SSNLF - March'23 Semi-Cap Recap

2023-03-14 08:45:22 ET

Summary

- The semiconductor industry is experiencing a downturn due to a decrease in consumer demand, high inventory levels resulting from that and geopolitical tensions between China and the US.

- The long-term case for semiconductor equipment manufacturers remains strong, driven by the ongoing digitalization of. well, everything.

- Geopolitical headwinds in the short term ought to become tailwinds as excess capacity is created.

Semiconductor Demand Update

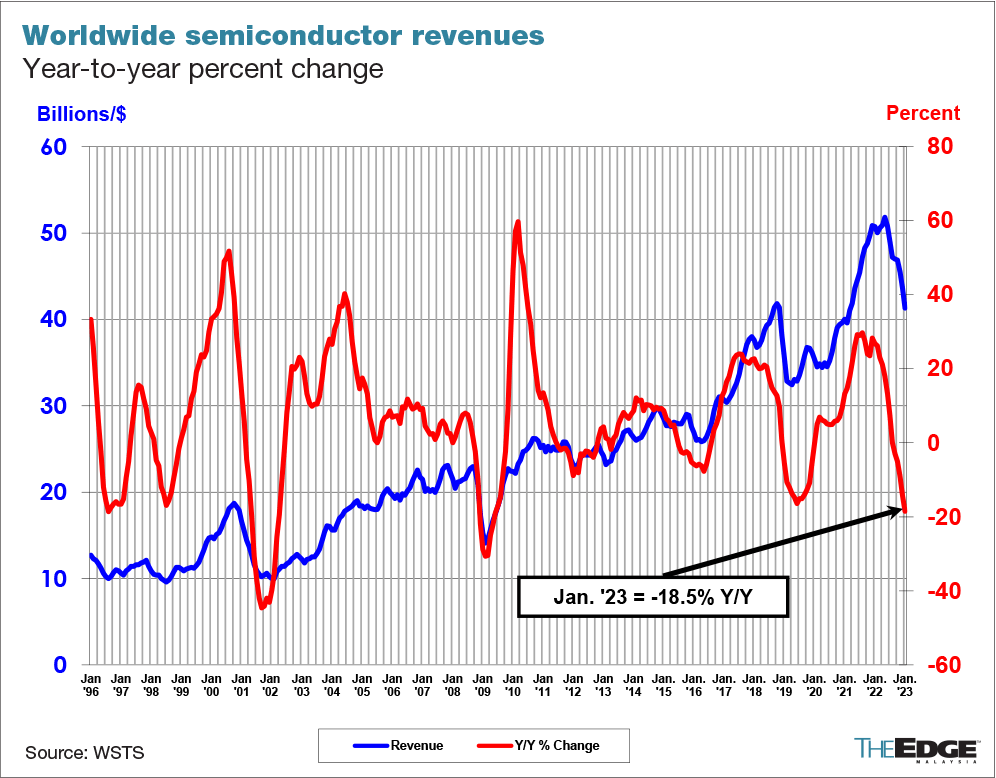

Demand for semiconductors has seen better days.

Sales this past January were down 18.5% year-on-year and 5.2% sequentially, as reported by the SIA. This lackluster performance is to a large extent attributable to soft market demand in the consumer sector, to inventory build-up, especially in memory, and to the very sharp decline in Chinese orders.

{kind=link}

The Edge

Demand for memory semis had been declining for a while, with DRAM revenues down sequentially by over 30% in Q4’22, according to TrendForce , and with the inventory levels of Korean chipmakers at a 26-year high .

DRAM Revenue Evolution (TrendForce)

A similar sequential decline is presently occurring in logic and foundry, with TSMC ( TSM ) revenues down 18% M-o-M this February and expected “to be between USD 16.7 billion and USD 17.5 billion, representing a 14.2% sequential decline at the midpoint” in Q1. This too is driven by ongoing end-market demand softness and further inventory adjustments at TSMC’s customers.

Causing further stress on chip demand, in late 2022, the Biden administration announced export control measures aimed at limiting China’s access to US AI and semiconductor technology. These effectively deny China access to leading-edge chips, as well as the software and the equipment that are needed to produce them. The new policy also prohibits U.S. individuals, including Green Card holders, and corporations from facilitating such exports or transferring any relevant technological know-how. This has led to a 27% decline of semiconductor imports in China in the February 2023 YTD period.

This market softness has led chipmakers to revise their capex plans downwards. Over the past several months, most memory players have reduced their capex plans, with SK Hynix going as far as stating that they would halve their capital expenditures in 2023 . Logic seems somewhat more resilient. In their most recent earning calls, TSMC announced that they expect demand to recover in the second half of 2023 and that they would "only" trim capex from $36.3 billion to a $32-36 billion range.

The (Long-Term) Case for Semiconductor Equipment

In line with their customers, wafer fabrication equipment (WFE) manufacturers have given mixed guidance, erring towards bearish territory for the March quarter. ASML , with its high exposure to logic and a large order backlog, expects revenues to come in within the Q4’22 range, whereas LAM Research ( LRCX ), which is highly exposed to Korea and memory expects quarterly sales to drop from $5.3 billion to a $3.5-4.1 billion range. One thing they do agree about is that with China accounting for anywhere between 15% and 25% of revenues for most OEMs, the short-term impact of the export bans won’t be rosy . In aggregate, the sharp decline in China revenue, coupled with a soft macro backdrop, has most pundits agreeing that in 2023 we will see a slight contraction in the demand for semiconductors, and therefore semi capex and WFE.

Having said that, we must bear in mind that long-term growth in semis is rooted in enduring trends such as the steady expansion of computing across a broader set of applications and the reconfiguration of supply chains. And indeed, the recent recruitment announcements by TSMC , ASML and Applied Materials ( AMAT ) attest to a widespread belief among industry participants that the recovery will come sooner rather than later, and that companies need to have the right human capital in place to deliver.

In fact, casting the current malaise aside, the fundamentals for semi and semi-cap demand remain strong.

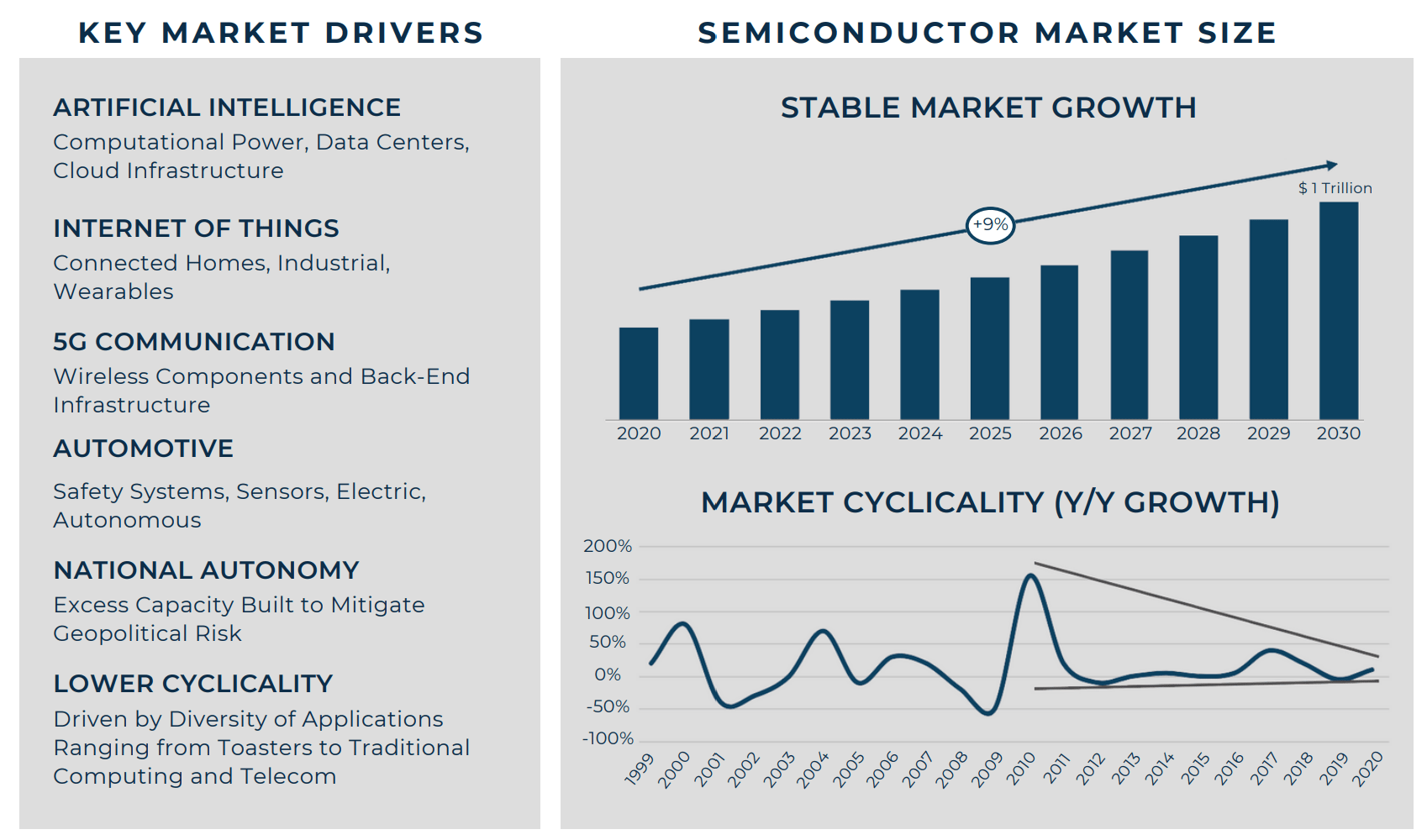

Semiconductors are the building blocks that enable most economic megatrends to take shape. Artificial Intelligence, Mobility, the Internet of Things and Smart Cities all rely on improved computing efficiency, or as I call it, the "semiconductorisation" of the economy. To illustrate with a popular example, Electric vehicles (EVs) generally require three times more semiconductors than internal combustion engine cars, due to the complex electronic systems needed for battery management, power electronics, electric motor control, etc. Additionally, EVs often require more advanced chips, such as silicon carbide (SiC) and gallium nitride (GaN), to achieve higher efficiency and performance. And that is not even taking into consideration the infrastructure that is required to power them.

In other words, the electrification of Mobility is enabled by semiconductors. The same is the case for Autonomous Vehicles, AI, the IoT and, in general, most economic megatrends. The snapshot below articulates some of the market drivers that are expected to drive semiconductor demand to the notorious $1 trillion projection by 2030.

{kind=link}

Self, AMAT

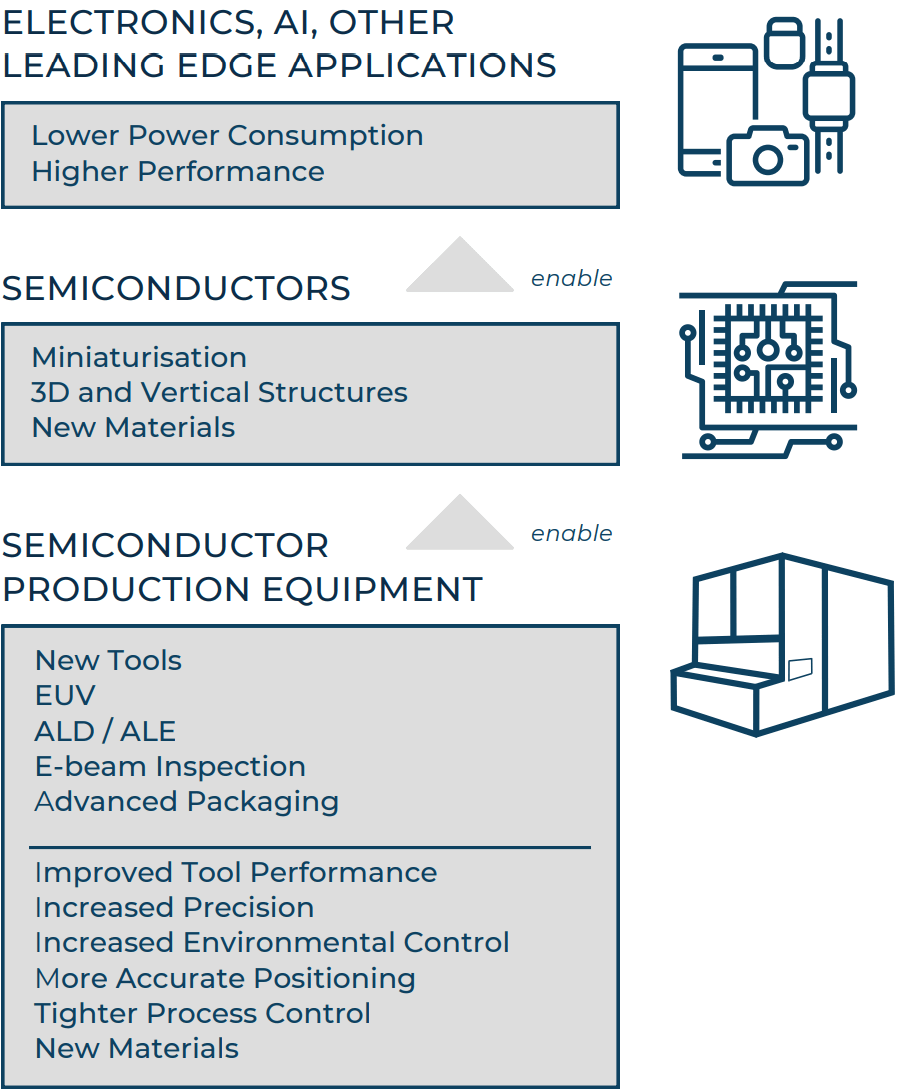

As demand for semiconductors grows, so does the demand for the tools that are used to produce them. Moreover, as semiconductors get smaller and more efficient, new and/or better semi-cap tools are needed to enable their development. Ergo, the growth and the technical development of semiconductors is dependent on the tools that are used to fabricate them, as illustrated below.

{kind=link}

Self

In addition to the ubiquity of chips driving demand for semi-caps, I also expect the current geopolitical landscape to benefit the sector immensely. The desire of governments to redistribute semi production globally, for reasons ranging from security to supply chain resilience, will generate excess capacity at an aggregate level. That capacity will be distributed between China on one hand and the rest of the world on the other, in the form of re-shoring (e.g., US, Germany) or friend-shoring (e.g., Singapore, Japan).

This increased, and possibly suboptimal, fab footprint will require more WFE than would have been necessary under the current semi supply chain configuration. To capture this demand, it is likely that semi-cap OEMs and other suppliers will follow their customers as they reshuffle their footprint. In fact, a number of announcements made in recent months hint that WFE OEMs are readying capacity to prepare for a surge in demand. Those announcements range from concrete capacity investments to more speculative exploration, especially by non-US domiciled OEMs:

- Towards the end of 2022, Applied Materials announced its “Singapore 2030” programme, which aims to invest $600 million in the red dot and create 1,000 jobs in the process.

- Around the same time, French materials supplier Soitec ( SLOIF , SLOIY ) announced its intention to invest €400 million to expand its capacity in Singapore .

- Tokyo Electron ( TOELF , TOELY ) has purchased land in Texas , presumably to start production in the vicinity of fabs currently under construction by Texas Instruments ( TXN ) and GlobalWafers.

- Laser and power source supplier Trumpf has initiated a $40 million extension of its Farmington, Conn. facility

- A delegation of suppliers to ASML , including VDL ETG, Neways and NTS Group, is currently touring Asia to identify prospective manufacturing bases outside of China. It is unclear whether ASML has any plans to expand its footprint in Asia beyond the current barebone setup in Taiwan.

For further details see:

March'23 Semi-Cap Recap