VMEO - Longleaf Partners Small-Cap Fund Q2 2023 Commentary

2023-07-20 01:31:00 ET

Summary

- Longleaf Partners Funds is a suite of mutual funds and UCITS funds that Southeastern Asset Management, the investment advisor to the Longleaf Partners Funds, created in 1987 as a way for Southeastern employees to invest alongside their clients.

- Longleaf Partners Small-Cap Fund added 3.70% in the second quarter, taking year-to-date returns to 8.10% for the first half.

- In the second quarter, we initiated three new positions, added to Boston Beer Company, a new purchase in the first quarter, sold Vimeo and LANXESS, converted our Lumen equity position to a smaller position in Lumen bonds, and trimmed several strong performers.

{kind=link}

| Returns reflect reinvested capital gains and dividends but not the deduction of taxes an investor would pay on distributions or share redemptions. Performance data quoted represents past performance. Past performance does not guarantee future results. The investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance of the fund may be lower or higher than the performance quoted. Performance data current to the most recent month end may be obtained by visiting southeasternasset.com. The prospectus expense ratio before waivers is 1.01%. The expense ratio is subject to a contractual fee waiver to the extent the Fund’s normal operating expenses (excluding interest, taxes, brokerage commissions, and extraordinary expenses) exceed 0.95% of average net assets per year. This agreement is in effect through at least April 30, 2024, and may not be terminated before that date without Board approval. |

Longleaf Partners Small-Cap Fund (LLSCX) added 3.70% in the second quarter, taking year-to-date ((YTD)) returns to 8.10% for the first half. While the portfolio’s lack of exposure to Health Care and relative overweight to Consumer Staples weighed on relative results in the quarter, the Fund’s differentiated holdings within the Financials and Real Estate sectors contributed to absolute and relative returns in the quarter and for the first half. We have built a unique, diversified, and relatively defensive portfolio in the Fund. We own a collection of stable businesses with strong brands that are by and large out of the economic crosshairs - tortillas, beverages, insurance, sports - with great management partners in place that navigate even the most challenging markets. We believe this differentiated positioning will be a source of future outperformance.

The Russell 2000 has been one of the relatively weaker markets in 2023, as investors have fled what they view to be more volatile, cyclical companies in favor of increasingly mega-cap growth companies. These stocks dominated markets over the last decade but suffered an initial collapse of over 30% from January 2022 to the Nasdaq’s recent low point in October 2022, before rallying over 40% in the last six months. The market rarely moves down (or up) in a straight line, as we have learned through multiple previous cycles. This reminds us of the early stages of the dot-com bubble, when the Nasdaq fell over 35% from March 2000 highs before temporarily rebounding 36% in 2Q 2000, only to drop a further 80% over the subsequent 25 months, as shown in the charts below.

{kind=link}

While every period is different, we believe the mega-cap tech darlings are similarly primed today for a more precipitous decline in the face of peak margins on top of increased competition and regulation.

The Fund’s ability to produce strong relative results is not predicated on a technology stock correction or on small-cap stocks more broadly recovering. We continue to see solid operational results across our portfolio holdings, translating into positive stock performance for many. Our management partners are on offense with strong balance sheets and pricing power, allowing them to grow and recognize value in more challenging market environments.

We encourage you to watch our video with Portfolio Managers Ross Glotzbach and Staley Cates for a more detailed review of the quarter.

{kind=link}

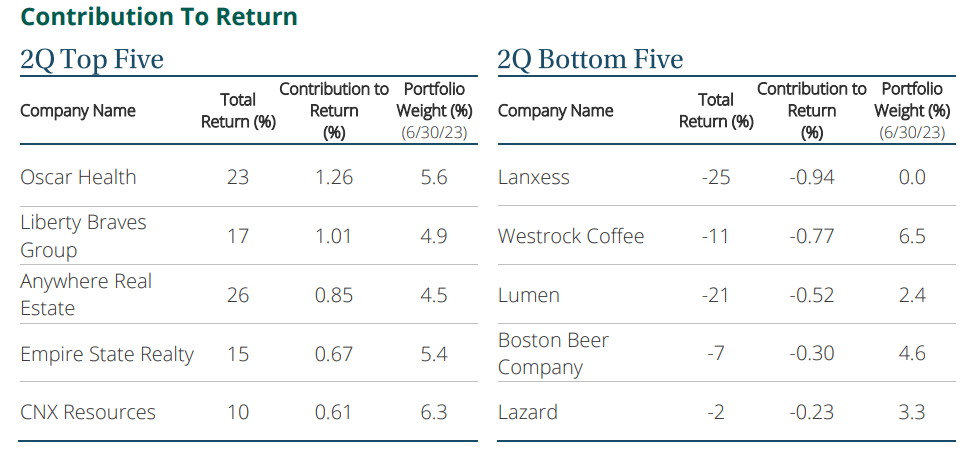

- Oscar Health ( OSCR ) - Health insurance and software platform Oscar Health was again the top performer in the quarter and for the first half. New CEO Mark Bertolini brings significant operational expertise, as well as a strong endorsement value to the business, given his long-term track record as CEO of Aetna. As discussed last quarter, his compensation package aligns his interests with shareholders. He is already executing on improved cost control and operational efficiency that should translate into improved results in the next 6-12 months. In the quarter, the company affirmed near-term results are on track.

- Liberty Braves Group ([[BATRA]], [[BATRK]], [[BATRB]]) - Liberty Braves Group, which owns the Atlanta Braves baseball team and real estate around the stadium, was another top contributor in the quarter. Liberty is on track to spin out this tracking stock as a standalone company in the third quarter, which is likely to result in a price re-rating, as we have seen in numerous other Liberty tracking stock investments over our history. The baseball team is off to a strong start this season, and the Braves sold out of season ticket inventory for the first time in franchise history and drew their largest home opening crowd in Truist Park history. Our appraisal has steadily grown, and we believe the Braves could be an interesting take-out candidate once it trades as a standalone business.

- Anywhere Real Estate ( HOUS ) - Real Estate brokerage franchisor Anywhere was another solid performer in the quarter and for the first half, benefitting from “green shoots” in the seemingly bottomed-out US housing market. Management has maintained strong cost control, and even at this depressed level, Anywhere is producing net positive free cash flow ((FCF)) today with the potential for strong future franchise fee growth.

- LANXESS ([[LNXSF]], [[LNXSY]]) - German-listed specialty chemical company LANXESS was the top detractor after announcing a higher-than-expected profit warning in the quarter. The company has faced a triple whammy of industry-wide destocking, exposure to delayed demand recovery in China, and costs related to cleaning up the operations of the business. We believe the scale of the warning reflects management taking all the pain upfront to ensure it was a “one and done” warning. We exited the position post-quarter end to fund new positions, as it no longer qualified as a top-20 holding for the Fund.

Portfolio Activity

In the second quarter, we initiated three new positions, added to Boston Beer Company ( SAM ), a new purchase in the first quarter, sold Vimeo ( VMEO ) and LANXESS (discussed above), converted our Lumen ( LUMN ) equity position to a smaller position in Lumen bonds, and trimmed several strong performers. Founded in 1984 by Jim Koch, Boston Beer today includes original beer brand Samuel Adams, Twisted Tea (which has become the largest part of the value), regional craft beers like Dogfish Head, Angry Orchard cider, and Truly Seltzer, where it is the number two player in its category. Boston Beer’s share price soared to over $1,200 per share amid a great “seltzer boom” in 2020, which ultimately proved to be a fad, providing us an opportunity to invest in this great business that has compounded over time at a double-digit compound annual growth rate ((CAGR)). We are still building out the three new holdings purchased in the second quarter, two of which we’ve owned successfully before.

We exited Vimeo and long-term position Lumen in the quarter, both of which were disappointing investments that resulted in a permanent capital loss in the portfolio. At Vimeo, we initially misjudged how much of a COVID beneficiary the business had been, and our sum-of-the-parts valuation proved to be too generous for some of the underlying assets that were less differentiated than we originally believed. We sold our remaining equity position in Lumen, after reducing our position in the first quarter when it became clearer the new management team under CEO Kate Johnson would not pursue a strategic path to monetizing Lumen’s consumer business. At their first analyst day in early June, new management presented disappointingly weak financial targets and significant further spending without a clear path to revenue growth. Throughout our holding period, we saw bond market pricing holding up and supporting our case for the strength of Lumen’s balance sheet, but in the second quarter, this reversed with bond prices becoming overly distressed. We lowered our appraisal as our outlook for the company deteriorated, leading to a full exit in our equity position in the quarter. However, the incredibly depressed bond prices created a unique opportunity to own Lumen bonds that are backed by hard assets (property plant and equipment to which the company assigns a $150 billion replacement cost) and offer equity-like returns. The bonds are not as dependent on the people part of the case and offer a compelling opportunity to implicitly pay a 3x EBITDA multiple for assets with a materially better risk-reward profile.

While any permanent capital loss is disappointing, having taken these losses and others put the Fund in a very tax-advantageous position, meaning we could realize significant future capital gains without incurring a capital gain distribution. The higher-than-average portfolio changes YTD illustrate the continued improvement in our process and the productivity of the team, with the proceeds of our exits going to fund new opportunities with a better margin of safety and significant potential upside. Kodak ( KODK ) ended the quarter at a larger-than-6.5% position size, and we expect to work this down in due time. Similar to how Westrock Coffee ( WEST ) temporarily exceeded our 6.5% position limit at the start of the year, we will not rush a move like this to hit a quarterly report, but we will always be working to get to the right weighting. Just after the quarter end, Kodak announced a major refinancing, which both expanded and extended its term loan. This signals heightened confidence in the Kodak turnaround and in the various sources of value at the company by a lender who is also an equity owner and board seat holder.

Outlook

The Fund delivered a solid first half, despite macro headwinds, and with materially different return drivers than the index. We believe this positions the Fund to deliver differentiated future returns. The research team has been busy evaluating existing holdings and identifying new opportunities, resulting in upgrades to the portfolio. Our management teams have been similarly busy, taking steps to get the underlying value of their businesses recognized. The portfolio ended the quarter with a compelling price-to-value (P/V) ratio in the mid-60s%, indicating significant future potential upside.

Important disclosuresBefore investing in any Longleaf Partners Fund, you should carefully consider the Fund’s investment objectives, risks, charges, and expenses. For a current Prospectus and Summary Prospectus, which contain this and other important information, visit Mutual Fund Resources| Longleaf Partners Funds | Southeastern Asset Management Please read the Prospectus and Summary Prospectus carefully before investing. RISKS The Longleaf Small-Cap Fund is subject to stock market risk, meaning stocks in the Fund may fluctuate in response to developments at individual companies or due to general market and economic conditions. Also, because the Fund generally invests in 15 to 25 companies, share value could fluctuate more than if a greater number of securities were held. Smaller company stocks may be more volatile with less financial resources than those of larger companies. The Russell 2000 Index measures the performance of the 2,000 smallest companies in the Russell 3,000 Index, which represents approximately 10% of the total market capitalization of the Russell 3000 Index. The Russell 2000 Value index is drawn from the constituents of the Russell 2000 based on book-to-price (B/P) ratio. An index cannot be invested in directly. EBITDA is a company’s earnings before interest, taxes, depreciation and amortization. Free Cash Flow ((FCF)) is a measure of a company’s ability to generate the cash flow necessary to maintain operations. Generally, it is calculated as operating cash flow minus capital expenditures. Compound annual growth rate ((CAGR)) is the mean annual growth rate of an investment over a specified period of time longer than one year. “Margin of Safety” is a reference to the difference between a stock’s market price and Southeastern’s calculated appraisal value. It is not a guarantee of investment performance or returns. As of June 30, 2023, the top ten holdings for the Longleaf Partners Small-Cap Fund: Eastman Kodak, 8.7%; Westrock Coffee, 6.5%; Gruma, 6.5%; Mattel, 6.4%; CNX Resources, 6.3%; White Mountains, 6%; Oscar, 5.6%; Empire State Realty, 5.4%; Liberty Braves, 4.9% and Hyatt Hotels, 4.8%. Fund holdings are subject to change and holdings discussions are not recommendations to buy or sell any security. Current and future holdings are subject to risk. Funds distributed by ALPS Distributors, Inc. LLP001443 Expires 10/31/2023 |

Editor's Note: The summary bullets for this article were chosen by Seeking Alpha editors.

For further details see:

Longleaf Partners Small-Cap Fund Q2 2023 Commentary