FCX - Lundin Mining: Copper Narrative Is Not Playing Out Like Expected

2024-01-02 19:45:35 ET

Summary

- Lundin Mining has acquired new mines in Chile and is investing in Argentina, aiming for cost savings and increased production capabilities.

- Copper prices are expected to increase due to supply shortage, but new mines and a decrease in Chinese construction demand are significant.

- ING predicts a copper supply surplus going into FY2024, decreasing copper prices, while Lundin has overextended in its expansion plans.

- The recent closure of a major mine presents a good exit opportunity.

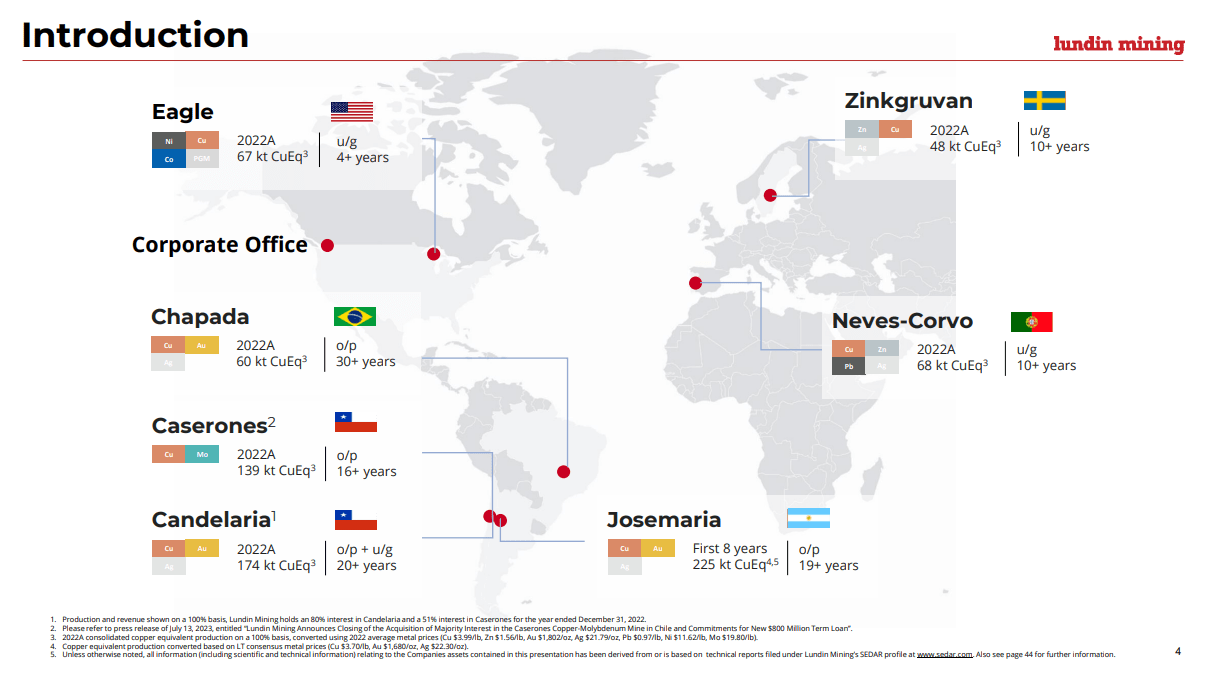

Lundin Mining (LUNMF) is a family-owned mining business focused on copper based in Canada. The company is diversified across different mines and minerals. They operate mines in different countries, such as Chile, Sweden, and Argentina. It is a relatively small miner, which is expanding rapidly.

Lundin Mining Operations (Lundin Mining Q3, 2023)

{kind=link}

Lundin mining is primarily focused on copper, which makes up the majority of their production and profits. The reason for this strategic focus on copper is the energy transition from burning fossil fuels to more electrical use cases. The increased use of electrical energy is predicted to increase copper demand.

This same bullish narrative is shared by many copper miners, such as Freeport-McMoRan ( FCX ), attracting significant investor interest in copper miners as a whole. An important report on this trend was published by S&P Global, predicting a worldwide shortage in copper as a result of these trends.

Copper's role in the energy transition

Copper is useful in electrical use cases because of its conductive properties. There is no real replacement for the copper wiring that is used in many electrical devices and increasingly so in green energy. Although aluminium wiring can also be used, it has several inferior properties compared to copper.

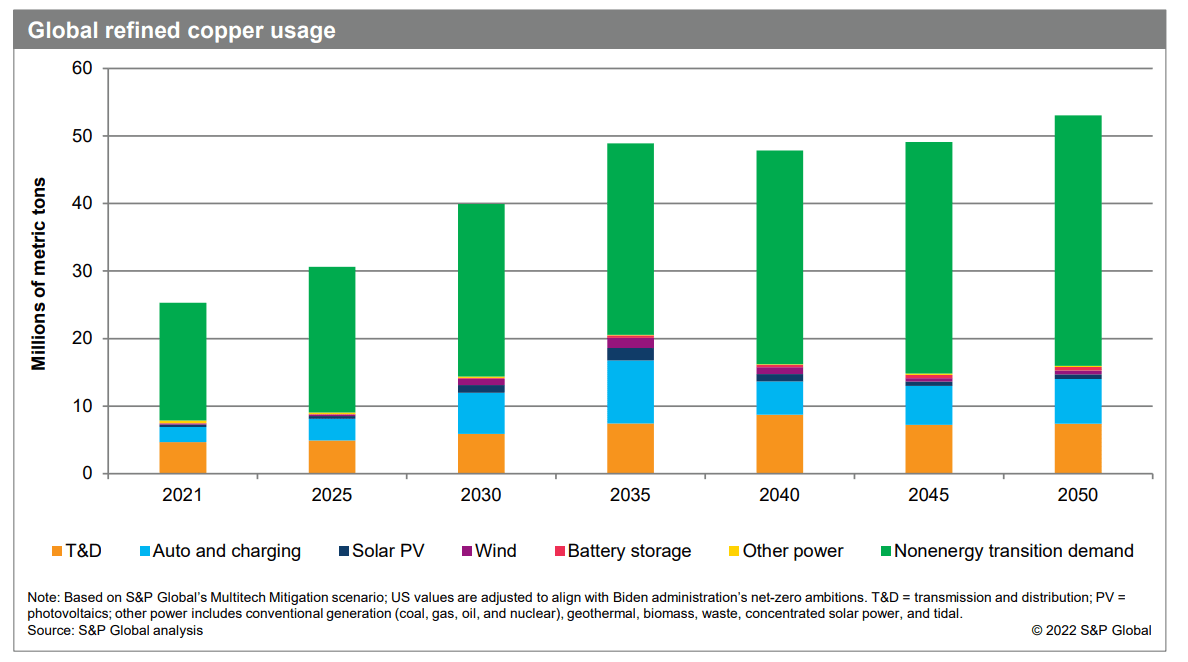

According to S&P Global , copper demand is expected to increase drastically over the coming decade. The chart below shows their predictions for copper demand. The green bars confusingly show "non-green" copper demand, such as the use of copper in construction and manufacturing projects. The other colored parts show demand in various areas increasing because of the "electrification" of the economy as the world shifts to net zero emissions. For instance, the increased use of copper material in electrical vehicles (EVs).

However, this bullish prediction is relatively speculative and questionable. The total demand from "green" use cases is still only a small part of the total copper demand. The main increase is predicted to come from "auto and charging", which is the blue bar in the chart below. Unfortunately, the adoption of EVs has slowed down recently because of decreased subsidies and EVs have not even started significant adoption yet outside of affluent Western societies.

Projected Copper Demand ( S&P Global, 2022 )

{kind=link}

Questioning this bullish copper narrative

Copper is not a rare mineral in the sense that there is not enough copper in the ground, but the story is that it is difficult to extract enough of this copper. There is an increasing demand for copper projected, but this is not followed by a large increase in supply because of various reasons (e.g., environmental). This implies that copper prices will increase because of a supply shortage. However, an increase in price would incentivize more production. According to S&P Global, however, a big increase in copper supply would be unlikely:

One way to meet the demand growth would be to develop and open new mines. Theoretically, future demand could be met by opening three “tier-one” mines, each producing 300,000 metric tons of copper per year every year for the next 29 years. ( S&P Global, 2022 p.46 )

This doesn't sound like an impossible task to me, but according to S&P Global, this will be very difficult to pull off. It is a very lengthy and expensive process to develop a new copper mine, such that starting a new mine now would take approximately 10 years to develop starting from scratch. Due to environmental regulations, it has become increasingly difficult to get permits for mining rights and all the easily available copper has been mined first. Developing new mines is therefore more costly and difficult than before, e.g., deep sea mining .

[Opening these new mines] would be a monumental and taxing job, and without any precedent historically and costing over $500 billion in today’s dollars. Moreover, it can take more than a decade and a half to develop a new mine. ( S&P Global, 2022 p. 46 )

This is a questionable statement by S&P Global, as it is not unprecedented for the international mining community to build three "Tier-1" mines. The existence of such tier-1 mines, such as the Candelaria mine that Lundin operates, already shows that it is possible to develop such mines. It seems to me that the S&P Global report tries to create a bull case for copper.

Ongoing development of new mines (supply)

There are multiple projects underway to increase the supply of copper. For instance, the Josemaria project that Lundin Mining is developing would already add about 130,000t of copper annually, thereby meeting about 15% of this supply gap alone. The total capital investment for this project is estimated to be about $3b, so repeating six of these smaller projects would cost about $18b extra for a total investment of $21b instead of the $500b that S&P Global is predicting. In addition to this project, there are multiple copper projects under development. For example, the large supply that IVPAF Ivanhoe Mines is bringing to market, with a variety of different projects in Angola and Congo .

Construction going on at Josemaria (Saxum Engineering)

This increase in supply could close the anticipated supply gap, especially when the projected demand turns out to be lower than expected. And there are various reasons to believe that copper demand will decrease in the near term.

Copper's Future Demand ("Non-Green")

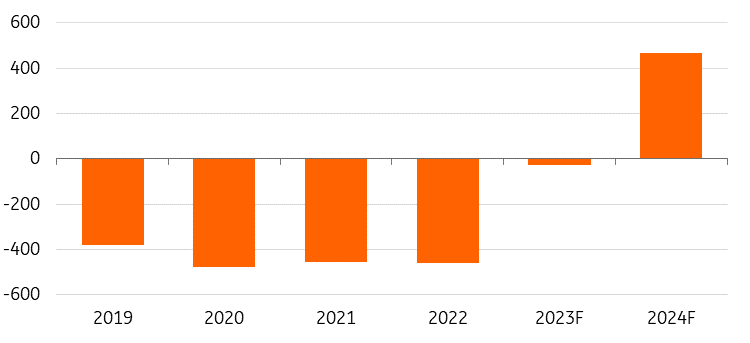

Green energy is still only a small part of copper demand, currently, the majority of demand comes from construction (e.g., it's 25% of China's total copper consumption). With the current property crisis in China, it's likely that construction will decrease and thereby negatively impact copper demand in the short term. This is because China has built too many homes, which are now empty ghost towns. It can already be seen that Chinese construction is down, hurting copper prices. According to ING research, we are moving into a supply surplus in the coming year because of this construction slowdown:

We believe that until the market sees signs of a sustainable recovery and economic growth in China, we will struggle to see a long-term move higher for copper prices. ( ING, 2023 )

Copper supply deficit/surplus (ING research 2023)

{kind=link}

ING's analysis of the copper market spells doom and gloom for next year. With a large surplus of copper supply next year, the copper price will go down. Despite some projected growing demand from green energy projects in the long term, there is a big projected decrease in demand from traditional sectors such as Chinese construction and manufacturing in the short term for FY2024.

We believe the short-term outlook remains bearish to neutral for copper demand and we do not foresee a substantial recovery in prices before the second quarter of the year, which should mark the starting point for Fed rate cuts. We see prices averaging $8,300/t in 1Q before moving higher to $8,400/t in 2Q. Prices are likely to remain volatile through the year as markets will continue to react to macro drivers. ( ING, 2023 )

This predicted surplus for next year stands in contrast to S&P Global's scenario where there would be a large supply deficit next year. However, this report stems from 2022 when the Chinese construction crisis was not yet evident.

Copper Market Balance ( S&P Global, 2022 )

Uncertain Future "Green" Demand

Importantly, the proposed drivers of increased copper usage such as EVs and building out the electrical grid are not such big drivers of copper demand compared to the traditional sources of demand. The main use of copper remains to be in construction and manufacturing mainly in China. However, the energy transition could still increase copper demand long-term.

Unfortunately, the impact of this "green" copper demand is uncertain and highly dependent on various things in the future. For instance, if the energy transition takes longer than expected, or if the Net Zero plan does not unfold like planned, then the impact of that on copper prices could be very negative for investors. It seems quite likely to me that these goals will not be achieved and that EV adoption will be limited mostly to Western countries. Furthermore, re-election of Trump in 2024 could derail and put the brakes on the energy transition in general as well, which will further hurt copper miners.

Copper intensity in EVs ( S&P Global, 2022 )

{kind=link}

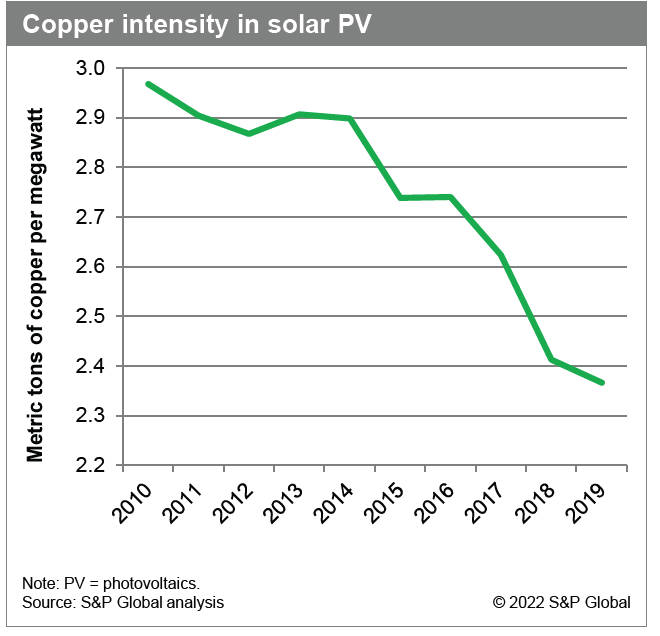

Finally, in addition, due to various improvements in engineering, manufacturers will most likely reduce the intensity of copper usage. Increasingly so, as copper becomes more expensive, which is happening in the case of solar panels. In the same line, recent innovations have reduced copper usage in EVs.

Recent Developments

Lundin has two new mines due to the recent acquisition of Caserones in Chile and the ongoing Josemaria project, developing a new mine in Argentina. This is a large and expensive construction project that will take some time to start production. According to the company , they estimate that this new mine will be operational around FY2026. Given the large costs involved with developing new mines, this takes its toll on the company's net profits and balance sheet.

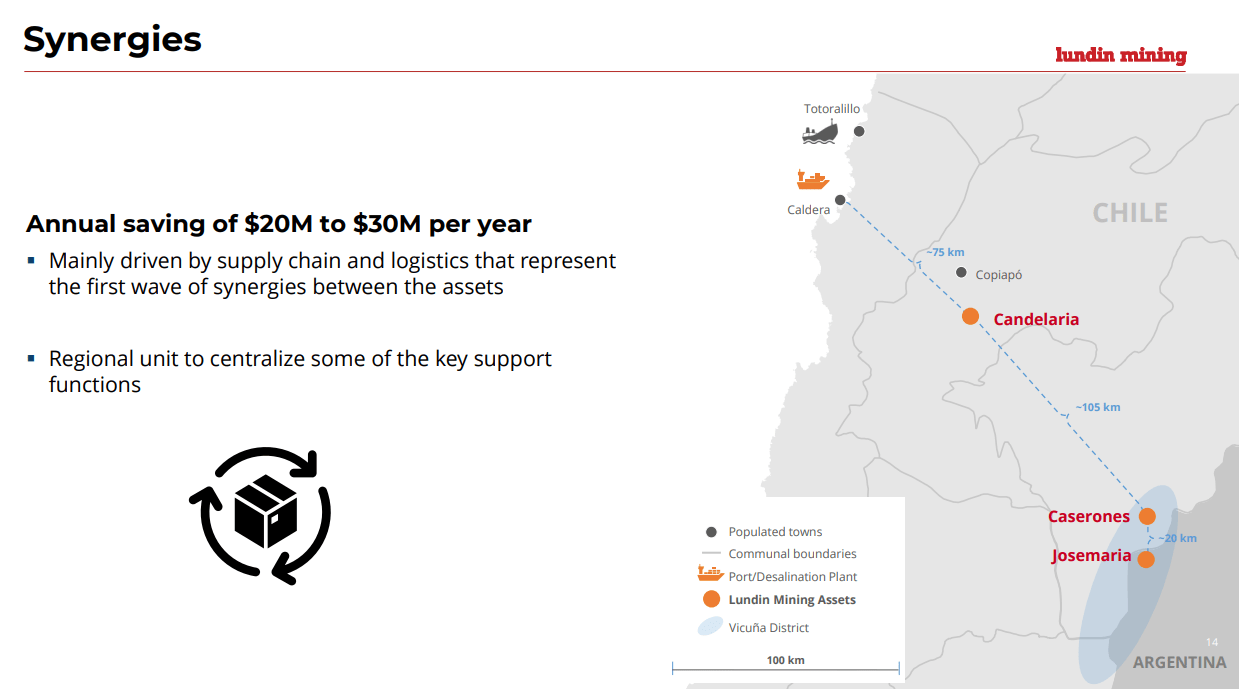

New project synergies (Lundin Mining, 2023)

{kind=link}

Lundin Mining claims that there is "synergy" of these new mining projects around their main Candelaria mine, synergy is perhaps the most overused term in business but here it could actually make sense. The new mines could share resources and supply chain networks because they are close together (i.e., 20 km). This could form an important "mining district" for Lundin Mining, which they claim could lead to approximately $20-30m in cost savings.

However, their main Candelaria mine is still more than 100km away from the two new mines. It remains to be seen how much synergy can be created between these projects, but acquisitions generally turn out less great than expected. The company does not plan to make any further acquisitions for now.

Financial Performance and Balance Sheet

As a commodity business, Lundin Mining is very dependent on the general economy and the global copper prices that determine its earnings potential. The limitation of this analysis is that copper prices are very volatile, so the value of these assets differs drastically based on the market price of copper. The price of copper has been very volatile in recent years, as shown below:

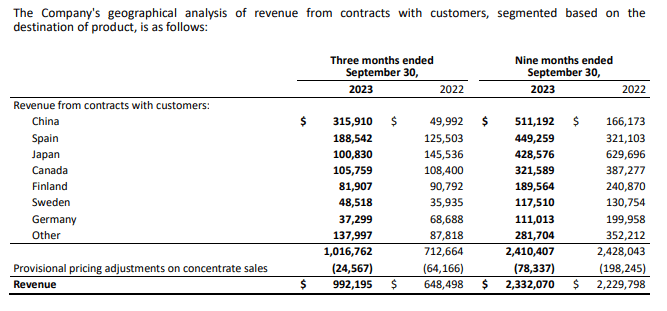

Most of the company's revenue comes from China because it is still the main manufacturing hub of the world, where copper is used in manufacturing electrical appliances and in construction. According to this table, the Chinese revenue more than tripled year-over-year but this wasn't even mentioned in the earnings call. This table is hidden on page 66 of the Q3 report. From this, I can conclude that the Chinese Copper demand is the crucial factor for copper miners, instead of the proposed western "Green" energy of EV demand.

Geographical Revenue Split (Lunding Mining Q3 2023)

{kind=link}

For Lundin Mining, their balance sheet is deteriorating because of the large capex spend. The debt position has increased and a lot of cash has been spent on acquisitions and developing the Josemaria project. To improve their balance sheet, Lundin is considering to sell a stake in their Josemaria mine (minority).

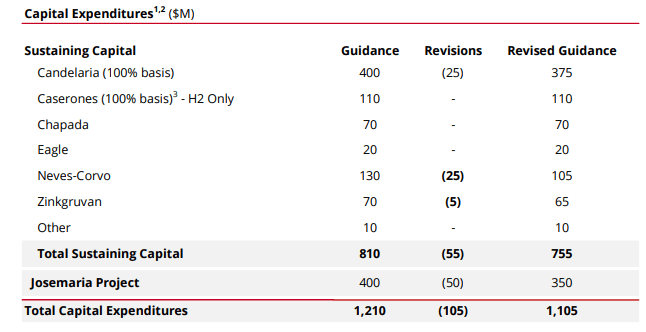

CapEx guidance (Lundin Mining, 2023)

{kind=link}

Lundin Mining is spending a lot to maintain its operations. The investing capex of $400m in Josemaria project can be added back to free cash flow to measure sustaining capital spend, which is $755m. Still, mining is a very capital-intensive industry that is also very dependent on fluctuations in copper prices.

Conclusion

Lundin Mining is a reasonably well-run company currently trading at a fair valuation. It is investing heavily to increase its production capabilities, but it has stretched its balance sheet in doing so. With a projected copper supply surplus going into 2024, the company could run itself into financial trouble.

Most importantly, the long-term narrative of S&P Global about a surge in copper demand due to green electrification is relatively speculative and uncertain. Even if this predicted surge in demand would occur, it could be met by increased supply which would nullify the price effect of increased demand. The recent actions by Lundin Mining already show this dynamic; by investing to increase production they are already closing this anticipated supply gap, just like other competitors might do as well.

Next to "green" copper demand, there are many different, and in my opinion, more important demand drivers, at play that investors may not consider. Most importantly, Chinese construction and manufacturing driving copper demand. In my opinion, the whole case for investing in copper miners should therefore not be based solely on future "green" copper demand. If you want to capitalize on increasing EV usage, then I believe that it would make more sense to invest in EV producers, or EV-related infrastructure, instead of copper mining companies that might indirectly benefit from EVs in a complex way.

My rating for FCX, Lundin (and other copper miners) is therefore a " Sell ", because of a projected copper supply surplus going into FY2024 but it might become an interesting buy again next year with a reduced stock price. The closure of a major mine has created a short-term sell opportunity, where investors can take some profits. In the long term, copper will remain important, but the long-term bullish narrative is questionable. In any case, the timing of an investment in copper and the energy transition is a crucial factor.

For further details see:

Lundin Mining: Copper Narrative Is Not Playing Out Like Expected