PXD - Matador Resources: Strong Q3 2022 Results Still Attractively Valued

Summary

- Matador Resources reported incredibly strong earnings, showing considerable growth across the board.

- The company's fourth quarter may come in a bit weaker than the third due to current energy market trends.

- The company has been aggressively paying down its debt and now has a remarkably strong balance sheet.

- The firm's midstream subsidiary is also performing well and positioned to generate record cash flow this year.

- The stock appears to be considerably undervalued relative to the market as a whole.

On Tuesday, October 25, 2022, Permian Basin-based independent exploration and production firm Matador Resources Company ( MTDR ) announced its third quarter 2022 earnings results. At first glance, the company's results were fairly solid as it beat the expectations of its analysts on both revenues and earnings. In addition, the company posted fairly substantial year-over-year growth in most measures of financial performance. It is perhaps not especially surprising that an energy company would do reasonably well given the significant increases that we have seen in energy prices over the past eighteen months. Obviously, Matador Resources benefited from this as well as growing production, indicating that the company is attempting to take advantage of today's high-price environment. There were many other things to like in this earnings report as well but despite all the good things right now, the stock remains very cheap. Thus, there could be an opportunity for an investor to take advantage of the situation and earn a profit.

As my long-time readers are no doubt well aware, it is my usual practice to share the highlights from a company's earnings report before delving into an analysis of its results. This is because these highlights provide a background for the remainder of the article as well as serve as a framework for the resultant analysis. Therefore, here are the highlights from Matador Resources' third-quarter 2022 earnings results:

- Matador Resources brought in total revenues of $840.928 million in the third quarter of 2022. This represents a 78.03% increase over the $472.351 million that the company reported in the prior-year quarter.

- The company reported an operating income of $483.274 million in the most recent quarter. This compares quite favorably to the $230.186 million that the company had in the year-ago quarter.

- Matador Resources produced an average of 105,214 barrels of oil equivalent per day during the reporting period. This represents a fairly large 16.86% increase over the 90,033 barrels of oil equivalent per day that the company produced on average last year.

- The company declared a dividend of $0.10 per share, double the level that the company had at the start of this year.

- Matador Resources reported a net income attributable to the common shareholders of $337.572 million in the third quarter of 2022. This represents a 65.78% increase over the $203.628 million that the company reported in the third quarter of 2021.

It seems certain that the first thing anyone reading these highlights will notice is that essentially every measure of financial performance showed improvement compared to the prior-year quarter. This is not exactly unexpected as the biggest cause of it is that energy prices were higher during the third quarter of 2022 than they were last year. We can see this quite clearly by looking at the prices that the company received for each unit of crude oil or natural gas that it sold:

| Q3 2022 |

| Q3 2021 |

| Realized Price, Crude Oil ($/bbl) |

| $91.69 |

| $58.43 |

| Realized Price, Natural Gas ($/mcf) |

| $7.55 |

| $6.05 |

It should be fairly obvious how this served to increase the company's financial performance. After all, the more money the company receives for each unit of product that it sells, the higher its total revenues unless its production drops significantly. That was certainly not the case with Matador Resources. In fact, while its production was down compared to the second quarter, it was quite a bit higher than during the corresponding quarter of last year:

Matador Resources

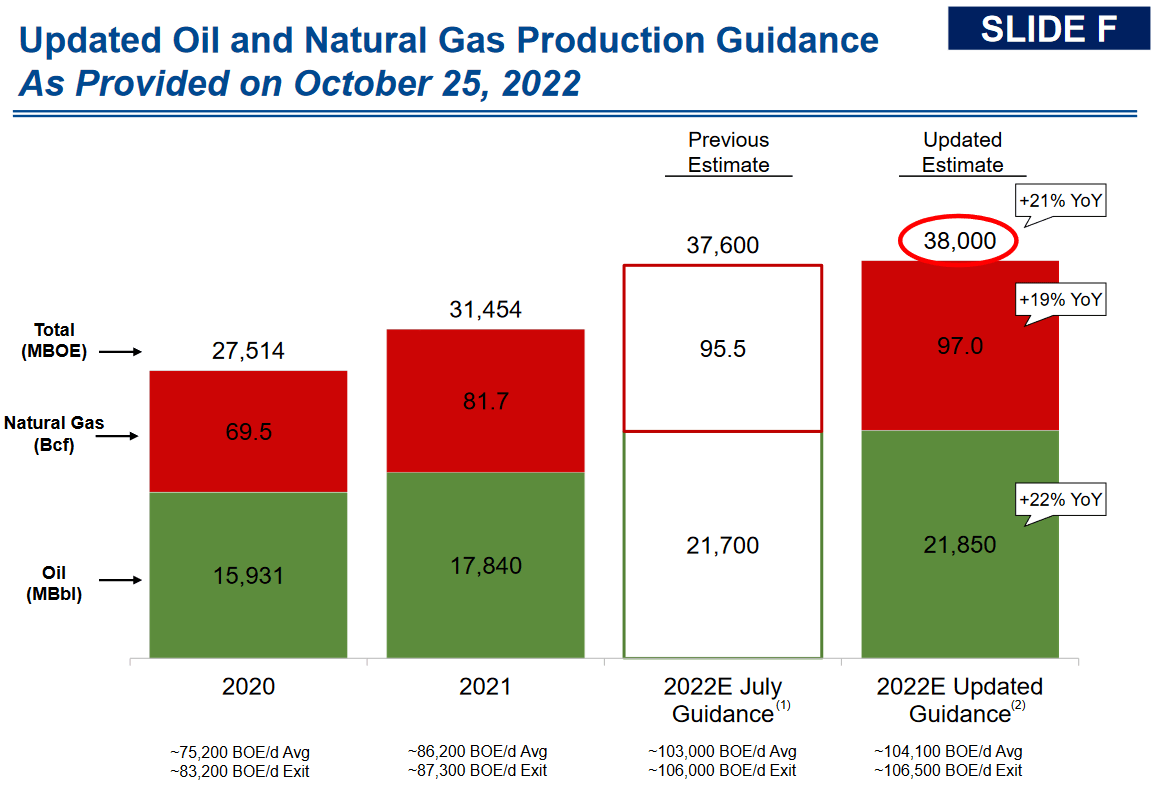

The decline in production quarter-over-quarter was somewhat disappointing, although Matador Resources did beat its guidance so that was certainly nice to see. The company did not provide a reason for the decline that was seen during the quarter but it was a small enough sequential decline to have been caused by just about anything, including things that are completely out of the company's control. We, therefore, do not really have to worry about it. Matador Resources stated in the conference call that it expects to increase its production by 1% in the fourth quarter of 2022 compared to the third quarter. That would be a slight improvement even though it would still be less than the company produced in the second quarter. Overall though, Matador Resources is going to beat the full-year production guidance that the company provided back in July:

{kind=link}

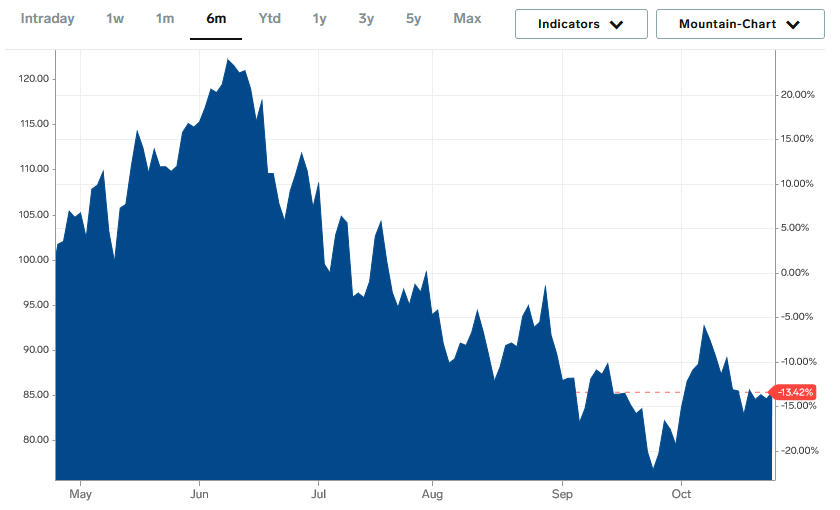

Unfortunately for Matador Resources, crude oil prices in the fourth quarter have not been especially cooperative. As we can see here, prices have been declining since June and have been hovering near six-month lows since the start of October:

{kind=link}

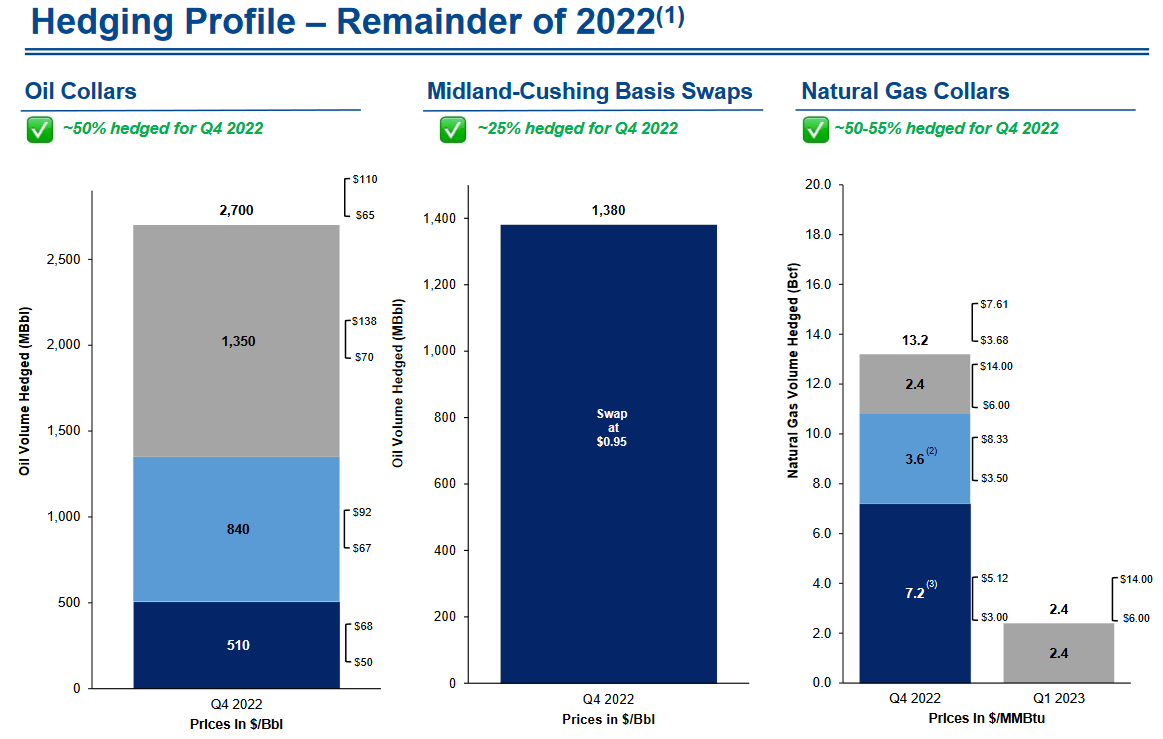

If this continues, as it probably will, the lower prices could offset the increased production over the remainder of the year and result in the company's fourth-quarter financial performance being somewhat worse than it delivered during either the second or third quarters of 2022. As is the case with many independent energy companies though, Matador Resources has some ways to protect itself against this situation. The primary way that it does this is by hedging its production. In short, the company uses derivative contracts such as forward and futures contracts to essentially lock in a selling price for its production. Depending on the basin, the company has 25% to 50% of its expected fourth-quarter crude oil production and 50% of its expected fourth-quarter natural gas production protected by these hedges:

{kind=link}

This is nice as it does provide Matador Resources with a certain amount of protection against declines in energy prices. Unfortunately, we can still see that a significant portion of its cash flow is still largely dependent on crude oil and natural gas prices. There may be some reasons to expect energy prices to fall, at least in the short term. One of the biggest reasons for this is the deteriorating economic conditions in the United States. In both the first and second quarters of 2022, the country saw its gross domestic product decline. This is the classic definition of a recession, although the government has not yet stated that it is one for political reasons. As I pointed out in a recent article , it seems likely that the same will be the case in the third quarter, which would be another indicator of deteriorating economic conditions. During recessions, Americans tend to cut back on driving, vacations, and many other activities that require the consumption of crude oil. Thus, the demand for crude oil declines, and this applies negative pressure on energy prices. With that said, President Biden also recently stated that the U.S. government will buy crude oil at a price of $72 per barrel to refill the Strategic Petroleum Reserve. This effectively created a floor on energy prices so we can be reasonably confident that crude oil will not fall below this price because of the buying pressure that the government's purchases would exert on supplies.

In various articles over the years, I discussed the financial problems faced by many independent shale operators. This is illustrated by the fact that prior to the COVID-19 lockdowns, the domestic energy industry was the largest issuer of junk debt . Matador Resources has been using some of its newfound good fortunes with today's high energy prices to fix its debt problems. During the past two years, the company has reduced its outstanding debt by $775 million:

{kind=link}

This is something that is very nice to see because debt is a much riskier way to finance a company than equity due to the fact that debt must be repaid. This is normally accomplished by issuing new debt and using the money to pay off the maturing debt. This can, however, cause a company's interest costs to increase following the rollover depending on the conditions in the market. In addition to this, a company needs to make regular payments on its debt if it is to remain solvent. Thus, any decline in cash flow could push a company into financial distress if it has too much debt. This is an especially big problem for energy companies like Matador Resources due to the volatility of commodity prices.

However, the company's debt does not appear to be much of a problem anymore. We can see this by looking at its leverage ratio, which is also known as the net debt-to-adjusted EBITDA ratio. This ratio essentially tells us how many years it would take the company to completely pay off its debt if it were to devote all of its pre-tax cash flow to that task. At the close of the third quarter, Matador Resources had a leverage ratio of 0.2x, which is not only a significant improvement over the 2.8x ratio that the company had back in October 2020 but it is in fact one of the lowest ratios in the energy industry. This is one of the big reasons why Matador Resources' credit rating was upgraded recently. The company is now a "BB-rated" company as opposed to simply a "B-rated" one. While it needs to continue performing well to become investment-grade, the vote of confidence from all three major credit rating agencies is very nice to see.

One unfortunate thing that we see in these results is that Matador Resources' production costs increased significantly. While this has been the trend since the second quarter of 2021, the increase was quite significant during this quarter:

Matador Resources

This is admittedly disappointing but it is understandable. Indeed, the whole industry has been seeing its costs increasing fairly rapidly despite years of efforts to reduce costs. The biggest reason for this is the same inflation that we have been suffering from as consumers. The energy industry uses a significant amount of steel and diesel fuel in their drilling and well completion tasks and prices of both of these products have been rising fairly dramatically. Despite the increase in costs, Matador Resources still generates incredibly high profit margins. During the quarter, it cost the company an average of $29.71 per barrel of oil equivalent produced. As oil prices remain substantially above that, it is able to generate substantial amounts of money. In fact, the company would still clearly be profitable if energy prices do indeed decline somewhat in the near future. This is something that any investor should be able to appreciate.

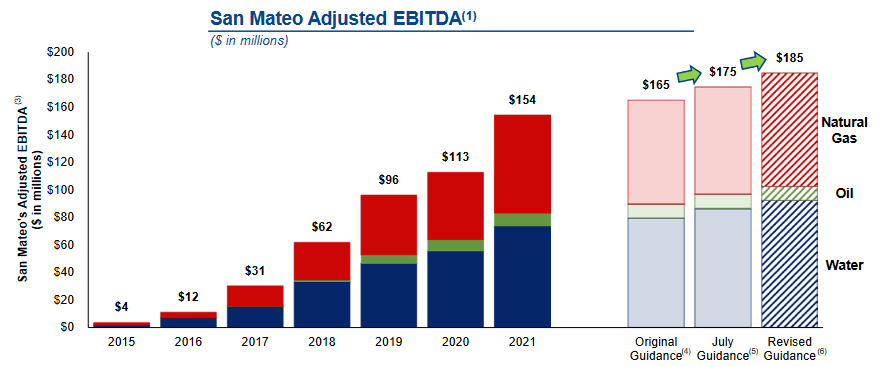

As I mentioned in previous articles on Matador Resources, the company is also part-owner of a midstream firm. This firm, San Mateo Midstream, operates crude oil, natural gas, and produced water gathering and transportation infrastructure networks in Eddy County, New Mexico, and Loving County, Texas. The company also owns the Black River natural gas processing plant in New Mexico. As is the case with any other midstream company, San Mateo Midstream makes its money from long-term contracts with its customers that are based on resource volumes, not on resource values. This proved to be a very profitable business model during the quarter as San Mateo benefited from higher volumes across its business than in either the previous quarter or the third quarter of 2021. Its produced water gathering system actually set a new volume record:

Matador Resources

Unlike many other midstream providers that are partially or fully owned by an upstream energy producer, San Mateo Midstream has several customers apart from Matador. This is nice because it results in new money coming into the overall corporate structure. San Mateo succeeded in getting a number of contracts from these outside customers during the quarter, which positions it for forward growth. That would be a continuation of the midstream company's historic growth trajectory:

{kind=link}

This benefits Matador Resources because the midstream company pays out its cash flow to the joint venture partners (Matador Resources and Five Point Energy). The more money San Mateo Midstream makes, the more money Matador Resources ultimately receives. The success that is seen here is thus another thing that should make any investors in the company quite pleased.

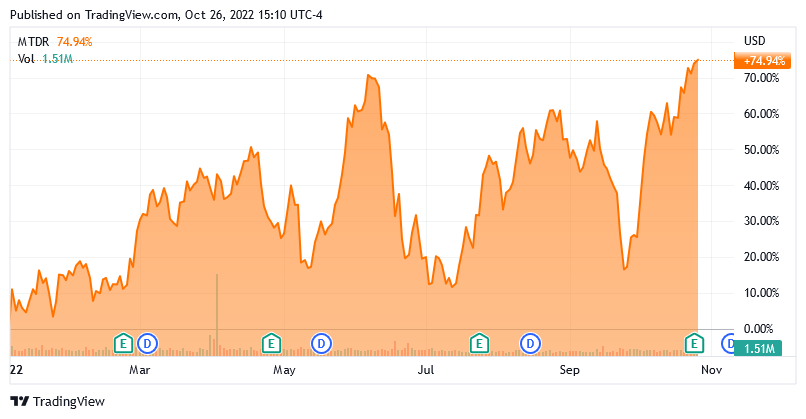

In the introduction to this article, I stated that Matador Resources still appears to have a reasonable valuation despite the strong performance that the stock has already delivered this year. The stock is up an incredible 74.94% year-to-date, making this one of the only stocks to deliver a positive return in 2022:

{kind=link}

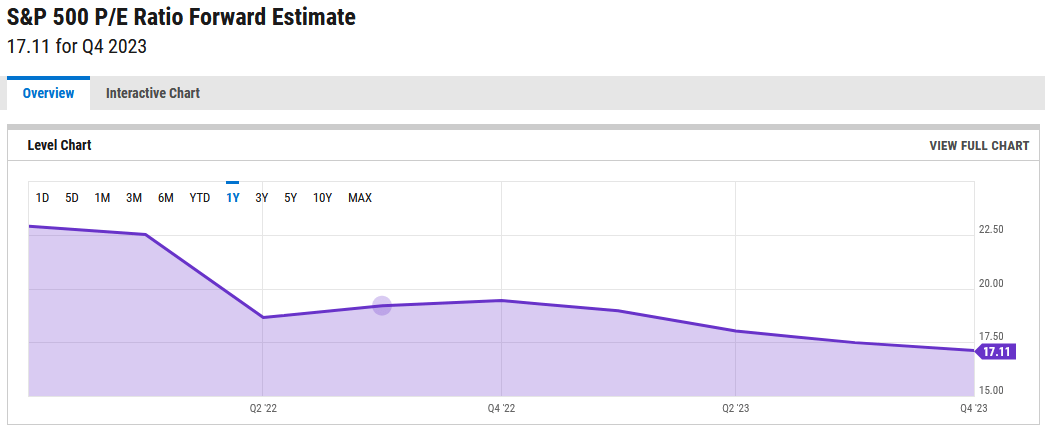

We can see that the stock still has a remarkably low valuation by looking at the forward price-to-earnings ratio. This ratio basically tells us how much an investor is paying today for each dollar of earnings over the next twelve months. According to Zacks Investment Research , Matador Resources currently has a forward price-to-earnings ratio of 6.35. This is very cheap in today's market as the S&P 500 index ( SPY ) has a forward price-to-earnings ratio of 17.11:

{kind=link}

However, as I have pointed out in various previous articles, pretty much everything in the traditional energy industry is incredibly cheap right now despite the surge in crude oil and natural gas prices that we saw over the past two years. Thus, it may make some sense to compare Matador Resources' valuation to that of some of its peers. This is done in this table:

| Company |

| Forward P/E Ratio |

| Matador Resources |

| 6.35 |

| Diamondback Energy ( FANG ) |

| 6.14 |

| Pioneer Natural Resources ( PXD ) |

| 8.26 |

| Continental Resources ( CLR ) |

| 6.57 |

| Devon Energy ( DVN ) |

| 8.50 |

Clearly, this table illustrates my point about everything in the energy industry being incredibly cheap in comparison to the market as a whole. Matador Resources is somewhat better valued than many of its peers, though. Admittedly, it is not the absolute cheapest company on the list but it is still offering a very attractive value proposition relative to its peers and to the market as a whole. There therefore may be a reason to purchase shares of the company today given the strong results that the company delivered in the third quarter of 2022.

In conclusion, Matador Resources has clearly been benefiting from the high energy price environment, which is clearly shown in these results. The company has been using its newfound good fortune very intelligently by reducing its debt. This should overall position the company well to weather any economic troubles that may come in the near future. Despite the strength that we see here and the strong appreciation that it has seen this year, Matador Resources still presents investors with a very attractive value proposition. Overall, the stock still could be a buy today.

For further details see:

Matador Resources: Strong Q3 2022 Results, Still Attractively Valued