SNES - Long Cast Advisers Q3 2023 Letter

2023-11-11 01:30:00 ET

Summary

- Long Cast Advisers, LLC, is an independent-registered investment adviser investing on behalf of individuals, family offices and endowments. It is concentrated on long-term investing, focused on small-cap companies.

- Long Cast Advisors achieved cumulative net returns of 8% for the 3Q23 quarter and 20% year-to-date.

- The portfolio saw strong performance from certain stocks, while others detracted from returns. The firm added to certain holdings and exited others to optimize tax purposes.

- The article discusses three smaller holdings in detail, highlighting their unique attributes and growth potential.

Dear Friends and Clients:

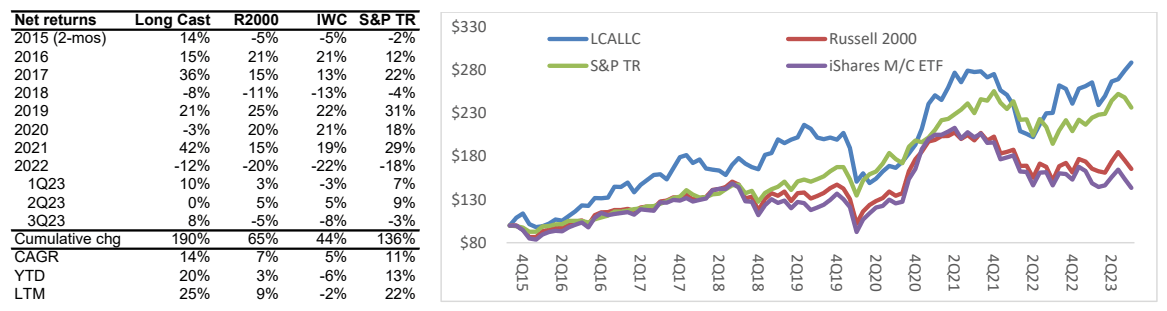

Welcome and thank you for reading. For the 3Q23 quarter (ended September 30, 2023), cumulative net returns were 8%. YTD returns through quarter end were 20%. Since inception in November 2015 through quarter end 3Q23, LCA has returned a cumulative 190% net of fees, or 14% CAGR. As a backdrop to returns, since inception through 3Q23 we comfortably exceed two widely used representative indices for passive small company investing, the iShares Micro-Cap ETF ( IWC ) and Russell 2000 Index ( RTY ), and at present, the S&P.

Past performance is no guarantee of future results. Individual account returns may vary .

{kind=link}

Long Cast continues to attract clients aligned with its long term, small company centric and research- intensive focus. I welcome the continued interest from individuals and institutions as I patiently grow the business, and have capacity to add more accounts.

PORTFOLIO UPDATE

MTRX was the top performer in the quarter, followed by MAMA , QHRC and RSSS . Detractors were CCRD , RELL , DAIO and PDEX . During the quarter we added to MTRX and substantially exited smaller holdings in AIM , SNES and SANW to “harvest” their losses for tax purposes, leaving us with a more concentrated portfolio, with fewer stocks and more cash. My goal is to keep our losses small and our gains large, and in these cases at least, I did. Given geopolitical tensions, I’m leaning towards holding more cash than usual while continuing to scour for new ideas. When it comes to investing, I try to never be in a rush.

Our 2Q letter included a brief write up around our top five-positions. Very little has changed substantively around our thesis for owning these, so I thought I would add a little bit of detail on three of our smaller holdings. If I could point to similarities to all three companies, I would say, they are all small, customer centric, trying new things, and run by smart humble managers who are iterating towards better solutions. I consider them “high IQ” companies, a concept I’ll touch in the end of this letter.

PDEX is a small contract manufacturer in the medical device space. The core product is a battery powered handheld driver used by surgeons to screw implants or plates into bone (think knees, spines, facial reconstruction, et al) with a precise amount of torque to avoid stripping. The company has its own engineering team to develop its own products and works with branded device manufacturers to develop theirs (I believe Stryker is the largest single client).

I don’t normally think of contract manufacturing as a wonderful industry but there are few aspects about this company that make it an unusual, compelling and attractive long-term investment. I elaborate on three of these attributes below.

The Board: Chairman Nick Swenson and Board member Ray Cabillot together own about 40% of the company. They are thoughtful investors who run their own hedge funds (AO Partners and Farnam Street Partners, respectively) and they manage the capital allocation strategy at PDEX. The evidence observed in the growth in book value per share, which I believe have their “fingerprints” suggests a focus on value creation.

New manufacturing facility: The company doubled the size of its manufacturing space by acquiring a new facility four miles from the existing headquarters in Irvine, CA. The build out and validation of the space took much longer than expected, partially impacted by COVID, and partially because this is a tiny company that doesn’t have a lot of experience doubling the size of its manufacturing space. The expansion is now complete. Obviously, the space doesn’t promise additional revenues but it doubles the size of the opportunity.

Backlog: Along with doubling the size of its manufacturing footprint, the company doubled the size of its backlog to $41M through a large order from a leading customer. The inference is that FY24 could be a high growth year.

SOTK is another company expanding its footprint and backlog. I last wrote about this in 4Q21. The Milton, NY based company historically made specialty nozzles for depositing specific and measured amounts of liquified materials. Over the last decade it has transitioned from just manufacturing nozzles for OEM’s to now designing, manufacturing and selling the units themselves. Two of their recent innovations are a roll to roll continuous system for fabric coating and a continuous glass coating system that is more precise and efficient than existing solutions on the market.

The company owns the industrial park from which it operates and over the last few years as tenant leases have lapsed, it has taken over more of its space for manufacturing. With year-end backlog at record highs, additional capacity and easy comparisons, significant growth in ’24 seems likely.

A near term opportunity, towards which there is some visibility, is customers going “from the lab to the production” i.e. they used SOTK equipment “in the lab” and now need larger higher priced units to produce at scale. I believe one can observe an example of this in process. Here’s a video from a start- up using SOTK equipment in the lab (the logo is covered in tape) and here’s a photo from an article about that company in Fast Company with a larger piece of SOTK equipment in the background (their equipment sprays on the materials to form a catalyst that looks like a large bike tire repair patch).

The long term opportunity, which in my view could yield multiples greater return, could occur if SOTK’s spray deposition can replace some portion for the large market for higher cost batch process vacuum deposition. I believe that the company is pursuing R&D and / or license deals pursing this opportunity. In the meantime, without regard for any unknowable future, you have a profitable company funding its own growth, operating with a healthy balance sheet and patiently developing solutions around a core skillset. These are the kinds of things that favorably tilt the odds towards long term value creation.

Finally, on RSSS , which I recently wrote about in the 4Q22 letter, it is worth a short update here, to share a video of my interview with its CEO at September’s Microcap Leadership Summit.

IN CONCLUSION: ON “CORPORATE IQ”

The various geo-political tensions put my head in a dark place. War is wasteful and driven by passion and ideology. It stifles growth and the effects are tragic. I gave up my belief in God after reading “Thinking Fast and Slow” (a “System 2” solution to a “System 1” problem) and threw my lot in with Humanity (talk about a Job-ian experience) so I have hope and faith that we can do better, despite all so much evidence to the contrary. Isn’t that what faith and belief are all about?

Fortunately, our invested capital is less impacted by the news than my spirit. It is however affected by the downdraft impacting the small cap markets, to which I pin rising rates as the ultimate culprit. Credit drives everything and since smaller companies tend to have more vulnerabilities than larger companies – they are less diversified, more reliant on fewer customers and limited financing options - they get discounted earlier in a cycle. When rates peak, they should do better sooner. In short, I think it is an opportune time to source new ideas.

As I consider what I’m looking for in an investment, I’m drawn to a vague notion of “corporate IQ”. The thought came about when I observed a “high IQ” manager who was a terrible CEO replaced by an “average Joe” who I think is a terrific CEO. I’m sure everyone can point to examples that demonstrate how intelligence and management are very different skillsets.

The attributes that define corporate IQ are varied and I’m sure it’s not worth my time to try to nail down every single one. It’s not about intelligence of the management but whether or not the company presents in a way that’s aligned with the problem they aim to solve for their customer. Companies that I consider “high IQ” are run by managers who tend over time to learn from their mistakes (we all make them) and apply an iterative and incremental process to improvement. They take the long view. They are open and responsive to criticism. They don’t operate for the satisfaction of their own or their CEO’s ego but for the purpose of solving a problem for customers at a margin that generates returns for shareholders. They practice humility. I do try to run my own business along these principles as well.

Whatever corporate traits one might consider “high IQ”, the other aspect worth realizing – and in my mind, the more important one - is that in the process of norm scoring, you will find that half the companies in a population will be below average on that score. Keeping this in mind is way of setting a base rate. As a long-term investor, if I can simply eliminate the likelihood that I’m investing in a below average IQ company, then I’ve made my job a bit easier.

I remain committed to building a durable and sustainable business based on a repeatable investment process and intelligent capital allocation. I appreciate your entrusting me with your capital and the responsibility associated with being its steward. If you have any comments or questions, please don’t hesitate to call.

Sincerely

Avi

Editor's Note: The summary bullets for this article were chosen by Seeking Alpha editors.

For further details see:

Long Cast Advisers Q3 2023 Letter