MXCT - MaxCyte: Picking Up This Pick And Shovel Play For Next-Gen Therapies

2023-04-12 04:49:05 ET

Summary

- MaxCyte’s flow electroporation technology has made them the industry leader and the best bet for biotech companies that need a partner that specializes in non-viral cell engineering.

- MaxCyte’s revenue mostly comes from milestone and royalty payments for licenses and SPLs who are looking to use their technology to develop and commercialize cutting-edge therapies.

- I believe MXCT is a perfect Pick and Shovel ticker for cell and gene therapies. I am giving MXCT a conviction level of 3 out of 5.

- MXCT offers an attractive risk/return profile for investors that want exposure to the cell and gene therapy area, but do not have the risk appetite to invest directly in the space.

The recent boom in cell therapies and gene therapies has created a new industry that specializes in the tools and services needed to discover, develop, manufacture, and commercialize these therapies. Admittedly, most of this industry has existed for a considerable amount of time, however, the recent approval and commercialization of these cutting-edge therapies have increased the need for more players and technologies. MaxCyte ( MXCT ) is one of the established players in the cell and gene therapy arena with their cell therapy platform and electroporation products. MaxCyte offers leading cell engineering technology, enabling the development of a growing set of advanced cell-based therapeutics for its partners. MaxCyte is positioned to benefit from the growing interest in these therapies making it an attractive pick-and-shovel play.

I am attempting to find an opportunity to establish a respectable speculative position in MXCT stock this year.

I intend to discuss why I like “Pick and Shovel” healthcare investments. In addition, I provide some background information on MaxCyte and their recent performance. Then, I present my thesis and how I intend to initiate a position in MXCT.

Pick and Shovel

Although I do love reading research papers and studying clinical trial data, I have to admit that trying to stay on top of pharmaceutical and biotech companies can be laborious at times. One could spend hours reading through a company's 10-Ks, presentations, earnings, and clinical data readouts to ultimately figure out whether the company or the ticker is a hard pass. So, whenever I come across a promising “Pick and Shovel” play, I am happy to forgo the clinical data overload and focus on the business model and financial performance. In biopharma, we have several different types of pick-and-shovel companies that can either support the discovery of drugs, the development of drugs, manufacturing, distribution, logistics, patient management, etc. These companies have business models that allow them to receive upfront, milestone, and/or royalty payments from partner programs. The obvious benefit here is that a pick-and-shovel company is not taking on the risk of developing a drug and relying on its commercial success. What is more, these companies can have numerous partners that employ the same product or service, which allows for multiple revenue streams and attractive margins. If that pick-and-shovel company becomes a market leader, they will become the “Go-To” partner for their products or services, which often leads to a steady stream of new and repeat partnerships.

As a result, investing in a healthcare pick-and-shovel company allows you to have exposure to some of the most lucrative industries, but without the binary risk-reward profile that is associated with the end developer or owner of the drug/therapy. In some ways, you can see some of these tickers as an ETF, where you have exposure to a sector or industry instead of a singular company. If the industry grows, the pick-and-shovel company should grow with it.

Looking at the figure below, we can see how MaxCyte fits this model.

{kind=link}

Background of MaxCyte

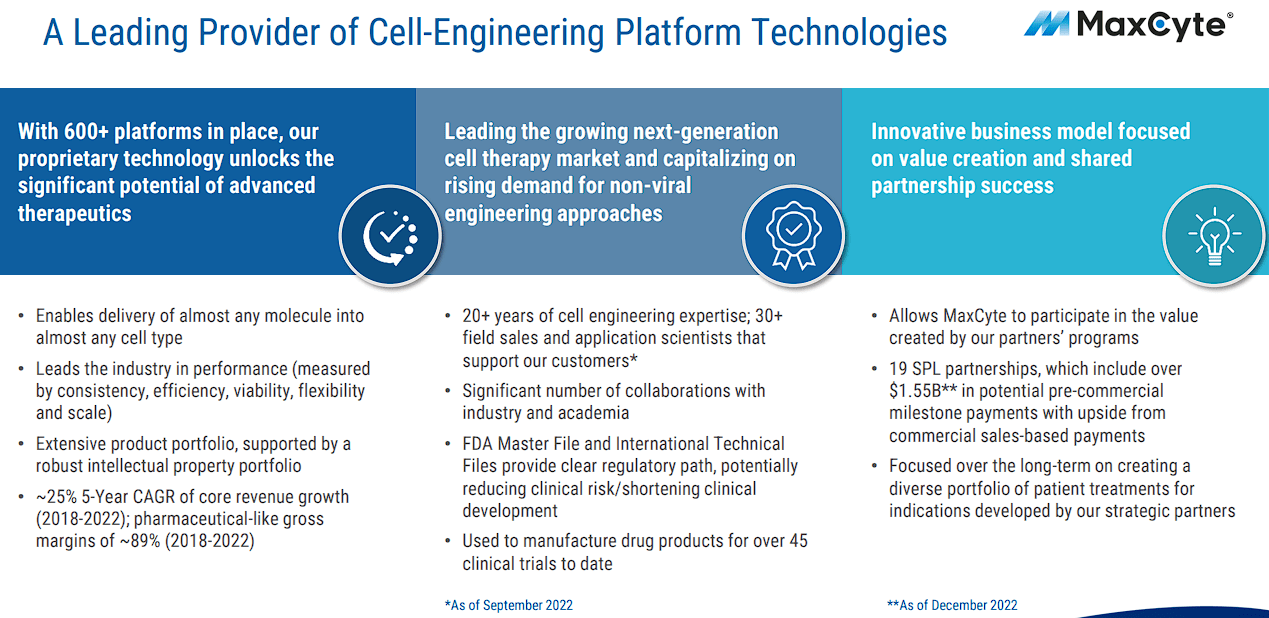

MaxCyte has over 20 years of perfecting their cell engineering prowess to construct their Flow Electroporation technology and transfection workflow.

What Is Their Flow Electroporation?

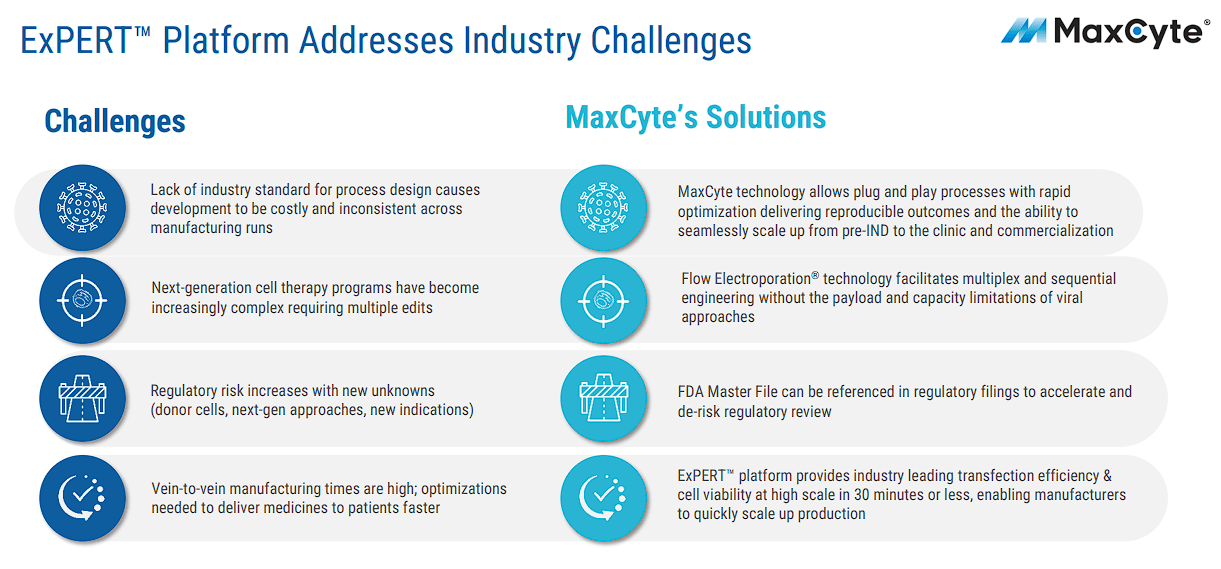

Electroporation is a non-viral transfection method that relaxes cell membranes, thus, permitting genetic payload to pass into the cell. What makes MaxCyte’s flow electroporation technology unique is that it allows cells to flow recurrently into the processing chamber where distinct volumes are electroporated, then continuously collected. These attributes allow cell and gene therapies to be engineered at an outsized scale compared to other electroporation options.

Their industry-leading high-efficiency ExPERT instruments improve cell viability and scalability that can be employed from discovery to commercialization. MaxCyte is considered one of the leaders in electroporation with best-in-class technology that works in all cell forms including primary cells, stem cells, and cell lines. Furthermore, the company's technology yields high cell viability and transfection efficiencies consistently in excess of 90% . These instruments transfect at enhanced timelines with the additional advantage of reduced manufacturing expenses. What is more, these efforts produce work that is cGMP-compliant, even at a large-scale.

{kind=link}

So, MaxCyte’s products and services should be attractive for both companies just getting started with their R&D and a commercial company looking to scale up to billions of cells.

Who Are MaxCyte’s Customers and Partners?

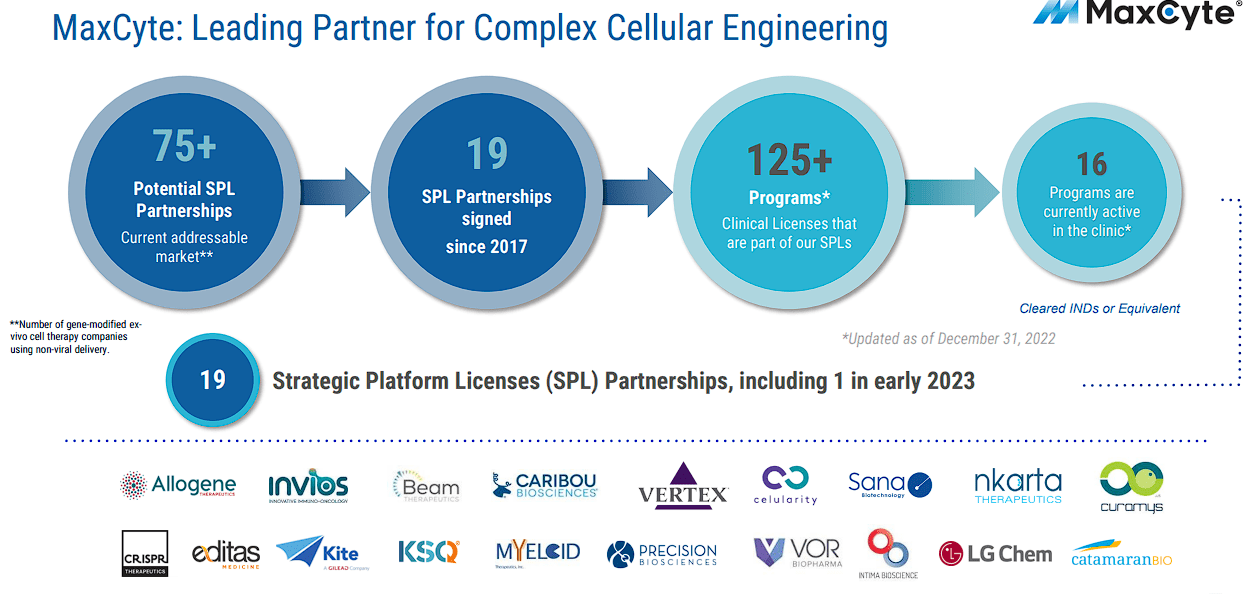

MaxCyte supplies products and services for cell therapy, gene editing, cell-based assays, viral vector production, antibody production, protein production, and vaccines. MaxCyte’s global customer base is involved in all stages of development, in particular, cell therapy customers in the early development stages. As of their last update, MaxCyte’s total number of strategic platform license “SPL” partnerships is at 19, and the company is confident in their ability to amass new partners in the coming years. Recently, MaxCyte signed an SPL partnership with Vertex ( VRTX ) which has the clinical and commercial rights to employ MaxCyte’s technology for the development of exa-cel (CTX001), which is an autologous, ex vivo CRISPR/Cas9 gene-edited therapy for sickle cell disease “SCD” and transfusion-dependent beta-thalassemia “TDT”. Admittedly, MaxCyte’s technology was already used in the development of exa-cel under an agreement with CRISPR Therapeutics ( CRSP ), so it isn’t big news for the platform. However, the Vertex agreement entitles MaxCyte to licensing fees and program-related revenue. Considering Vertex recently completed exa-cel’s BLA, we could see some of that entitled revenue in the near term.

{kind=link}

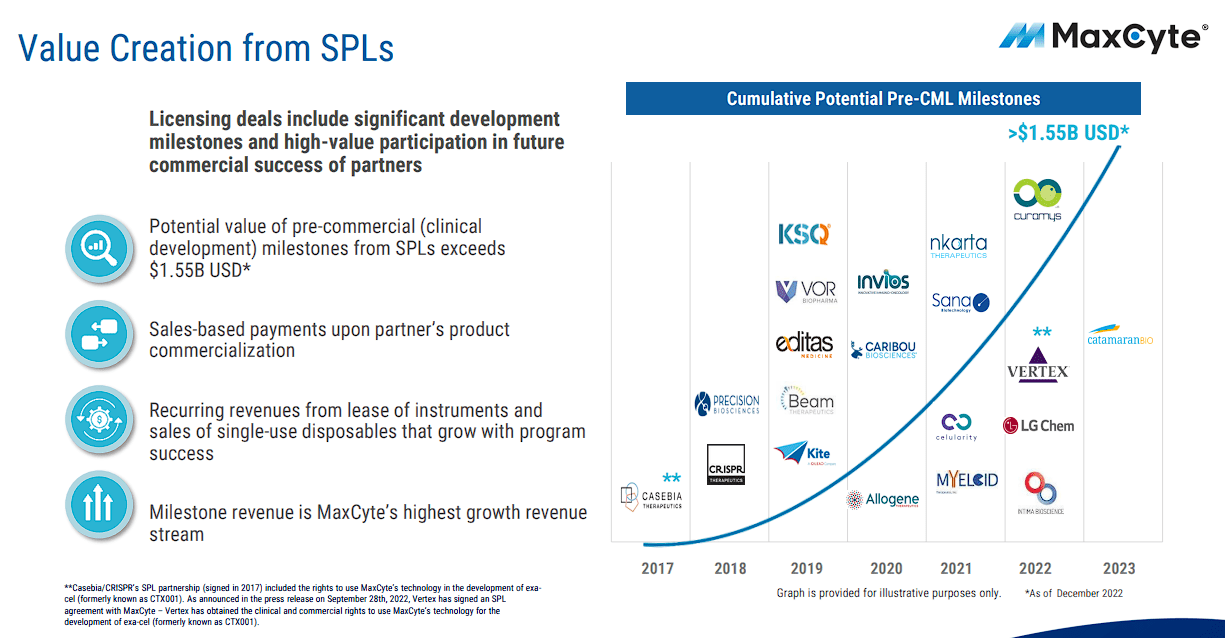

To get an idea of what these partnerships can deliver in terms of revenue, the company believes that the potential value of their pre-commercial milestones from SPLs is greater than $1.55B. In addition, the company should have sales-based revenue from the products and recurring revenue from the lease of instruments as well as disposables.

{kind=link}

Again, this is only for their current SPL partnerships, so there is potential growth from additional SPL partnerships and other customers.

Recent Performance

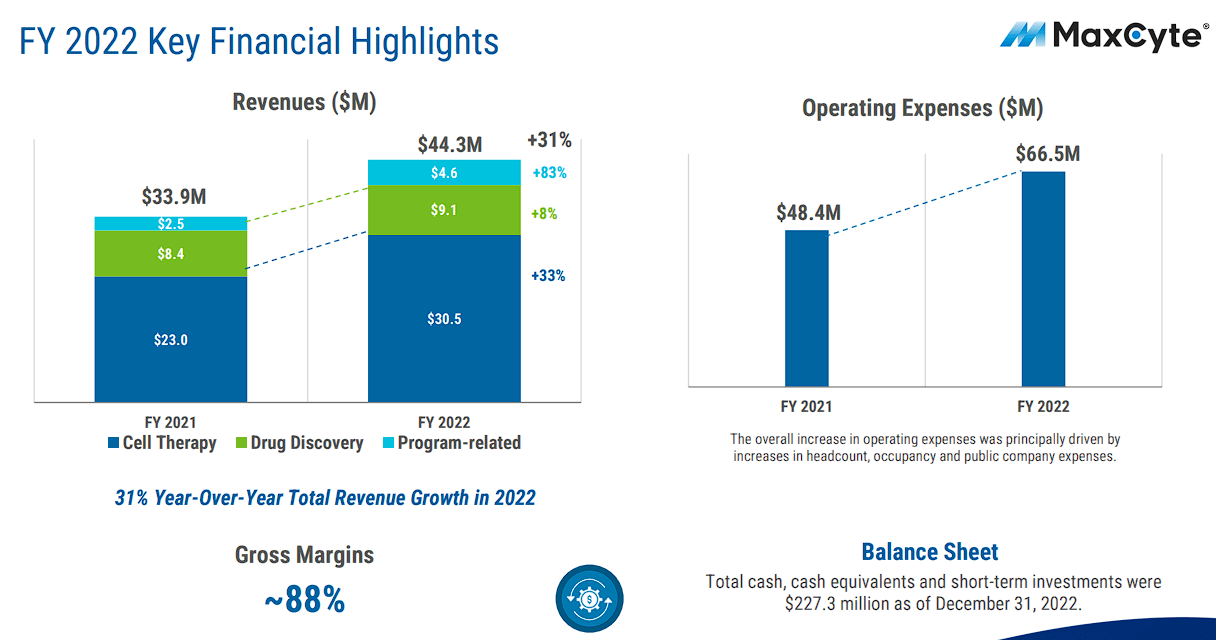

MaxCyte has been establishing a solid growth record since going public. The company’s recent Q4 earnings revealed a beat on EPS and a miss on revenue. However, the company was still able to report year-over-year revenue growth. For the full year, MaxCyte pulled in $44.3M, which is up from $33.9M in 2021. However, OpEx went from $48.4M in 2021, to $66.5M in 2022. In addition, MaxCyte left 2022 with a healthy bankroll of $227.3M in total cash, cash equivalents, and short-term investments.

{kind=link}

The company set their initial 2023 guidance for total revenue growth of 21% to 26% from 2022. What is more, MaxCyte expects their core revenue to grow 20% to 25% over 2022 with SPL revenues coming in around $6M.

Expanding The Business

MaxCyte has been working hard to improve their products and services including more than tripling their manufacturing space and process development facilities. MaxCyte is continuing to launch new products to service their customers and build out their capacity including adding automation. Moreover, MaxCyte is looking into expanding their core technology with process analytics and product characterization.

In September, the company formally launched MaxCyte’s ExPERT VLx large-scale transfection system, which improves scale for development and manufacturing across an expanse of uses, such as transient proteins. The VLx is expected to have broad compatibility and will help cut development timelines during preclinical development and clinical trials. The VLx system unleashes a new market prospect for MaxCyte, which supports their long-term revenue growth prospects.

{kind=link}

Not only will they be able to serve more customers, but they should also have a broader portfolio of products and services to offer.

My Thesis

My MXCT thesis can be simplified into ingredients and recipes. When I look at MaxCyte, I see that they have all the ingredients needed to promote growth and the recipe to follow to ensure they do it right. First and foremost, MaxCyte finished 2022 with a strong balance sheet to support their estimated growth. Second, MaxCyte's ExPERT platform appears to be market-leading and is an empowering technology in the company’s partner's therapeutic development strategies. Third, MaxCyte’s partners are well-funded and frontrunners in the cell therapy industry pioneering gene-editing and cell engineering methods.

{kind=link}

So, MaxCyte has the cash, the product, and the customers… that seems like some quality ingredients needed for growth.

MaxCyte also has a reliable recipe that makes them the clear choice for customers looking for reliable products and services. From a potential partner or customer perspective, MaxCyte has a solid track record of making significant investments to enhance their ability to service new markets, and be competitive in emerging therapeutic developments that are preparing for the clinic and then commercial launch. If I am going to initiate the development of a cell or gene therapy, I am going go with the company that has a strong resume of success and is known to make MaxCyte investments that expand their offerings to their current and prospective partners, thus, fortifying their position at the top of the industry.

MaxCyte just needs to remain the go-to partner for these cell and gene therapy companies, who cannot risk using subpar equipment to perform R&D and to use in commercialization. By bolstering their position as the industry leader, they stand to benefit from this expanding market.

Moreover, MaxCyte is a pick-and-shovel player in this industry, so the company has little-to-no risk even if the partner’s cell therapy fails to make it through the FDA. The company would still have numerous other programs to collect revenue from and maintain its growth trajectory. As long as the cell therapy industry continues to expand, we should see MaxCyte’s revenue continue to swell in the coming years. In fact, Street analysts anticipated MaxCyte to report strong double-digit growth in the coming years and will essentially double by 2025.

{kind=link}

That level of growth typically bodes well for the share price and the ticker’s long-term outlook.

Last, but not least, we have to expect that larger life sciences tools and services companies such Thermo Fisher ( TMO ), Repligen ( RGEN ), or Bio-Rad ( BIO ) would consider adding MaxCyte to their portfolio. Considering MaxCyte is considered the industry leader, it should fetch a premium valuation.

Risks

MaxCyte has a few risks that you need to consider when managing your position. Primarily, there is the possibility their partnered programs don’t make it through the FDA and onto the market. The company’s primary value driver is the potential payments and royalties from those programs. So, a failure in the clinic will hurt the company’s valuation and long-term outlook. Another major concern is competition, which is limited at this point in time, however, the industry is expanding so I have to believe there are potential competitors looking to find an opportunity to capture some of MaxCyte's market. Obviously, competition will be a looming threat that could weigh on the share price.

Another risk to consider is that MXCT is an underfollowed ticker with less than 1,000 followers on Seeking Alpha and has been a publicly traded company for less than two years. So, it is possible that the company will continue to make significant progress, but the news will travel under the radar and the ticker barely responds to any positive update.

Despite these concerns, I am still bullish on MXCT and have assigned the ticker a conviction level of 3 out of 5.

My Plan

Typically, I like to initiate a position in a speculative ticker with a minuscule-sized buy to get my feet wet and will stick to a consistent schedule of making small periodic investments over the next few years until I reach a full-sized position. Indeed, I do look to book profits throughout this time period, however, I attempt to reapply the original investment once the ticker recedes back to my Buy Threshold. For MXCT, I am planning on taking a more aggressive approach by starting with a larger position that will allow me to book a larger profit earlier and quickly transition the position into a "house money" status. This would essentially de-risk the remaining shares, thus, allowing me to maintain a speculative position for a long-term investment.

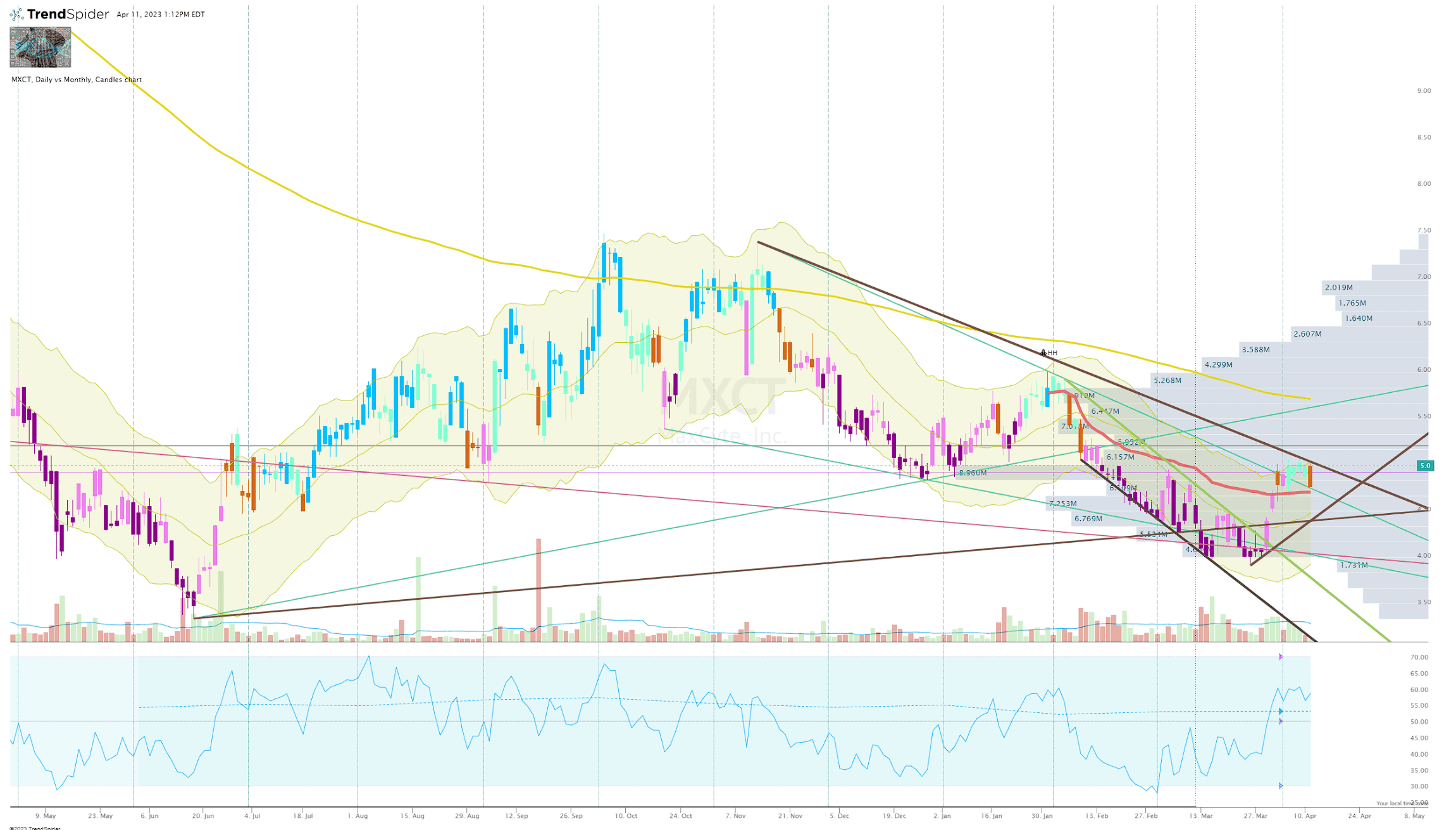

I am setting my Buy Threshold to $5.00 per share, which will be the most I am willing to pay for MXCT at this time. Once the share price dips below $5 per share, I will look for a high conviction reversal setup before clicking the buy button.

{kind=link}

MXCT Daily Chart Enhanced View ( TrendSpider )

Long-term, I expect to manage an MXCT position for at least five years in anticipation the company will continue to grow with their market and benefit from their extensive list of partnerships. Ultimately, I expect MXCT to graduate from my speculative “Bio Boom” portfolio and move to the “Bioreactor” growth portfolio.

For further details see:

MaxCyte: Picking Up This Pick And Shovel Play For Next-Gen Therapies