TUSK - Mammoth Energy Services: The Little Frac Company That Could Sort Of

2023-11-30 08:30:00 ET

Summary

- Mammoth Energy Services has received payments from PREPA for hurricane work in Puerto Rico, prompting a fresh look at the company.

- The company has found a niche in the OFS industry and may see better days ahead, depending on the weather.

- TUSK's Q3 2023 results showed a decrease in revenue and net income compared to the same quarter last year.

- TUSK is rated a Hold.

Introduction

I was reminded of Mammoth Energy Services ( TUSK ) in reviewing another company and thought I take a peek. We have covered the company previously and here's a link to past articles. I've been mostly negative on TUSK, once predicting it would go out of business. TUSK has managed to stay afloat and has actually begun receiving payments from PREPA for the hurricane work performed by its industrial services division in Puerto Rico a few years back. I had written this possibility off entirely, and that alone prompts a fresh look at the company.

{kind=link}

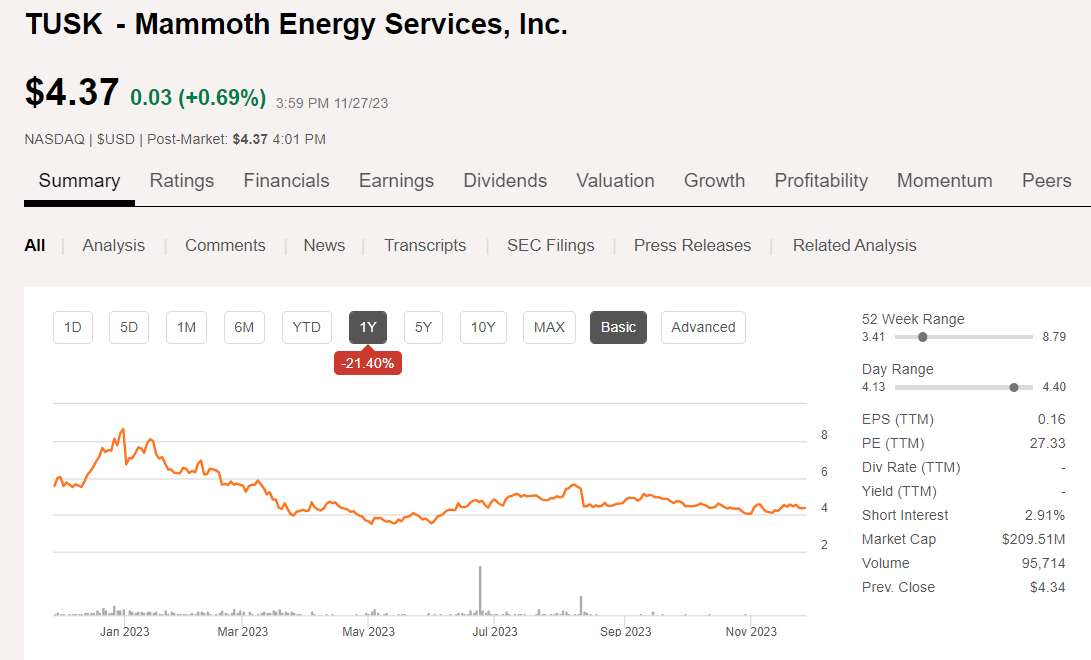

Since March, the company has traded in a fairly tight range between $4 and $6.00 per share and is currently in the lower portion of that range. An accomplishment of sorts when you consider the whirlwind that has beset the general OFS industry over the same period. Clearly, the company has found a niche, and may in fact see better days, weather permitting.

On technicals, the stock is at its lower support line and just below its 200-Day SMA. There was a big~3 mm share, move out of the stock in late June at 30X its normal trading volume, just before it announced that first $10 mm payment from PREPA. Institutions and hedge funds hold 82% of the company and have been buying in recent times. Wexford Capital remains the largest holder with 47% of the company. It's also one of the largest lenders as will be discussed in the quarterly review.

With that preamble, let's review the thesis for TUSK and the Q-3 call to see what guide posts we might uncover.

The thesis for TUSK

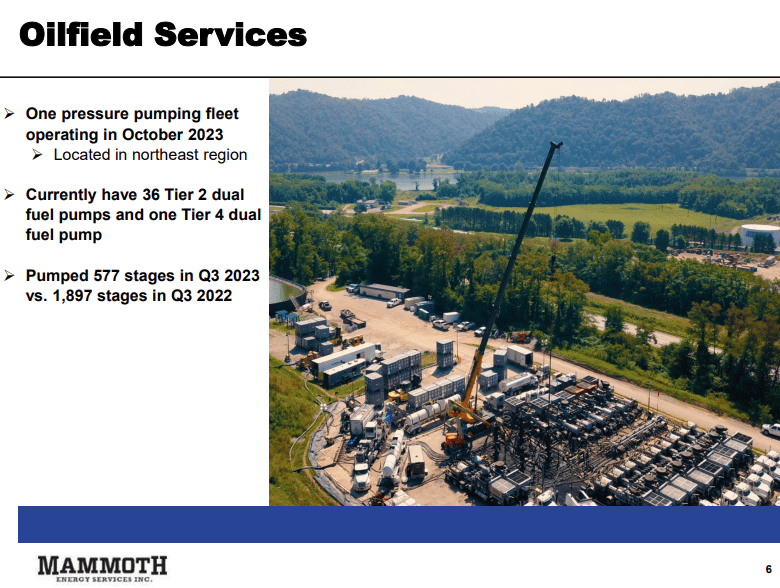

TUSK is a play on a niche fracking company supplying pressure pumping and proppant services. I am going to suggest the company's clientele list is price sensitive and fairly narrow as much of the company's 6-fleets is Tier 2 Dual Fuel, and runs a lower gas to diesel blend than higher rated Tier 4 Dual Fuel engines. If TUSK is to be a long-term player, the Tier 2 units will need to be upgraded to Tier 4, and that will take money - probably $1.5-2.0 mm per unit. Money that's not currently being generated by the business. The company's $18 mm capital budget has no provisions for these upgrades at present.

TUSK completion services (TUSK)

{kind=link}

Arty Straehla, CEO, comments on the trend in the fracing business and the outlook for 2024-

Despite the softness we've experienced this year, we are now seeing signs of increasing completion activity as we hold discussions and plan for 2024 with our customers. This is helping to improve our line of sight for the next few quarters, and we are encouraged by what we are seeing. We expect this trend to improve fleet counts in 2024.

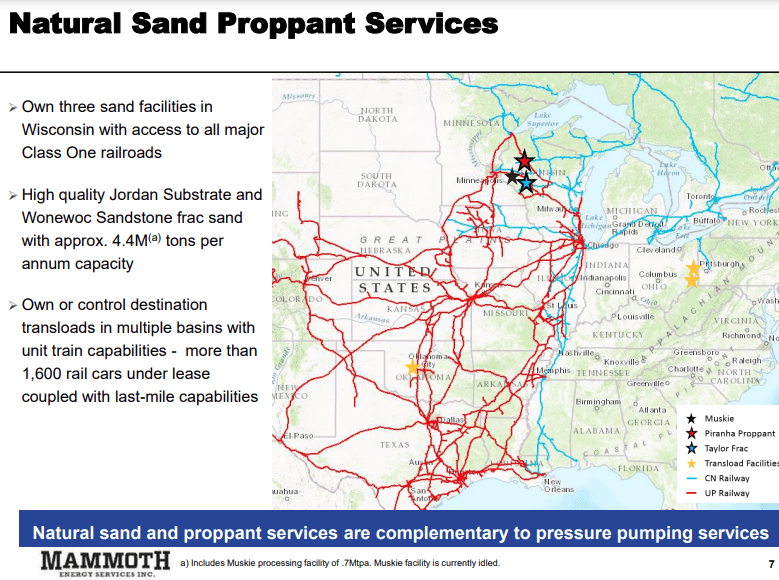

The company also participates in the fracing proppant business through a series of mines in Wisconsin with access to rail. These supply a high grade (high quartz) material that has superior sphericity and crush strength. The three mines Mammoth operates have a nameplate capacity of 4.4 mmpta.

TUSK proppant footprint (TUSK)

{kind=link}

Currently, only two facilities are operating as Mammoth's requirements recently are far less than their capacity with only 352K tons sold in Q-3.

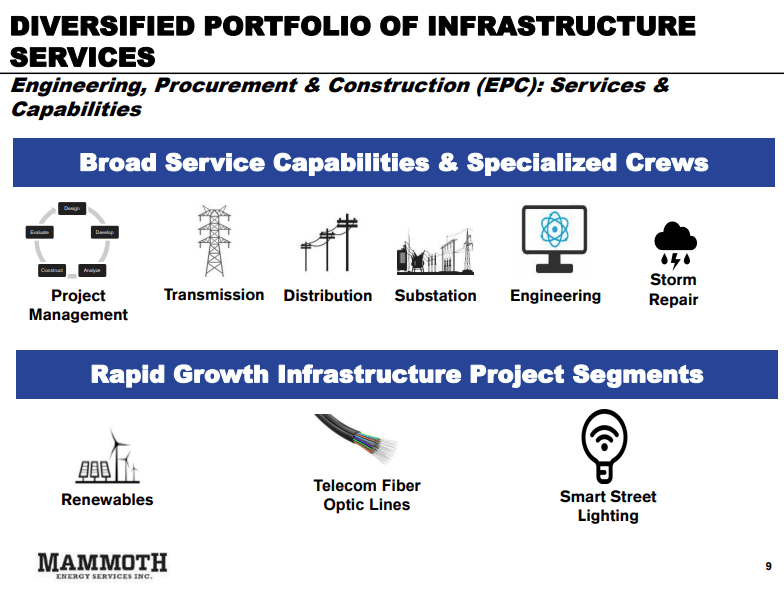

Finally, Mammoth has an industrial services sector that has grown over the years and is a likely beneficiary of work related to the build-out and ramping up of the electrical grid to support Inflation Reduction Act goals.

TUSK industrial portfolio (TUSK)

{kind=link}

Arty Straehla, CEO of TUSK, comments on the growth potential for the industrial sector-

In our infrastructure segment, we continue to expect improved funding for projects created from the Infrastructure Investment and Jobs Act as those dollars are expected to flow through into increased bidding activity in late 2023 and into 2024, especially in the fiber and substation business.

The PREPA play

A lot of ink has been spilled on TUSK's very tardy PREPA bill, and I am not going to add a great deal to it now. Please give my older articles a read if you desire greater immersion in this topic. What's relevant now is TUSK is starting to receive significant payments on this debt. That's significant as I had completely discounted this eventuality in previous reports. Live and learn, I suppose. In the second and third quarters of this year, TUSK has received $22.1 mm past due billings, with $394 mm remaining. Here are Straehla's comments regarding the status of the PREPA payments-

While we were pleased to have received some payments from PREPA, they have still only paid a portion of what is owed and a fraction of what FEMA has made available to PREPA for the work performed by Cobra. Cobra’s work has been affirmed by FEMA and numerous independent reviewers. However, as of today, we are still owed over $394 million by PREPA and we will continue to pursue payment for that work we completed.

With the recent success, I give a lot more credence to them, eventually collecting the full amount of this debt, than I once did. We will even model it in when we take a stab at an appropriate price for the company.

Q-3, 2023

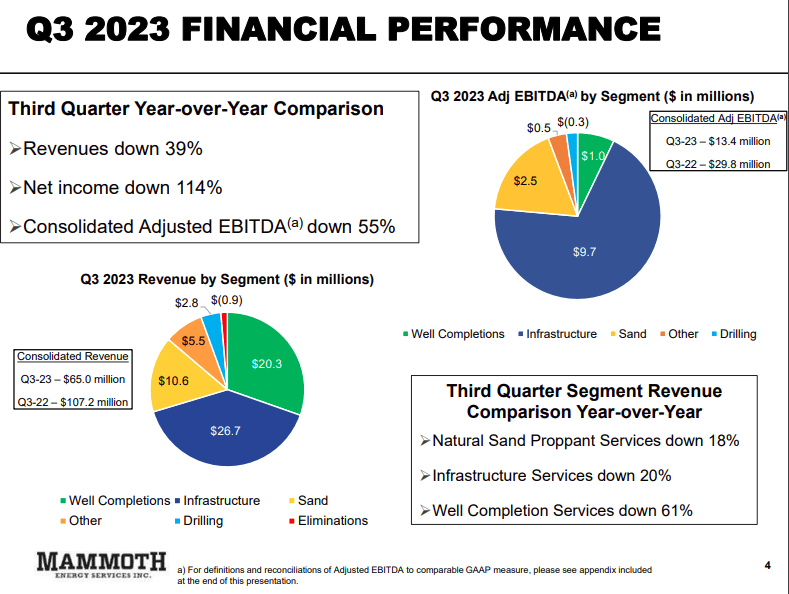

Mammoth’s total revenue during the third quarter of 2023 came in at $65 million compared to $107.2 million during the same quarter last year. Well Completions contributed $20.3 mm of that amount. Their sand division sold approximately 352,000 tons of sand during the third quarter of 2023, compared to 341,000 tons of sand during the same quarter last year. The average price for sand sold during the third quarter of 2023 was approximately $30.18 per ton, compared to $29.95 per ton during the same quarter last year.

Mammoth Financials, Q-3 2023 (TUSK)

{kind=link}

The Infrastructure Services Division contributed revenue of $26.7 million for the third quarter of 2023 compared to $33.3 million for the same quarter last year.

Their net loss for the third quarter of 2023 was $1.1 million, compared to net income of $7.7 million for the same quarter of last year. Adjusted EBITDA was $13.4 million for the third quarter of 2023, a decrease compared to the $29.8 million from the same quarter of 2022.

CapEx for the third quarter of 2023 was approximately $4.7 million, and the company expects to operate within the reduced CapEx budget of $18 million for 2023.

Selling, general and administrative expenses totaled $10.4 million during the third quarter of 2023, compared to $9.7 million for the same quarter of last year. This increase is primarily the result of certain legal fees associated with the work they performed in Puerto Rico.

As of September 30, 2023, TUSK had cash on hand of $10.5 million and debt of approximately $69 million. Their total liquidity was approximately $21.5 million. The company successfully completed the refinancing of its credit revolver facility last month, with Fifth Third Bank. That combined with the Wexford 5-year $45 mm term loan is expected to secure Mammoth's liquidity for the next five years.

Company filings

Risks for TUSK

I see one risk as being related to their size and the age of their equipment. It hasn't been generating sufficient income to offset capex involved in its maintenance. That is problematic, particularly as the Patterson-UTI ( PTEN )/NexTier (NEX) combination is strong in this area.

Another is their geographic focus in the Northeast, which is leveraged to gas. To be fair, this risk also has an upside with the company standing to benefit from higher gas prices, if and when they should arrive. We've made a case for them moving into the mid-$3s from weather and LNG exports , but the current overhang in storage keeps pushing this to the right, as we have seen.

Your takeaway

It would be hard to put a buy sign on TUSK at the present time. I looked at the Q-3 reports for two of the biggest North East drillers, EQT Corp. ( EQT ) and CNX Resources ( CNX ) for signs that there was going to be an activity ramp in the Marcellus/Utica basin that could possibly benefit TUSK. I didn't see that. Both EQT and CNX are keeping production targets flattish for 2024.

TUSK might be a bet for an activity bump in the case of a harsh winter. It rallied to over $8.00 per share in January of this year, so the precedent has been set. Stronger gas prices would be the stimulus for a rally in TUSK. All of that noted, TUSK rates a hold at current levels.

Options might be the safe way to play optimism in TUSK, calls in May were pretty cheap for adventurous souls.

For further details see:

Mammoth Energy Services: The Little Frac Company That Could, Sort Of