DEMZ - Matrix Asset Advisors Q2 2023 Capital Markets Commentary And Quarterly Report

2023-08-10 09:15:00 ET

Summary

- Matrix Asset Advisors is a Value-Driven asset management company. Our investment philosophy and process has allowed us to build a cohesive team of key investment professionals, enabling us to be both opportunistic and responsive.

- The S&P 500 continued its rally in Q2 2023, driven by a small number of technology stocks rebounding from 2022's selloff.

- Growth stocks outperformed the broader market, while energy, utilities, and healthcare were the worst-performing sectors.

- The stock market is expected to broaden its rally in the second half of the year, with a focus on undervalued stocks and sectors that have lagged in the first half.

Capital Markets Highlights

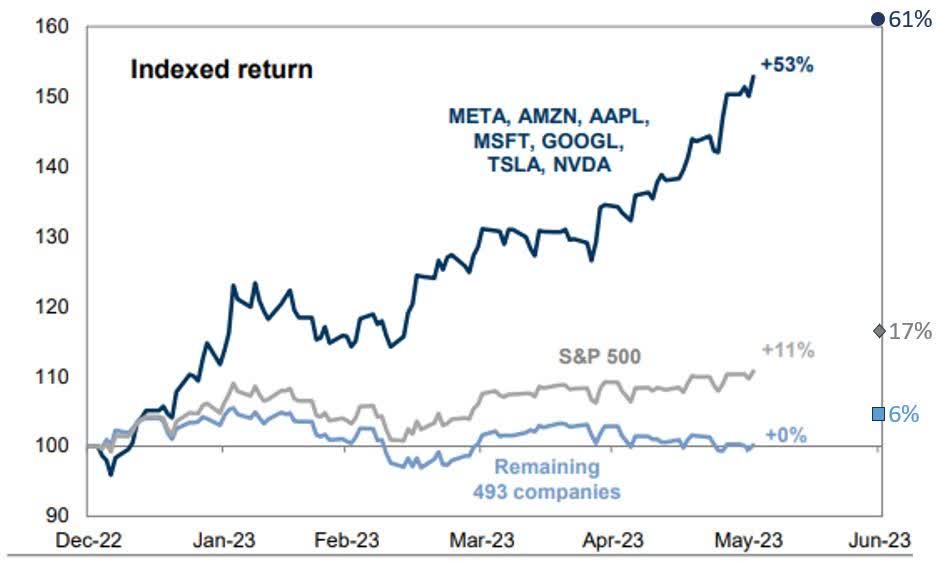

The S&P 500 [1] ( SP500, SPX ) continued its 2023 rally in the second quarter, rising by 8.7%. The return for the first six months of the year was up 16.9%. The index’s gain in the second quarter and year-to-date through June 30 has been driven by a small number of technology stocks with outsized increases (“the magnificent seven”) rebounding from 2022’s sharp selloff and boosted by investor enthusiasm for stocks that are expected to benefit from advances in artificial intelligence ((AI)). The remaining 493 stocks in the S&P 500 ® were only modestly higher year-to-date, through June 30. Below is a chart that highlights this divergence [2] .

{kind=link}

Growth stocks [3] led the market higher in the second quarter and year-to-date through June 30, with the broader market and stocks with higher dividends lagging. Among market sectors, Technology, Consumer Discretionary, and Communications Services stocks have been the best performers while Energy, Utilities, and Healthcare have been the worst-performing sectors. This is the opposite of the leaderboard in 2022.

During the second quarter, the Federal Reserve raised interest rates by another 0.25%, increasing the Fed Funds rate at their May meeting to 5.00%-5.25%. The Fed left the Fed Funds rate unchanged at their June meeting but left open the possibility of one or two more interest rate hikes before year-end.

Fixed Income returns in the second quarter were down slightly but are generally modestly positive for the year-to-date through June 30.

Oil and many other commodities have declined this year, a surprising development for those who expected a rebound following China’s post-Covid economic reopening, OPEC’s decision to reduce oil production, and the ever-present threat of supply disruption from the war in Ukraine. In the U.S., the crude oil price benchmark ended the quarter at $69.86 per barrel, down from $80.16 on 12/31/22. International oil prices have fallen for four quarters in a row [4] , and the S&P GSCI Commodities Index is down about 9% this year [5] .

Our Thoughts Going Into Q3

We remain optimistic about the stock market’s prospects for the balance of the year, even in the face of significant economic and geopolitical uncertainty. Though the economy is showing some signs of deceleration after the Fed’s rapid increase in interest rates over the past 15 months, and the resumption of student loan payments later this year is likely to slow consumer spending, the economy has proved to be more resilient than many expected. With the job market remaining strong, government spending elevated, consumer credit in good shape, and consumer confidence at an 18-month high, we believe the economic slowdown will be manageable, and we do not expect a significant recession.

If the economy avoids a significant recession and the Fed completes its interest rate increase cycle this year, we believe the market will quickly shift its focus to the next period of economic growth, which should be bullish for stocks.

Coming into 2023, we believed last year's stock market decline left the overall market and many individual stocks at attractive price levels, as investors overly discounted a significant downside case for stocks and the economy. We also believed many of the weakest-performing sectors in 2022 were poised to bounce back this year in a market rotation. Returns in the first half of 2023 suggest this has likely mostly played out.

Looking forward, however, we expect the stock market rally to broaden. We don’t believe that the performance difference between the market’s favorite few technology stocks and the rest of the market will continue and expect the performance gap to narrow as the AI mania subsides and investors increasingly focus on the relative attractiveness of many stocks with good business fundamentals that have been left behind. We expect some of the laggards in the first half of 2023, like Financials, Healthcare, and Industrials, to make meaningful contributions to the market's upside in the back half of the year.

One very bullish signal for our holdings is the level of insider buying. Insider buying activity during 2023 for companies in our portfolios appears to be at the highest level in many years. 16.7% of the companies in the large-cap value portfolio have had meaningful insider buying, while 28% of the positions in Dividend Income have seen insider buying. Together 21.4% of our holdings in the Value and Dividend strategies have had notable insider purchases.

While corporate insiders have many reasons to sell shares they own, they primarily buy based on a belief that the stock is attractively priced with favorable prospects. Insiders generally have the best insight into their company’s prospects, and academic studies have highlighted the excess returns that can follow healthy insider buying. We believe this elevated level of insider buying strongly supports our bullish outlook for these stocks and our portfolios overall.

Finally, regarding fixed income investments, with the outlook for inflation showing signs of significant improvement, and our belief that the Fed is nearing the end of its rate hiking this cycle, we think high-quality, short-term bonds are attractive today, offering a reasonable return with modest risk. At current yields, they can add important components of stability and income to a balanced portfolio.

Reported inflation and inflation expectations data have improved meaningfully, although not in a straight line. Also, most manufacturing and distribution logistics issues have been resolved. The Fed has just paused its rate increases, but its statement on future monetary policy was hawkish and will likely evolve based on additional inflation and employment data. While the Fed may increase the Fed Funds rate one or even two more times for insurance, we believe they are near the end of raising interest rates for this cycle.

Below is a chart showing the decline in the Consumer Price Index over the past 12 months. The May CPI was up +0.1% (annualized up +1.5%), with the 3-month annualized rate at +2.2% and the 6-month annualized rate at +3.2%.

.

Large Cap Value Strategy

In the second quarter of 2023, Matrix’s Large Cap Value Portfolio (LCV) added to its good start to the year, posting a positive mid-single-digit return. For the first six months of the year, the LCV portfolio is up low double digits, behind the technology-weighted S&P 500 ® but nicely ahead of the Russell 1000 ® Value Index.

The portfolio has been led higher by many of last year's fallen angels, like Amazon ( AMZN ), Apple ( AAPL ), Alphabet ( GOOG , GOOGL ) , Meta Platforms ( META ), and Microsoft ( MSFT ).

So, while the Value style has struggled in general this year, our portfolio has been driven higher by our exposure to a number of the mega-cap Technology plays caught up in the AI rally.

Importantly, while the portfolio has nice year-to-date gains, we think it has substantial additional upside. We expect some of the recent laggards like Financials, Healthcare, and Industrials to make meaningful contributions to the portfolio’s upside in the back half of the year.

During the quarter, we started a new position in United Health Group ( UNH ), a healthcare company with two businesses – UnitedHealthcare, the nation’s largest health insurer, and Optum, a provider of medical services including primary care, urgent care, outpatient surgical centers, and pharmacy management. The company is a leader in the healthcare industry, and its strong profit and earnings growth record has often been rewarded in the market with a premium multiple. The stock falls out of favor periodically when investors become concerned about political, regulatory, reimbursement, legal, and healthcare inflation risks. We view the stock's recent underperformance as an opportunity to invest in a very high-quality company at an attractive price.

We also added to the position in L3Harris ( LHX ) with proceeds from several modest scale-backs, and for taxable accounts made some trades as part of our tax mitigation strategy. We had generally reversed these trades by the end of the quarter.

The largest sector weightings in the LCV portfolio on June 30 continue to be Technology, Financials, and Healthcare.

Technology stocks have been a key contributor to returns in 2023 after last year's bear market left many of these stocks at compelling prices. We think this performance can continue, but likely at a more measured pace in the second half of 2023. We believe some laggards in the recent meltup, like Cisco Systems ( CSCO ), PayPal ( PYPL ), and Qualcomm ( QCOM ) are poised to excel in upcoming periods.

Our Financials are trading at cyclically low valuations as a result of significant short-term overhangs, and we believe they are due for meaningful multiple expansion. The recent Fed stress test results and subsequent dividend increases highlight the strength of the banking group overall and the stocks we own. Insider buying in Financials is well above average and is another data point that strongly supports our upbeat outlook for this area.

After its very strong relative 2022 performance, Healthcare stocks have been one of 2023 weakest sectors. We believe this will likely be a pause that refreshes, and we are very upbeat about their prospects for the balance of the year.

On June 30, the average P/E multiple of the LCV portfolio was 17.6x and 15.3x on 2023 and 2024 estimated earnings, with discounts to the S&P 500's 20.3x and 18.1x estimated P/Es. The median P/E is at a compelling 15.1x and 12.8x 2023 and 2024 estimated earnings. The average embedded appreciation potential of the portfolio was 42.5%, which is very attractive on an absolute basis and above our historic average.

Portfolio companies generally showed solid operating performance vs. expectations in their recent quarterly reports, even as the economic environment becomes more challenging. The LCV portfolio outpaced the market on earnings and revenues vs. expectations.

Overall, we think the Large-Cap Value portfolio can add to its early 2023 gains, as its companies have strong and growing franchises, are positioned to weather the uncertain business and financial environment, and trade at very attractive valuations. We expect stocks that lagged in the first part of the year to lead the portfolio higher as the year progresses.

Dividend Income Strategy

After a very good relative year in 2022, defending well in the market’s sharp decline, the Dividend Income portfolio’s performance was about unchanged in the second quarter and showed a modest decline for the first six months of 2023, underperforming the S&P 500 ® and the Russell 1000 ® Value Indexes in both periods.

Very few of the mega-cap Technology stocks that have driven the market in 2023 are dividend payers and thus are not candidates for inclusion in the Dividend Income strategy. For that reason, dividend strategies in aggregate have struggled year-to-date through June 30, and are flat to down modestly [6] . According to Ned Davis Research, the past six months have been the worst first-half performance for dividend payers relative to nonpayers since 2009 7 . We believe this significant short-term lag is likely to be followed by an equally powerful reversal and catch-up period for dividend payors.

While MDI’s performance has been frustrating so far this year, the underlying operations, cash flows, and fundamentals of the companies within are strong and valuations are very attractive. This leads us to be upbeat about the portfolio's prospects for the balance of the year. Insiders seem to agree, as we are seeing the most insider buying that we have seen in a decade, with 28% of the positions in the portfolio showing healthy levels of insider buying.

We have used the market’s volatility to start new positions, add to existing holdings at compelling prices, and opportunistically trim/exit positions that achieved our goals. This should position the Dividend Income portfolio to rebound strongly as the market’s returns broaden.

During the second quarter, we added a new position in Pfizer ( PFE ), a leading global pharmaceutical company. Key product areas for Pfizer are cardiovascular, metabolic, migraine, and women's health, a vaccine portfolio across all ages with a pipeline focus on infectious diseases with significant unmet medical needs. Pfizer sales and earnings grew significantly during the pandemic, benefitting from its Covid vaccines and treatment products. The company is in a transition from a Covid to a post-Covid world with revenues and earnings declining in 2023. After this post-Covid reset, Pfizer is expected to grow sales by 3% to 4% per year and earnings by 6%+ per year. The company’s stock price stock peaked at more than $61 in December 2021. Now below $40, Pfizer’s valuation is attractive at 11 times earnings with a healthy and sustainable 4.4% dividend yield.

We sold out of the position in Coca-Cola ( KO ) to fund a more attractive opportunity in General Dynamics ( GD ). We modestly scaled back Microsoft and Starbucks ( SBUX ), as they became oversized due to strong gains in the past few months.

For taxable accounts, we made some trades among Financial stocks to capture valuable tax losses while maintaining our desired exposure to the sector. We had generally reversed these trades by the end of the quarter.

The MDI portfolio is very attractively priced on June 30, with average P/E multiples of 16.2x and 14.4x estimated 2023 and 2024 earnings, compared to the S&P 500’s 20.3x and 18.1x. The median P/E is at an even more compelling 13.7x and 12.3x 2023 and 2024 estimated earnings. The embedded appreciation potential is an attractive 40.7%, which is well above its historic average.

In the second quarter, four of our companies increased their dividends with an average raise of 7.4%. For the first six months of the year, 12 of our portfolio holdings increased their dividends by 6.7%. On June 30, the portfolio had a 3.19% dividend yield, which compares very favorably to the 1.55% yield on the S&P 500 ® and the 2.40% yield on the Russell 1000 ® Value.

The Dividend Income portfolio’s largest sector concentrations were unchanged from the previous quarter: Financials, Healthcare, and Technology.

For our Financial holdings, credit profiles remain strong and interest income robust, even as valuations have continued to decline. We believe their P/E multiples can expand significantly when forecasts of forward economic conditions improve and current overhangs ease. All of our Financial holdings passed the most recent Fed stress test with most already following up with healthy dividend increases. Insider buying in Financials is well above average and is another data point that strongly supports our upbeat outlook for this area.

After its very strong absolute 2022 performance, Healthcare stocks have been one of 2023’s weakest sectors. We believe this pullback has set the stage for the next meaningful move higher, and we are very upbeat about their prospects for the balance of the year. Beyond their significant upside potential, we believe our Healthcare stocks can be helpful as stable, defensive plays with strong dividend yields in an uncertain economy.

Our expectation that Technology would bounce back in 2023 has generally come to pass, though performance has been uneven. While the sector is up nicely overall in Dividend Income, we believe our holdings still have good additional upside potential and should continue to move higher, even when the upside slows for Technology stocks overall.

Although the Dividend Income strategy’s performance has been frustrating in the first half of the year, this comes after a very strong relative performance in 2022 when it achieved its goal of being more protective during a tumultuous market and is in line with a peer group of Dividend Income strategies. The portfolio continues to generate a strong and growing income stream, and we believe is poised for solid gains in the second half. As noted earlier, insider buying at 28% of the holdings supports our bullish outlook.

Bonds

After a strong start to the year bond returns were flat to slightly lower for the quarter but are modestly higher year-to-date through June 30. Interest rates rose across the maturity spectrum for the period, but higher coupons mostly offset the pullback in prices for the quarter and fully offset the modest pullbacks in prices since the start of the year. Looking forward, we believe the current interest rates offered by short-term bonds (3 months to 5 years) will provide a positive return even if short-term rates move modestly higher.

Yields on the 10-year Treasury rose during the second quarter to 3.81% vs. 3.48% at the end of the first quarter. The 10-year Treasury rate was 3.88% at the start of the year.

As we move through 2023, we anticipate the Federal Reserve may pause on its aggressive interest rate policy as job growth and inflation are expected to ease. But inflation is still higher than the Fed’s longer-term 2% goal and one or two more interest rate hikes are very possible before this interest rate hiking cycle is over.

Matrix’s fixed income positioning has been very conservative in recent years, focusing on high quality corporates, U.S. Treasuries, agencies, and municipals with nearer-term maturities. This served us well in the 2022 bond market sell-off and allows us to get very healthy current income streams with short-term bonds paying the same or more than longer-dated bonds.

During the quarter, we continued to take advantage of the solid yields offered on shorter-term bonds and added to our portfolios with a focus on three-month to three-year US Treasuries and Agencies.

Our taxable and municipal bond portfolios were modestly higher for the quarter and for the first six months of the year and generally in line with our benchmarks.

At current healthy interest rates, shorter-term bonds are very attractive to us, offering good income and minimal principal risk. We continue to be cautious about long-term bonds where we think there is more interest rate risk when the economy reaccelerates, and the yield curve normalizes (higher long-term rates versus short-term rates).

Balanced Accounts

After a difficult year in 2022 for balanced accounts, where both stocks and bonds declined, stocks and bonds returned to their more traditional return characteristics in the first half of 2023, with stocks driving long-term growth and bonds providing portfolio stability, income, and modest gains over time.

We continue our overweight to equities believing that stocks are more attractive than bonds for capital appreciation. But after years of being very cautious in our fixed income outlook, we are upbeat about short-term bonds. Their yields are attractive and provide good income with minimal risk of capital loss.

Thank you for the trust you have placed in us. Please contact us with any questions you have about the information in this commentary or your portfolio.

Footnotes[1] All references to the stock market are the S&P 500 ® unless otherwise noted. [2] Source Goldman Sachs 12/31/22-6/1/23, updated by Matrix through 6/30/23. [3] This and future references to Sector and/or Asset class specific returns are from J.P. Morgan Market Insights “ Guide to the Markets ® ” US 3Q/2023 as of June 30, 2023 [4] Barron’s June 30, 2023, Oil is on Track for Record losing Streak. [5] Barron’s July 3, 2023, Stocks are Running Hot. Your Portfolio Needs a Tuneup. [6] VMY Equity return was down -0.47% and the SDY Equity return was down -0.78% YTD through June 30, 2023. [7] WSJ, July 2, 2023, Investors Spurn Dividend Paying Stocks as AI Booms. Disclosure: The information provided is for demonstrative and academic purposes and is meant to provide valuable insight into market cycles, NOT a recommendation to buy or sell any security. Any investments referenced above may currently be held, or traded by Matrix Asset Advisors. Investment Advisory Services are offered through Matrix Asset Advisors, an SEC Registered Investment Adviser. No offer is made to buy or sell any security or investment product. This is not a solicitation to invest in any investment product of Matrix Asset Advisors. Matrix Asset Advisors does not provide tax or legal advice. Consult with your tax advisor or attorney regarding specific situations. Opinions expressed are subject to change without notice and are not intended as investment advice or to predict future performance. Investing involves risk, including the potential loss of principal. No investment can guarantee a profit or protect against loss in periods of declining value. All information is believed to be from reliable sources; however, we make no representation as to its completeness or accuracy. The Securities identified and described do not represent all of the securities purchased, sold, or recommended for client accounts. Actual portfolio holdings may vary for each client and there is no guarantee that a particular client’s account will hold any or all of the securities identified. The reader should not assume that an investment in the securities identified was or will be profitable. Opinions and projections are as of the date of their first inclusion herein and are subject to change without notice to the reader. As with any analysis of economic and market data, it is important to remember that past performance is no guarantee of future results. The securities identified and described herein may not represent all the securities purchased, sold, or recommended for client accounts. The reader/viewer should not assume that an investment in the securities identified was or will be profitable. All data is through (or as of) 6/30/2023 unless otherwise noted. For more information about Matrix Asset Advisors, please visit our website at Matrix Asset Advisors. Our website includes our firm’s Client Relationship Summary document. Definitions: S&P500 ® Index is a broad-based unmanaged index of 500 stocks, which is widely recognized as representative of the equity market in general. You cannot invest directly in an index. Russell 1000® Value Index measures the performance of those Russell 1000® Index companies with lower priceto-book ratios and lower forecasted growth values. Fixed Income type of investment security that pays investors fixed interest or dividend payments until their maturity date. Inflation is a sustained increase in the general level of prices for goods and services. Treasury Securities often simply called Treasuries, are debt obligations issued by the United States Government and secured by the full faith and credit (the power to tax and borrow) of the United States. Interest Rate is the amount a lender charges a borrower and is a percentage of the principal—the amount loaned. Fed Funds Rate is the interest rate at which depository institutions lend reserve balances to other depository institutions overnight on an uncollateralized basis. Reserve balances are amounts held at the Federal Reserve to maintain depository institutions' reserve requirements. Recession was a significant, widespread, and prolonged downturn in economic activity. Credit Quality is a measurement of an individual's or company's creditworthiness, or the ability to repay its debt. P/E Multiples the ratio for valuing a company that measures its current share price relative to its per-share earnings. The Yield Curve is a curve on a graph in which the yield of fixed-interest securities is plotted against the length of time they have to run to maturity Market Valuation is the value of an asset based on the price that would be paid for it if it were sold at a certain time. Unemployment when someone can work and wants to work but is unable to find employment. The Bureau of Labor Statistics ( BLS ) specifically defines unemployed persons as those who don't have a job but are available for work and have looked for work in the past four weeks. Dividend Yield is a financial ratio that tells you the percentage of a company's share price that it pays out in dividends each year. Earnings per Share ((EPS)) is a company's net profit divided by the number of common shares it has outstanding. EPS indicates how much money a company makes for each share of its stock and is a widely used metric for estimating corporate value. Municipal Bond is a bond issued by state or local governments or entities they create such as authorities and special districts. In the United States, interest income received by holders of municipal bonds is often, but not always, exempt from federal and state income taxation. Financials a section of the economy made up of firms and institutions that provide financial services to commercial and retail customers. Health Care all businesses involved in the provision and coordination of medical and related goods and services. Information Technology businesses that sell goods and services in electronics, software, computers, artificial intelligence, and other industries related to information technology ((IT)). Consumer Discretionary an economic sector classification of non-essential consumer goods and services. Communication Services includes companies that sell phone and internet services via traditional landline, broadband, or wireless. The communications sector also includes companies that create and produce of movies, television shows, and other content. Growth Strategy a collection of business initiatives that seek the maximization of a company's value within a period. Operating Results measures the amount of profit realized from a business's operations after deducting operating expenses such as wages, depreciation and cost of goods sold. US Governments (Treasuries) are debt obligations issued by the United States Government and secured by the full faith and credit (the power to tax and borrow) of the United States. Agencies a low-risk debt obligation that is issued by a U.S. government-sponsored enterprise ((GSE)) or other federally related entity. High Grade Corporate Bonds that are believed to have a lower risk of default and receive higher ratings by the credit rating agencies, namely bonds rated Baa (by Moody's) or BBB (by S&P and Fitch) or above. These bonds tend to be issued at lower yields than less creditworthy bonds. Federal Reserve is the central banking system of the United States. It was created on December 23, 1913, with the enactment of the Federal Reserve Act, after a series of financial panics led to the desire for central control of the monetary system in order to alleviate financial crises. Mega Cap is a designation for the largest companies in the investment universe as measured by market capitalization. Economic Growth an increase in the production of economic goods and services, compared from one period of time to another Consumer Confidence measures how optimistic (or pessimistic) consumers are about the state of the economy. Consumer Credit debt taken on by a consumer, typically to be repaid with interest in the future. As an economic indicator, consumer credit is used to gauge the indebtedness of Americans. Artificial Intelligence the ability of a digital computer or computer-controlled robot to perform tasks commonly associated with intelligent beings Dividend Income Large Cap Core - the largest U.S. companies, or those with market capitalizations of $10 billion or more, where neither growth nor value characteristics predominate. Large Cap Growth - shares of the largest U.S. companies, or those with market capitalizations of $10 billion or more , that are projected to grow faster than other large-cap stocks. Large Cap Value - shares of the largest U.S. companies, or those with market capitalizations of $10 billion or more, that are considered underpriced based on fundamental analysis. companies that pay out regular dividends. Value Strategy investment strategy that involves picking stocks that appear to be trading for less than their intrinsic or book value. Balanced Accounts combines asset classes in aFinancial Portfolio: What It Is, and How to Create and Manage Onein an attempt to balancerisk and return. Portfolios are divided between stocks and bonds, either equally or with a slight tilt, such as 60% in stocks and 40% in bonds. Balanced portfolios may also maintain a small cash or money market component for liquidity purposes. Insider Buying the purchase of shares in a corporation by a director, officer, or executive within the company. Corporate Insiders either a senior officer, director, or an above 10% equity owner. Once classified as a corporate insider, people in these positions must adhere to very strict disclosure regulations required by the Securities and Exchange Commission (SEC). Bullish Outlook an investor believes a stock, or the overall market will go higher Short Term Bonds - a bond that will pay back your principal, or mature, quickly, typically within four years. Embedded Appreciation Matrix’s measure of potential upside of a stock from its market price to our estimate of its fair/intrinsic value. Geopolitical the study of how geography and economics have an influence on politics and on the relations between nations OPEC The Organization of the Petroleum Exporting Countries is an organization enabling the co-operation of leading oil-producing countries in order to collectively influence the global oil market and maximize profit. S&P GSCI Commodities Index serves as a benchmark for investment in the commodity markets and as a measure of commodity performance over time. It is a tradable index that is readily available to market participants of the Chicago Mercantile Exchange. Energy Sector is the totality of all the industries involved in the production and sale of energy, including fuel extraction, manufacturing, refining and distribution. Utility Sector companies that provide electricity, natural gas, water, sewage, and other services to homes and businesses. Manufacturing the making of goods by hand or by machine that upon completion the business sells to a customer. Distribution Logistics combines all the moving parts that drive retail. It is a combination of processes that efficiently move goods through the fulfillment process, from warehouse to end customer. Hawkish a financial advisor or policymaker who believes that monetary policies should maintain high-interest rates to curb inflation. They are primarily interested in high-interest rates as they relate to Fiscal policy. CPI The Consumer Price Index ((CPI)) consists of a family of indexes that measure price change experienced by urban consumers. Specifically, the CPI measures the average change in price over time of a market basket of consumer goods and services. The market basket includes everything from food items to automobiles to rent Earnings Revenue- Revenue is the income a company generates before deducting expenses. Earnings, on the other hand, represents the profit a company has earned; it is calculated by subtracting expenses, interest, and taxes from revenue. The Magnificent Seven large tech-oriented companies. The group includes Apple, Microsoft, Alphabet, Amazon, Nvidia, Tesla, and Meta. |

Editor's Note: The summary bullets for this article were chosen by Seeking Alpha editors.

For further details see:

Matrix Asset Advisors Q2 2023 Capital Markets Commentary And Quarterly Report