MXCT - MaxCyte: Engineering The Next Biotech Wave

2023-05-30 13:38:58 ET

Summary

- Cutting-edge cellular engineering firm MaxCyte (MXCT) has developed a platform which enables modifications to cells.

- Applications of MaxCyte's cellular engineering platform are far-reaching, such as cell-based therapies, gene editing, and drug discovery.

- With a $1.55+ billion backlog of milestones from Strategic Program Licenses and potential royalties longer term, MaxCyte is starting to look like an attractive investment.

For the past two decades, MaxCyte ( MXCT ) has been developing its technology platforms to enable the future of cellular engineering. There has been palpable excitement about the advances in biotech with CRISPR , and we believe that the best way to get exposure to the broader gene editing/cell engineering revolution may be through MaxCyte.

What is Cellular Engineering?

Cellular engineering is the process of modifying biological cells to achieve a specific result. Over time, these tools have become more precise and can now affect cells at the molecular level. One example of this is gene editing, which uses tools like CRISPR/Cas9 to add or remove specific genes from a cell. With further technological advancements, the possibilities for cellular engineering are limitless.

What Role Does MaxCyte Play?

MaxCyte focuses on technology platforms that allow for electroporation. Let's review the high-level biology:

Electroporation is the use of high-voltage pulses applied to a cell membrane, making the membrane transient. With the membrane now permeable, molecules such as drugs, antibodies, DNA, or RNA can be passed into the cell.

Electroporation Diagram (www.btxonline.com)

MaxCyte's ExPERT instruments provide a best-in-class solution for what they call Flow Electroporation . The solutions provided by MaxCyte's proprietary technology aid in drug discovery, cell-based research, and ultimately commercialization of cell therapies.

MaxCyte's Business Model

While the technology broadly has broad implications for the future of humanity, as investors we can marvel at the business model that MaxCyte has developed.

The higher potential and higher revenue opportunities for MaxCyte come from their Strategic Partnership Licenses or SPLs. The SPLs are a license for a company to use MaxCyte's technology for the discovery and development of a therapeutic. In exchange for allowing partners to use their technology, MaxCyte receives a series of incentive payments and ultimately a royalty for any commercial drugs developed using their technology. MaxCyte has SPLs with notable biotech businesses such as Vertex ( VRTX ) and CRISPR Therapeutics ( CRSP ). They estimate that their current market opportunity is up to 75 or more SPLs.

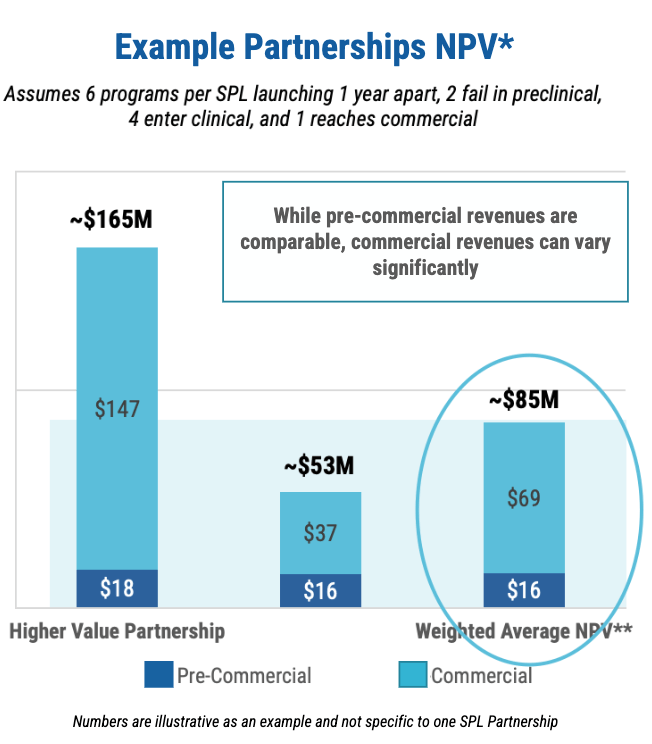

MaxCyte NPV per SPL (MaxCyte Investor Presentation)

{kind=link}

Each partnership can lead to multiple clinical programs where the actual research and discovery for new therapeutics are done. As shown in the illustration above from their most recent investor presentation , the company estimates that they have a weighted average NPV of roughly $85 million per SPL . Across the 20 current SPLs, the implied net present value of MaxCyte's partnerships would be $1.7 billion. Taking into account the 55 partnerships that they have not yet solidified, the company is implying that their total market opportunity is about $6.4 billion .

Despite having 125+ clinical programs, of which 16 are active in the clinic, MaxCyte has not yet been associated with any commercial drug. While they are not yet receiving any commercial royalties, the business has been sustainably producing incredible gross margins of up to 89% representing the massive profitability potential of the business at scale.

Let's break down all of the revenue streams that lead to the strong 89% margin:

Razor and Razor-Blade Model

MaxCyte leases instruments to customers and sells single-use disposables for these instruments. This is a razor and razor-blade kind of business with very high margins on single-use disposables.

Milestone Payments

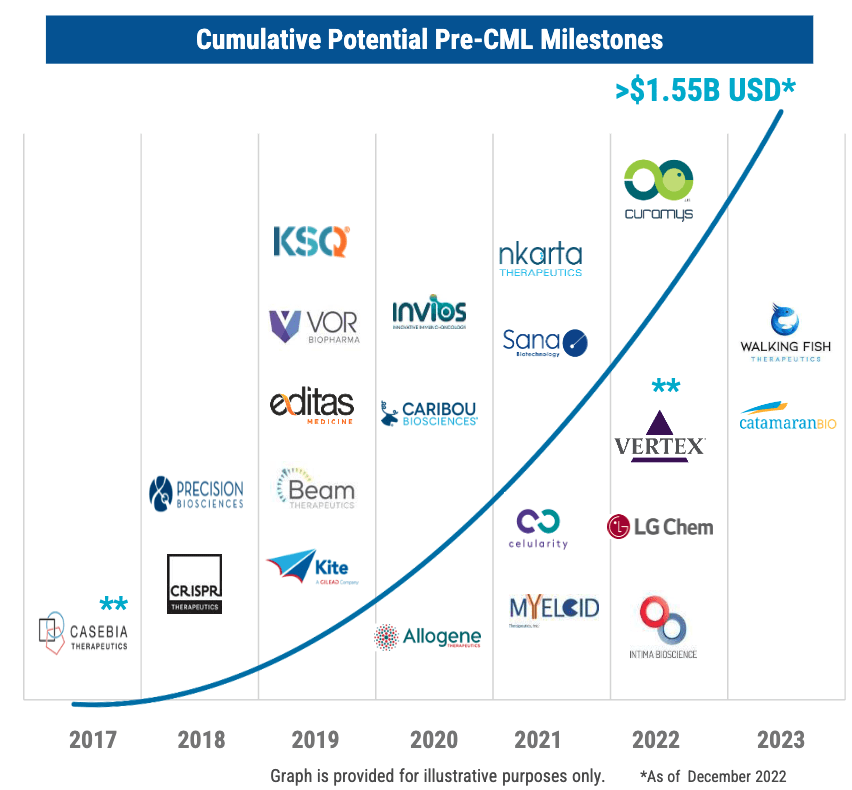

As its partners progress in their clinical programs, MaxCyte is given milestone payments. These pre-commercial milestones, if all successful, would net MaxCyte a total of $1.55 billion in revenue. These milestones alone represent a massive opportunity for the business and the stock as the current market capitalization is only $390 million at the time of writing.

Cumulative Milestones (MaxCyte Investor Presentation)

{kind=link}

Commercial Royalties

If a drug from an SPL reaches maturity, then MaxCyte will receive a royalty which will be a percentage of sales from that commercial drug. This revenue will be the crux of the long-term success of the business, but may not be meaningful in the short to medium term.

Thesis

We began following MaxCyte when they did their US IPO at $13.00 a share in 2021. The stock traded as high as $17.20 a share, but it has been all downhill since. As of writing, shares trade at $3.75, down 78.2% from the highs. However, there have not been substantial adverse developments in MaxCyte's business and there still remains substantial upside for shareholders if the company can get a reasonable number of drugs to market.

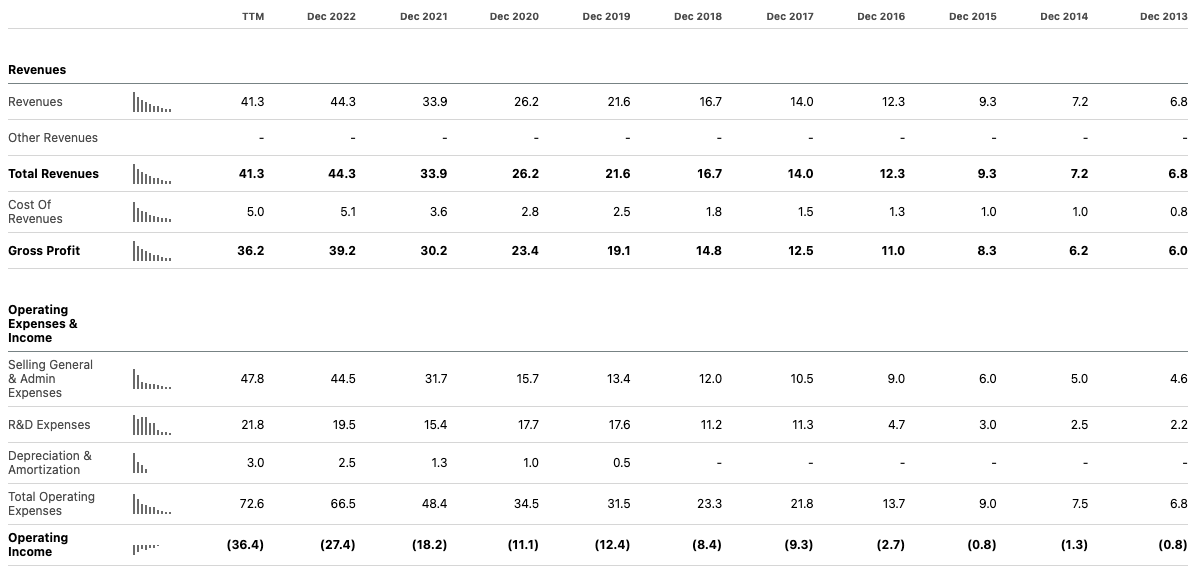

MaxCyte Income Statement (Seeking Alpha)

{kind=link}

While revenue has been growing at over 25%, losses have grown substantially and have remained much higher than revenue. The good news is that the company has an incredibly strong balance sheet with $224.7 million in cash and short-term investments. At the current rate of losses, MaxCyte has over 6 years of runway. While there is some concern that the losses will continue to accelerate, the upside from the successful commercialization of drugs and milestone payments more than compensates for this risk.

Revenues from SPLs (MaxCyte Investor Relations)

{kind=link}

We are still very early in cellular engineering and the development of revenues from MaxCyte's SPLs.

The key questions for the future value of MaxCyte are as follows:

- How many of the clinical programs eventually make it for commercialization?

- What will be the royalty payments received on average for any commercial drugs?

- How much of the $1.55 billion in potential milestone payments will MaxCyte earn?

- Will losses stabilize as the company scales?

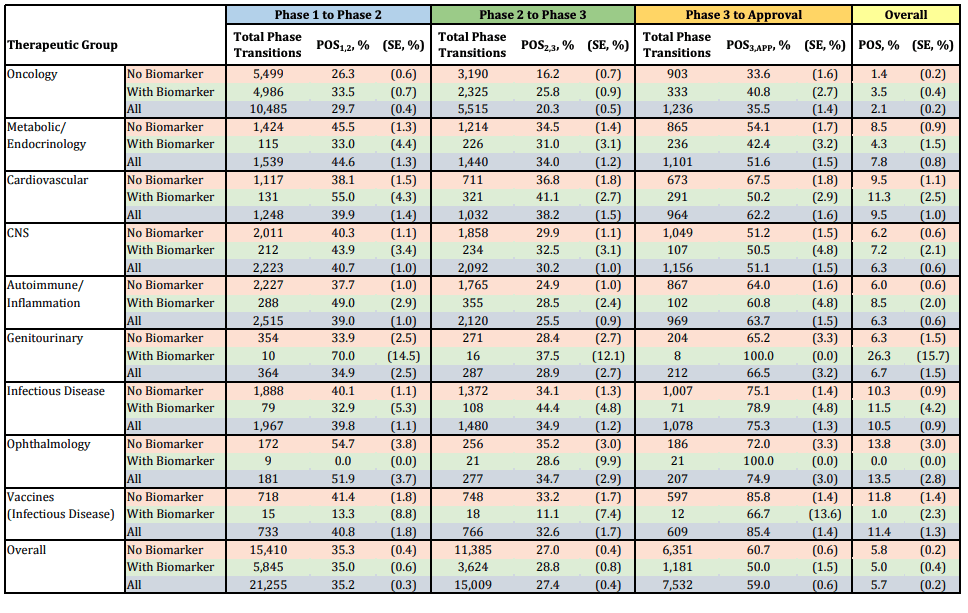

In order to determine what the fair value is for MaxCyte, we need to develop a framework to answer these questions. Let's start by estimating the number of clinical programs that will make it to commercialization. Data from the NIH shows that success rates vary widely with oncology success rates as low as 1.4% and certain Genitourinary drugs having success rates of up to 26%.

Success Rate By Drug Type (ncbi.nlm.nih.gov)

{kind=link}

While cellular therapies are not shown in the chart above, let's make the assumption that they are accepted at the overall average rate of 5%. Without taking into consideration the current phase of the 125 clinical programs, we can say that 5% of the 125 programs will succeed leading to an average of 6.25 drugs making it to commercialization.

So how much will each commercialized drug generate in sales? The most successful drug by projected 2023 sales will produce $23 billion in revenue. However, this would be a substantial overestimate of the average sales we can expect from MaxCyte SPLs. While the sales data for all 1,600+ approved FDA drugs, we estimate that the average revenue per year of such a drug is approximately $370 million. Across the 6.25 drugs, we anticipate making it to commercialization, which would be $2,312.5 million in annual revenue from which MaxCyte will be owed a royalty.

Each SPL has a negotiated royalty, so we have to make another assumption. To be conservative, let's assume that the royalty will be 2.5% of sales on average. So 2.5% of the $2,312.5 million in gross sales to partners will result in $57.81 million in net revenue to MaxCyte per annum.

Now this will not be the only source of value for MaxCyte as the business will also sell a significant number of disposables to commercial partners and earn substantial amounts from milestones along the way.

Given the number of assumptions we have had to make, I'd conservatively say that instrument sales and milestone payments offset the operating losses that we are seeing today. Further, I don't expect that royalties will be substantial for at least another 3 years.

MaxCyte Valuation (Author's Representation)

Again, there are a number of value drivers - such as instrument and disposables sales, milestone payments, and any additional SPLs signed by the company - that have not been included in this valuation. The valuation exercise here should show that the market has priced shares of MXCT below the value of future royalties and cash on the balance sheet. Even in this scenario, we have an upside of 60% from today's price.

Risks

We made a lot of assumptions to get a reasonable estimate of MaxCyte's value. Any variance in these assumptions could cause a dramatic shift in value per share.

For example, if approval rates for cell /gene therapies are in-line with oncology drugs long term at the low rate of 1.7%, then we would only expect 2.125 drugs making it to market. This would lead to a present value of equity of $359 million which would imply that shares of MXCT are still overvalued by roughly 7%.

Additionally, there is a key risk that costs continue to balloon at MaxCyte at a higher rate than the company earns revenue from milestones, disposables, or royalties. If MaxCyte is unable to offset its cost structure with high-margin revenues, then the fair value of the business is likely less than the present value of royalties plus cash as shown above. In the worst-case scenario, MaxCyte may burn through too much cash and be unable to tap capital markets for additional financing before substantial revenues come online. Given that the business has a 6-year run rate at current burn rates, I don't think this is a large risk.

Recent Turbulence

MaxCyte's share price has not fallen vertiginously without reason. In the past quarter, management lowered guidance for 2023 revenue and noted that they are lapping some comparable results in the past two years that will not be repeated going forward. Doug Doerfler, MaxCyte's CEO, explained in detail in the most recent earnings call . " It's important to note that in the first half of 2022, laboratories came back to near full capacity following COVID-19-related disruptions which resulted in elevated spending on instruments and PAs in that six-month period and has created a more difficult year-over-year comparison for the first half of 2023. "

Additionally, MaxCyte's partners have been increasingly cost conscious as they cannot tap equity markets for new capital as easily as in the years past. This has slowed progress in clinical programs with MaxCyte as well as a reduction in sales of equipment and disposables. Future revenue growth will be seasonal and somewhat unpredictable until the business has built a robust revenue stream from commercial stage SPLs.

Conclusion

While I find most biotech businesses to be too speculative, the platform-like business model makes MaxCyte a diversified collection of bets on a very promising new class of therapeutics. Given the strong balance sheet which should protect the downside reasonably well at today's share prices and the possible upside, MaxCyte is a compelling bet at today's share price.

For further details see:

MaxCyte: Engineering The Next Biotech Wave