DLAKF - Lufthansa Stock Can Fly Higher On Business Strength

2023-11-06 13:53:20 ET

Summary

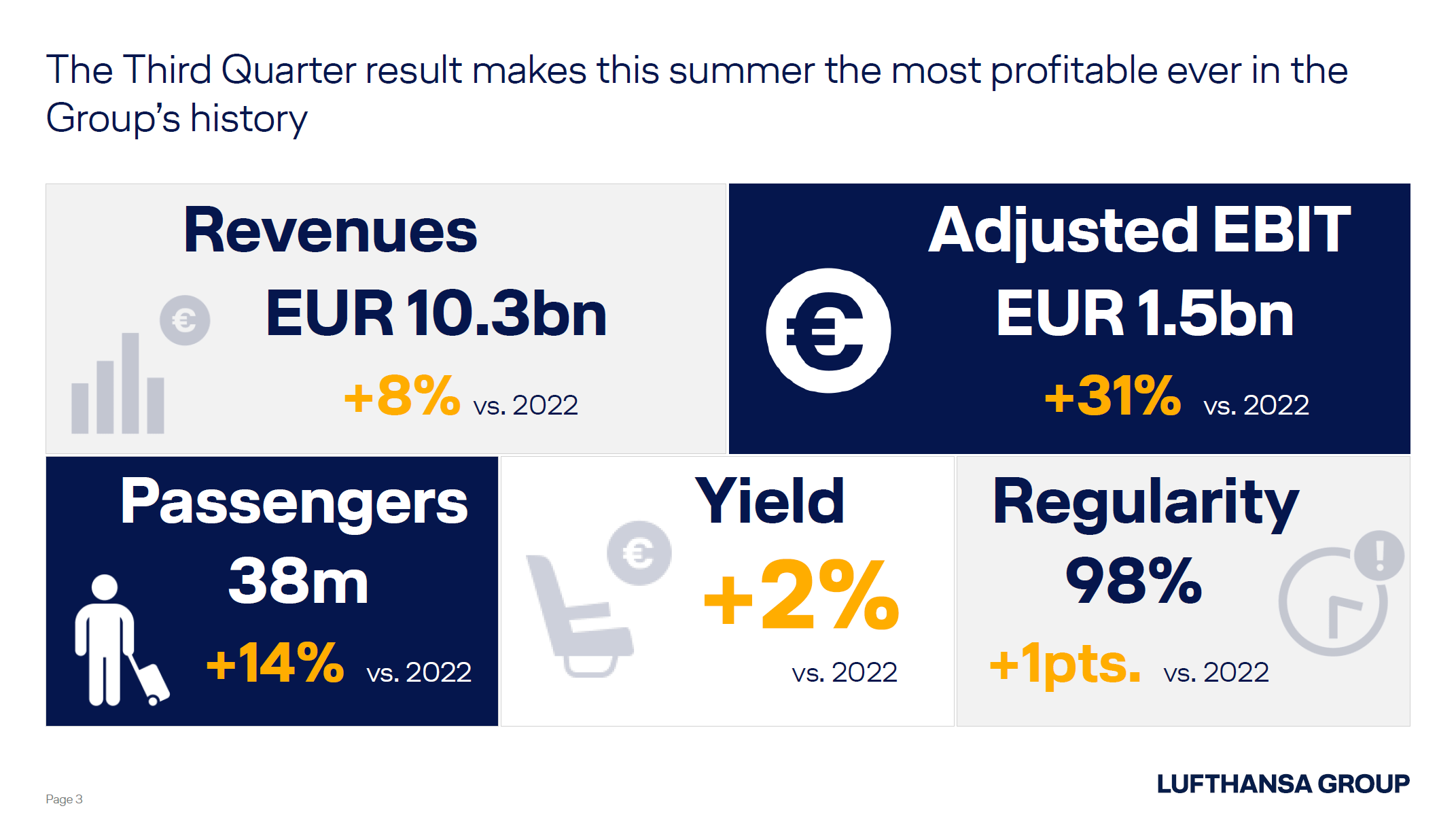

- Lufthansa's Q3 revenues were up 8% to €10.3 billion, marking the highest ever revenue quarter for the company.

- Passenger air travel business showed strength with a 14% increase in revenues, aided by yield expansion and lower fuel costs.

- Lufthansa expects strong demand for passenger air travel to persist and has a strong cash position to service debt.

I've been following Deutsche Lufthansa AG ( DLAKF , DLAKY ) for a while and while I am certainly not a big fan of their product on the European market, I do like the way the management is managing the company. Generally, I think post-pandemic the big legacy carrier groups are doing a better job managing the business so with the current changing cost structure including high oil prices it is going to be interesting to see how each group manages the business. In this report, I will be re-evaluating my rating for Lufthansa.

Lufthansa Results Radiate Demand Strength

{kind=link}

Lufthansa's revenues were up 8% to €10.3 billion on a 14% increase in passengers. It marked the highest-ever revenue quarter for the company with the exception of the summer of 2017 when the insolvency of Air Berlin boosted results for the Lufthansa Group. The increase in revenues falling short of the passenger growth should not be viewed as a negative marker for the demand environment for passenger air travel as the revenues are the entire group's consolidated results.

{kind=link}

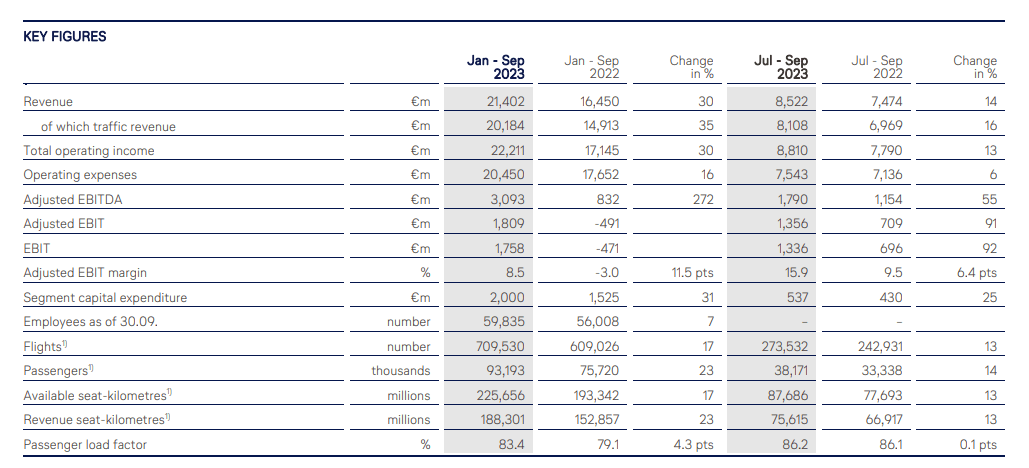

Solely looking at the passenger air travel business, we see that 13% capacity was added year-over-year and that translated into 14% higher revenues aided by yields expanding around 2%. The yield expansion was most notable in the long-haul operations with an expansion of 2.6% compared to 0.8% for the short-haul business. All of this was achieved with a capacity that was 12% lower than in 2019 and corporate travel only having recovered 60% in terms of volume. Results were further aided by lower fuel costs. On a 13% increase in capacity, revenues jumped 14% and unit costs declined around 1%. Unit costs excluding fuel are still 13.2% ahead of 2019 levels, but there are really two elements that feather into this. The first one is that the capacity is still 12% below 2023 levels. So essentially, if the capacity is fully recovered, the CASK excluding fuel would be around 1% higher. The second element is the cumulative price increases since 2019 which is 25.9%. So, I would say that the company is managing costs very well.

{kind=link}

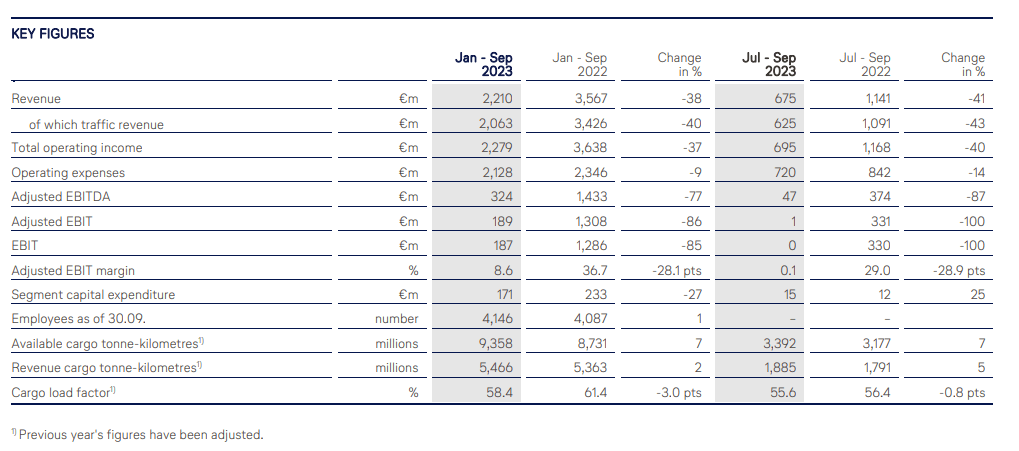

The strong results for Lufthansa's passenger operations were partially offset by the logistics business also known as Lufthansa Cargo. As more and more belly freight is coming online and the e-commerce boom seen in the past three years or so is tapering, air freight results remain under pressure. However, on a 41% decrease in revenues, the company managed to breakeven which I think is not a great result but very realistic for the current supply and demand setting. Yields are stabilizing, which is a positive sign, and for the fourth quarter driven by seasonality, the company expects its air freight business to be profitable.

{kind=link}

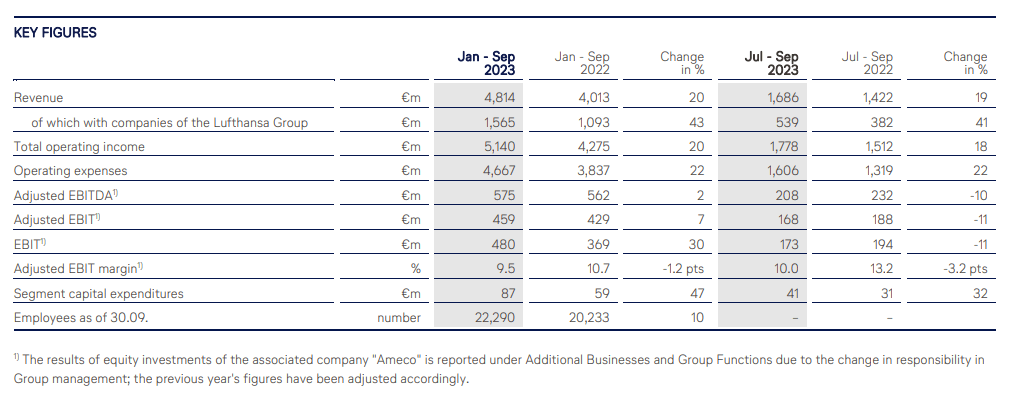

Lufthansa Technik saw its revenues increase by 19%, but it did not translate to the bottom line as EBITDA decreased by 11% driven by higher CapEx and the negative effect of currency exchange rates.

All in all, we are seeing strong group results where the passenger business continues to show strength with yield expansion weighed down by the challenging environment for air logistics and negative forex effects on the results for Lufthansa Technik.

The Headwinds And Tailwinds For Lufthansa

{kind=link}

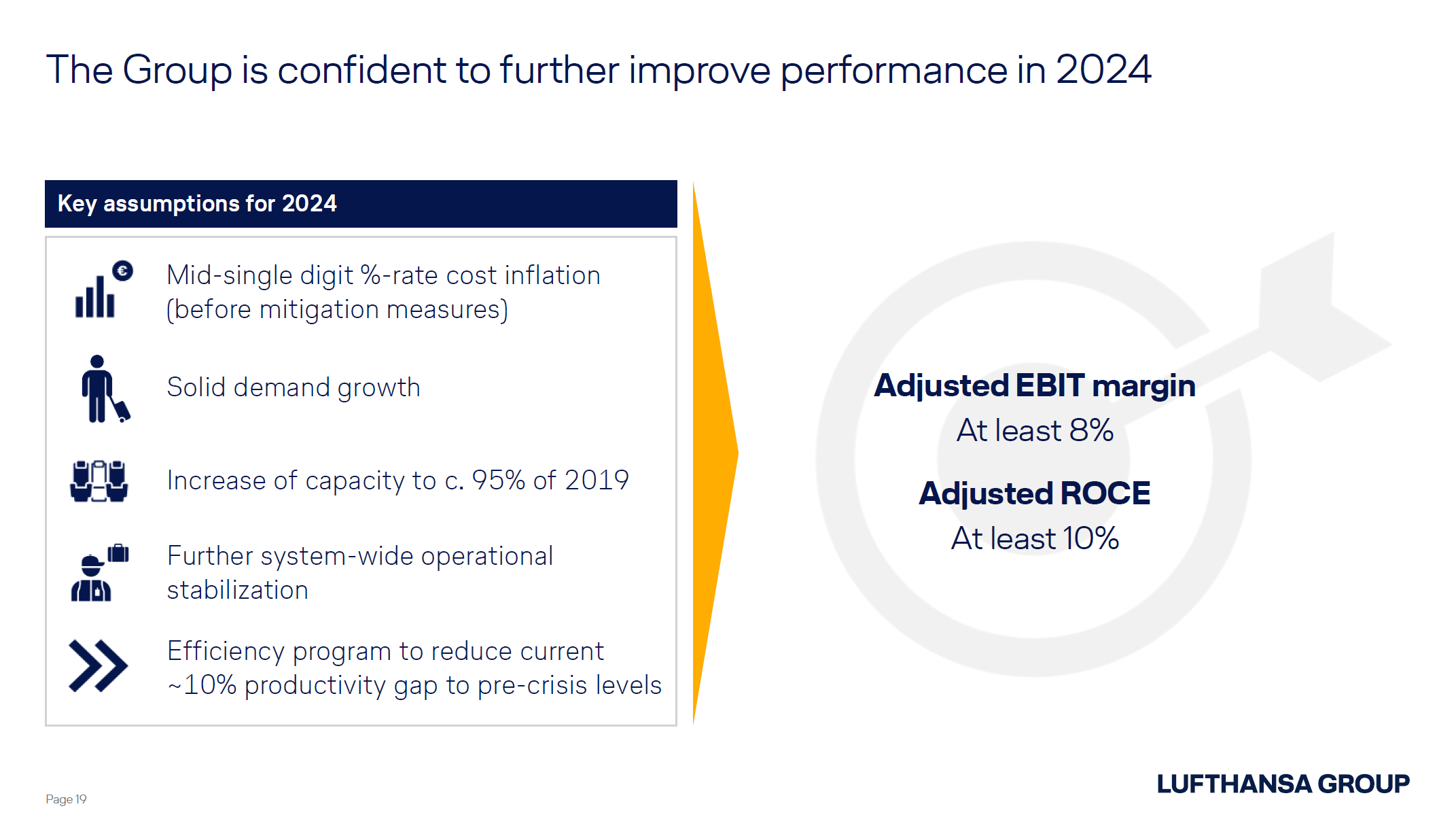

Lufthansa has kept its 2023 guidance unchanged indicating capacity levels of 85% of 2019 and Q4 2023 capacity of 91% with adjusted EBIT targeted at a minimum of €2.6 billion and significant positive free cash flow despite the increase in oil prices. It is more interesting to shift our focus to 2024. For 2024, the company is 74% hedged on fuel consumption with the expectation that fuel costs will be stable year-over-year. Furthermore, the company expects to operate at 95% of pre-pandemic capacity and further reduce unit costs aided by an efficiency program initiative.

The pressure that the company faces is with regard to the Pratt & Whitney ( RTX ) GTF issue which will see on average, 20 airplanes grounded in 2024 for the Lufthansa Group. The company is addressing these issues by extending the operations of some of its Airbus A320ceo family airplanes. The continued shortage of airplanes is also expected to continue benefiting Lufthansa Technik, where on a case-by-case basis Lufthansa will determine whether to do some required MRO activity in-house or outsource it to service external customers.

{kind=link}

Corporate travel is expected to recover to 70%, which is somewhat below initial expectations presented earlier this year. This, however, does not mean that revenues will be lagging significantly as the yields on corporate travel are extremely strong compared to pre-pandemic times and we also see more interest in premium leisure products while the German lower-yield market is one of the reasons for the slower recovery, but that is hardly a bad thing. Furthermore, the long-haul operations are still in the early innings of recovery primarily in Asia.

Lufthansa will fully recover in the North American market and exceed 2019 levels in the European market with a reduced focus on the German market. In China, international demand will be 80% recovered, but Lufthansa will only have 65% of its capacity restored and in Asia-Pacific, the company will pace its capacity with the demand. In all end markets, with Asia-Pacific excluding China being the exception, we see that demand is in excess of Lufthansa's ability to supply and that likely also holds for its peers. It's a bit of a long-winded way to say that Lufthansa expects the current strong demand environment for passenger air travel to persist.

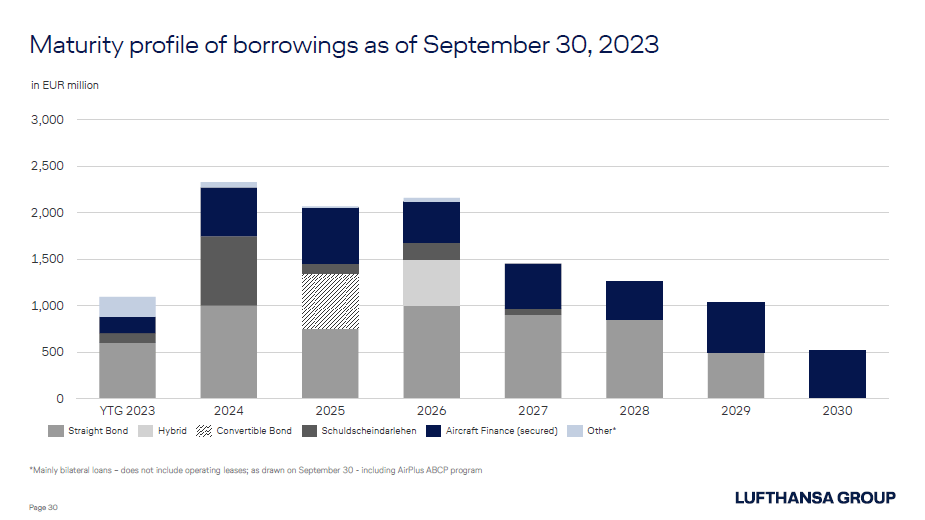

Lufthansa Has A Strong Cash Position To Service Debt

{kind=link}

Quarter-over-quarter, Lufthansa has reduced its net debt by €800 million and €1.5 billion since the start of the year. The company has €9 billion in cash and cash equivalents including marketable securities which means that it can service its net debt through 2026 while there is roughly €2.5 billion of assets held for sale. So, the company can service its debt with cash and cash equivalents plus proceeds from assets held for sale, which puts it in a very comfortable position given that free cash flow generation is not even factored into this.

Does Lufthansa Pay A Dividend?

Lufthansa currently does not pay a dividend, but it is looking to distribute between 20 and 40 percent of its recurring net income among its shareholders. The consensus estimate is that Lufthansa will be reporting a net income of €1.75 billion for the year, which would put dividends distributed in 2024 at €350 million to €700 million. With a share count of around 1.2 billion shares, this would indicate around €0.30 to €0.60 per share implying a forward yield of 4 to 8 percent which I would consider to be somewhat attractive. From a yield perspective, it would most certainly be attractive, but airlines are not known for providing a stable underlying stock price which reduces the appeal somewhat.

Lufthansa Stock Became A Stronger Buy

{kind=link}

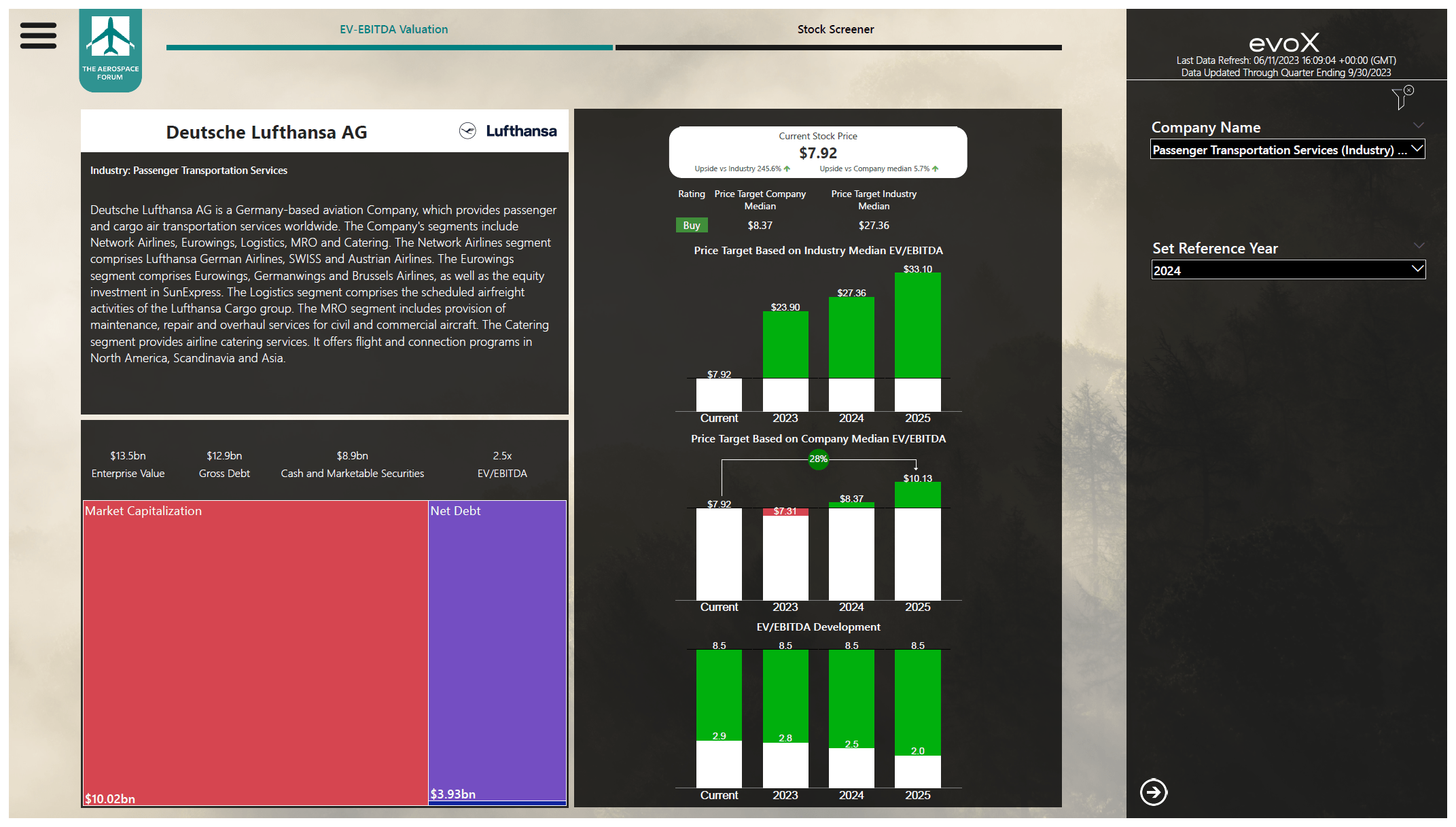

After carefully studying and implementing the balance sheet data for Lufthansa as well as the forward projections, my model shows a $1.60 lower price target for Lufthansa. However, due to the significant decline in stock prices, the upside has improved to 28%.

As a result, I am reiterating my buy rating for the stock as Lufthansa continues to operate in a capacity-constrained market, has a manageable debt, will pay a dividend again, and has its forward fuel consumption hedged for 74%. Furthermore, the sale of the remainder of the LSG Group was finalized in October and the sale of Lufthansa AirPlus, specialized in processing corporate travel payments, is expected to be completed in 2024. All of this helps the company focus on its core business. Further supporting the company's liquidity and focus is the planned spin-off of Lufthansa Technik adding further appeal to the business.

Conclusion: Prudent Execution At Lufthansa Warrant A Buy

While there is significant pressure on airline stocks due to rising oil prices and some observed fatigue in the US domestic market, Lufthansa has a significant upside. What we do see is that the company's stock price has tanked over the past six months, but contrary to the US domestic market, which Lufthansa obviously does not serve, Lufthansa's end markets remain strong, and the company has hedged a significant portion of its fuel consumption into 2024 providing two drivers of strength going forward while the company should be able to easily service its debt and focus its business by means of selling parts of the non-core business.

For further details see:

Lufthansa Stock Can Fly Higher On Business Strength