VWAPY - Major Yet Subtle BYD Developments Investors Haven't Paid Attention To

2023-10-09 16:41:55 ET

Summary

- BYD has positioned itself as the first/only successful legacy automaker in navigating the shift to electric at scale without compromising on profitability, while also emerging as a global leader.

- But the stock has underperformed broader markets in recent weeks, despite blockbuster Q3 delivery volumes that reinforce its full year 2023 target.

- The increasing mix of auto sales is expected to improve the unit economics of BYD's vertically-integrated production model.

- We believe markets are underpricing this mix shift, which likely sets BYD up for a potential upward re-rating on its valuation multiple, moving it closer to those attributable to its high-growth EV manufacturing peers.

BYD ([[BYDDF]]/[[OTCPK: BYDDY]]) has been the most successful legacy automaker in navigating through the transition to electric. By leveraging its appeal in the Chinese auto market, as well as the competitive advantage that comes with its vertically integrated business model at scale, BYD is becoming an increasing threat to usurping industry leader Tesla’s ( TSLA ) EV crown. This is corroborated by Tesla’s implementation of aggressive price cuts over the past year in an attempt to shore up delivery numbers, with the ensuing price war rocking the performance of all peers except BYD. Tesla’s lead against BYD in global BEV delivery volumes is also rapidly diminishing, with the gap in Q3 narrowing to 3,456 vehicles – the slimmest yet.

Yet BYD's stock has underperformed broader markets over the past month despite its blockbuster delivery numbers. The stock is down about 5% over the past month, relative to the Hang Seng Index’s ( HSI ) approximately 3% drop over the same period. And despite gains of more than 20% on a year-to-date basis, the stock also underperforms by wide margins relative to its North American counterparts, and trades at less competitive multiples than local Chinese EV upstarts still strapped for cash.

The modest performance continues to underscore the impact of several headwinds. They include BYD’s exposure to multiple compression risks facing high capital-intensity auto manufacturing businesses under the risk-off market environment despite their high growth nature. This headwind has been further exacerbated by the incremental drag of historically lower multiples attributable to the parts manufacturing sector, which is also priced into the stock to reflect BYD’s role as a leading supplier of batteries for both the auto and consumer electronics market. More importantly, ongoing geopolitical risks remain a significant overhanging discount factor on Chinese equities, overshadowing the fundamental resilience of names like BYD.

However, BYD’s expanding reach across the EV manufacturing supply chain and across various vehicle types and pricing segments are expected to reinforce its roadmap in becoming one of the most efficient and competitive players in the increasingly electric and digital economy. The stock has largely traded in line with auto parts manufacturing and supplier multiples like that of CATL , but increasing consolidation of EV market share in China and abroad underscores potential for an upward multiple re-rate from current levels.

BYD’s Electrification Journey

BYD has orchestrated one of the fastest and most successful transitions to electric relative to its legacy auto manufacturing peers at home and overseas. The company ceased production of its legacy ICE models in early 2022, becoming not only the “first mainstream automaker” to do so but also the first to maintain market share gains at a profitable beat under the transition.

Specifically, BYD’s monthly delivery volumes have been forging new records at a consistent pace since. BYD finished the third quarter with deliveries of 287,454 vehicles in September, representing a run-rate that could boost annual sales beyond its 3-million-vehicle target by the end of the year. Having already delivered more than 2 million vehicles (or more than 1 million BEVs) in the first nine months of 2023, with consistent double-digit sequential growth, BYD’s full-year delivery guidance of 3 million vehicles seems almost conservative.

The results underscore BYD’s advantage in capitalizing on China’s auto boom led by the transition to EVs over the past several years. Thanks to the company’s ability to vertically integrate manufacturing at scale, and the Chinese government’s generous financial incentives, the BYD brand has been able to maintain its reputation for affordability and quality in the transition to electric, which has successfully captured the likes of China’s mainstream market. Specifically, BYD’s vertically integrated business model, which spans the manufacturing of cars as well as some of the key components within them, has enabled its transition to electric both smoothly and profitably at scale, compensating for the capital intensity that comes with the endeavour. Recall that BYD has long been a manufacturer and supplier of leading EV battery technologies, including the “ Blade ” battery launched in 2020 which can currently be found integrated in foreign rival EV models, including Toyota’s ( TM / OTCPK:TOYOF ) bZ3 and Kia’s ( OTCPK:HYMTF ) EV5 for the Chinese market.

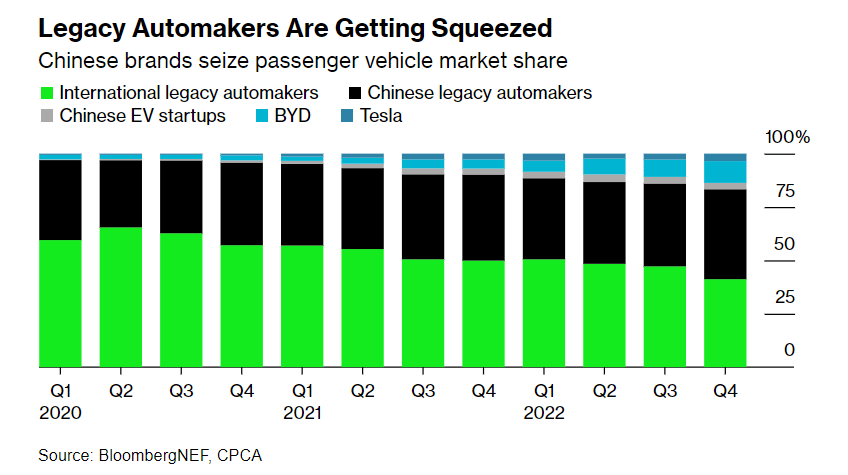

The competitive advantage highlights the divergence from struggles observed in global ICE automakers historically favoured by the Chinese market, including GM ( GM ) and Volkswagen ( OTCPK:VWAGY / OTCPK:VLKAF / OTCPK:VWAPY ). Many of BYD’s foreign rivals are only now starting to allocate capital towards the build-out of internal supply chains, while also struggling to attract sufficient demand needed to achieve economies of scale. The challenge to maintain internal profitability without compromising on affordability for consumers has been gradually displacing the market share of foreign automakers. And much of this has transitioned to the benefits of BYD, as corroborated by its rise in the ranks to becoming “China’s top-selling car brand in the first quarter”, ousting VW by widening margins.

{kind=link}

Consolidating the Chinese EV Market

BYD’s cost advantage, enabled by its vertically integrated business model at scale, has allowed it to consolidate share within China’s auto market – the largest and fastest growing in the world. Despite the aggressive price war launched by leading rival Tesla, which has led to steep price drops across more than 40 auto brands in China this year, BYD has maintained competitive gross profit margins of more than 18% in the second quarter, up by more than 100 bps sequentially. In addition to gradual margin expansion, BYD’s vertically integrated business model has also allowed it to take share of its rivals’ growth and profits by being a key supplier of critical EV technologies – most notably, its batteries, which commands about 16% of global market share and makes BYD the second largest supplier in the industry.

The company’s recent introduction of two additional premium brands – namely, Yangwang and Fang Cheng Bao – is expected to further its TAM. The two newly launched brands aims at penetrating the RMB 1+ million ($137,000+) segment. Specifically, the Yangwang brand has debuted with two battery electric models – the U8 SUV and the U9 supercar – with prices starting at RMB 1,098,000, subsidized by a RMB 8,000 rebate by BYD if the deposit is paid before December 31, 2023.

{kind=link}

Meanwhile, the Fang Cheng Bao “ Leopard 5 ” hybrid SUV unveiled at the Chengdu Motor Show in August is estimated to boast a starting price between RMB 300,000 to RMB 400,000 , with the brand currently accepting pre-orders with a RMB 1,000 deposit, despite limited details on the production and delivery timeline. The brand has also hinted at future models including the “Super 8” SUV and “Leopard 3”. The Fang Cheng Bao flagship SUV is expected to debut with a hybrid powertrain, taking advantage of the segment’s increasing appeal in China:

{kind=link}

Despite the premium price charged, BYD has not relinquished its reputation for affordability in the two luxury brands. Current purchases of the Yangwang U8 comes with an attractive portfolio of post-sales freebies, including 10-year free in-vehicle 5G data availability, 8-year free roadside assistance and 3-year free roadside charging services, in addition to the RMB 8,000 rebate on eligible purchases before December 31, 2023. By leveraging its vertically integrated production strategy to enable significant cost efficiencies, alongside an attractive value-for-money proposition to attract demand from prospective buyers, BYD effectively broadens its appeal and reach to a greater audience across the Chinese auto market with the two new sub-brands.

As discussed in previous coverage , the strategy largely differs from BYD’s upstart peers in the Chinese market. While many of China’s local EV brands have started off business by penetrating the higher priced segments in an attempt to bolster profit margins and pave the way for supporting a capital-intensive journey into auto manufacturing, BYD has shown success in doing the opposite. Both Yangwang and Fang Cheng Bao are likely to drive further consolidation in China’s premium EV sector, given BYD’s brand reputation among local buyers. Specifically, the upper tier 1 and tier 2 Chinese economies, which have remained the most active drivers of EV adoption in the region, continues to show significant headroom for growth – EV penetration rates average close to 40% in the more affluent Chinese regions, with plug-in SUVs being the best-selling vehicle type, underscoring favourable tailwinds for Yangwang and Fang Cheng Bao’s initial go-to-market strategies. Taken together, the two sub-brands stand a good chance at complementing the mass market BYD brand in further displacing both domestic and foreign rivals’ market opportunities and aid further expansion of its own local market share. This will inadvertently drive greater scale to BYD’s vertically integrated business model, and enable a sustained trajectory of profitable growth over the longer-term.

BYD Beyond China

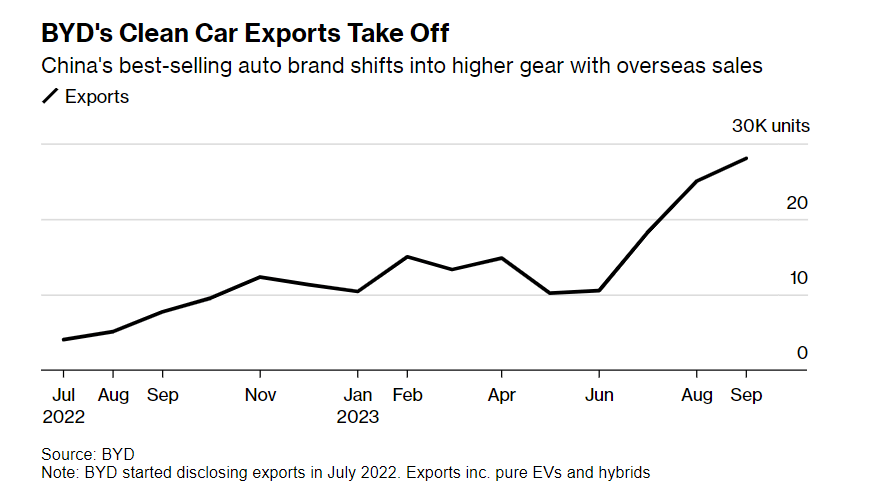

In addition to broader electrification tailwinds at home, bolstered by BYD’s mission-critical role in the provision of supporting innovations, the company has also “identified the global business as a new avenue for growth”. Since expanding its passenger vehicle sales to international markets in 2021, BYD now sells in more than 54 regions, with export volumes reaching new records. BYD reported a 9% mix of overseas deliveries during the third quarter, accelerating from 5% in the second quarter.

{kind=link}

With plans to further expand its presence across the APAC, EMEA and Latin American regions, BYD’s overseas strategy is likely to become a “key volume driver” and complement its rising market share dominance at home. Specifically, Chinese imports currently account for 8% of Europe’s EV sales. Current market forecasts anticipate the figure to jump to 15% by mid-decade, bolstered by the appeal of Chinese EVs’ affordability to prospective buyers in Europe, with prices being on average 20% cheaper than local EU-made models. This has incentivized the European Commission to launch a year-long probe into “Chinese subsidies for EVs in a bid to ward off a flood of cheap imports”. Dubbed as “anti-subsidy actions”, any findings could potentially lead to the imposition of import duties on Chinese EVs aimed at levelling their prices to domestic offerings.

However, BYD executives have recently played down the risks of the ongoing EU investigation, citing that the current EV adoption and competition trends in the region are a function of the broader “ revolution ”. Even in the event that an anti-subsidy import duty is imposed by the EU government, BYD is likely to weather the headwinds better than other home-grown Chinese rivals given its strong balance sheet and efficient cost structure. BYD’s presence in the overseas passenger EV markets also outperforms its local peers by wide margins, which further reinforces its prospects of becoming a global staple brand, similar to its mass market peers from Japan and Korea. BYD is currently one of the best-selling Chinese brands in Europe, with the “Atto 3” SUV being the top-selling EV in Sweden over the summer. And the company likely has “volumes over profitability” as the near-term strategy in its overseas playbook, with an aim to first bolster its reputation in international markets, then expand their scale in markets beyond China.

Meanwhile, BYD’s relatively limited presence in the North American passenger vehicle market is likely to be compensated by its commercial footprint within the foreseeable future. BYD is currently a key seller of electric buses to the North American market, taking advantage of opportunities ensuing from governments’ zero-emissions targets pledged in recent years. Market data shows that the electric bus market in North America is primarily consolidated among five players, with BYD being the leader . This highlights BYD’s expanding global reach, despite its decision to not partake in North America’s passenger EV opportunities, citing the Inflation Reduction Act as one of the barriers to entry.

We believe BYD’s decision to focus on commercial opportunities in the North American market is a prudent choice. It allows the company to leverage the commercial ties it has been building in the region since more than a decade ago, while also enabling an observation period on the performance success and mishaps of emerging mass market peers like Vietnam’s VinFast ( VFS ) to better gauge North Americans’ preferences before planning an entry to the market.

Valuation Considerations

BYD continues to underperform its local EV peers, despite massive outperformance on key performance metrics spanning delivery volumes, sales growth, and profitability.

{kind=link}

Instead, the stock’s performance appears to mirror its parts manufacturing peers, which are valued at a much lower multiple due to their high capital intensity and slim profit margins.

{kind=link}

The relative comparisons highlight not only the geopolitical risk discount factor on Chinese growth equities, but also the drag of inherently lower valuations attributable to the parts manufacturing sector on BYD's stock performance. But with its sales mix rapidly shifting to an auto-dominant stance, which alongside expanding auto sales growth is likely to aid further gross profit margin expansion through scale, we see BYD’s potential for an upward valuation re-rating from current levels.

BYD 2022 Annual Report

This prospect is further complemented by BYD’s introduction of new sub-brands aimed at the premium segment as well as its rapidly expanding international strategy, which will enable TAM expansion and drive further volumes and scale to the broader business.

Given BYD’s currently leading fundamental performance as the largest manufacturer of BEVs and second largest manufacturer of EV batteries, as well as its prospects of maintaining a sustained profitable growth trajectory, the stock warrants a higher multiple in line with the industry average. Even at the blended EV and battery manufacturing P/S multiple of 1.9x, BYD's stock shows upside potential of more than 70% towards $52.

Macroeconomic Factors to Consider

In addition to valuation considerations on a relative basis to its peers, we believe BYD is also well-positioned to take advantage of an impending shift in macroeconomic factors in favour of Chinese equities. Admittedly, Chinese equities have taken a toll in recent years, burdened by significant discounts attributable to their elevated geopolitical, regulatory and macroeconomic risk exposures. However, we see several potential near-term tailwinds that could alleviate pressure on Chinese equities, particularly BYD given its strong underlying business fundamentals:

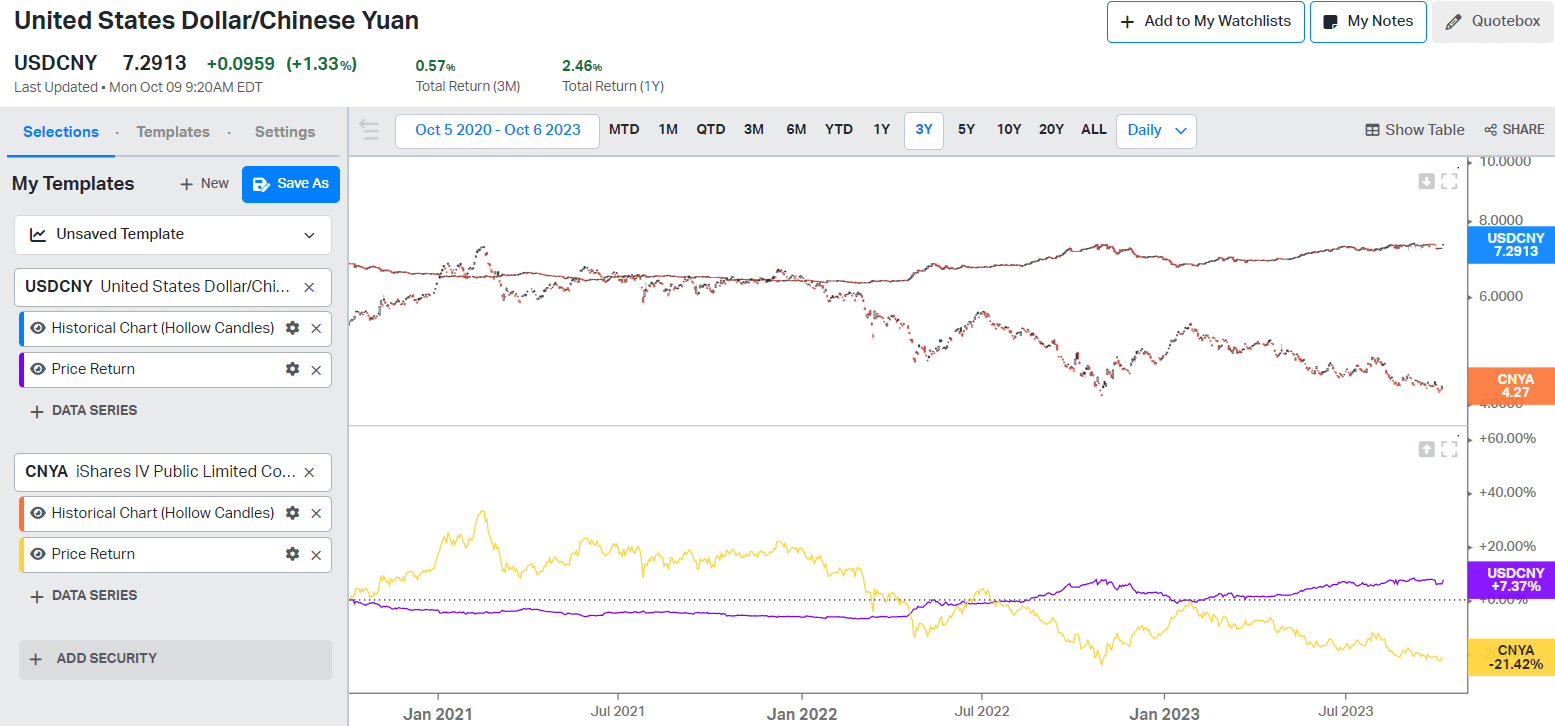

Moderating yield and dollar strength: Following Fed Chair Jerome Powell’s reaffirmation on policymakers’ support for a “ higher for longer ” rate environment, alongside recent economic data that continues to portray resilient financial conditions, the 10-year Treasury yield has surged towards 16-year highs of nearly 4.9% last week. The rising yield has generally incentivized demand for the dollar over the past year, given the appeal of returns on U.S. Treasuries relative to the sovereign debt of other countries, including China.

Specifically, the U.S.'s latest monetary policy tightening cycle has led to the largest “ yield differentials ” between American and Chinese sovereign debt. Historically, the yield on China bonds has led that of U.S. Treasuries. But the tides turned following the Fed’s latest rate hike cycle, which clashed with Beijing’s need to loosen its monetary policy in an attempt to save China from its post-pandemic economic slump. The yield gap on 10-year notes issued by the world’s two largest economies, with U.S. Treasury in the lead, has reached a 16-year high of more than 160 bps over the summer, and now exceeds 200 bps. This has accordingly weighed on the performance of the yuan as the dollar strengthens. And the yuan’s underperformance (or the dollar’s strengthening) has historically been correlated to weaker performance in Chinese equities – equities remain the most popular asset class in China, and the yuan’s weakening has largely made it more expensive to partake in their growth prospects.

{kind=link}

However, with the U.S. 10-year yield repeatedly contesting, yet failing to breach the 5% threshold in recent weeks, markets are likely not buying into the Fed’s higher for longer narrative. This is in line with gradually weakening economic conditions, despite recent data that shows continued resilience in the labour market, which could potentially tip it into a downturn. While the timeline of an ensuing loosening of monetary policy remains uncertain, recent trends of resistance on the surging long-end Treasury yield underscore the market’s expectations for normalization towards lower levels within the near-term, and reflects relative investor optimism on what “higher for longer” potentially entails. This makes a potential near-term tailwind for the yuan, which could alleviate some of the adverse pressure on Chinese equity valuations and unlock pent-up gains in BYD's stock, underpinned by its fundamental outperformance over the past year.

Diminishing leveraged trades: The potential for normalizing Treasury yield could also discourage net carry trades. Specifically, traders have been increasingly shorting Chinese equities over the past year, not only because of their relative risk exposures but also because of the favourable mathematical set-up of the trade. The differential between surging Treasury yields and fees paid on shorts have resulted in a positive net carry, which makes the downside bets on Chinese equities a profitable undertaking. But expectations for normalizing Treasury yields could potentially eradicate this incentive, and unleash greater volatility, and potential short squeezes, to markets – particularly Chinese equities like BYD, which have been heavily shorted over the past year.

Benefits of the base effect: The compressed Chinese equity valuations continue to reflect their exposure to ongoing macroeconomic headwinds in the region. However, economic performance is likely to start lapping an easier prior period comparison relative to the impact of a high base felt over the past year.

This is in line with improved spending , albeit modest, relative to pre-COVID levels observed over China’s latest Golden Week holiday in celebration of the establishment of the PRC. With the market’s focus still being on the prospects of stimulus to lift the Chinese economy from the impact of a broader property slump and soft post-pandemic consumer spending growth, the impending shift towards a more favourable base effect in the coming months has likely yet to be priced into the cohort’s valuations. This could be another potential near-term tailwind for underperforming Chinese stocks underpinned by robust fundamentals like BYD.

The Bottom Line

BYD continues to demonstrate itself as a key driver of consolidation in the global EV market. Not only is it going after incremental share gains in the Chinese EV market with two new premium sub-brands, but the company is also looking to capture expanding opportunities overseas while partaking in competing rivals’ prospects by being a key component supplier at the same time. BYD also boasts the competitive advantage of executing its long-term growth roadmap at a profitable pace, underpinned by successful vertical integration of production at scale.

From a valuation perspective, BYD is also likely on the verge of an inflection point. We see prospects of a potential upward valuation re-rate given the rapid shift in sales mix towards higher-margin vehicle production and sales. Despite the overhanging headwinds facing Chinese equities, BYD has, time and again, demonstrated durable competitive advantages capable of driving a sustained profitable growth trajectory. BYD’s fundamental strength remains a key accretive factor to the stock’s valuation prospects in our opinion, which makes it well-positioned to realize pent-up gains when broader market conditions permit.

For further details see:

Major, Yet Subtle BYD Developments Investors Haven't Paid Attention To