MATW - Matthews International: The Easy Money Has Been Made But There's Still A Little Life Left

2023-08-02 17:25:00 ET

Summary

- Matthews International's stock has performed well despite mediocre financial performance in recent years.

- This year, the picture is looking up for the most part, driven by two of the firm's operating segments.

- The company isn't the most stable, but some additional upside likely exists from here.

One of the great things about buying value stocks is that you don't necessarily need financial performance of those businesses to be all that special in order for the market to eventually realize that shares are underpriced. A great example of this can be seen by looking at Matthews International ( MATW ). Since I wrote about the company last in May of 2022, the business has not performed exceptionally well from a financial perspective. Of course, it hasn't been operated poorly either. I would classify overall performance as mediocre. Having said that, shareholders have still been rewarded materially, with shares shooting up, even in relation to the broader market. Fast forward to today, and with the stock trading at higher levels than it was previously, investors would be right to ponder whether now is the time to look elsewhere for opportunity.

The easy money has been made

Over a year ago, on May 27, 2022, I wrote an article that took a bullish stance on Matthews International. In that article, I acknowledged that economic concerns and weak margins had caused the stock's pain. Even in spite of that pain, overall bottom line results were forecasted to decline only marginally for that year. This, combined with how cheap the stock was, led me to believe that some attractive upside existed for shareholders. And sure enough, that's precisely what happened. After rating the stock a ‘buy’ to reflect my view that shares should outperform the broader market moving forward, we saw the units appreciate an impressive 45.1%. That is materially higher than the 12.3% rise seen by the S&P 500 over the same window of time.

{kind=link}

Author - SEC EDGAR Data

In some respects, financial performance for the business has been improving. To see what I mean, we need only look at data covering 2023 compared to 2022. Revenue during the first three quarters of the year came in at $1.40 billion. That represents an increase of 7.3% over the $1.31 billion the business generated in sales for the same window of time one year earlier. It might be tempting to just stop the analysis when it comes to revenue here. But unlike many other firms, particularly ones that are fairly small in size, Matthews International deserves a deeper look. I say this because it is not a simple enterprise. In fact, investors would be wise to view it as three distinct businesses all rolled up into one.

The first of these is the part of the company that has always interested me the most. But that's because I like odd types of businesses that you wouldn't normally think to invest in. This is the Memorialization segment of the enterprise. For those not well acquainted, this is the part of the company that is responsible for the production and sale of memorialization products that are used mostly in cemeteries, funeral homes, and crematories. Examples here include cast bronze memorials, granite memorials, caskets, cremation and incineration equipment, and more. As I wrote about in an article covering another player in this space known as Service Corporation International ( SCI ), a firm that focuses on the ownership and operation of funeral homes and cemeteries, the space has seen some weakness this year because the prior years were times when the industry benefited from the COVID-19 pandemic.

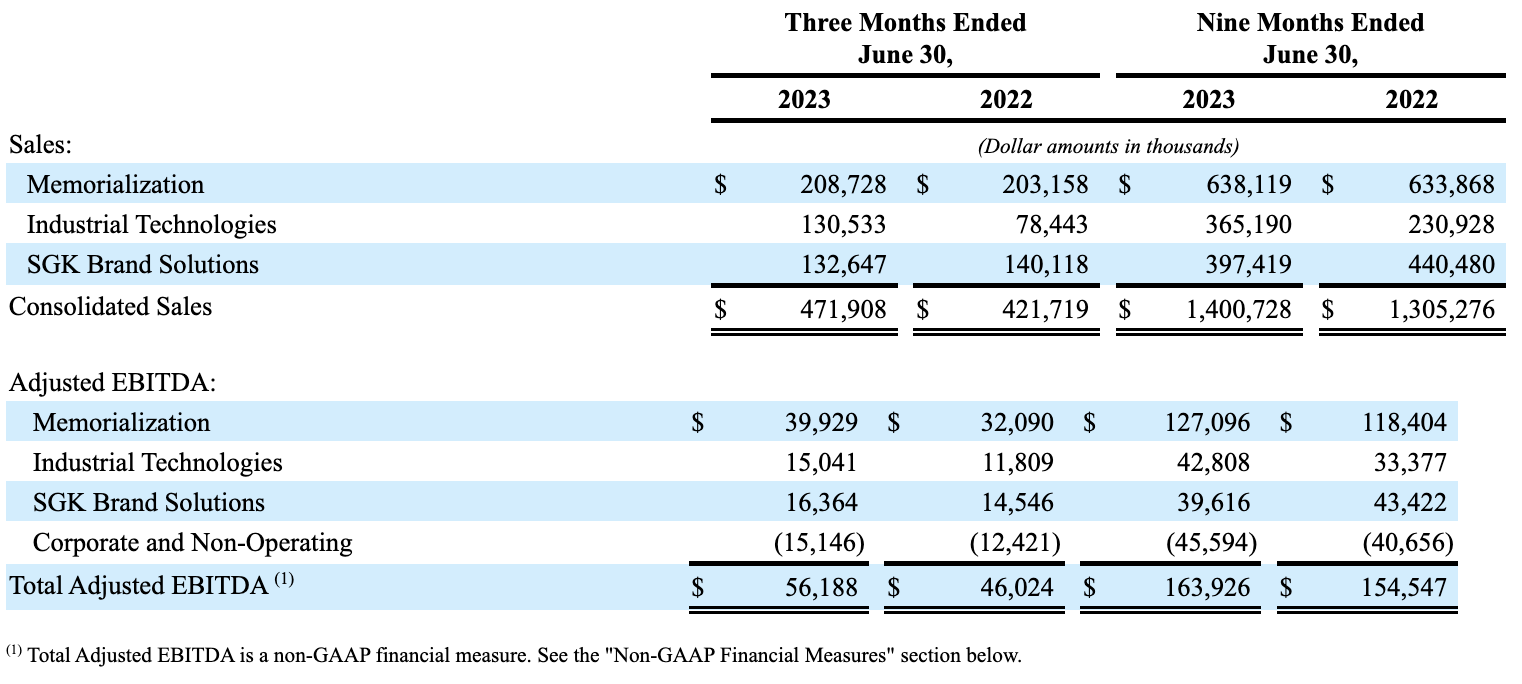

Knowing this, I would have thought that Matthews International’s Memorialization segment would have seen some weakness this year as well. But that's not what happened. Revenue in the first nine months of the year came in at $638.1 million. That represents an increase of 0.7% over the $633.9 million in sales generated one year earlier. According to management, this rise reflected higher pricing that the company charged to its customers, as well as higher sales of granite memorial products, mausoleums, and cremation equipment across the US. It also benefited to some extent from its acquisition of Eagle Granite Company. However, these increases were offset to some extent by lower casket sales and bronze memorial product sales. Foreign currency fluctuations also impacted revenue negatively to the tune of $2.3 million.

To be clear, the reduction in sales associated with caskets should not be a surprise to investors. For decades now, fewer people as a percent of the population have chosen to be buried and more have chosen to be cremated. A big part of that has to do with cost. Cremation is far more affordable than burial in a casket. In 1970, for instance, only about 5% of Americans chose to be cremated. By 2020, this number had grown to 56%. And according to the National Funeral Directors Associations , as much as 80% of the US population we'll choose to be cremated by 2035. So this will continue to be something of a headwind for the company, even though a growing population will help offset this to some degree.

{kind=link}

Matthews International

Next, we have the Industrial Technologies portion of the business. This is the true growth machine of Matthews International. The segment is responsible for producing, selling, and servicing, custom energy storage solutions, engaging in product identification and warehouse automation technologies and solutions work, and more. Some of its offerings include fulfillment systems that are used for identifying, tracking, picking, and conveying consumer and industrial products. And on the energy side of things, the company makes engineered calendaring, laminating and coating equipment that can be used for the production of lithium-ion batteries and components of fuel cells.

Revenue during the first nine months of the 2023 fiscal year for this segment came in at $365.2 million. That's 58.1% above the $230.9 million in sales generated one year earlier. According to management, this increase was largely the result of two different acquisitions that the company made in 2022. However, organic growth associated with its purpose-built engineered products, largely involving energy storage solutions for the EV market, as well as higher product identification sales and higher sales associated with warehouse automation solutions, all helped the business considerably. Interestingly, revenue would have been higher had it not been for an $8.5 million impact caused by foreign currency fluctuations.

Lastly, we have the laggard of the group. This is the segment known as SGK Brand Solutions. Through this segment, the company provides packaging and brand experience solutions for its customers. Revenue under this segment actually fell 9.8%, declining from $440.5 million to $397.4 million. This drop in sales, according to management, was driven in part by a $17.9 million hit associated with foreign currency fluctuations. The rest of the drop in sales, however, was the result of multiple factors, including lower brand revenue from Europe, a decline in sales of cylinder packaging products in Europe, and lower retail-based sales in both the US and European markets.

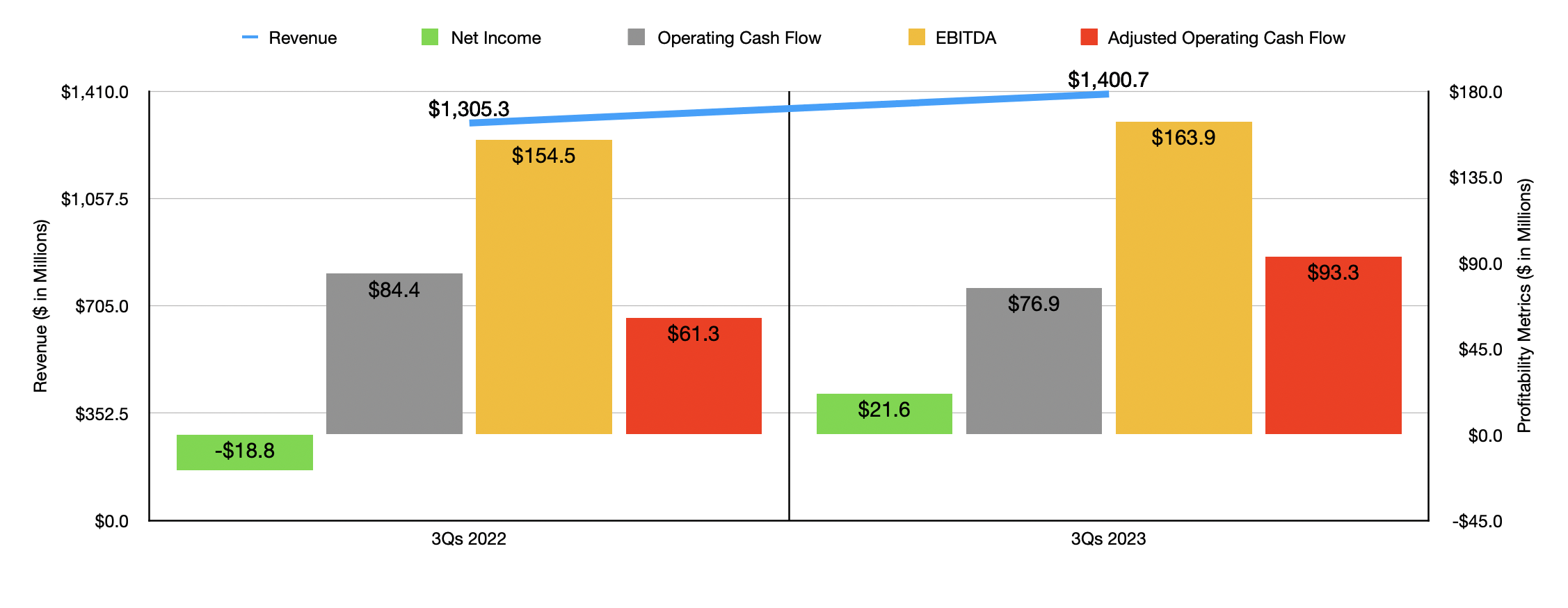

With revenue rising, bottom line performance for the company also improved. Net income went from negative $18.8 million to positive $21.6 million. The same segments that were responsible for the increase in sales also reported bottom line improvements, while SGK Brand Solutions reported a decline in profitability. This should not be all that surprising. Other profitability metrics were rather mixed. For instance, operating cash flow fell from $84.4 million to $76.9 million. But if we adjust for changes in working capital, we would get an increase from $61.3 million to $93.3 million. Meanwhile, EBITDA for the company grew from $154.5 million to $163.9 million.

{kind=link}

Author - SEC EDGAR Data

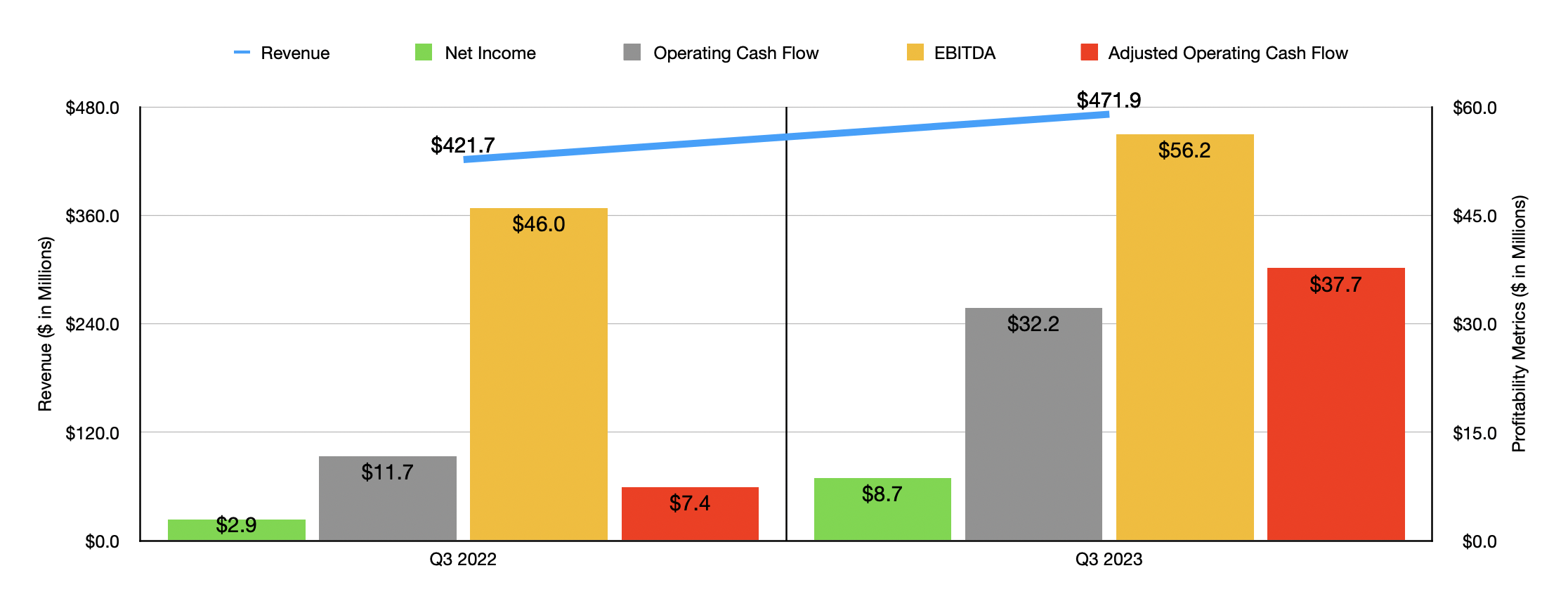

As you can see in the chart above, performance for the company has remained largely positive even as of the third quarter that management just reported on. Revenue, profits, and cash flows, were all up year over year. What this demonstrates is that, even though economic conditions have been uncertain, the company continues to perform well where it can. And once again, the same segments that added to the company's top line in the first nine months as a whole relative to the same time last year were also responsible for the strength in the third quarter on its own. It is noteworthy, however, that SGK Brand Solutions actually reported an improvement in its profits, with EBITDA climbing from $14.5 million to $16.4 million.

{kind=link}

Author - SEC EDGAR Data

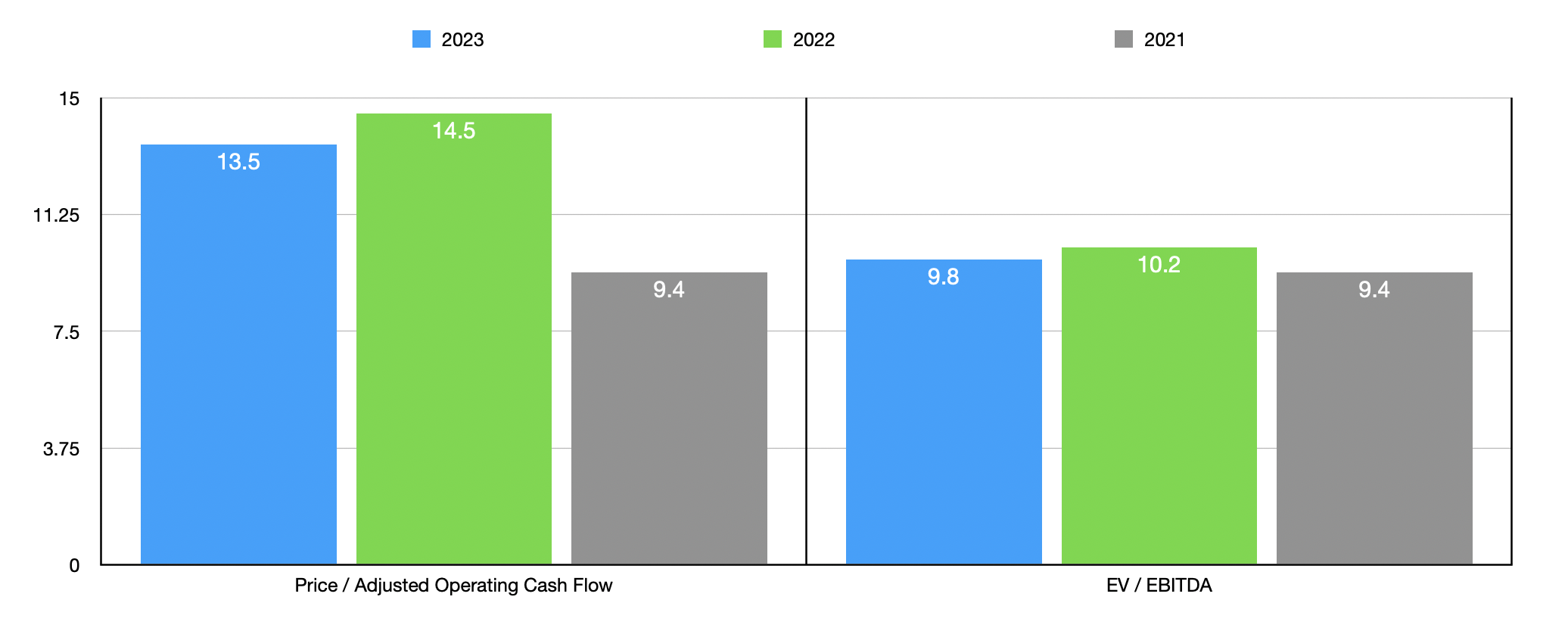

When it comes to the 2023 fiscal year in its entirety, management said that investors should anticipate the company generating EBITDA of between $215 million and $235 million. They even came out and said that it's almost certain that the metric will come in above the $220 million limit. If we assume that adjusted operating cash flow will change at the same rate year over year as what EBITDA is forecasted to, then we would expect a reading of $104.1 million. Using these results, you can see how shares of the company are priced above. Because of bottom line improvements, units are looking cheaper on a forward basis compared to if we were to use data from 2022. But the picture is still not quite as positive as it was using data from 2021.

To put all of this in perspective, it's worth mentioning that when I wrote about the company more than a year ago, the forward price to adjusted operating cash flow multiple for the business for the 2022 fiscal year was 6.1. The forward EV to EBITDA multiple was 7.4. But because of the significant increase in share price, the stock has gotten far more expensive. The good news for investors is that shares are still reasonably affordable, though perhaps not as cheap as some might think. The fact of the matter is that historical financial performance for the business has been very volatile from year to year. And companies like that do deserve to trade at something of a discount. Relative to the only other company that I feel comfortable comparing it to because, like Matthews International, it has operations in the death care space while also having other diverse operations, Hillenbrand ( HI ) is trading at a price to operating cash flow multiple of 15.5. While shares are more expensive than Matthews International on this front, they are cheaper when it comes to the EV to EBITDA multiple, posting a reading of 8.7.

Takeaway

All things considered, I would say that Matthews International has been a great win in my book. I regret not buying shares of the business, but I honestly didn't think that units would appreciate this much. In the grand scheme of things, I would say that shares are still priced low enough to offer some upside. But that upside is severely limited compared to what it was last year. Given all of these factors, I feel comfortable rating the company a soft ‘buy’ at this time. But if we see another 10% upside or so, I almost certainly will downgrade it to a ‘hold’.

For further details see:

Matthews International: The Easy Money Has Been Made, But There's Still A Little Life Left