discount rate of 10%, incorporating the firm's high debt levels and average equity risk. Additionally, I calculated a revenue growth rate of 3%, lower than the smoothed-out 5Y average, and lower than the projected net-interest income CAGR of 5.21% in the UK retail and commercial banking industry.

{kind=link}

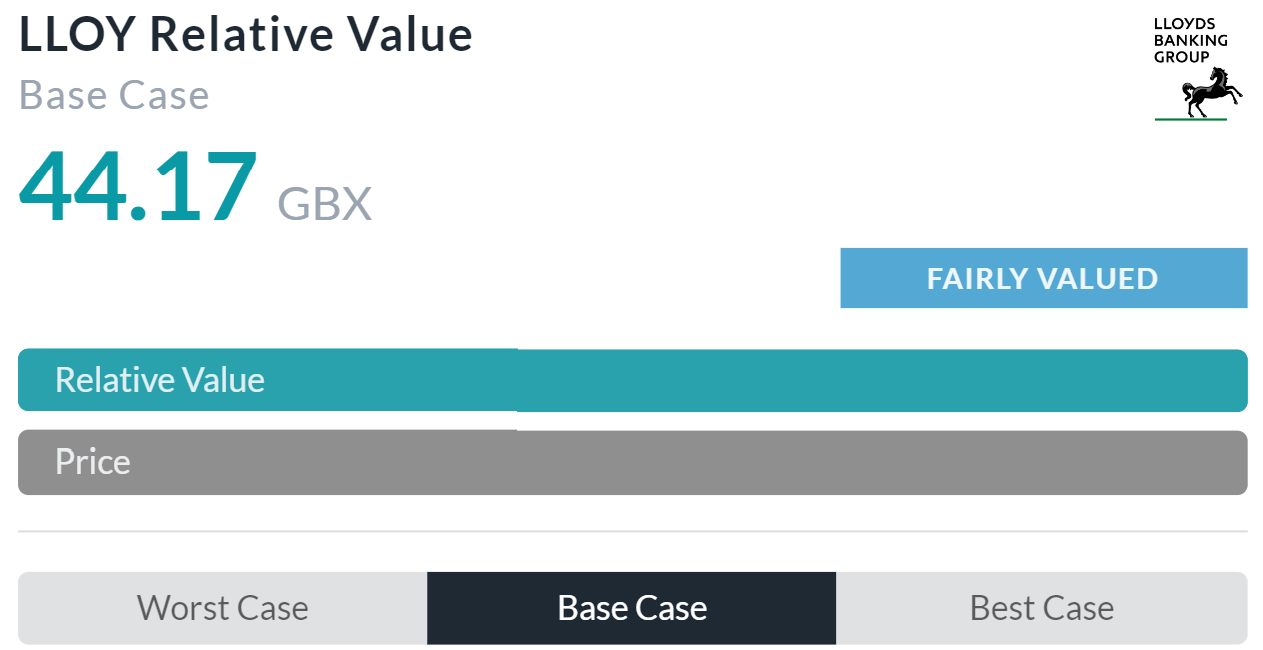

Alpha Spread's multiples-based relative valuation tool challenges my thesis on undervaluation, estimating that Lloyds currently trades at fair value.

However, Alpha Spread's failure to compare Lloyds with similarly sized companies with available data skews averages downwards, reducing the efficacy of the tool.

{kind=link}

As such, Lloyds' value is more accurately represented by my discounted cash flow.

Rates Drive Success in Retail, Increased Commercial Presence Supports Scale & Stability

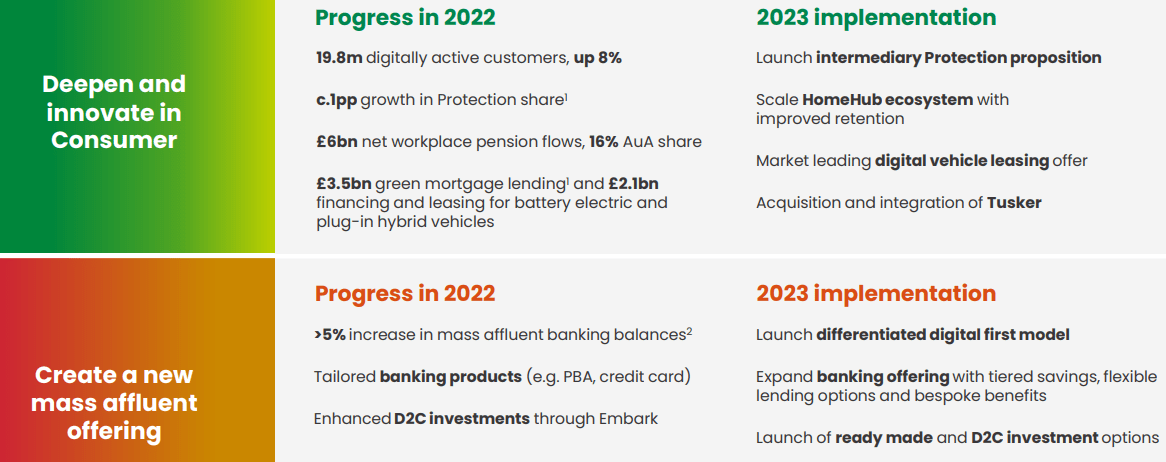

Lloyds' core business remains its retail offerings, which the firm aims to expand on a scale and margin basis. The bank aims to do this through combined investments in accessibility to retail consumers while increasing the firm's presence in the higher end of the banking mass market. On a more granular level, Lloyds seeks to broaden its digital footprint, offer increasingly specialized banking solutions, support direct-to-consumer investments, and offer a diverse range of financial solutions to a range of consumers.

{kind=link}

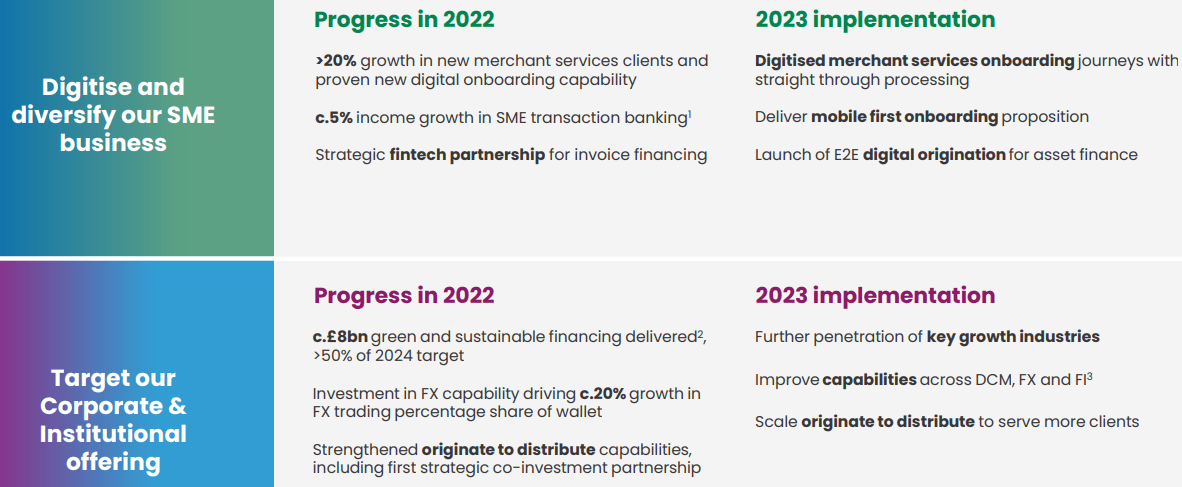

The firm's mass affluent offering is accompanied by diversification in Lloyds' commercial business, seeking an outsized expansion in commercial and corporate lines for cash flow diversity in addition to scale growth. Lloyds seeks to do so by digitizing the merchant onboarding process, the integration of origination capabilities, and scaled capacities across different asset classes such as fixed income and foreign exchange products.

{kind=link}

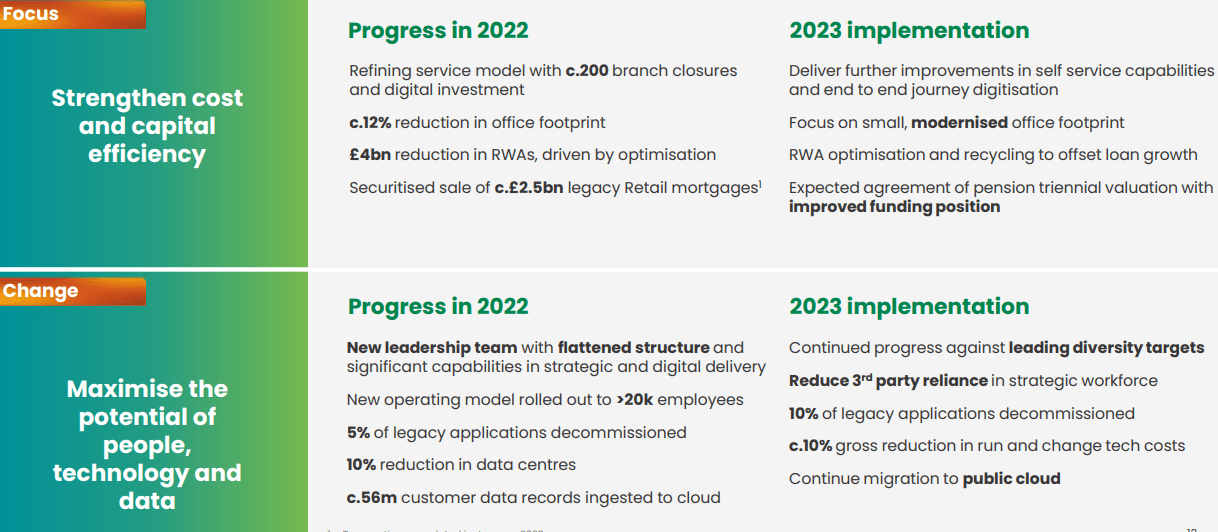

These strategies work in sync with Lloyds' financial and operational discipline strategy, with concentrations on reducing costs and deleveraging through reduced real estate footprint, labour efficiency through digitalization, and tech cost reductions, among other objectives.

{kind=link}

Wall Street Consensus

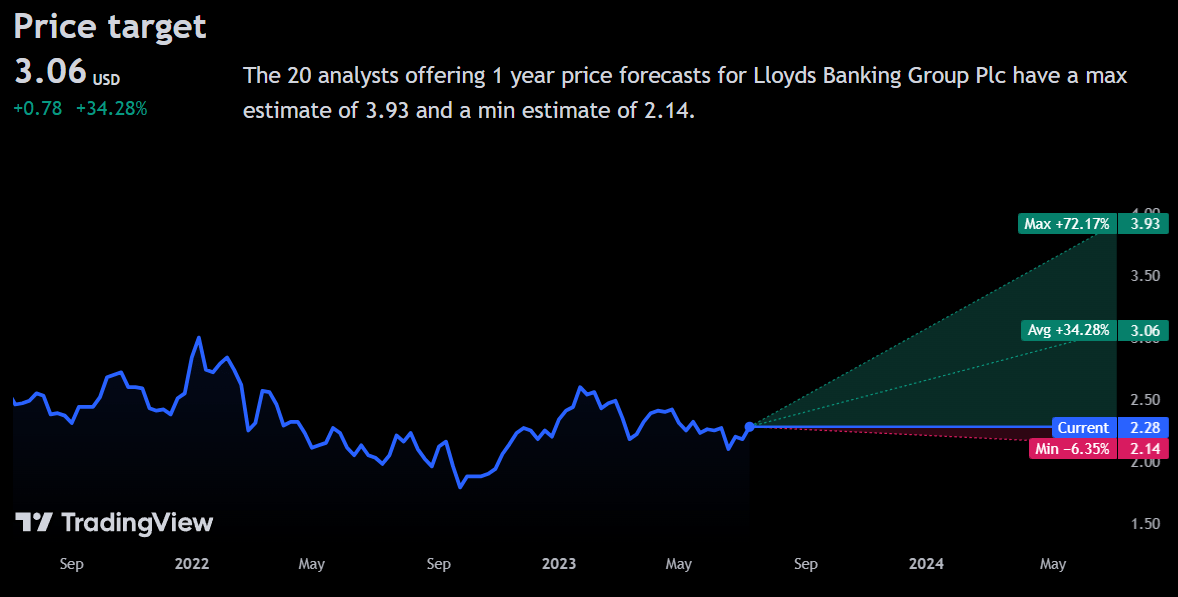

Analysts largely support my positive view of the stock, estimating an average 1Y price target of $3.06, a 34.28% increase.

{kind=link}

Even at the minimum projected 1Y price target of $2.14, a 6.35% decline, investors can expect to preserve their wealth when accounting for Lloyds' dividend.

As such, analysts echo my opinion that Lloyds is fundamentally undervalued and remains operationally superior to peers.

Risks & Challenges

Continued Macro Risk in the UK May Diminish Loan Demand

Contrary to other Western markets, which are seeing a reduction in core inflation levels and have thus been able to reduce the rate of interest rate growth, the UK has seen higher levels of sustained inflation and may see stickier interest rates. Although this may support the company's net interest income in the short and medium runs, sustained levels of inflation and high interest rates may lead to reduced demand for credit products, diminishing Lloyds' scale growth potential.

Lloyds Remains Highly Leveraged, Reducing Growth Prospects

A common theme among major British banks remains a high degree of leverage; that rings true for Lloyds as much as any other. Lloyds' high debt levels, combined with rising interest rates, may harm the firm's cost structure, reducing profitability and the ability to reinvest in its ambitious growth capabilities. Although Lloyds has developed a multitude of capital efficiency programs to focus capital on deleveraging, failure to adequately reduce debt levels may reduce long-run cash flows.

Conclusion

Looking forward, Lloyds remains discounted relative to its financial position, a value proposition only enhanced by the firm's lean operational strategy, mass affluent offering, and growth across commercial and corporate banking.

For further details see:

Lloyds Banking: Sticky Interest Rates Support Recovery, Though Risks Remain