LYG - Lloyds: Still 10x P/E And 4%+ Dividend Yield After Recent Rally

Summary

- Lloyds shares have risen 17% since we reinitiated coverage in July, but still have a P/E of about 10x and a Dividend Yield of 4.3%.

- Net Interest Income has already benefited much from higher rates, and we expect further benefits as well as more rate hikes.

- Credit losses remains the biggest risk, but Lloyds’ loan book is relatively high-quality and losses should be manageable in size.

- We expect further dividend increases and more buybacks in 2023, as Lloyds' capital ratio is 1.5 ppt higher than its target.

- With stock at 49.24p, we expect an exit price of 58p and a total return of 32% (10.5% annualized) by 2025 year-end. Buy.

Introduction

We review our Lloyds Banking Group plc ( LYG ) case after shares have gained 18% (in U.K. pounds, including dividends) since we reinitiated our coverage in July:

| Lloyds Share Price (Last 1 Year) Source: Google Finance (20-Jan-23). |

Lloyds still looks attractive on relatively low expectations. Return on Tangible Equity (“ROTE”) is expected to be around 13% in 2022, and we now believe it can be at 10% for the next few years. Net Interest Income has benefited significantly from higher interest rates, and more should follow when the “structural hedge” continues to be redeployed over time. Other Income is stable and Operating costs are growing as planned. Macro-driven credit losses in the U.K. remains the biggest risk, but Lloyds’ loan book is relatively high-quality and losses should be manageable in size. The U.K tax rate now appears stable with an increase of just 1 ppt from April 2023. CET1 ratio is 1.5 ppt higher than targeted, so further dividend increases and buybacks are likely. The current Dividend Yield is 4.3% and, assuming a long-term 10% ROTE, the P/E multiple is 10x. We expect an exit price of 58p and a total return of 32% (10.5% annualized) by 2025 year-end. Buy.

Lloyds is scheduled to release its full-year 2022 results on February 22.

Lloyds Banking Group Buy Case

Lloyds is the #1 retail bank in the U.K., largely focused on the domestic market, and offer a wide range of products and services to consumers, SMEs as well as corporates and institutions.

Retail Banking contributes nearly two-thirds of Lloyds’ income and profits, while Commercial Banking and Insurance & Wealth were the other segments. Net Interest Income (“NII”) represented more than two thirds of income in 2021, and 63% of the’ loan book consists of personal mortgages:

| Lloyds Key Financials by Segment (2021) Source: Lloyds results release (2021). NB. Retail Banking and Commercial Banking will each be split into two units in 2022. |

NII is the most important part of our investment case. The core of Lloyds’ business is its large low-cost deposit base, where customers often accept lower rates because of Lloyds’ brand name and their own inertia, and where and unit costs are kept low by economies of scale. Lloyds generates NII from its deposit base through both lending and a “structural hedge” that functions similarly to a portfolio of fixed-rate bonds. In years past Lloyds’ NII was under pressure because a low-rate environment led to more competition and reduced its Net Interest Margin (“NIM”). However, the Bank of England has started raising U.K. interest rates in December 2021 and Lloyds’ NIM has benefited significantly.

Credit losses are the main risk in our investment case, but we expect Lloyds’ credit losses should be limited even in the event of a U.K. recession, because its lending products have traditionally been targeted at the prime+ part of the market and its mortgage portfolio has conservative Loan-To-Value ratios (averaging 42.1% for the entire portfolio and 63.3% for new business as of 2021 year-end). Lloyds’ Impairment in the pandemic year of 2020 was £4.25bn, or just 0.6x of its Profit Before Impairment that year. In the event of a prolonged economic downturn, we still expect Lloyds to have one bad year but then return to a solid ROTE in subsequent years.

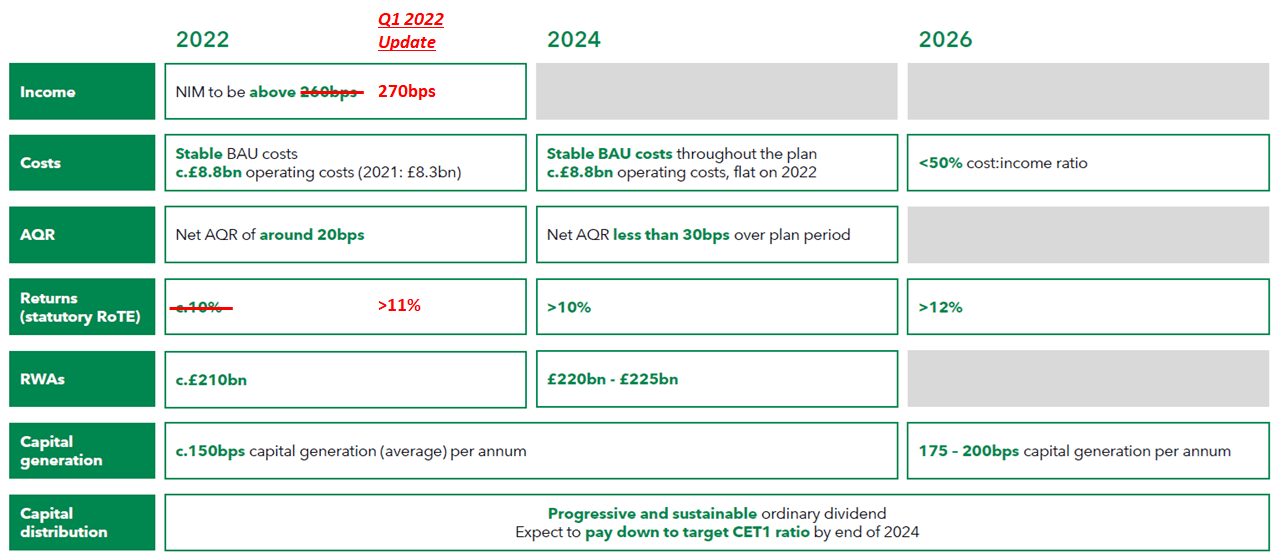

Since February 2022, Lloyds has been implementing a new strategy under new CEO Charlie Nunn (who took up the role in August 2021). Key pillars of this strategy include deepening existing consumer relationships, diversify the SME business and selectively expanding Corporate & Institutional offerings. Operating costs were expected to increase from £8.3bn in 2021 to £8.8bn from £2022 onwards, but with the Cost/Income Ratio returning to less than 50% by 2026. The result of the plan was expected to be a ROTE of more than 10% from 2024 and more than 12% from 2026:

| Lloyds Medium-Term Targets (2022-26) Source: Lloyds results presentation (Q4 2021); annotations by Librarian Capital. |

{kind=link}

(2022 ROTE was initially expected to be “around 10%”, but was already revised to more than 11% at Q1 results in April).

We are cautious about the new strategy, as they mostly seem to involve merely doing the same things as before but better (with the exception of the new investment offering), and also sceptical about the new management team’s apparent lack of a track record in operational excellence. In our base we assumed a ROTCE of only 8.5%.

Lloyds has had strong quarterly results since our last update, helped by rate hikes, and we now believe medium-term ROTE is likely to be 10%, though it can be temporarily lower if credit losses become elevated in a U.K. recession.

Lloyds 2022 ROTE Now Expected to Be 13%

Management raised its guidance for 2022 ROTE to “around 13%” at H1 results in July. The latest 2022 guidance, released with Q3 results in October, are as follows:

| Lloyds 2022 Outlook Source: Lloyds results presentation (Q3 2022). |

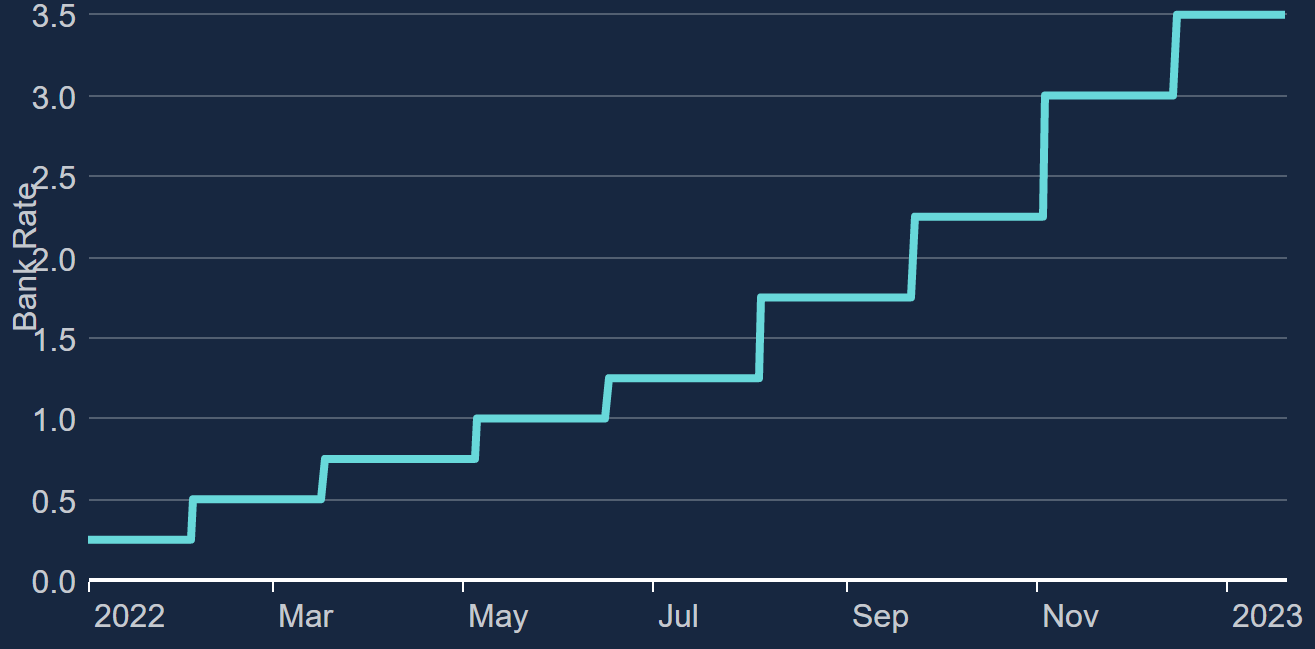

The main driver of the higher guidance is a higher NIM, which was expected to be “above 260 bps” as of July but is expected to be “more than 290 bps” as of October. The Bank of England has continued to raise its base rate , from 1% at the end of June 2022 to 2.25% by October and 3.50% now:

{kind=link}

The higher NIM has more than offset slightly higher credit costs (represented by the Asset Quality Ratio, or “AQR”), and will likely make it easier for Lloyds to achieve its target ROTE in 2023 and 2024 (all else being equal). Sell-side analysts have asked about raising 2023 and 2024 targets and management, while stating that it is too early to update these targets, seem to agree that this is a possibility:

“We put forward a 2024 ROTE of greater than 10%. There have been, as you know, significant developments across the market since then ... Many of those trends that we've seen in terms of market rates and Bank (of England) base rate changes lead to sustained improvements in the context of Net Interest Income in the context of Net Interest Margin, both this year and beyond.”

William Chalmers, Lloyds CFO ( H1 2022 earnings call )

Movements in the cashflow hedge reserve following rate increases have also resulted in a smaller Net Asset Value (without affecting actual earnings), reducing the denominator in ROTE calculations and raising the ROTE.

We now believe ROTE can be at 10% for the next few years, unless credit losses become elevated in a U.K. recession. We believe recent operating results support this view.

Lloyds’ Quarterly Results Trending Up

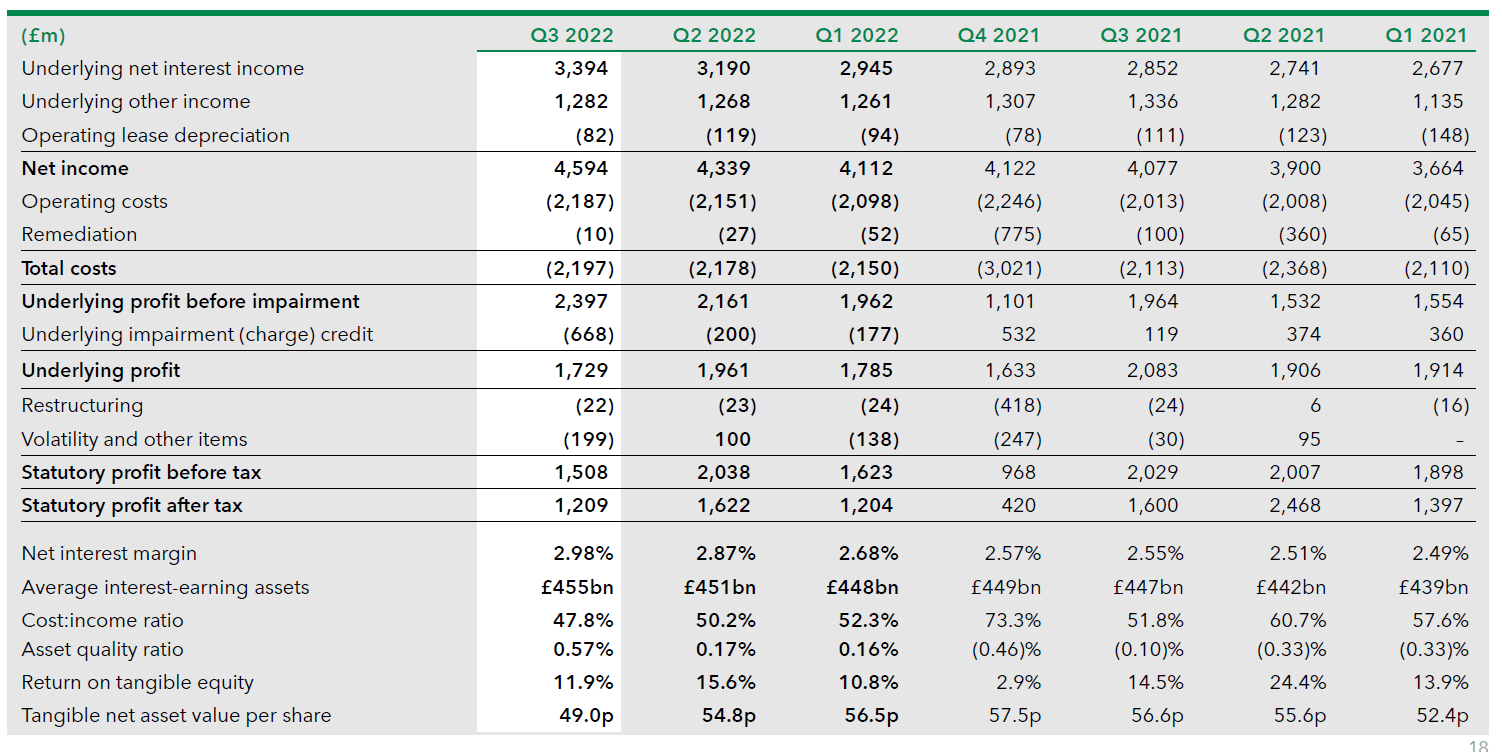

Lloyds’ operational performance has been trending up in recent quarters, as shown in the table below:

{kind=link}

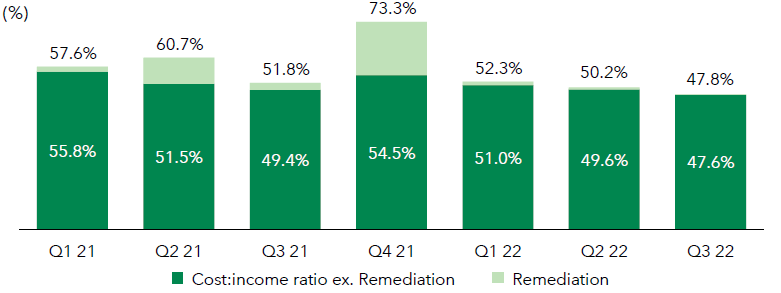

Underlying Profit Before Impairment has increased sequentially each quarter in 2022. This stood at £2.40bn at Q3 2022, compared to £2.16bn in Q2 and £1.96bn in the prior-year quarter. This is a key measure because it reflects a bank’s earnings power before credit volatile provisions. The trend is even clearer if we exclude Remediation Costs associated with regulatory penalties or settlements, which can also be volatile.

Net Interest Income has been the main driver of this sequential growth in profits, rising consistently from £2.68bn at Q1 2021 to £3.39bn by Q3 2022. As shown in the table, this is mainly driven by a similarly consistent increase in the NIM from 2.49% in Q1 2021 to 2.98% by Q3 2022, though Average Interest-Earning Assets also rose slightly (3.6%) in this period, on a consistent trajectory except for the seasonal post-holiday dip in Q1 2022.

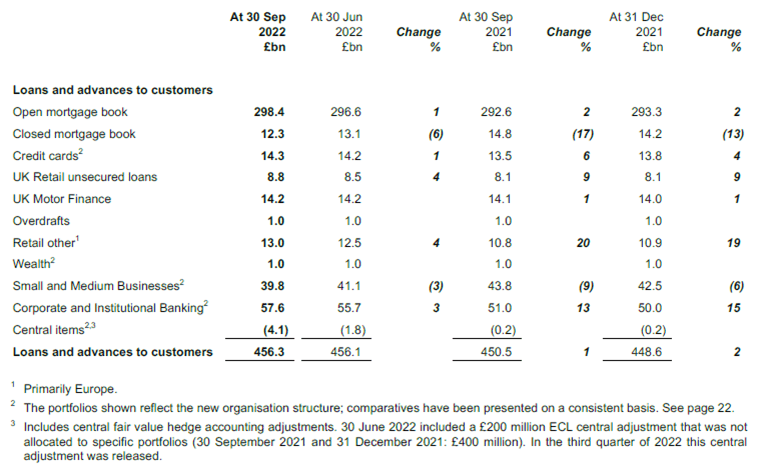

Lloyds’ loan growth during 2022 was partly offset by the repayment of government-guaranteed COVID support loans among Small and Medium Businesses. Except this and the Closed Mortgage Book, loan growth has been positive in most categories, with larger percentage increases in targeted areas like Corporate and Institutional Banking:

| Lloyds Loans & Advances to Customers (Q3 2022 vs. Prior Periods) Source: Lloyds results release (Q3 2022). |

{kind=link}

Other Income has been broadly stable at around £1.3bn each quarter.

Operating Costs has been rising due to planned investments, while “Business As Usual” costs remain “essentially stable”. The Cost/Income Ratio has been volatile due to Remediation Costs, but has been improving excluding Remediation Costs largely due to rising revenues:

{kind=link}

Asset Quality Ratio follows the same trajectory at other banks, with negative AQRs representing the release of COVID-19 reserves in 2021, but positive AQRs representing credit costs returning to normal in 2022. AQR spiked to 0.57% in Q3 2022, primarily due to a downward revision in macroeconomic outlook, with the latter responsible for £618m in impairments (offset by a £200m release of COVID-related reserves) compared to a total net impairment of £668m.

Return to Tangible Equity was consistently above 10% each quarter in 2022, and was 12.9% for Q1-3 overall (but with a benefit of about 1 ppt from movements in the cashflow hedge reserve as described above).

Higher Rates Driving Net Interest Income

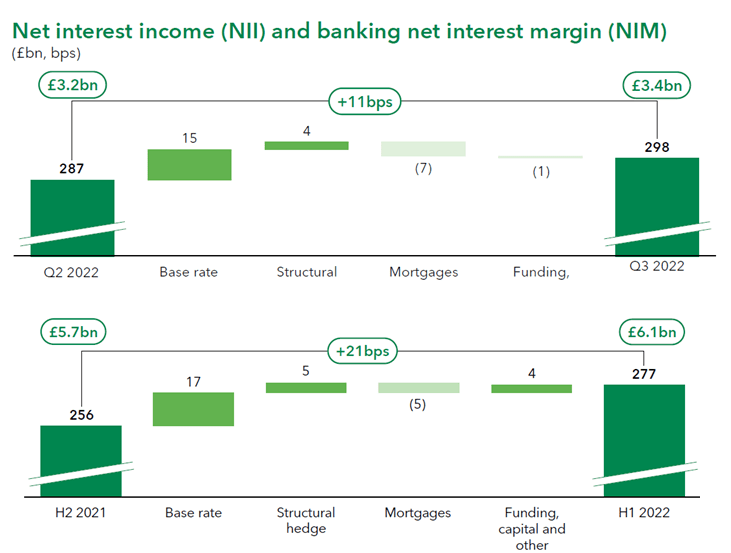

Lloyds has benefited significantly from the rise in the Bank of England base rate, by far the biggest component in the increase of its NIM since 2021, as shown in the charts below:

| Lloyds Net Interest Margin Bridge (H2 2021 to Q3 2022) Source: Lloyds results presentation (Q3 2022). |

{kind=link}

Lloyds expects to pass on only 50% of the benefit of rate hikes to deposit customers, and so far in 2022 they have actually passed “a little below” this as of Q3 2022 results. We believe they will have to pass on more over time. Each 10 ppt in the deposit pass-through rate is worth £50m to the NII and 1 bps in the NIM in year 1.

The rise in the base rate has more than offset margin headwinds from competition.

The competition on mortgages continues to be a significant negative for Lloyds’ NIM as shown above, with the margin on new mortgages still lower than that on existing mortgages that gradually mature or are refinanced. Completion margin on new mortgages was as low as 60 bps in both Q2 and Q3 of 2022, compared to 190 bps in Q4 2020 and 115 bps in Q4 2021. (Back book margin was stated as 150 bps in Q4 2021.) We do not expect this to improve much (though at worst it will probably stabilize), especially as Lloyds is now growing its mortgage book again.

The “structural hedge” has been a tailwind to NIM and NII as each maturing portion is replaced with one of higher rates. It has risen to £250bn in size as of Q3 2022 and has a rate of “a shade over 1%”. The average maturity is 3.5 years and management expects to redeploy much of it “into more like a 4-4.5% environment” “in the next year or so”. The “structural hedge” already generated £2.2bn (14% of group income) in 2021 and will likely generate much more in the future.

| Lloyds Structural Hedge (Since 2017) Source: Lloyds results releases. |

We expect NII growth to remain healthy in the medium term, with further rate hikes in 2023, and then a stable or slightly down NIM thereafter as the benefits from the “structural hedge” helps offset headwinds in mortgages.

Credit Losses Likely To Be Limited

Macro-driven credit losses in the U.K. remains the biggest risk, but Lloyds’ loan book is relatively high quality.

Qualitatively, Lloyds has a declared focus on higher-quality borrowers in the “prime+” segment of the market.

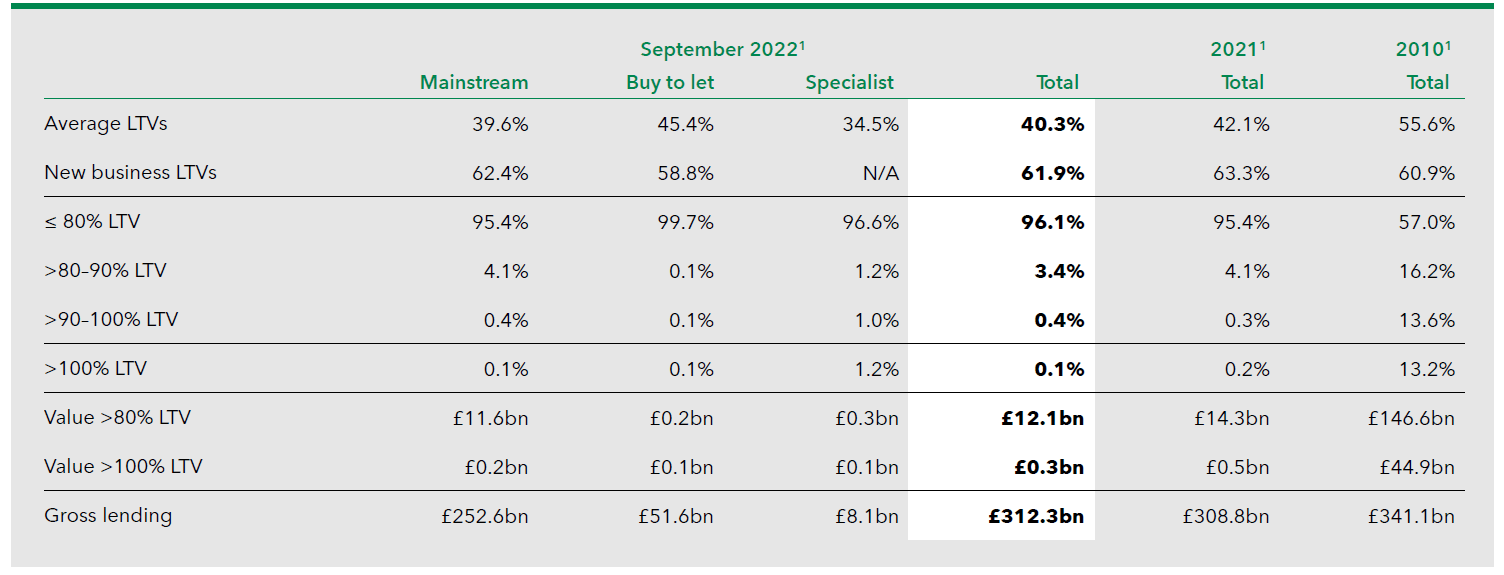

Quantitatively, Lloyds has continued to maintain high Loan-To-Value ratios on its loans, for example with 97% of its personal mortgages being on LTV of less than 90%:

| Lloyds Personal Mortgages Loan-to-Value Ratios (Q3 2022) Source: Lloyds results presentation (Q3 2022). |

{kind=link}

Management also described its Commercial Real Estate exposure as having been “significantly de-risked”, with net exposure down to £10.9bn and an average LTV of 39%.

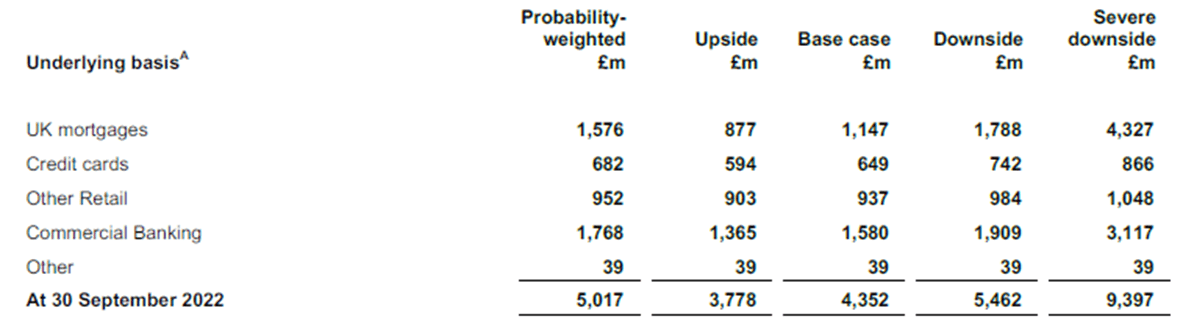

As of September 2022, Lloyds has an Estimated Credit Loss (“ECL”) Allowance of £5.02bn, or 1.1% of its Loans & Advances to Customers. A “Severe Downside” scenario, which includes U.K. unemployment rising to 9.8% in 2023, peaking at 10.5% and remaining at 9.5% even in 2026, carries an ECL of £9.40bn:

| Lloyds ECL Allowance By Scenario (Q3 2022) Source: Lloyds results release (Q3 2022). NB. All figures in millions. |

{kind=link}

The £4.38bn difference between the current ECL Allowance and the “Severe Downside” ECL is, by definition, management’s estimate of further credit losses in a worst-case scenario. It can likely be easily absorbed by Lloyds’ Underlying Profit Before Impairment, which totalled £7.62bn in the last 4 quarters, in a single year.

Visibility on Limited U.K. Tax Hike

The U.K tax rate now appears stable, with an increase of just 1 ppt from April 2023.

Since taking up his role in October, U.K. finance minister Jeremy Hunt has now confirmed limited tax rate changes for banks from April 2023, with a net increase of 1 ppt from two changes offsetting each other:

We do not expect any major changes on the tax rate. The current Conservative-led U.K. government does not have to hold new elections until January 2025. While the Conservatives are significantly behind in opinion polls, the Labour opposition has pledged not to increase the Banking Surcharge or introduce windfall taxes on U.K. banks.

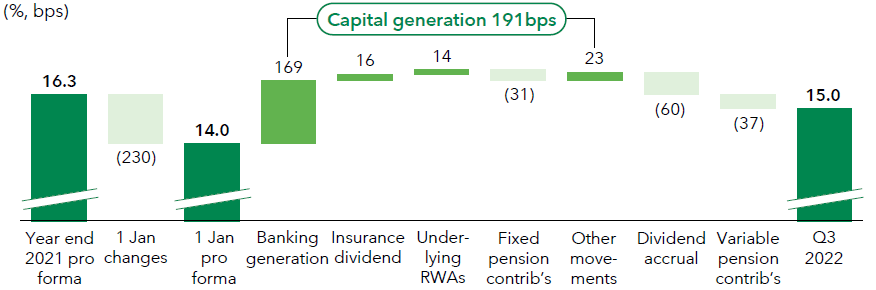

Further Dividend Increases & Buybacks

Lloyds’ CET1 ratio was at 15.0% in September, 1.5 ppt higher than the 13.5% targeted (12.5% minimum plus 1% buffer). (Management has kept CET1 at 14.0% at the start of 2022 because of macroeconomic uncertainties.)

{kind=link}

The surplus capital means that we believe further dividend increases and buybacks are likely in 2023. Decisions on the dividend and buybacks tend to be taken after each year-end, then announced with full-year results in February.

The interim dividend was already raised by 20%. Lloyds has a “progressive and sustainable” dividend policy, which means dividends should grow over time but remain a fraction of what management views as sustainable EPS.

A £2bn share buyback program was announced in February 2022 and completed in October, repurchasing more than 6% of outstanding shares. Management comments indicate a new program is likely.

However, not all of the earnings can be distributed to shareholders, as an agreement with Lloyds’ pension scheme in February 2021 requires the bank to contribute annually to the pension scheme a sum of £800m plus 30% of in-year shareholder distributions (dividends and buybacks) until the pension deficit is closed (in 2025 in our estimates).

Lloyds Dividend Yield & Valuation

At 49.24p, Lloyds shares are trading at:

- 1.0x P/TBV, relative to Q3 2022 TBV of 49.0p per share

- 10x P/E, relative to our assumption of a medium-term ROTE of 10%

- 4.3% Dividend Yield, relative to last-twelve-month total dividend of 2.13p

Share buybacks have been a regular part of Lloyds’ capital allocation, with £2.0bn of buybacks (equivalent to 6.8% of the current market capitalization) announced in February and expected to be completed by the end of 2022.

Lloyds Return Forecasts

We increase our ROTE forecasts but keep most other assumptions unchanged:

- ROTE to be 13% in 2022 (was 11.0%) and 10% thereafter (was 8.5%)

- A 10% reduction in 2022 NAV related to the cashflow hedge reserve (new assumption)

- Dividends, buybacks and pension contributions to be 94.5% of Net Income (unchanged)

- Dividend to grow 15% in 2022 and then 5.0% annually (was 2% in all years)

- Pension contributions to be £800m plus 30% of dividends and buybacks (unchanged)

- Buybacks to be conducted at 1.2x P/TBV (was 0.8x)

- P/E to be 10x at 2025 year-end (unchanged)

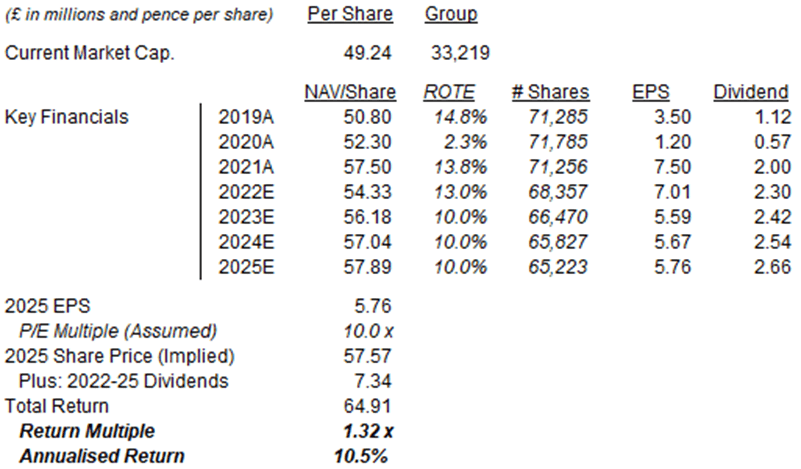

Our new 2025 EPS forecast of 5.76p is 1% higher than before (5.68p), with the higher ROTE assumption being mostly offset by the lower NAV and more expensive buybacks:

{kind=link}

With stock at 49.24p, we expect an exit price of 58p and a total return of 32% (10.5% annualized) by 2025 year-end.

Is Lloyds Stock A Buy? Conclusion

Lloyds still looks attractive on relatively low expectations.

We reiterate our Buy rating on Lloyds Banking Group.

For further details see:

Lloyds: Still 10x P/E And 4%+ Dividend Yield After Recent Rally