RIO - McEwen Mining: Don't Chase The Stock Here

Summary

- McEwen Mining Inc. is one of the best-performing stocks year-to-date, up 21% vs. a flat return for the S&P 500.

- These returns have complemented an already impressive Q4 performance, with McEwen Mining up 79% in Q4 and outperforming its benchmark, the Gold Juniors Index.

- However, I don't see this move supported by fundamentals, and while McEwen Mining may have been reasonably valued at lower levels, I see limited margin of safety above US$7.00.

- Given McEwen Mining's track record of consistent share dilution and its relatively marginal operating assets, I see this rally above US$7.05 as an opportunity to book some profits.

While 2022 was a year to forget for the major market averages with double-digit declines in the S&P 500 Index (SP500) and Nasdaq Composite (COMP.IND), the Gold Juniors Index ( GDXJ ) managed to outperform. An unsuspecting stock was one of the best performers: McEwen Mining Inc. ( MUX ). This outperformance was partially attributed to the recovery in gold, but also to McEwen Mining having a copper asset that it wasn't getting much value for, which appears to be reflected in the stock finally. That said, its primary operations haven't seen much improvement, and San Jose's costs (49% interest) have remained elevated, impacting income from this asset. So, with the core business leaving much to be desired, I don't see any way to justify chasing MUX above US$7.00.

{kind=link}

Q3 Results

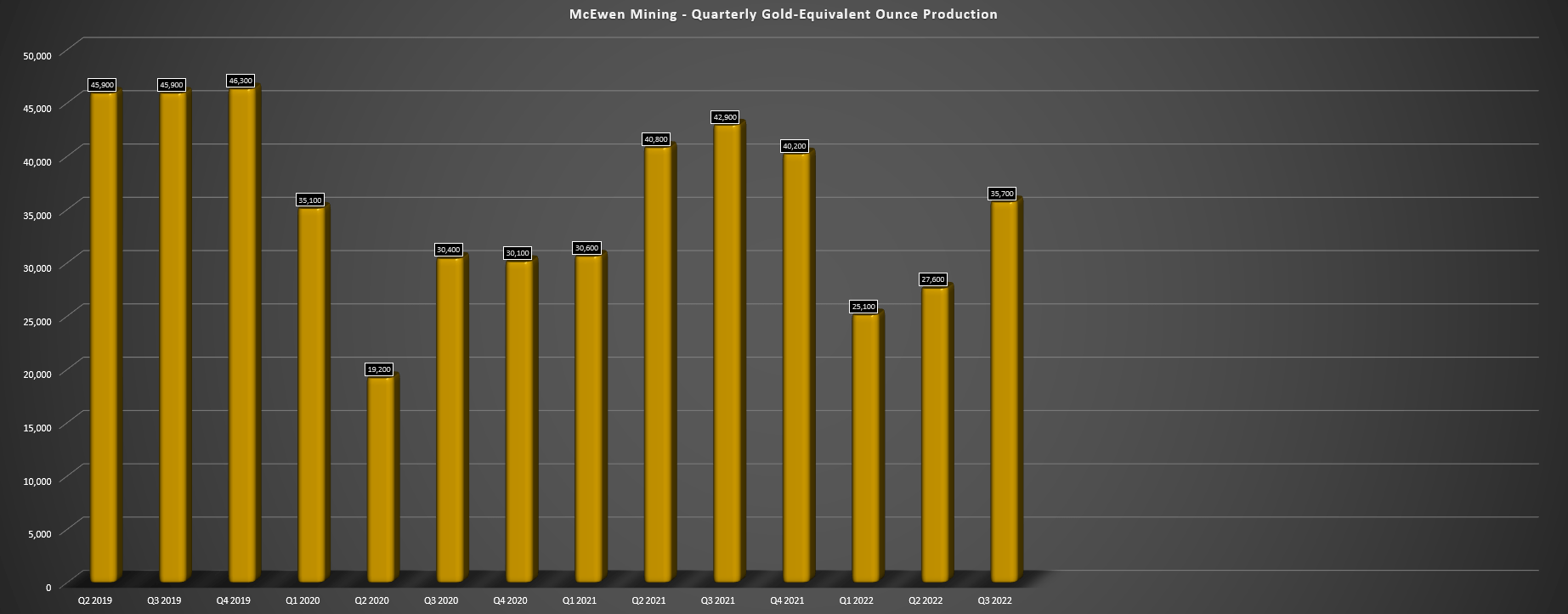

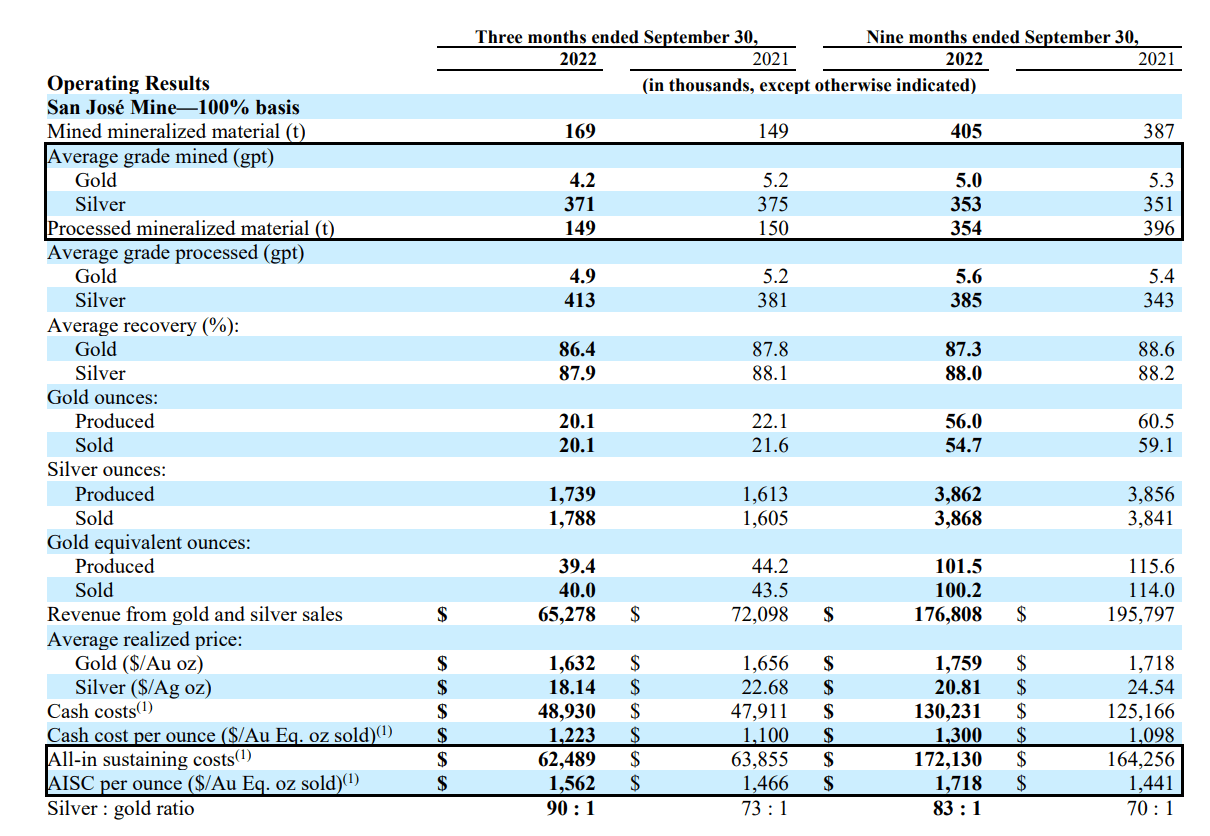

McEwen Mining released its Q3 results in November, reporting quarterly production of ~35,700 gold-equivalent ounces (including San Jose interest), a 17% decline from the year-ago period. This was related to lower production at San Jose due to lower grades and recoveries, and costs remained elevated at the asset, with all-in-sustaining costs [AISC] of $1,562/oz, impacting McEwen Mining's investment income in the period ($0.8 million). Meanwhile, at McEwen's primary operations, the Fox Complex had a better quarter and a much better year thus far, but this was offset by Gold Bar, where production fell to 7,200 ounces of gold at industry-lagging AISC of $2,049/oz. Let's take a closer look at the quarter below:

McEwen Mining - Quarterly GEO Production (Company Filings, Author's Chart)

{kind=link}

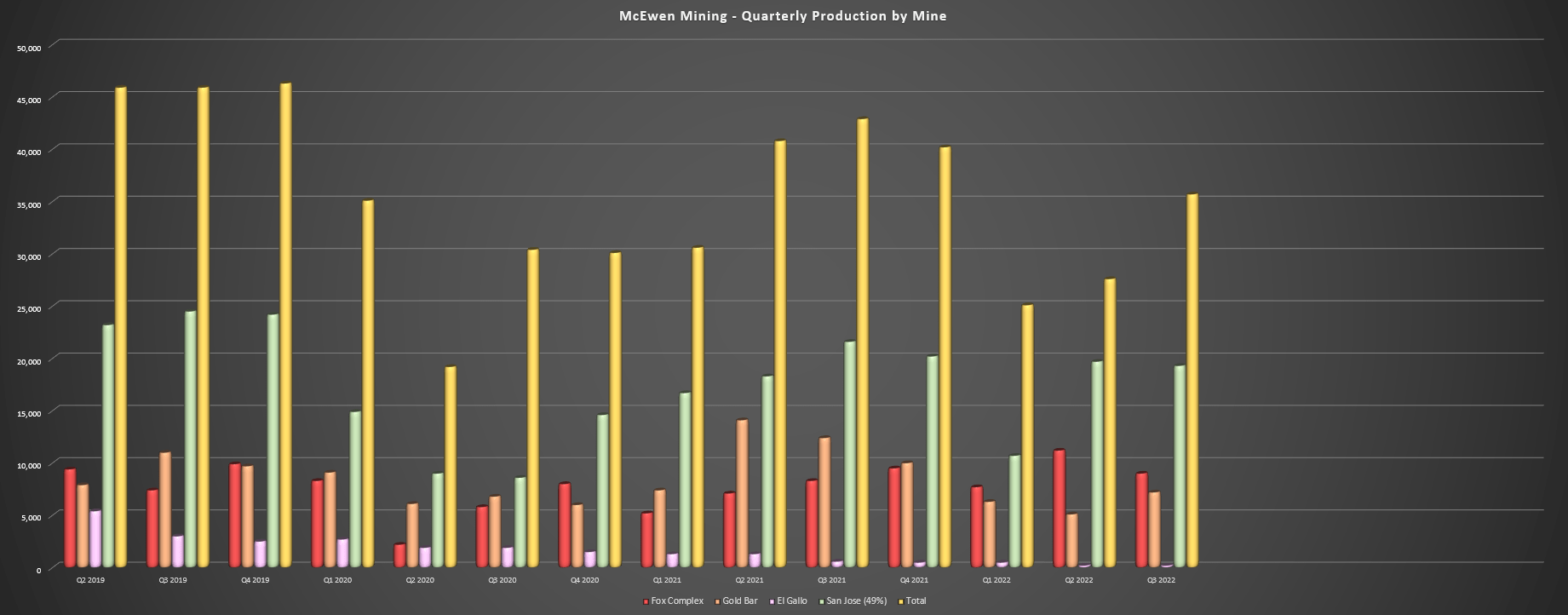

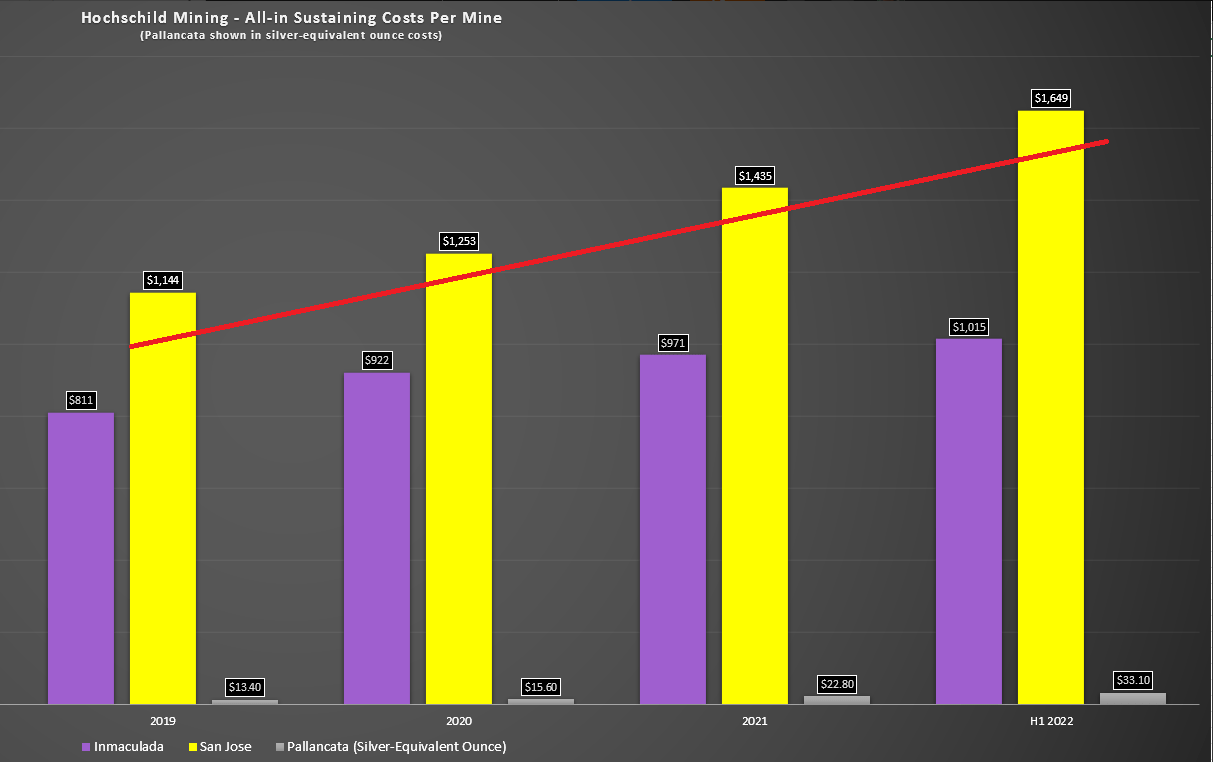

Looking at its mines and its San Jose interest individually, we can see that it was another soft quarter for San Jose with less than 20,000 GEOs of attributable production, well below pre-COVID-19 levels. This can be attributed to the declining grade profile at San Jose, contributing to much higher costs at the asset when combined with inflationary pressures, as the below chart of Hochschild Mining's ( HCHDF ) cost performance highlights (yellow bars). Worse, San Jose's reserves were sitting at just ~36 million silver-equivalent ounces as of year-end 2021. Notably, this is despite using a relatively high gold and silver price of $1,800/oz and $26.00/oz, respectively.

McEwen Mining - Quarterly Production by Mine (Company Filings, Author's Chart) Hochschild Mining - AISC are shown with San Jose (MUX 49% Interest) (Company Filings, Author's Chart)

{kind=link}

{kind=link}

Given this relatively small reserve base (what's likely to be less than 1.4 billion tonnes of ore at year-end 2022 vs. ~300,000 tonnes processed per annum), San Jose appears to have a sub-5-year mine life unless it can replace its reserves. While I certainly wouldn't rule this out, its inferred resource base is slightly lower than its current reserve base, suggesting that grades will likely remain below pre-COVID-19 levels when the asset had decent cost performance and was a meaningful contributor for both Hochschild and McEwen Mining with its 49% interest. To summarize, it's hard to be overly optimistic about this asset post-2025, and this represents a huge chunk of McEwen Mining's current GEO profile.

San Jose Production & Costs (Company Filings, Author's Chart)

{kind=link}

Grades at San Jose have declined from 436 grams per tonne of silver and 6.7 grams per tonne of gold in FY2017 to 353 grams per tonne of silver and 5.0 grams per tonne of gold this year, and should remain at or below these levels in FY2023 and FY2024.

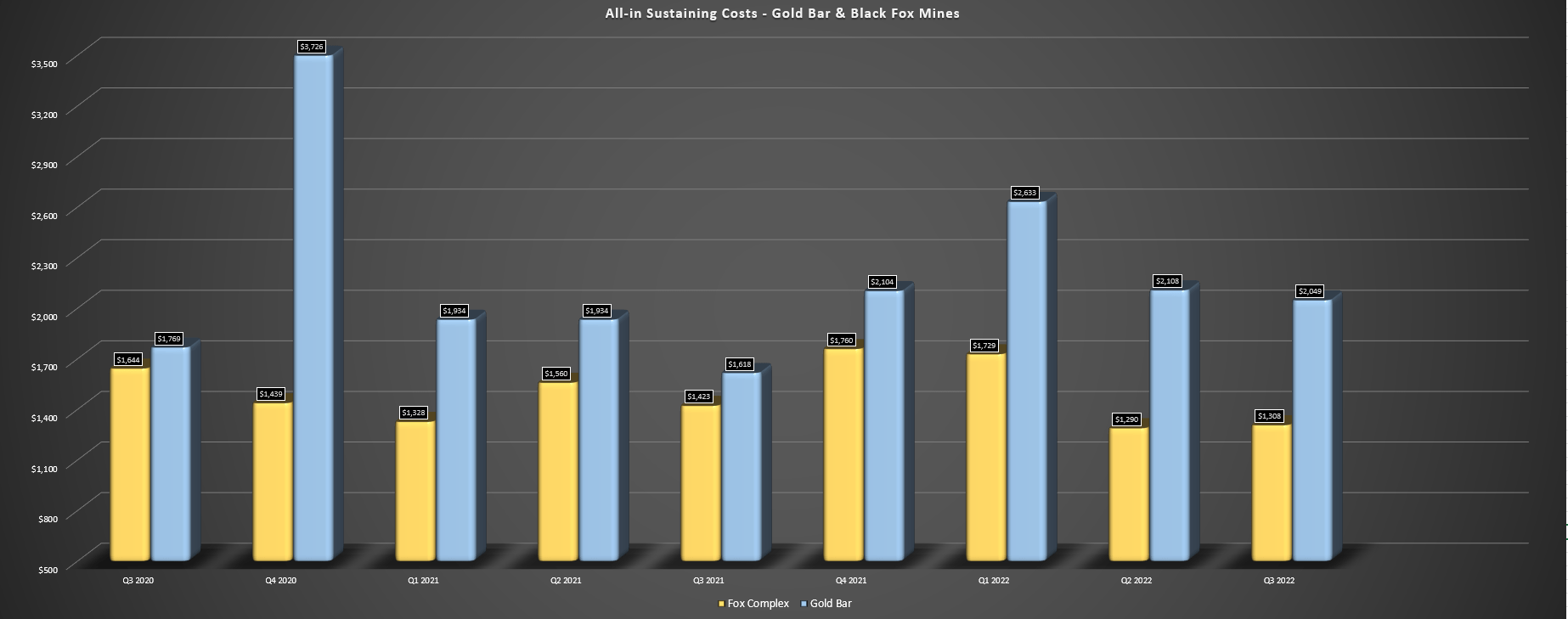

Moving over to the Gold Bar Mine in Nevada was another disappointing quarter for this asset, with gold production of ~7,200 ounces, a more than 35% decline from the year-ago period. The decline in production was related to lower mining rates (contractor availability) and carbonaceous material that was treated as waste. The result of the much lower production was that costs spiked to $2,049/oz, up 27% year-over-year despite being up against easy comps ($1,618/oz in Q3 2021). Fortunately, mining will start at Gold Bar South by year-end, with a lower strip, higher grades, and no carbonaceous material. Still, the reserve base here is small (~66,000 ounces), so I don't see this as a game-changer for this marginal asset by any means.

AISC - Gold Bar & Fox Mines (Company Filings, Author's Chart)

{kind=link}

Finally, looking at McEwen Mining's Fox Complex in Ontario, the operation was an anomaly for McEwen Mining, with a solid quarter that saw higher production and lower costs. This was evidenced by gold production of ~9,000 ounces at cash costs of $774/oz and AISC of $1,308/oz, a meaningful improvement from ~8,300 ounces at $1,423/oz AISC in Q3 2021. Higher grades drove the improved production and costs, and the company hopes to increase production by boosting throughput, which could positively impact unit costs.

Unfortunately, while Fox was a highlight in the quarter, McEwen Mining's costs still came in well above the industry average on a consolidated basis ($1,500/oz plus across its three assets), and all-in-sustaining costs are sitting above $1,650/oz year-to-date. So, while things have certainly improved after a very rough past two years, and it's possible McEwen Mining might finally make it through a year without meaningful share dilution in 2023, it's hard to be bullish on the company when its best asset is a ~50,000-ounce producer with $1,200/oz + AISC.

Recent Developments

Looking at recent developments, the major news was the closing of a ~$82 million offering that included a $25 million investment by Nuton, which is Rio Tinto's ( RIO ) leaching technology venture. In addition to this much-awaited financing being closed that sets McEwen Copper up for an IPO this year, McEwen Copper entered into a collaboration to advance the understanding of the possible application of heap leach technology at its massive Los Azules Project in San Juan, Argentina. For those unfamiliar, McEwen Mining owns a 68.1% interest in McEwen Copper, and Los Azules is one of the largest undeveloped copper assets globally, with costs expected to be at the low end of the cost curve.

While this investment by Nuton is positive, it's worth noting that the investment is chump change for Rio Tinto, and the company has made similar deals with several other projects in the sector over the past year. In addition, while many investors might be anxious to see the results of the PEA, it could disappoint from a capex standpoint, given that we've seen considerable inflation since 2017, and upfront capex was already estimated at nearly $2.4 billion. So, with the impact of inflationary pressures, I wouldn't be surprised to see a sharp increase in upfront capex to $3.0+ billion and also some pressure on operating costs with increased costs for sustaining capital and the inflationary impact on mining and processing costs. Let's dig into MUX's valuation:

Valuation

Based on ~51 million fully diluted shares and a share price of US$7.05, McEwen Mining trades at a market cap of ~$360 million, which is a very reasonable valuation for a 150,000+ ounce producer on a GEO basis. That said, this assumes that all of the company's mines are moderately profitable. In McEwen Mining's case, the company continues to have negative AISC margins at Gold Bar, San Jose's AISC are razor thin, and while the Fox Complex is improving, this is still an average asset at best, with year-to-date AISC above $1,325/oz. So, I would argue that a generous valuation for its gold business and San Jose interest as it stands today is $210 million or $4.10 per share ($1,000 per ounce of attributable annual GEO production).

{kind=link}

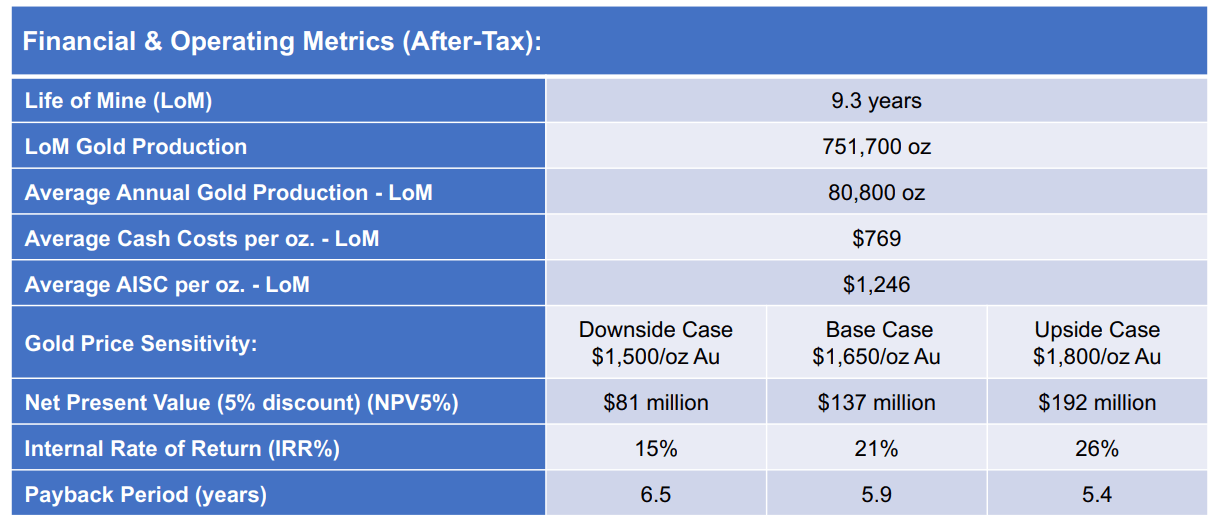

As shown above, and while it doesn't fully capture the negative impact of inflationary pressures, McEwen's Fox Complex has an After-Tax NPV (5%) of $137 million at a $1,650/oz gold price, so I think it's more than reasonable to assign $130 million in value to this asset.

However, with MUX having a majority interest in a top-5 copper asset (not owned by a major), it's only fair to assign some value to this asset. I would argue that a conservative fair value is McEwen Mining's low estimate of $3.25 per share. This is based on a purchase price of $485 million for Josemaria Resources, which is multiplied by McEwen Mining's 68.1% interest in McEwen Copper and a 50% discount given that Josemaria was a public company and this value was based on a premium (takeover price). Finally, McEwen Mining has a royalty portfolio, which includes a 1.25% NSR on Los Azules (Argentina) and Elder Creek (Nevada). I see a value for this portfolio of $40 million conservatively or $0.80 per share.

If we add all these values together, we arrive at a fair value of US$8.15 per share, slightly above MUX's current share price of $7.05. In a less conservative scenario in which we assign $280 million in value for McEwen's interest in McEwen Copper [US$5.50 per share], McEwen Mining's fair value on a sum-of-the-parts basis would climb to US$10.40, which would represent a 47% upside from current levels. However, I prefer to err on the conservative side. And, even if we did use the upside case, I prefer a minimum 50% discount to fair value when buying small-cap producers, meaning that McEwen Mining's low-risk buy zone would still come in at US$5.20 or lower using the upside case scenario.

Technical Picture

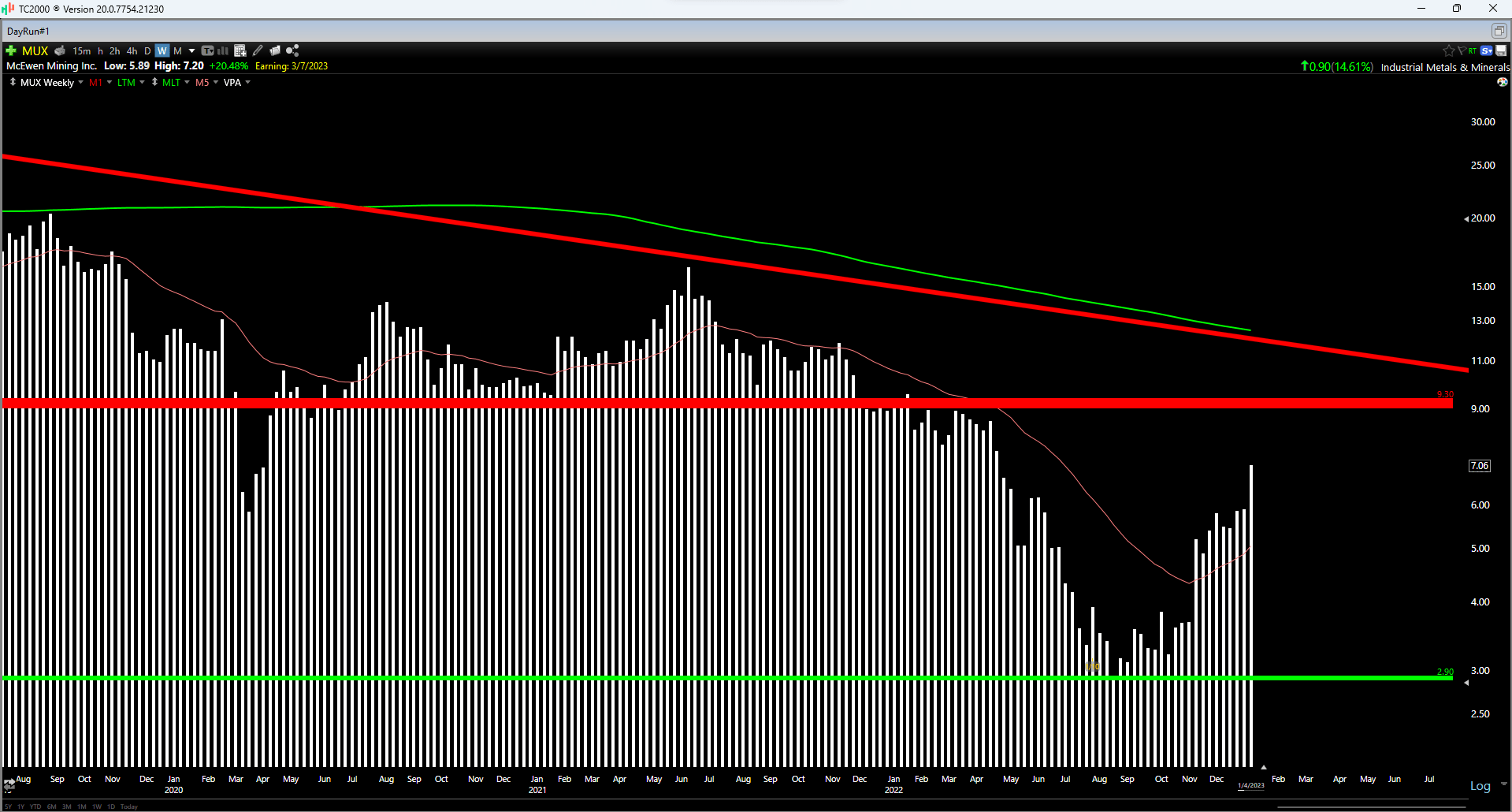

Although the fundamentals suggest that some further upside is possible depending on what one believes McEwen Copper's fair value to be (and assuming sentiment remains positive for gold and silver), the technical picture is less favorable. This is because McEwen Mining is now in the upper portion of its support/resistance range, with strong resistance overhead at US$9.30 and no strong support until US$2.90 - US$3.10. This translates to a reward/risk ratio of 0.55 to 1.0, with $2.20 in potential upside to resistance and $3.95 in potential downside to support. Hence, I see the stock as susceptible to profit-taking, and I believe that chasing the stock above US$7.05 is not the best idea.

{kind=link}

Summary

McEwen Mining has undoubtedly had a much better year, and sentiment has improved for the stock, with investors looking forward to a Los Azules PEA next year and McEwen Copper's IPO, which could help to provide a better idea of its value in this asset once trading in the public market.

That said, two of the company's core assets have elevated costs and relatively short mine lives. Plus, while one asset has improved, it's a relatively small operation with costs slightly above the industry average on an AISC basis. Hence, a lot of McEwen Mining's valuation is riding on Los Azules, and it's possible the PEA could disappoint from a capex standpoint as we see the impact of inflationary pressures on its construction costs (previous study completed in 2017).

To summarize, while investors have enjoyed a nice run in MUX over the past several months, I don't see any way to justify chasing the stock above US$7.05, and I see this sharp rally above US$7.00 as an opportunity to book some profits. Obviously, the stock could go higher, and I have been wrong before, but the goal in trading is to buy high-quality names when they're out of favor and trading at a deep discount to fair value. McEwen Mining is not a high-quality company; it is no longer out of favor and no longer trades at a deep discount to fair value, suggesting an elevated risk in paying up for the stock.

For further details see:

McEwen Mining: Don't Chase The Stock Here