ETV - MCN: Strong Performance But Premium Persists

2023-03-25 05:11:21 ET

Summary

- MCN has been able to reduce losses relative to the market.

- This would be thanks to its call-writing strategy plus holding a significant portion of its portfolio in money markets.

- The defensive positioning of this fund has been quite simple but incredibly effective.

- Other investors have seemed to take notice as the fund continues to trade at a rich premium.

Written by Nick Ackerman, co-produced by Stanford Chemist. This article was originally published to members of the CEF/ETF Income Laboratory on March 23rd, 2023.

Madison Covered Call & Equity Strategy Fund (MCN) is an interesting fund that has been able to buck the losses experienced by the S&P 500 Index in the last year. This would be thanks to its defensive positioning with a covered call strategy on a large portion of the portfolio and its sizeable allocation to a simple cash-like position in a money market fund. Here's a look at the performance since our previous update .

MCN Performance Since Previous Update (Seeking Alpha)

As cash is earning something these days, and it has been able to produce gains, that isn't necessarily a bad thing either. That being said when investing in a fund, one might expect it to be mostly invested. Sitting in cash is something an investor can do on their own to whatever level they feel is appropriate.

All that being said, what would continue to keep MCN on the watchlist for me is the fund's persistent premium. It would appear that other investors have taken notice of the fund's strong performance and bought up the fund. In fact, the premium has been pushed a bit higher since our prior coverage. As a premium hasn't historically been common, I still find it hard to get too excited. This is especially true when around a quarter of the fund is invested in a money market fund.

For those already holding, it's definitely been working. So I would understand one wanting to continue to sit tight. You also aren't just getting the management of an allocation to a money market but a fairly broad range of common stocks and an options strategy. For that reason, I believe an update is still a worthwhile exercise.

The Basics

- 1-Year Z-score: 0.66

- Premium: 7.62%

- Distribution Yield: 9.44%

- Expense Ratio: 1.08%

- Leverage: N/A

- Managed Assets: $148 million

- Structure: Perpetual

MCN's investment objective is "a high level of current income and gains." They look to achieve this with an "actively managed equity portfolio of common stocks with a covered call option strategy." The covered call strategy is designed to "reduce the risk compared to just owning the stock, and provide stable, reduced-volatility participation in the equity market while providing a steady income return from options premium."

The fund's expense ratio is about normal for a covered call closed-end fund. With no leverage, that's one less concern that we have to worry about with this fund.

Performance - Premium Persists

A call writing fund outperformance of the S&P 500 Index in a down year isn't anything new. That's part of what their appeal is, as it is a slightly defensive strategy. A covered call strategy works best in a flat market otherwise, but MCN's addition to holding a significant allocation to cash (26.7% as of their last report in a money market) meant even better results. Here's a look at the performance of MCN compared to the S&P 500 ETF (SPY).

YCharts

However, it's not all sunshine and rainbows. While the fund is performing well through this volatile period and should for a while now, it meant giving up the upside during most of the last decade when we had a raging bull market. This is generally one of the trade-offs for carrying a call-writing fund.

YCharts

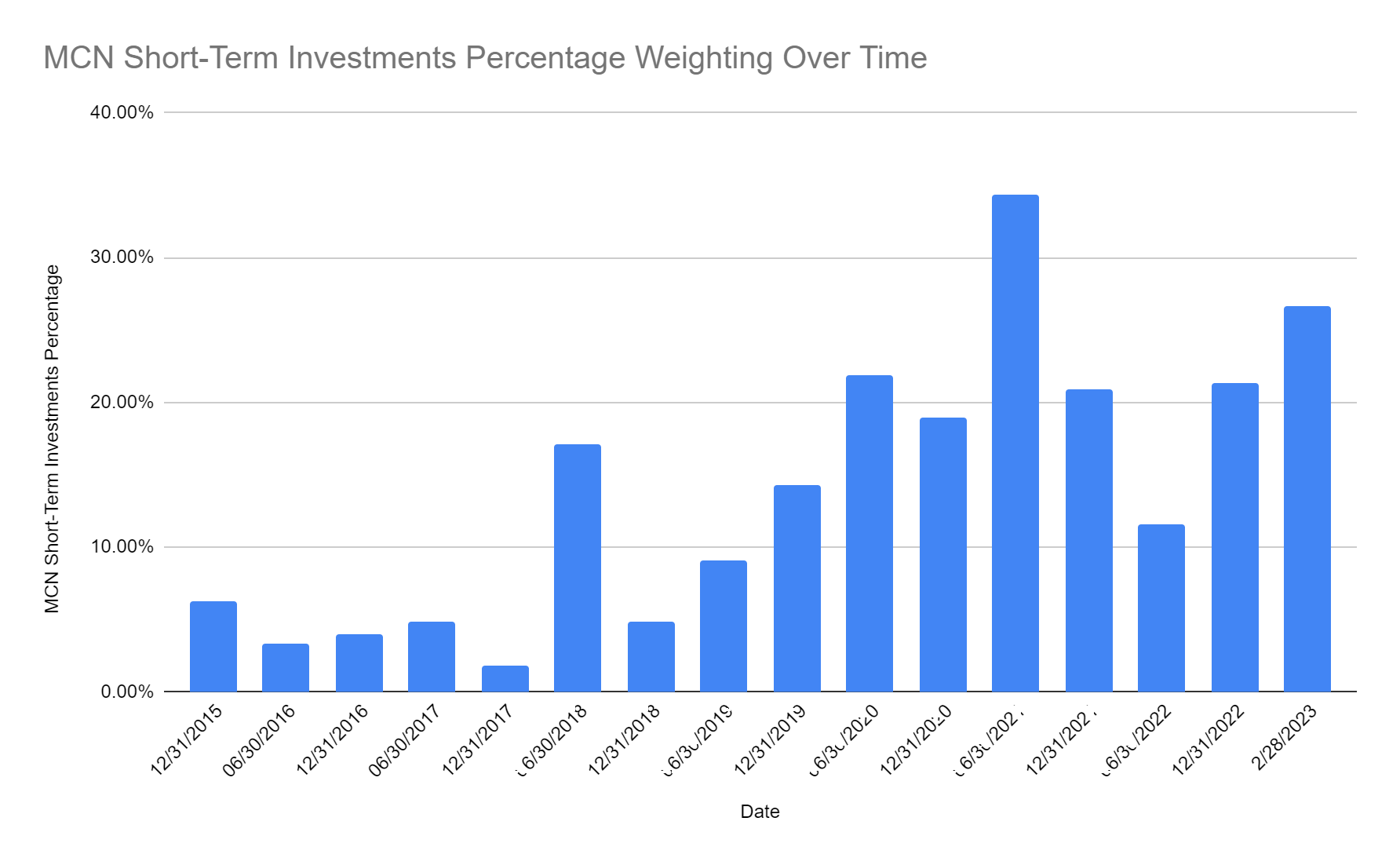

They aren't always so overallocated to money markets, varying quite wildly over the years. However, the allocations in the last few years have been a bit larger than in previous years. This can make sense as money market funds are starting to yield something.

MCN Short-Term Investment Weighting Over Time (Author Compiled Data From Annual And Semi-Reports)

{kind=link}

Given these higher allocations to short-term investments, over the longer term, it also meant weaker results relative to some peers. The peers I've included are Eaton Vance Tax-Managed Buy-Write Opportunities ( ETV ), First Trust Enhanced Equity Income Fund ( FFA ) and BlackRock Enhanced Capital & Income Fund ( CII ). Where MCN had outperformed ETV was on total share price results, but that was as ETV's valuation came down and MCN's premium rose.

YCharts

However, I'm not too worried about the longer-term performance or the shorter-term performance but more of a worry about the fund's premium. In my opinion, the fund is set up for an uphill battle if its history is any guide. CEFs tend to be mean reverting, so when we see a fund that has traditionally traded at a discount for many years, we would expect it to return at some point.

At that point, it could be a better opportunity for investors considering this fund. The main risk here is that even if the fund continues to perform well - as it should in this environment - if it goes back to a discount, an investor would never really realize the success of the underlying portfolio.

YCharts

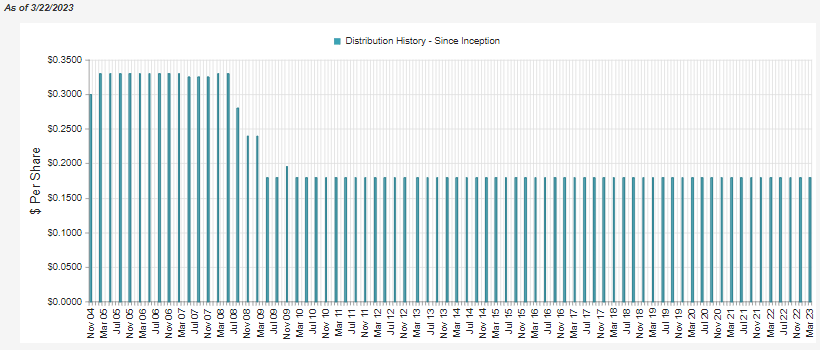

Distribution - Attractive And Steady

Another item that MCN can boast about is a long-term history of being able to maintain the same distribution to shareholders. They cut their quarterly distribution through the GFC, but many other funds did. So I don't think we can hold that against them.

{kind=link}

There is another downside to a fund when trading at a premium. The fund's premium means that while shareholders receive a distribution rate of 9.44%, the fund actually has to earn 10.16%. There isn't a significant difference at this time, but it does mean the fund has to provide a double-digit performance going forward to maintain the distribution. The money-market yields of ~4% are a nice start, but they will need additional sources of capital gains to get the fund there.

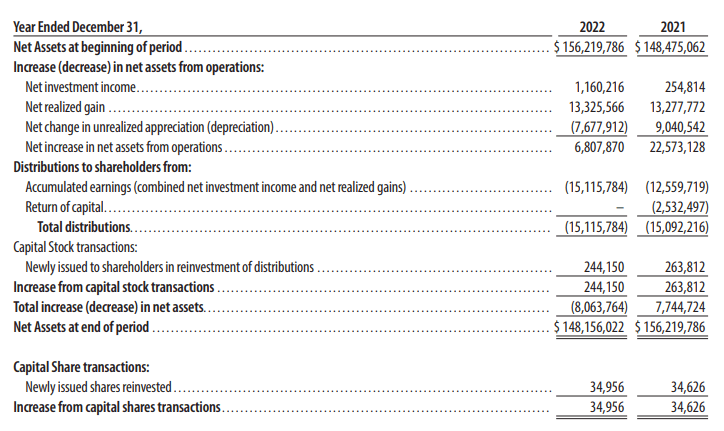

Net investment income increased year-over-year, which is at least partially attributable to the yield rising on the money market fund. Still, the NII coverage here is 7.68%. That means we need to find another 92.32% of coverage.

In the last year , we can see that was largely covered via the realized gains in the portfolio. That's often a good sign as it means the fund mostly covered its distribution through gains and income.

{kind=link}

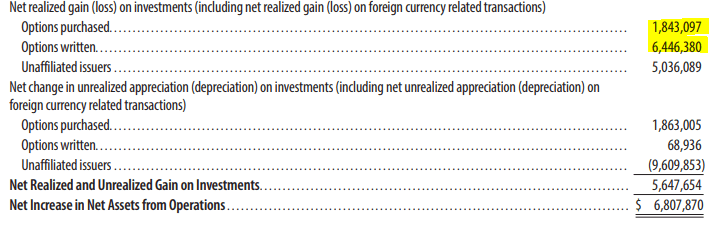

Options are one way the fund can find realized capital gains, even in a flat or down market. Therefore, we need to look at what the potential coverage from the options strategy they utilize can contribute. When looking at that, of the $13.326 million in realized gains, a significant portion came from options written.

The fund even purchased options, which contributed positively to performance. Purchased options aren't common for CEFs, as the vast majority simply write calls against their underlying holdings or indexes.

{kind=link}

Of course, we can't completely ignore the unrealized losses the portfolio sustained either. That's why equity funds will generally require a rising market to cover payouts to shareholders. Even despite these positive contributions from the fund's options strategy, there was a shortfall.

For tax purposes, the bulk of the distribution was identified as ordinary income in 2022, with long-term capital gains as the remainder.

For the years ended December 31, 2022, and 2021, the tax character of distributions paid to shareholders was $13,560,297 ordinary income and $1,555,487 for long-term capital gain for 2022 and $12,559,719 ordinary income and $2,532,497 for return on capital for 2021.

Additionally, they noted that they "did not recognize qualified dividend income during the fiscal year ended December 31, 2022." Meaning that most of these distributions would not have any tax benefits to investors.

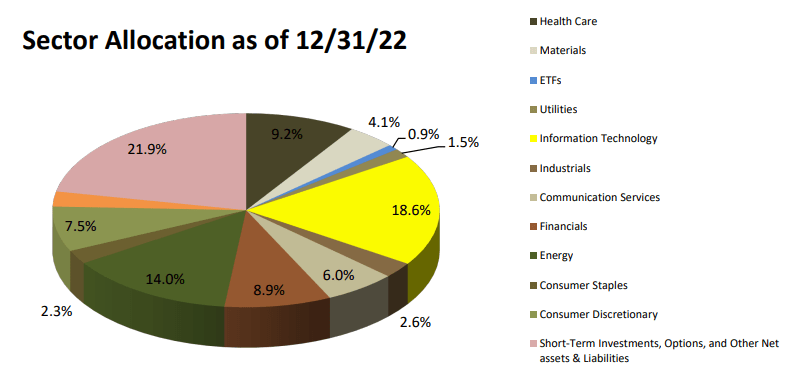

MCN's Portfolio

At the end of 2022 , they listed that 82.6% of their fund was equities covered with call options. They listed only 37 different positions at that time as well. They often carry only a small number of positions, which can mean some concentration risk. On the other hand, they still do a fairly good job at keeping the fund diversified in terms of sector allocations.

{kind=link}

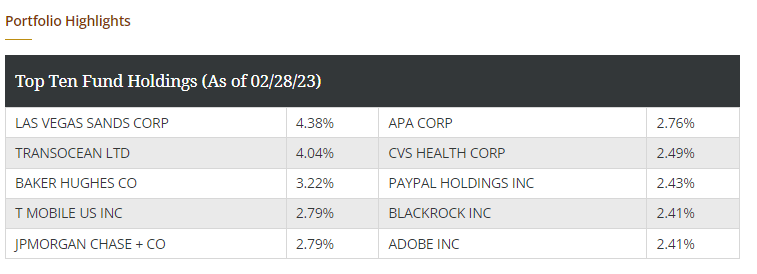

At the end of February 2023 , looking at their full holding list shows 39 positions. So this is a fairly regular feature of this fund to carry a relatively lower number of positions. This would be 40 total positions if we include the 26.7% allocated to SSC Government ( GVMXX ). The yield for this is currently 4.47% .

{kind=link}

That being said, the top ten holdings are still fairly well allocated without one or two positions being significantly overweight.

{kind=link}

It should also be noted that the fund's turnover is fairly high. In the last year, it was 104%. For 2021 it was an even higher 178%. For turnover, that's on the higher end of what I regularly see when looking at CEFs.

Las Vegas Sands ( LVS ) was a position previously at 2.9% or the 8th largest position, but it has moved up to the number one spot. New names to the top ten that weren't there in our previous update are; Transocean ( RIG ), JPMorgan ( JPM ), APA Corp ( APA ), PayPal ( PYPL ), BlackRock ( BLK ) and Adobe ( ADBE ).

That being said, the only positions we saw previously that are no longer a part of the portfolio at the end of February 2023 are only Honeywell ( HON ) and Gilead Sciences ( GILD ). So the actual high turnover doesn't always mean there are a lot of positions being added or deleted from the fund.

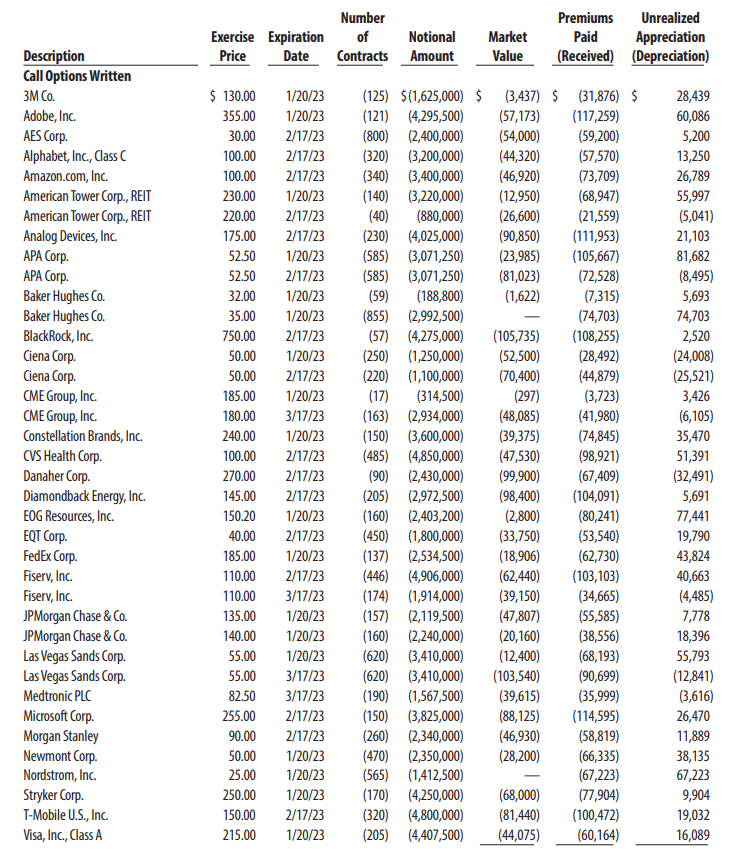

Instead, it could be higher turnover as the fund has options they are selling and then turning around and buying positions back. Here's a look at the options they had outstanding at the end of 2022. All of these have actually expired now, but it can give us a good idea of what sorts of contracts they are entering.

{kind=link}

The average length of their contracts was listed at 39.4 days at the end of 2022. That's similar to the 38.9 days they had listed in our previous update.

Conclusion

MCN is an interesting CEF with an options writing strategy; they've even generated some results from buying options. The longer-term results from the fund have been weaker, even relative to peers. However, the shorter-term results, thanks to holding onto a fairly elevated level of short-term investments, meant stronger results recently. The fund jumping to a premium would have also benefited those that held since the fund was trading at a discount. That being said, it's precisely the fund's premium that keeps it more of a watchlist than a buy at this time.

For further details see:

MCN: Strong Performance, But Premium Persists