MXCT - MaxCyte: Still Bullish Despite Soft Q2 Earnings

2023-08-21 17:18:40 ET

Summary

- MaxCyte reported a 5.9% decrease in Q2 revenue, attributing it to funding environments and the prioritization of internal pipeline assets.

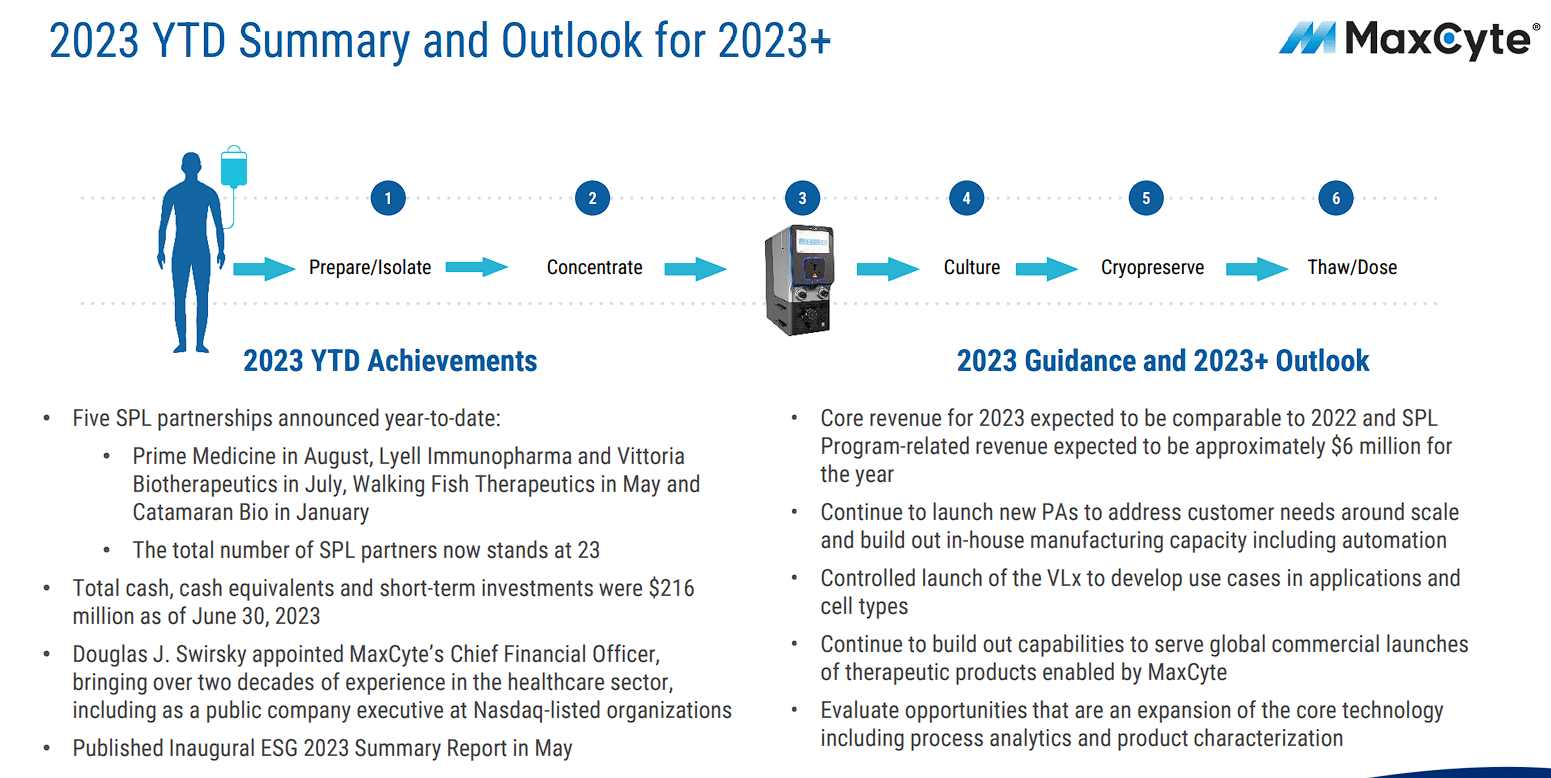

- The company remains optimistic about their Strategic Platform License revenue and has signed five partnerships this year, bringing the total to 23.

- MaxCyte finished the first half of the year with $216.1M in cash and believes it will support their future plans for profitable growth.

MaxCyte ( MXCT ) recently reported their Q2 earnings with a beat on revenue, and a 5.9% decrease year-over-year. The company's "core business" took a hit in Q2, only pulling in $8.3M, a 14% drop from Q2 of last year. MaxCyte attributed this lackluster performance to the life sciences' "funding environments" and companies moving towards the "prioritization of internal pipeline assets". The uninspiring earnings amped up the selling pressure, pushing the ticker down roughly 15% over the past week. Even with the market's headwinds, the company is still optimistic about their Strategic Platform License "SPL" revenue, and they expect about $6M for 2023. Furthermore, MaxCyte reported that they have signed five SPL partnerships year-to-date, which brings their "total number of SPL partnerships" to 23. Moreover, the company finished the first half with about $216.1M in cash, cash equivalents, and short-term investments, which MaxCyte believes will support their "future plans for profitable growth." Despite the market's reaction to the earnings, I am still bullish on MXCT on account of the company's impressive pipeline of ongoing and projected licensing agreements that hold significant value that is not being manifested in the share price. Therefore, I am looking to add to my MXCT position once MaxCyte sees an attractive reversal setup on the daily chart.

I intend to review the company's earnings results and provide my views on the quarter. Additionally, I will discuss why I am still bullish on MXCT and its long-term potential. Then, I will point out some downside risks that investors need to consider when managing their MXCT position. Finally, I will present my plan for adding to my position as MaxCyte moves closer to Q4 of 2023.

Q2 Review

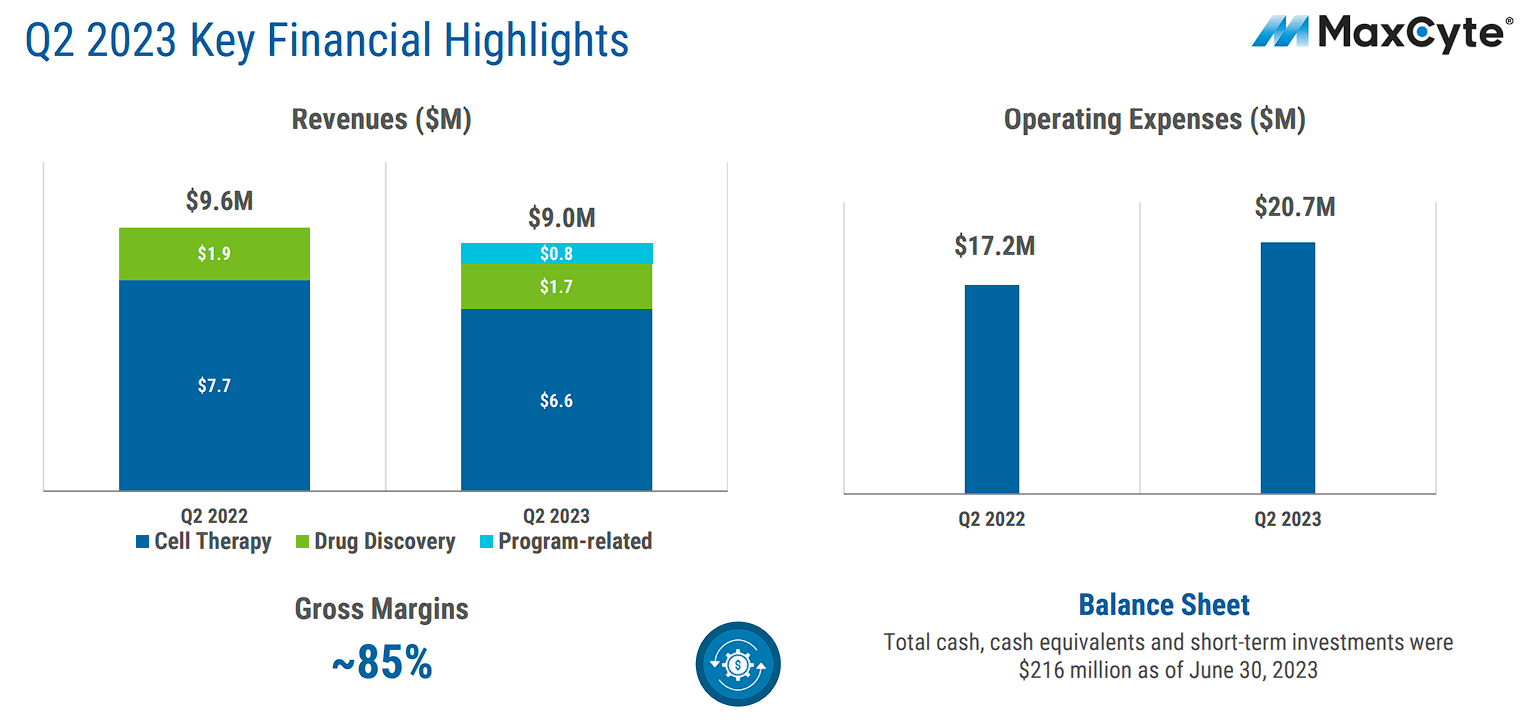

MaxCyte reported that their Q2 total revenue amounted to $9M, showing a 6% drop from Q2 of 2022. In Q2, MaxCyte's core revenue was $8.3M, marking a 14% reduction matched to Q2 of 2022. MaxCyte's core business, instrument, and PA sales were down by 24% in the first half of 2023 vs 1H of 2022. This decline encompassed a 14% year-over-year decrease in revenue from cell therapy customers, amounting to $6.6M, and a decline of the same magnitude in revenue from drug discovery customers, which totaled $1.7M. Revenues from leased instruments remained stable, experiencing a 2% growth in the first half of 2023 over the first half of 2022 mainly driven by MaxCyte SPL partners. MaxCyte documented $0.8M in SPL program-related revenue, showing the progress of MaxCyte partners in clinical trials.

MaxCyte Q2 Financial Highlights (MaxCyte)

{kind=link}

Digging into the financials, MaxCyte's gross margin for Q2 2023 came out to 85%, down from 88% in Q2 of last year, partly affected by enlarged in-house manufacturing and associated production costs. Total OpEx accumulated to $20.7M, up from $17.2M in Q2 of 2022. This bump in expenses was primarily due to an increased headcount in R&D, sales, and marketing. At the end of the quarter, MaxCyte had roughly $216M in combined cash, cash equivalents, and short-term investments. It is important the company has no debt.

MaxCyte attributed their cut in revenues to their difficult operating environment, which led to the industry prioritizing their R&D pipeline programs and assets. As a result, the company saw protracted purchasing cycles from their customers. Note that the first half of 2022 saw amplified demand as a result of pent-up purchasing succeeding COVID-related policy deviations and robust revenue growth from an approaching commercialization SPL partner.

The company also revealed that they are seeing prolonged purchasing cycles resulting in lower PA usage in the first half of this year. The company believes this was due to some R&D programs being moved to the back burner among earlier-stage customers and a drop in PA demand from a late-stage program that has reached the end of the regulatory pathway.

Consequently, MaxCyte has revised their full-year 2023 guidance and core revenue to be in the same ballpark as 2022. MaxCyte's expectations for their SPL program-related revenue remained roughly the same at around $6M for the year. This updated guidance factors in the cautious approach necessitated by the demanding macro environment and the scheduling of client and partner purchasing patterns.

MaxCyte First Half Highlights (MaxCyte)

{kind=link}

My Views On The Quarter

Despite facing some hurdles, MaxCyte reported $9M in revenue for Q2, with a 6% drop compared to Q2 of 2022. Clearly, this is a bit concerning, especially since core business revenues, including cell therapy and drug discovery customers, declined by 14%. However, I am focusing on the causes of the drop in revenues. The company reported protracted purchasing cycles from clients contributed to this decline. Yet, MaxCyte updated their full-year 2023 guidance, anticipating core revenue to be similar to 2022. Obviously, we want to see growth over 2022, but considering the macro-environment, I am content with maintaining their position.

Another point to address is the fact that MaxCyte's OpEx increased. However, the increase in expenses was mostly driven by investments in their R&D, sales & marketing, and other growth efforts. Thankfully, the company has plenty of cash, which positions MaxCyte well for future profitable growth and attaining long-term objectives.

Yes, it wasn't a great quarter, but the macro-environment and purchasing cycles prevented them from reporting growth. The MaxCyte CEO mentioned in the earnings call as a "belt-tightening" among early-stage companies. So their drop in earnings performance was not primarily attributable to competition but rather related to financial constraints faced by early-stage companies.

The important point to consider is that the company saw a surge in revenue in the first half of 2022, so the year-over-year drop in revenue is a byproduct of pent-up demand left over from COVID.

Why I Am Still Bullish

Despite Q2's setback, I am still bullish on MaxCyte for a number of reasons. Primarily, the company's partnership pipeline remains robust, with five partnerships established this year. MaxCyte has one of the leading cell engineering platforms that has yielded products that are arguably critical pieces of the evolving cell therapy industry.

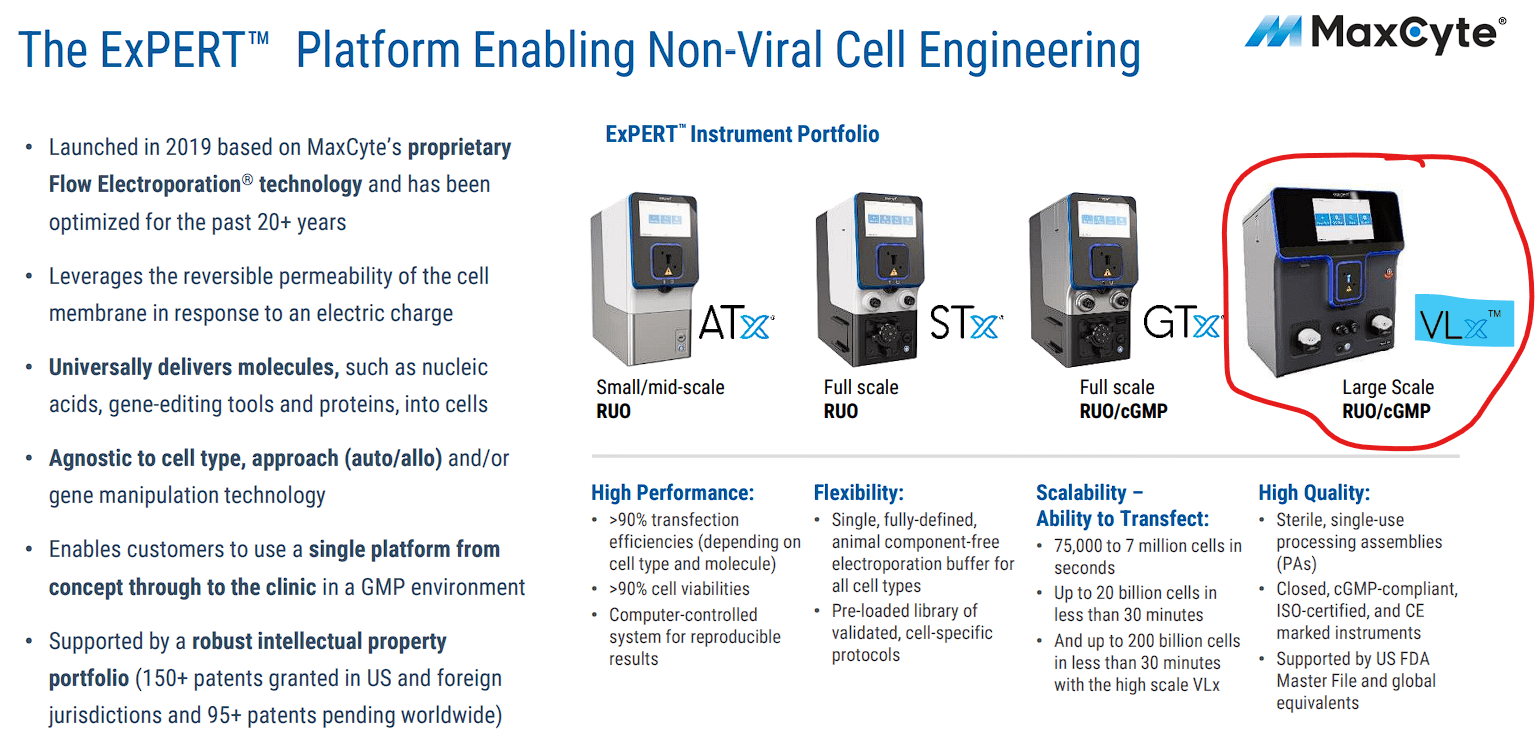

In addition, MaxCyte's platform is well-suited for industry trends moving towards non-viral cell engineering modalities, especially for next-gen therapies. If the industry is going to grow... it is likely that MaxCyte will benefit from it. In fact, MaxCyte's ExPERT VLx Large-Scale Transfection System is also gaining traction, offering potential applications in transient protein manufacturing and pre-clinical development. That system can transfect up to 200 billion cells in less than 30 minutes with a cGMP rating. So, the company seeing a bump in VLX sales tells me that cell therapy companies are preparing/prepared for large-scale development or commercialization.

MaxCyte ExPERT Platform (MaxCyte)

{kind=link}

I am also happy with how MaxCyte is proactively navigating the volatility of the cell therapy industry. In the face of industry challenges, MaxCyte's focus on finding the right strategic partnerships; developing and maximizing their innovative technologies; and being in a strong financial position gives me confidence that MaxCyte will achieve its long-term goals and that its technology's value to the industry remains strong.

Despite their recent setback, I still maintain a positive outlook and am eager to see the potential growth from MaxCyte's partnership signings and evolving pipeline.

Risks To Consider

As I mentioned in my first MaxCyte article , the ticker has a few risks that you need to consider when managing your MXCT position. Primarily, there is the prospect that their partnered programs don't make it past the FDA's review and onto the market. MaxCyte's prime value driver is the forecasted milestones and royalties from those companies. Therefore, a lackluster result from one of their partnered programs will put a dent in the company's valuation and long-term outlook. Of course, there is always the looming concern of competition, which is narrow at this point in time; nevertheless, the industry is growing, so I have to expect there are stalking competitors eyeing MaxCyte's prospective partners. For me, the biggest threat is Thermo Fisher ( TMO ), which is in the same markets as MaxCyte and is clearly one of the biggest life sciences companies in the world. Although MaxCyte might have some advantages with their technology, we shouldn't be surprised to hear if Thermo-Fisher is able to acquire or develop a viable challenger to MaxCyte's tech. Obviously, in general, competition will be a lurking threat that could put some drag on the share price until a clear leader is determined, but a competitive product from one of the juggernaut life sciences companies could really hurt MaxCyte's long-term outlook.

I will also reiterate that MXCT is an underfollowed ticker with barely over 1,000 followers on Seeking Alpha and has been a publicly traded company for roughly two years. So, it is likely that the company will continue making progress, but the majority of retail investors will be unaware, leaving algorithms to do most of the trading volume. This can be a positive in some aspects, but MXCT investors should not expect updates and traditional catalysts to have a significant impact on the share price, nor a lasting response.

Lastly, we have to consider whether the current cell therapy market environment will persist for a protracted period of time, and if MaxCyte fails to meet Street expectations. Failing to report significant growth is not only a problem for the company's financials but will also make MXCT a target for short sellers due to the company's relatively rich valuation grades.

Considering these concerns, I am changing MXCT's conviction rating from 3 out of 5 to 2 out of 5 and will remain in the Compounding Healthcare "Bio Boom" speculative portfolio for the foreseeable future.

My Plan

My MXCT position has been in hibernation after establishing a small position back with only a couple of minuscule additions. Indeed, my Bio Boom tickers are rarely ever sizable due to their speculative nature, but my MXCT position is embarrassingly small. I am looking to change my position's condition in the near future to take advantage of the prolonged sell-off that is grinding MXCT's valuation down to an attractive level. However, I am going to remain cautious until the technical indicators improve for the ticker.

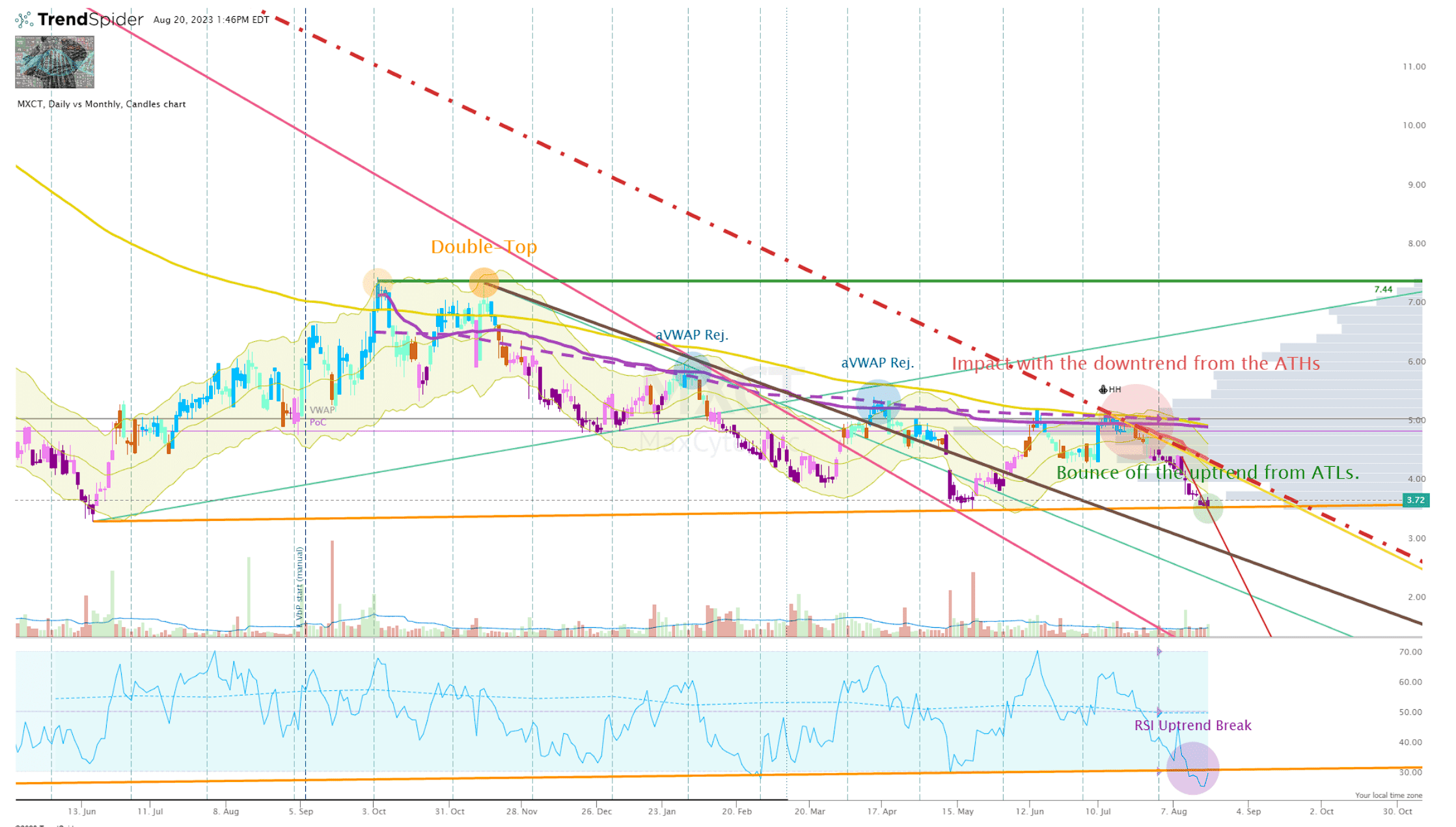

Currently, the MXCT Daily Chart looks quite bearish following a "Double-Top" in October of last year that created a nasty aVWAP that has suffocated every minor rally in the share price since.

MXCT Daily Chart (Trendspider)

{kind=link}

MXCT Daily Chart Enhanced View ( Trendspider )

The share price was showing a nice bullish reversal setup in July of this year, but the potential breakout ran right into a downtrend ray from the all-time high (dotted red line) that deflected the momentum, breaking the long-term RSI uptrend. Since then, the ticker has struggled to record a green day of trading and is now sitting just above an uptrend from all-time lows. The ticker did break the recent downtrend generated from the earnings report, so perhaps we will see a quick bounce here. However, we can see huge volume shelves above, so the ticker is probably going to need a positive update along with both the healthcare sector and the overall market to rally and clear that overhead volume. Unfortunately, though, I must concede that the path of least resistance is lower.

So, I am going to remain patient and wait for a few bullish indicators to light up before I even consider clicking the buy button below my one of my Buy Targets.

Once I see a high conviction reversal setup, I will make a small addition. Then, I will wait for a confirmed reversal before making an upsized buy order below my Buy Threshold, which should hold me over for the second half of the year.

As soon as my orders are filled, I will set a sell order at my Sell Targets to move my position into a "House Money" status in order to de-risk the position while maintaining a core position that is funded by remaining profit.

I expect to stick to plan for the remainder of 2023, however, the company did mention an upcoming partner approval event in their earnings call, which could potentially impact the company's revenue picture. They hinted at milestone payments and royalties associated with this approval but they didn't provide specific figures. This would have a significant impact on their near-term and long-term financial outlook and should have a positive impact on the ticker. Obviously, this would encourage me to revamp my MXCT strategy.

Furthermore, the company expects to see a stronger Q4. If the earnings report hits above expectations, I might consider revising my plan if we see some optimistic support from the market.

Long-term, I am interested in making MXCT one of the larger holdings in the Bio Boom portfolio due to it being a nice "Pick and Shovel" ticker and my expectation that MaxCyte will ultimately achieve profitability, and in turn, graduate to the "Bioreactor" growth portfolio.

For further details see:

MaxCyte: Still Bullish Despite Soft Q2 Earnings