MCN - MCN: A Fund For Investors Looking To Value And High Yield

2024-01-12 03:28:15 ET

Summary

- Madison Covered Call and Equity Strategy Fund has delivered strong performance compared to the benchmark, despite following a more value-oriented strategy.

- MCN offers diversification for investors with heavy exposure to stock indexes like the S&P 500 while yielding nearly 10%.

- The Fund's stable distribution policy and low exposure to the technology sector make it an attractive investment option.

While the broader market, alongside many funds, has relied on growth stocks to deliver much of their return over the past decade, the Madison Covered Call and Equity Strategy Fund ( MCN ) has followed a more valued-oriented strategy but has still delivered a strong performance compared to the benchmark.

After the rally over the past couple of months, the wait-and-see approach that we are seeing in 2024 so far is comprehensible, not only because of the speculation on the interest rate path but also regarding the market valuation that may limit the short-term upside.

The relatively low valuation of MCN can be an advantage now, as long as investors take a more balanced view on the value versus growth allocation this time. In addition, MCN offers diversification for investors with heavy exposure to stock indexes like the S&P 500, while yielding nearly 10%, boosted by extra income from covered calls premiums.

Fund Description & Highlights

NMC aims to generate high current income and capital gains by actively investing in common stocks and employing a covered call option strategy as well. The fund uses primarily an active stock selection strategy through fundamental analysis to identify companies to invest.

As of November 30th, 2023, 74.4% of the fund was invested in stocks, dropping from 80.6% on September 30th, 2023 and 86.6% on June 30, 2023. Meanwhile, nearly 21.0% of the portfolio was allocated to short-term government money market funds, 2.1% to the VanEck Gold Miners ETF (GDX) and 2.5% to covered call options.

The equities' portfolio is somehow concentrated, with only 41 stocks, and with top 10 holdings accounting for nearly 38.7% of its total equity exposure (Transocean (RIG), Las Vegas Sands (LVS), American Tower (AMT), Barrick Gold (GOLD), BlackRock (BLK), Medtronic (MDT), AES (AES), Elevance Health (ELV), APA Corp. (APA), Danaher (DHR)) and interestingly enough, there is no tech name among these top holdings.

From the sector allocation perspective, the fund has a large exposure to the health care sector with 19.0% of total equities, followed by consumer staples with 13.0%, energy 12.1%, basic materials 11.5%, financials 10.3%, consumer discretionary 8.7%, communication services 7.3%, utilities 6.2%, real state 4.3%, information technology 4.0% and industrials 3.1%.

The most significant divergence relative to S&P 500 allocation is the MCN's overweight position in health care (+6.6%), consumer staples (+6.4%), energy (+7.9%), basic materials (+9.1%) and its underweight exposure to information technology (-25.2%) and industrials (-5.9%).

Morningstar's website, consolidated by the author

As a result of MCN's stock allocation, we see the fund with a P/E of 14.3 as of Nov 30th, 2023, which is well below S&P 500's multiple of 18.5 at that time. Surely, MCN's underweight exposure to the technology sector is reflected in the fund valuation. In addition, some core holdings, such as Las Vegas Sands, Barrack Gold and Medtronic, trade at lower multiples and also play a major role here.

Meanwhile, NCM's covered call option strategy has been a bit conservative, with a 93% of the equities portfolio covered with options from the majority of individual stocks owned by the fund, as of Sep 30th, 2023, up from 83% level seen at the end of 2022, when global markets were still at a downtrend, dragged down by the rates hike cycle.

As the fund generally writes out-of-the-money options, it is expected that the equities in the portfolio have some upside until become in-the-money, while, at the same time, this strategy is able to generate income from option premiums. As a result, the fund can participate to some extent in the appreciation of stock prices, while still receiving option premiums.

The actual performance of the fund over time with the combination of both strategies can be seen in the next section.

Delivering Solid Returns Over Time

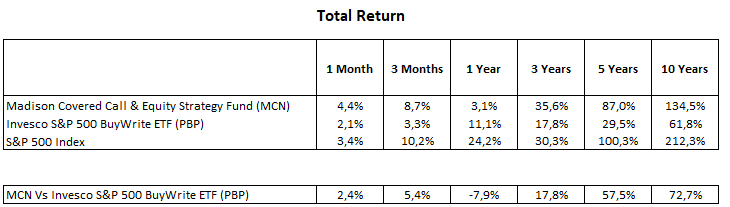

MCN has delivered quite a strong performance over the years, with total returns of nearly 35%, 87%, and 134% over 3, 5, and 10-year periods, respectively.

YCharts, consolidated by the author

{kind=link}

While last year was somehow disappointing, with a total return of only 7.3%, its compounding return, in the long run, has handily surpassed buywrite benchmarks, such as the CBOE S&P 500 BuyWrite Index. Here we used the Invesco S&P 500 BuyWrite ETF (PBP) for comparison purposes.

As expected, MCN and PBP underperformed the S&P 500, as the strong stock market over the past decade has favored investment strategies that rely only on stock price appreciation.

In spite of this, the performance of MCN has been noticeable in my view, taking into account the low exposure to the technology sector, which has been responsible for much of the stock market gains in the past years. Meanwhile, the fund has still outperformed the buy-write benchmark in most timeframes.

Stable Distributions

At current price levels, MCN's distribution rate of nearly 9.99% is at the higher end of the fund's historical range and above the average of other covered call funds of nearly 8.0%.

The fund has kept its quarterly distributions unchanged at $0.18 per common share since 2010. Such a stable distribution policy of course gives some comfort for shareholders looking for a safe source of income.

Over the recent years, despite the volatility we have seen in the stock market, MCN's management has been able to maintain the distribution. However, it was necessary to return part of the invested capital to shareholders to cover distributions, although it has remained at levels below 35%.

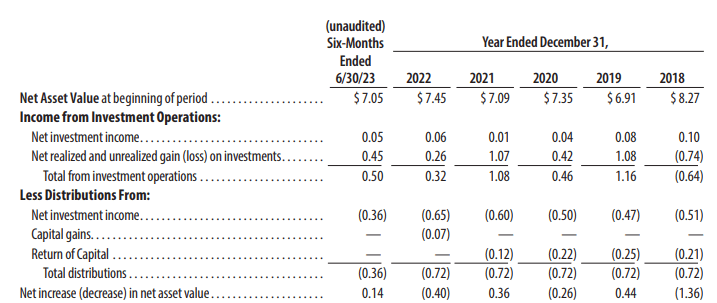

For context, as we can see from the fund 2023 semi-annual report, net investment income generated by interests and dividends covers just a small portion of distributions made over the past 6 years, as expected. The bulk of the income has come from realized and unrealized gains, including stock price appreciations and premiums from options written. Meanwhile, while we have commonly seen distributions as return of capital over the past years, but not at alarming levels, as mentioned earlier.

{kind=link}

That said, although the full-year report for 2023 has not been released yet, distributions in the back half of the year 2023 should have been well-covered by gains in the stock market plus options premiums. For instance, the performance in the first half of the year has already been quite good, with a net increase of asset value of $0.14 per share after distributions, boosted by realized and unrealized gains on investments of $0.45 per share, of which a third part stemmed from the covered call strategy.

Therefore, with a more supportive stock market after interest rates peaking and a meaningful part of the income generated by options premiums, I believe the likelihood of any distribution cut is quite low in the foreseeable future, absent we face an extended stock market correction that pressures the fund to review its distribution policy.

Price/NAV Premium Is Not A Concern

After trading at a discount for much of the last decade, shares of MCN have been trading at a premium since the year 2021, as opposed to several covered call funds that remain at a discount.

Since 2021, the premium over MCN's NAV has been most times in the mid-single digit, with a peak above 10% in October 2022 and April 2023. This suggests to me that while we may see MCN trading at a discount for some period, it is expected to be short-lived, and we are more likely to have the fund trading at a premium even higher than the current level of 4.5%, as investor seems to be comfortable paying up to hold shares of MCN for the time being.

That being said, I do not see the current premium as a problem as long as it stays below high-single-digit and economic conditions do not deteriorate, with soft-landing remaining the most likely scenario going forward.

Meanwhile, my view is that short-term pullbacks, as we are seeing at the beginning of 2024, are long-term buying opportunities for the stock market in general, particularly for MCN, as valuations are well below the S&P 500

Furthermore, MCN's portfolio with a low exposure to the technology sector gives investors an interesting diversification vehicle, while providing a juicy yearly distribution rate of nearly 10%.

Needless to say despite we see a buy case here, in the event of a more pronounced stock market leadership centered on big tech names, the relative performance of funds like MCN may be affected, compared to the S&P 500 for instance. However, in my view, even in this case, MCN should still be regarded as a valuable diversification fund.

For further details see:

MCN: A Fund For Investors Looking To Value And High Yield