MCN - MCN: A Covered Call Writing Fund For The Watchlist

Summary

- MCN has been brought up in the past, but more recently, it seems to have been a more frequent occurrence.

- I've run across MCN previously, but I haven't looked at the fund too much in-depth.

- The fund utilizes a covered call-writing strategy, generating premiums and helping to lead to a sizeable distribution yield.

Written by Nick Ackerman, co-produced by Stanford Chemist. A version of this article was published to members of the CEF/ETF Income Laboratory on August 26th, 2022.

There are several options for call-writing funds in the closed-end fund space. They generally provide a relatively more stable way to generate some higher yields. That is as opposed to funds that employ leverage. One such fund that has been being brought up more recently is the Madison Covered Call & Equity Strategy Fund ( MCN ).

This is a fund I've run across before, but I have never done a more thorough dive beyond that. That being said, the fact that it has been brought up more recently is interesting as it has coincided with a rapid rise lately. Perhaps not so surprising either if it has been getting more attention. Given the size of the fund being quite small, it doesn't take a lot to move the price around.

However, it has now pushed the fund from a fairly attractive discount to a premium. The fund was plagued, as most CEFs are, with a persistent discount for years. It was all of a sudden, in 2021, that the fund started exhibiting a premium. That also isn't that unusual as it was a trend we've seen in the CEF space, too, as a whole. CEFs that never traded at premiums all of a sudden started to. We saw valuations across the board had tightened that year too.

I'm not sure the latest premium makes it an appealing fund now. While it could push higher into premium territory, I'd wait until we get a dip from here. The market has been rather volatile in 2022, so I think we have some time before having to make any quick decisions. They aren't the only fund in the call-writing space that has run up significantly lately, driving the valuation to less appealing levels.

The Basics

- 1-Year Z-score: 0.86

- Premium: 6.59%

- Distribution Yield: 9.47%

- Expense Ratio: 1.08%

- Leverage: N/A

- Managed Assets: $150 million

- Structure: Perpetual

MCN's investment objective is "a high level of current income and gains." They look to achieve this with an "actively managed equity portfolio of common stocks with a covered call option strategy." The covered call strategy is designed to "reduce the risk compared to just owning the stock, and provide stable, reduced-volatility participation in the equity market while providing a steady income return from options premium."

The average length of the contracts was 38.90 days at the end of Q2. That could be seen as a bit of a difference in this fund. The Eaton Vance Tax-Managed Buy-Write Opportunities Fund ( ETV ) had an average of 14 days to expiration. They write index calls, but I use that fund as the gold standard for the call-writing CEF space.

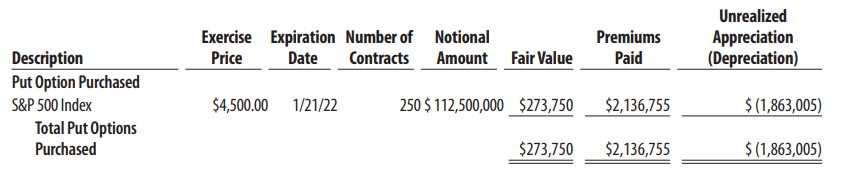

MCN writes calls on single stocks within its portfolio. They last reported being overwritten by just over 80%. They have also purchased S&P 500 Index put options at a substantial level relative to the size of their AUM. That was in their last annual report. The latest semi-annual report shows they didn't have any outstanding at that time.

{kind=link}

The fund is small, but that hasn't impacted the expense ratio significantly. The expense ratio for call-writing CEFs is right around 1%. The lack of liquidity here due to the smaller size should be a consideration before an investor jumps it.

Performance - Helpful Downside Protection Limits Long-term Performance

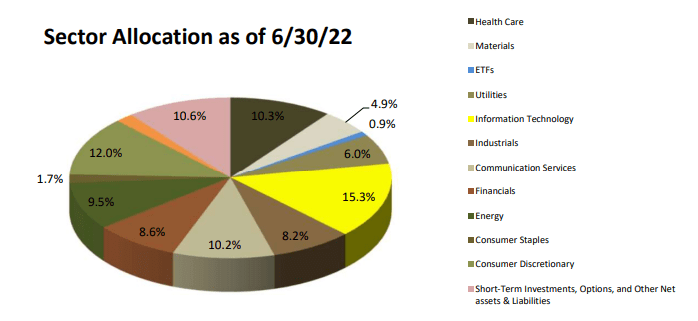

There are several funds that we can compare the performance of MCN with that would be appropriate. One thing I noticed is that MCN holds a lot of "short-term investments." These are money market funds. In the latest annual and semi-annual reports , this was 20.9% and 31.4%, respectively. More recently, the allocation was at 10.6%. On top of that, they could have purchased more put options on the S&P 500 Index since the latest report. That's why on a YTD basis, the fund has done quite well, relatively speaking.

I've included ETV in the total return comparisons. I've also added First Trust Enhanced Equity Income Fund ( FFA ) and BlackRock Enhanced Capital and Income Fund ( CII ) for comparison. I've included the SPDR S&P 500 ( SPY ) for context.

Ycharts

As we can see, defensive positioning played a huge role in that period. I looked at another random annual report for the period ending 2014 . Once again, we see that short-term investments and, this time, U.S. Government and Agency Obligations were a significant part of the portfolio.

Thus, I think it is unsurprising that it will be the weakest-performing fund over the longer term. This is especially true because we've been in bull mode through most of the last decade. Even while more recently, we've been experiencing a more frustrating bull market for long investors.

It also is why all these funds have underperformed in SPY. Again, SPY is only being utilized here for context. These are call writing funds in a vehicle that focuses on income rather than total returns or growth. In a bull market, call-writing funds perform worse because they can cap upside.

Ycharts

If one anticipates that we should continue to expect volatility through 2022, then MCN seems like a solid holding to continue to hold. It should continue to negate some of that volatility. It might not be appropriate for a longer-term holding if you have these other choices available due to its more defensive tilt.

That being said, I could easily see the main argument that it is an investors' hedge play in their portfolios. A smaller allocation that they hang onto for these volatile periods.

In terms of valuation, the time to buy probably isn't at these levels. What makes this more difficult is the overall market has declined too. Meaning that just because the premium is more elevated, the price has still been depressed. MCN isn't alone in having its discount narrow or premium become even more elevated. As we can see, ETV has also spiked up lately quite incredibly lately.

Ycharts

Distribution - Steady

This fund's distribution is similar to what we see in these peers. The fund came about in the early 2000s, before the GFC. They cut their distribution significantly after those events. Since then, they've held the payout steady every quarter for investors.

Ycharts

The latest distribution yield of 9.47% corresponds to a NAV rate of 10.10%. Fortunately, or unfortunately, depending on how you want to see it, MCN compares favorably as the highest of these peer funds. ETV is close, but FFA and CII are quite meaningfully lower.

(A new semi-annual report should be posted any day now. However, the suggestion for coverage meant I wanted to dive into this fund quickly. That's why I'll use the last annual report for the twelve months ending December 31st, 2022. It will still give us a general idea of the distribution coverage.)

In terms of distribution coverage, it is similar to any other equity fund in that it'll rely heavily on capital gains. Those can be harder to come by in a down market, but that's where the options can come into play. As those are also ways for the fund to generate gains, that can potentially happen no matter the current market conditions.

Additionally, due to the positioning of this fund, they aren't down nearly as far as their peers. That would normally be seen as a positive, but they are still the highest yielding of their peers too. So they aren't necessarily sitting as comfortably as we would want.

MCN Semi-Annual Report (Madison)

Net investment income coverage came in at just 4.9% in the latest six month period. That was an increase from the 1.69% NII coverage we saw in the prior year. Again, just reiterating how capital gains will be the driving force of coverage for the distribution.

In the six month period, option premiums contributed roughly $4.164 million in realized gains for the fund.

MCN Semi-Annual Report (Madison)

Combining those realized options written and the NII, we arrive at a distribution coverage of almost 26%. That's a significant shortfall where they need to find other capital gain sources from their underlying portfolio.

Where they could generate further gains is from the purchasing of put options if they entered into anymore of those contracts. In this case, we see that they had generated some gains on the purchased options.

For tax purposes, they have reported that most of the distribution is classified as ordinary income.

For the years ended December 31, 2021, and 2020, the tax character of distributions paid to shareholders was $12,559,719 ordinary income, and $2,532,497 for return on capital for 2021 and $8,698,635 ordinary income, $1,697,061 for long-term gain and $4,686,089 for return on capital for 2020.

One of the reasons for this could be that the calls they write will be classified as short-term capital gains.

MCN's Portfolio

We already mentioned several key features of MCN's portfolio. The high number of put contracts they had purchased heading into 2022 and the sizeable short-term investments. That's had a meaningful impact on how the fund has been performing on a YTD basis and over the years.

Tech is the highest allocation. This is then followed by consumer discretionary, healthcare, and materials. On top of this, energy is also a meaningful allocation at 9.5%. That's not something we see in these call-writing funds regularly. They tend to stick closer to allocations similar to the S&P 500.

{kind=link}

Overall, they stick with a fairly narrowly focused portfolio, coming in at only 41 positions. That can lead to better results than usual if they pick wisely, but also worse results if they pick unwisely or have unfortunate timing as they are less diversified.

The top positions in this fund are also quite interesting, which basically coincides with their more unusual portfolio positioning overall. T-Mobile ( TMUS ) is in the largest position. It's a sizeable one too.

MCN Top Ten Holdings (Madison)

Then there is Fiserv ( FISV ), which I've never heard of. They are a data processing and outsourcing services stock in the tech space. They provide payment and financial services worldwide. Then we have AES Corp. ( AES ), which is a utility company.

On a YTD basis, these three stocks have done quite well. That would further reinforce why MCN itself has also done well on a YTD basis, on top of their defensive positioning.

Ycharts

They aren't all strong performers for their top holdings, though. Comcast ( CMCSA ), Barrick Gold ( GOLD ) and Gilead Sciences ( GILD ) all have led to the downside among these top ten. GOLD had done incredibly well. Shortly after April and heading into May, it looks like it lost steam and has been sent stunningly lower.

Ycharts

Conclusion

MCN is an interesting call writing fund. Although, maybe we should say "option utilizing fund." That would encompass the fact that they've taken a serious bet by purchasing many put contracts. This isn't something they utilize all the time. The last time it looked like they had put options purchased was back in the semi-annual report for the period ending June 30th, 2022 . That was before the previous annual report; this will be something to continue to watch for.

Based on the performance so far, YTD, it would appear that they still have some of these they are employing. At least at some level. That's as well as their defensive positioning in money market investments.

With higher rates, money market yields could actually be called yields these days. However, over the long run, that will likely contribute to the fund underperforming. This is something we can see that happened historically. That doesn't mean it will be repeated, of course. But as long as they are positioned more defensively, that's what one might expect.

That all puts it in a fairly strong position for the argument of being a hedge in one's portfolio. The latest premium has pushed it to elevated levels. So I would consider, even for a hedge play, that we would want to see some of that deflate before picking up shares.

For further details see:

MCN: A Covered Call Writing Fund For The Watchlist