VLO - Marathon Petroleum Still A Buy For The Long Haul

2024-01-02 10:30:25 ET

Summary

- Marathon Petroleum Corporation owns significant US oil refining capacity and benefits from high barriers to entry in the industry.

- The company has a generous stock buyback program, healthy earnings from midstream operations, and exposure to lower-cost Canadian crude.

- Despite government policies favoring electric vehicles, consumers are still preferring hybrids and combustion engines, which benefits Marathon Petroleum's refining operations.

Marathon Petroleum Corporation ( MPC ) owns 2.9 million barrels per day ((BPD)) of US oil refining capacity in 13 refineries , much of a well-integrated midstream partnership, and 60,000 BPD of renewable diesel ((RD)) capacity. It benefits from the barriers to entry of high capital costs and the technical complexity of refining processes.

Although its stock price has gained 22% since my last analysis, I continue to recommend Marathon Petroleum as a buy. It has a very generous stock buyback program ($9.3 billion of firepower), healthy earnings from its midstream operations, good exposure to lower-cost Canadian crude, and profitable US refining operations that are competitively advantaged compared to those in Europe.

Investors should not confuse Marathon Petroleum with Marathon Oil Corporation ( MRO ) with which it was once integrated. MRO's business is upstream exploration and production.

Macro

The primary focus is on economic signals of recession (or not) and the Federal Reserve's interest rate policy-specifically, whether it will make cuts in 2024.

Oil prices have trended softer. In a few months, preparation for gasoline season, a time of key refining profitability, will ramp up. Moreover, US oil production is at an all-time high of 13.3 million BPD. For context, in 2005 US oil production fell as low as 5.0 million BPD. US oil refining capacity is 17.7 million BPD. The gap between production and refining is filled by oil imports.

But, lost in this is after a big 275-million-barrel sell-down from the US Strategic Petroleum Reserve, there is a far smaller SPR supply cushion. This could lift crude prices and is yet another one of the Biden administration's policies directed toward stifling all hydrocarbon supply and demand.

Still, contrary to US government policy, consumers are preferring hybrids to electrics, and EVs are a hard sell though the combustion engine phaseout remains a policy goal in many US states and Western European countries.

{kind=link}

Oil Prices and Refining Profitability

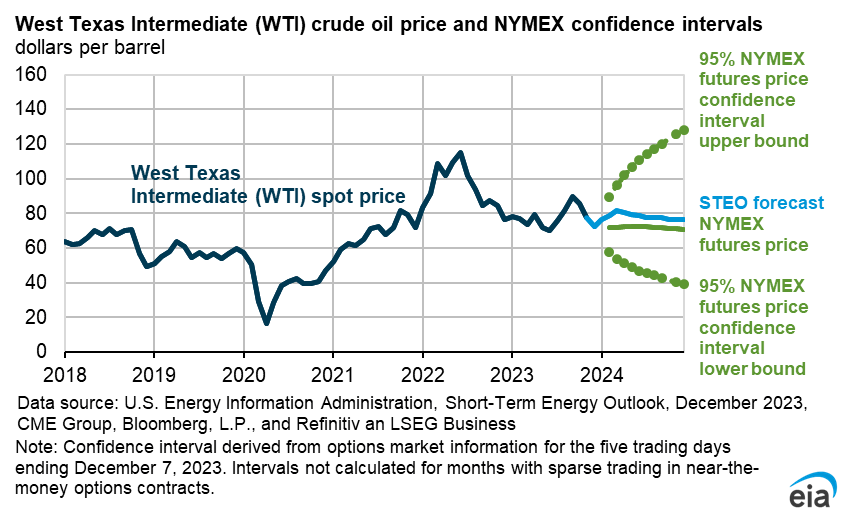

As the EIA's most recent short-term outlook shows, oil prices are expected to drift down in 2024.

On December 29, 2023, the closing NYMEX futures oil price was $71.65/barrel for WTI at Cushing, RBOB gasoline was $2.11/gallon (or $88.62/bbl), and diesel/heating oil was $2.53/gallon (or $106.26/bbl). All are for February 2023 delivery.

A recent price of WCS or West Canadian Select, one of Marathon's important crude feedstocks, was $21/bbl lower than WTI.

Natural gas prices are also lower than a year ago. Natural gas is a refinery fuel and so also a cost, although not as key as oil feedstock.

The crack spread is defined as three barrels of crude subtracted from the sum of 2 barrels of gasoline and one of distillate, and the specific crude used for this calculation is WTI-Cushing. The trend in the 3-2-1 crack spread, a measure of refining profitability, is shown below, with a significant drop in 4Q23.

energystockchannel.com

Third Quarter 2023 Results and Guidance

Because much of its midstream is contained in separately traded partnership MPLX LP ( MPLX ) refining is MPC's main operational focus. Marathon sells petroleum products to wholesale customers, to the Speedway business segment, and to independent retailers operating under the Marathon, Arco, and several other brands.

In the third quarter of 2023 , MPC reported net income of $3.3 billion or $8.28/share. This compared to a net income of $4.5 billion or $9.06/share for 3Q22. Adjusted EBITDA for the quarter was $5.7 billion compared to $6.8 billion for 3Q22.

MPLX increased its distribution by 10%. As majority owner, Marathon Petroleum expects to receive $2.2 billion annually from MPLX.

Marathon Petroleum increased its own quarterly dividend 10% to $0.825/share.

Investors should note that in 3Q23, the company returned $297 million to shareholders via dividends but nearly 10x more, or $2.8 billion, in share repurchases.

Projected 4Q23 crude refinery throughputs were 2.6 million BPD, or 90% of capacity. This is divided into 1.1 million BPD in the Gulf Coast region, 1.0 million BPD in the MidCon region, and 0.5 million BPD in the West Coast region.

The projected sweet/sour mix of crudes for 4Q23 was 55% sweet/45% sour.

In terms of strategy, Marathon has said it will not bid for the Citgo refining assets.

In its 3Q23 investor call, the company noted its exports to Latin America and the Caribbean have been strong.

Competitors

Marathon Petroleum is headquartered in Findlay, Ohio. It competes with virtually every US refiner. At the beginning of 2023, total US operable and operating refining capacity was 17.7 million BPD , so Marathon Petroleum's share is 16.4%, similar to Valero Energy Corporation's (VLO) US refining capacity.

Barriers to the US refining industry remain high due to siting issues; the large, fixed cost of capital assets; and a regulated, consumer-facing gasoline (and jet fuel and diesel) business that is highly competitive and much-scrutinized. All of Marathon Petroleum's 2.9 MMBPD of oil refining capacity is domestic.

In renewable diesel, MPC's Dickinson, North Dakota plant has been operating since 2021 and has capacity of 184 million gallons/year or 12,000 BPD. Startup of the Neste joint venture retrofit of its Martinez, California RD plant will add 730 million gallons/year or 47,600 BPD. Together the two will have capacity of 914 million gallons/year (about 60,000 BPD) of RD capacity or roughly a quarter of the US total.

Thus, expected US RD capacity equals 1.5% of US oil refining capacity.

Governance

On December 28, 2023, Institutional Shareholder Services ranked Marathon Petroleum's overall governance as 7, with sub-scores of audit (9), board (3), shareholder rights (9), and compensation (1). In this measurement, a score of 1 represents lower governance risk and a score of 10 represents higher governance risk.

As of September 2023, Marathon Petroleum's ESG ratings from Sustainalytics were "high" with a total risk score of 30 (71st percentile). Component parts are environmental risk 17.1, social 8.1, and governance 5.3. Controversy level is 3 (significant) on a scale of 0-5, with 5 as the worst.

On December 15, 2023, shorts were 2.7% of the floated stock. Insider ownership is a small 0.3%.

The company's beta is 1.49, representing steeper volatility than the market but reflecting variability in refining margins as a function of both crude oil prices (feedstock costs) and product prices.

On September 29, 2023, much of Marathon Petroleum's stock was held by institutions, some of which represent index fund investments that match the overall market. The five largest institutional holders were Vanguard (9.9%), BlackRock (8.3%), State Street (7.1%), activist firm Elliott Investment Management (2.9%), and Fidelity-related Geode Capital Management (2.0%).

Elliott Management urged Marathon Petroleum to restructure a few years ago, leading the company to profitably sell its retail operations and increase returns to investors. Elliott is now taking the same approach as MPC competitor Phillips 66 ( PSX ).

BlackRock and State Street are signatories to the Net Zero Asset Managers initiative, a group that, as of December 4, 2023, manages $57 trillion in assets worldwide and which limits hydrocarbon investment via its commitment to achieve net zero alignment by 2050 or sooner.

In late December 2023, executive vice president and chief financial officer Maryann Mannen was named president of MPC. Prior president Michael Hennigan will continue as MPC's chief executive officer. He will also lead the general partner of MPLX.

Logistics Partnership MPLX

On September 30, 2023, Marathon Petroleum owned 64.6% of the limited partnership units of $36.8 billion master limited partnership, MPLX LP ((MPLX)). Assets are primarily pipelines and terminals. While the partnership yields 9.3%, the attractiveness of partnership units is specific to an investor's tax situation and is not evaluated in this analysis.

A consideration is that Marathon Petroleum operationally integrates the partnership's midstream assets with its refining assets. And, since Marathon Petroleum owns 64.6% of MPLX, it receives large unit payouts.

Financial and Stock Highlights

Marathon Petroleum's market capitalization at the December 29, 2023, stock closing price of $148.36/share is $56.3 billion, a bit below last year's market capitalization of $57.1 billion due to a smaller number of shares at a 22% higher price.

The 52-week price range is $104.32-$159.65 per share, so the closing price is 93% of the one-year high. The company's one-year target price is $166.27/share putting the closing price at 89% of that level. Put another way, there is a 12% upside to the average one-year target price.

Trailing twelve months' earnings per share ((EPS)) is a quite extraordinary $26.51 reflecting very strong refining margins and the effect of share buybacks.

The average of analysts' estimated EPS for 2023 is $22.06 and for 2024 is $15.31, for a price-earnings ratio range of 6.7-9.7. MPC has beat analysts' EPS estimates by $0.35-$0.98/share in each of the last four quarters .

Trailing twelve-month returns on assets and equity are both excellent at 11.2% and 38.7%, respectively.

On September 30, 2023, the company had $57.2 billion of liabilities including long-term debt of $26.5 billion, and $90.0 billion in assets giving Marathon Petroleum a liability-to-asset ratio of 64%.

The company's $26.5 billion total debt is divided into $6.9 billion for MPC and $20.7 billion for MPLX.

Trailing twelve months' operating cash flow was $17.4 billion and levered free cash flow was $12.2 billion.

During October 2023, Marathon Petroleum increased its dividend 10% to $3.30/share, a yield of 2.2%. It also announced another $5 billion share repurchase authorization in addition to the $4.3 billion remaining on its existing authorization. Neither of these has an expiration date.

The company's mean analyst rating is 1.9, or "buy," from the nineteen analysts who follow it. At least one analyst rates it as fairly valued.

Marathon Petroleum will report fourth-quarter and full-year 2023 results on January 30, 2024.

Notes on Valuation

Book value per share is $67.00, less than half its current market price, indicating positive investor sentiment.

The EV/EBITDA ratio is a small 3.7, well below the preferred ratio of 10 or less and suggesting MPC stock is a bargain.

Positive and Negative Risks

Marathon Petroleum's primary risk is standard margin risk, that is, the difference between feedstock costs and product prices. Margins have reverted toward the mean after several previous strong quarters.

The company's renewable diesel production faces considerable competition from other refiners, a limited market, and for the Martinez plant, a delayed ramp-up to full capacity.

Inflation generally is a negative risk, as is the possibility of a recessionary demand drop or an equity market downdraft.

Although refiners face general and region-specific (especially the USWC) regulatory pressures from those states prohibiting future sales of gasoline-powered vehicles after 2035--effectively requiring electric vehicle sales only--whether the shortage of renewable-fueled electricity alters this deadline remains to be seen.

Moreover, customers have not flocked to EVs at the same pace as some had hoped.

Recommendations for Marathon Petroleum

Marathon Petroleum has good cash flow, particularly from its midstream partnership. While it has an affordable forward price/earnings ratio of 9.7, its dividend yield of 2.2% is not large. However, generous stock repurchases (up to $9.3 billion still authorized) have and are likely to continue to boost overall yields to investors.

More broadly, low SPR crude supply but high US native oil production are countervailing cost factors in oil refining. Investors should nonetheless be aware that refiners' margins have shrunk and are expected to continue to revert to the mean from higher levels in the last few years.

Of interest to some, this time of year is ahead of gasoline season, so maybe a lower, more value-oriented point in the price cycle.

I recommend Marathon Petroleum Corporation as a buy to energy investors and own shares myself.

Marathon Petroleum

For further details see:

Marathon Petroleum Still A Buy For The Long Haul