EOS - MCN: Suitability Depends On Your View Of The Market

2023-12-19 10:24:05 ET

Summary

- The Madison Covered Call and Equity Strategy Fund offers a 9.92% yield, higher than most equity funds.

- The MCN closed-end fund has slightly underperformed the S&P 500 Index in the past two months but has a higher yield.

- The MCN fund's covered call options strategy provides income but sacrifices some upside potential in a strong bull market.

- The fund has outperformed its peers during the tightening conditions of the past three years, but underperforms peers during easy money environments.

- The fund might fail to cover its distribution for the second year in a row, yet trades at a premium.

The Madison Covered Call and Equity Strategy Fund ( MCN ) is a closed-end fund, or CEF, that income-focused investors can employ in an effort to achieve their goals without needing to sacrifice the potential upside of an equity investment. As we have discussed in various previous articles, fixed-income funds typically have much higher yields than equity funds in today’s market. This is largely because the high-interest rate environment has resulted in fixed-income investments having much more attractive coupons than in the past, while equities continue to trade at levels implying massive growth going forward. The Madison Covered Call and Equity Strategy Fund is an exception to this, as it manages to boast a respectable 9.92% yield despite investing in a portfolio that consists of common equity securities.

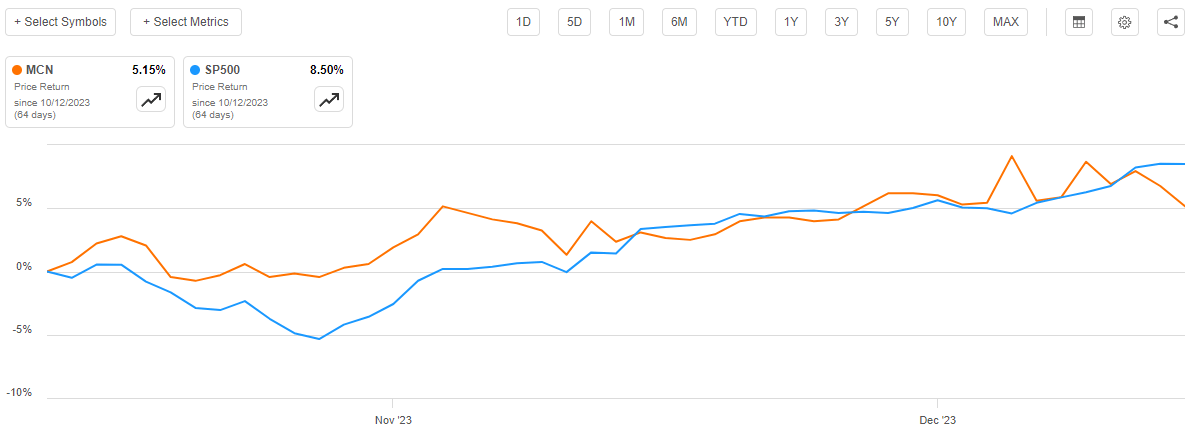

As regular readers are no doubt well aware, we last discussed the Madison Covered Call and Equity Strategy Fund in mid-October. Obviously, the general mood and atmosphere in the asset markets have changed significantly since that time. Investors have started front-running an expected pivot by the Federal Reserve and have been buying pretty much everything in sight, which has been driving up the price of both bonds and common equities. That buying frenzy has included shares of this fund, which are up 5.15% since the last time that we discussed the fund. This is, unfortunately, not quite as good as the 8.50% gain of the S&P 500 Index ( SP500 ) over the same period:

{kind=link}

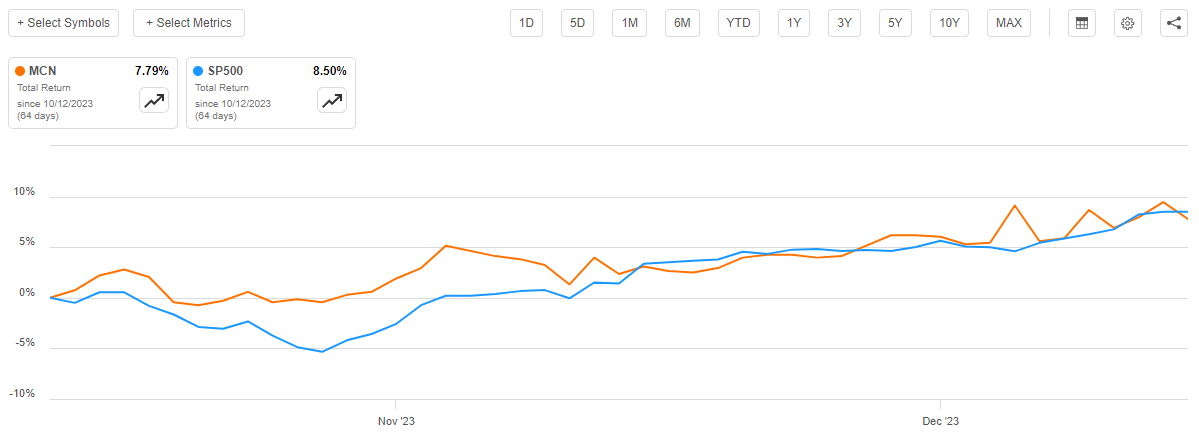

However, this fund has a much higher yield than the S&P 500 Index, so this performance comparison does not tell the whole story here. When we take the fund’s distributions into account, we see that investors who purchased the fund on the day that my prior article was released have gained 7.79% on their money:

{kind=link}

Thus, investors in this fund have slightly underperformed the S&P 500 Index over the past two months. This is pretty much what we would expect during a bull market run though, as we will see in just a few minutes. This fund does have an advantage over a traditional equity fund during a market correction though, which could be useful considering that there is a very real possibility that the market is wrong about the magnitude of the 2024 interest rate cuts. As such, there could be some reasons to consider purchasing this fund today if you can get it at a reasonable price.

About The Fund

According to the fund’s website , the Madison Covered Call and Equity Strategy Fund has the primary objective of providing a very high level of current income and current gains. The fund has the secondary objective of providing its investors with long-term capital appreciation.

Regular readers may recall that I have been critical of many funds that have long-term capital appreciation in their objectives in past articles. This was because those funds were generally fixed-income funds that were unlikely to be able to realistically deliver such an objective over extended periods of time. This fund is different, as its strategy does allow it to provide capital appreciation over the long term. The website explains the fund’s strategy:

We believe these goals can be met by investing in large and mid-capitalizations stocks that are, in our opinion, selling at a reasonable price with respect to their long-term earnings growth rates. The income comes in the form of option premiums which are generated by writing covered calls on a majority of the stocks in the portfolio.

Thus, this fund is basically employing a covered call options strategy to generate income. This is very different than most income-focused funds, as the latter focus on investing in bonds and other debt securities. This fund’s basic strategy is to use options to turn generate synthetic dividends from the stocks in its portfolio. The goal is for the option to expire worthless, allowing the fund to keep both the option premium that was paid by the buyer as well as the underlying stock. Thus, the option premium has much the same impact as if the stock paid a dividend equal to the value of the premium. As I pointed out in a recent article , the synthetic dividend can be quite large as a proportion of the stock price. Thus, the overall yield from doing this can be well into the double-digits.

The downside to this strategy is that the fund has to sacrifice some of the upside potential of the common stocks in the portfolio. This is the reason why it will usually underperform during a very strong bull market, as the received option premiums may not be sufficient to offset the sacrificed capital gains. As such, most funds that follow this strategy only have about a third to half of their portfolio overwritten. This allows for the provision of some income without sacrificing all of the potential upside. The Madison Covered Call and Equity Strategy Fund goes further than this, though. The fact sheet states that 93.4% of the stocks in the portfolio currently have options written against them. This is a higher percentage than we see at other funds that are using a similar strategy:

| Fund |

| % Overwritten |

| Madison Covered Call and Equity Strategy Fund |

| 93.4% |

| Eaton Vance Enhanced Equity Income Fund ( EOI ) |

| 44.0% |

| Eaton Vance Enhanced Equity Income Fund II ( EOS ) |

| 49.0% |

| BlackRock Enhanced Capital & Income Fund ( CII ) |

| 52.00% |

| BlackRock Enhanced Equity Dividend Trust ( BDJ ) |

| 50.27% |

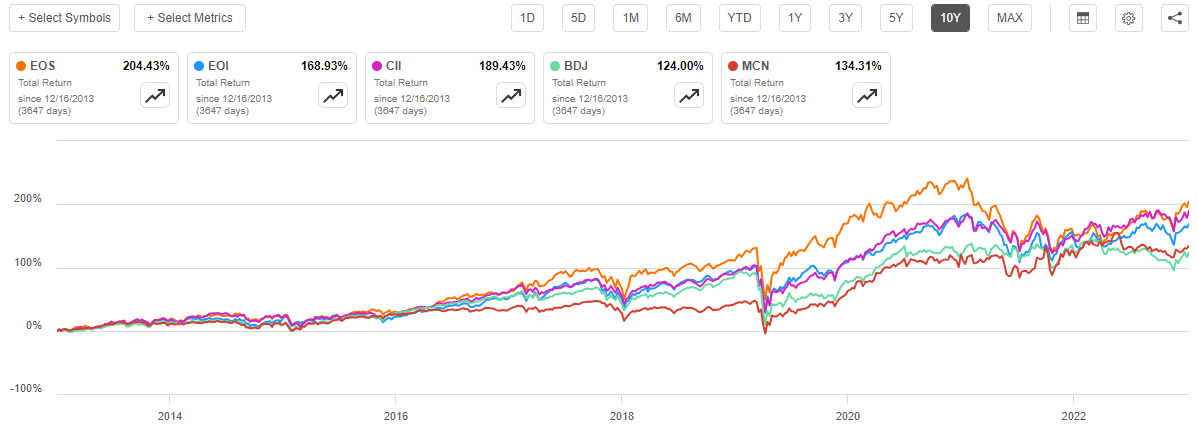

As such, those other funds may have a bit more upside potential in a strong market. This has actually proven to be the case over the past ten years:

{kind=link}

The above chart takes the distributions paid by each of these funds over the period into account. This is important because the Madison Covered and Equity Strategy Fund has a significantly higher yield than these competing funds. As we can see, the fund underperformed any of the rest of these funds except for the BlackRock Enhanced Equity Dividend Trust. This is somewhat understandable because a substantial percentage of the total returns provided by the market over the past decade came from a handful of technology stocks. All of these funds except for the Madison Covered Call and Equity Strategy Fund and the BlackRock Enhanced Equity Dividend Trust have fairly sizable allocations to those stocks.

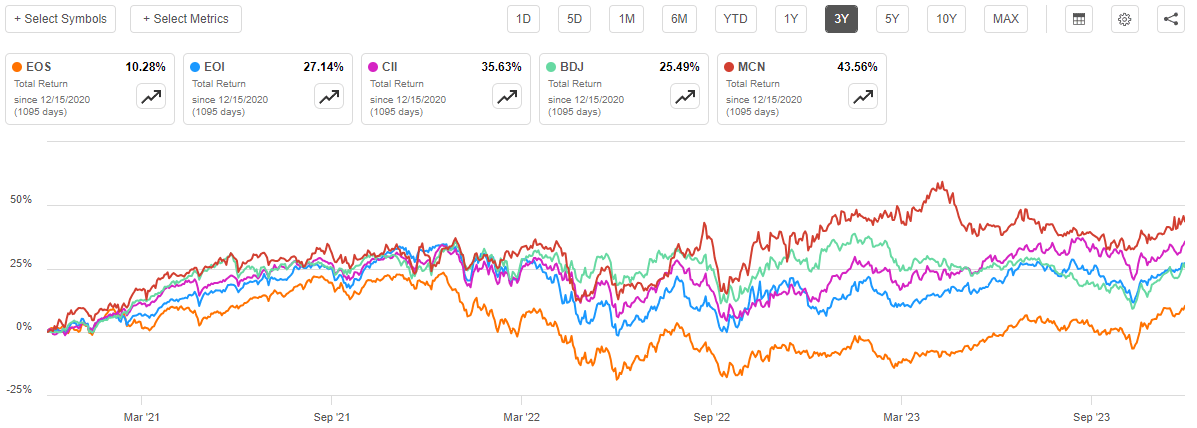

However, things get more interesting when we look at the performance of these funds during a period of time that was not a raging bull market. Over the past three years, the Madison Covered Call and Equity Strategy Fund was by far the best performer out of all five of these funds:

{kind=link}

The covered call strategy tends to outperform a standard equity portfolio during flat markets. This is because the received option premiums provide a sizable return, and the stocks are less likely to be called away. The strategy also outperforms during a bear market because the received option premiums offset some of the losses from declining stock prices. The Madison Covered Call and Equity Strategy Fund overwrites a greater percentage of its portfolio than any of these other funds so it will exhibit these characteristics to a greater degree than its peers.

This brings us to one conclusion. An investor who expects that the next decade will be characterized by the same easy money policies and expanding multiples as the previous one will probably be better served with one of the Eaton Vance or BlackRock funds. An investor who expects more subdued conditions as the excesses of the past twenty years are slowly worked out of the system would be better off with the Madison Covered Call and Equity Strategy Fund.

Distribution Analysis

As mentioned earlier in this article, the primary objective of the Madison Covered Call and Equity Strategy Fund is to provide its investors with a high level of current income and current gains. In pursuance of that strategy, it invests in a portfolio consisting of 42 common stocks (as of today) and writes call options against them. The premiums that the fund receives from these call options are pooled together with any capital gains that it manages to realize from the sale of appreciated securities. This pool of money is then distributed to the investors, net of the fund’s own expenses. As I have shown in previous articles, the synthetic dividend yield that can be realized via a covered call strategy is fairly high so we can probably expect that this fund’s shares would also have a very respectable yield.

That is certainly the case, as the Madison Covered Call and Equity Strategy Fund currently pays out a quarterly distribution of $0.18 per share ($0.72 per share annually), which gives it a 9.92% yield at the current share price. This is a bit higher than this fund’s peers possess:

| Fund |

| Current Yield |

| Madison Covered Call and Equity Strategy Fund |

| 9.92% |

| Eaton Vance Enhanced Equity Income Fund |

| 8.10% |

| Eaton Vance Enhanced Equity Income Fund II |

| 7.50% |

| BlackRock Enhanced Capital & Income Fund |

| 6.44% |

| BlackRock Enhanced Equity Dividend Trust |

| 8.56% |

This is almost certainly due to this fund being more aggressive with its call-option writing strategy compared to its peers, as we already discussed.

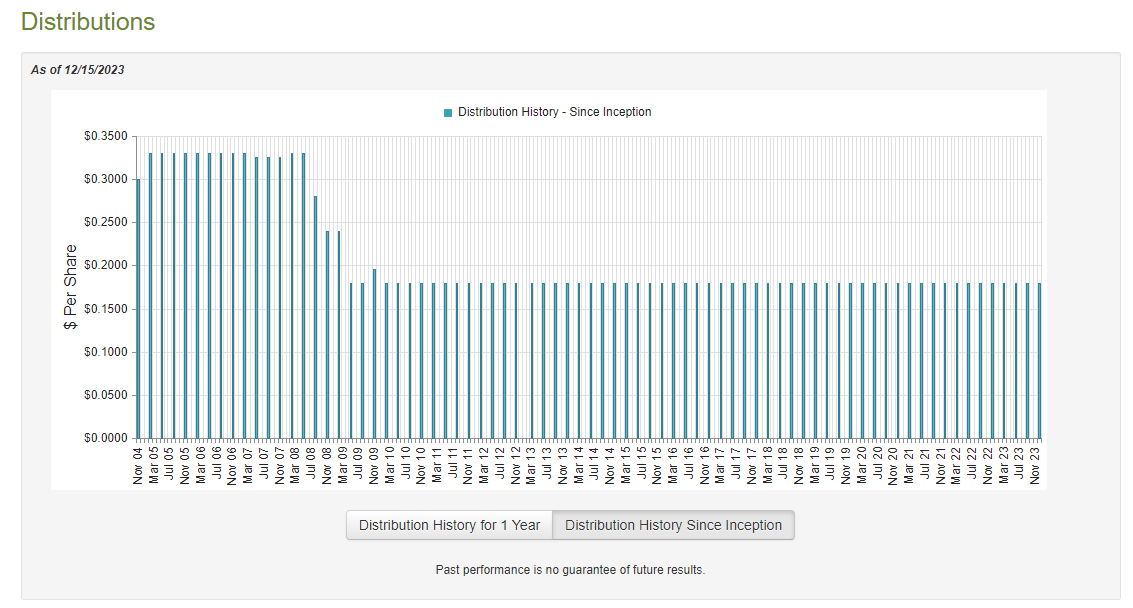

The fund’s distribution history over the past fourteen years or so has been quite solid, as it has generally managed to keep a steady payout. Unfortunately, its distribution history prior to that has not been nearly as attractive:

{kind=link}

For the most part, this distribution history will probably appeal to those investors who desire a steady and consistent source of income from the assets in their portfolios. One of the nice things about covered call option strategies in general is that they can smooth out the volatility that would otherwise plague an equity portfolio so there is no real reason to question the fund’s distribution history in that respect. We should always take a look at its financial performance though, as we generally want to avoid funds that are overdistributing and destroying their net asset value in the process. That policy is almost never sustainable over extended periods.

Fortunately, we do have a relatively recent report that we can consult for the purpose of our analysis. As of the time of writing, the fund’s most recent financial report corresponds to the six-month period that ended on June 30, 2023. As such, it will not include any information about the fund’s performance over the past five months or so. This is rather disappointing, as this period of time included a great deal of volatility, and it would be useful to see how well the fund managed to perform in such an environment. However, the period of time that is covered by this report is still acceptable, as it was generally a very strong market (much like today’s market) that generally provided the opportunity for profits from a common equity portfolio.

During the six-month period, the Madison Covered Call and Equity Strategy Fund received $779,407 in interest and $1,088,538 in dividends from the assets in its portfolio. We need to subtract the money that the fund had to pay in foreign withholding taxes, which gives it a total investment income of $1,861,944 during the period. The fund paid its expenses out of this amount, which left it with $1,040,199 available for shareholders. That was obviously nowhere near enough to pay the fund’s distributions, which totaled $7,567,594 during the period. At first glance, this could be rather concerning as the fund’s net investment income was clearly nowhere near sufficient to cover the amount of money that it paid out to its investors.

However, there are other methods through which the fund can obtain the money that it needs to cover the distribution. For example, the fund might be able to earn some capital gains by selling common stocks that have appreciated in price. It also receives money from the sale of call options. Realized capital gains and received option premiums are not considered to be investment income for tax or accounting purposes, but these things obviously do result in money coming into the fund that can be distributed to the shareholders. Fortunately, the fund did enjoy a great deal of success in this task during the period. The fund reported realized capital gains of $5,821,610 and had another $3,585,068 net unrealized capital gains during the period.

Overall, its net assets increased by $3,019,150 after accounting for all inflows and outflows during the period. Thus, the fund did technically manage to cover its distributions, although it did have to lean on unrealized capital gains to do it.

The fund’s net realized capital gains plus net investment income totaled $6,861,809 during the six-month period. Obviously, this was not enough to cover the fund’s distributions during the period. Thus, the fund had to partially rely on its unrealized capital gains to cover the distributions. The problem with doing this is that unrealized capital gains can be erased by any market correction. We had such a correction shortly after the period covered by this report ended, and it proved problematic for some other funds that were in this situation.

Unfortunately, this fund is one of them. As we can see here, the fund’s net asset value is down 3.05% since July 1, 2023:

{kind=link}

This suggests that the fund has failed to fully cover the distributions that it has paid out so far during the second half of this year. That is disappointing, as the deficit was sufficient to erase all of the surplus gains that the fund had during the first half of this year. The fund’s net asset value per share is down 0.71% year-to-date:

{kind=link}

This fund failed to cover its distribution over the full-year 2022 period, and if it ends up finishing down here then it will represent two straight years of failing to fully cover its distribution. That is something that should give any potential investors cause for concern.

Valuation

As of December 14, 2023, the Madison Covered Call and Equity Strategy Fund has a net asset value of $7.00 per share but the shares currently trade for $7.15 each. This gives the fund’s shares a 2.14% premium on net asset value at the current price. That is better than the 2.41% premium that the shares have had on average over the past month, but it is still probably a bit too much to pay. As we just saw, there is a very real chance that this fund will fail to fully cover its distribution for two years in a row, although it should get pretty close this year. As such, there is a real risk in purchasing it at a premium. It certainly makes sense to buy it at a discount though, if it ever swings to one.

Conclusion

In conclusion, the Madison Covered Call and Equity Strategy Fund is a strong performer during challenging market conditions, especially when compared to its peers. It tends to use the covered call strategy to a greater extent than similar funds. As such, it could be a very good choice if you are ambivalent or even moderately bearish on the market.

A strongly bullish investor who expects a continuation of the multiple expansion and easy credit conditions that dominated the past fifteen years would be happier with another fund. The Madison Covered Call and Equity Strategy Fund also might fail to cover its distribution for the second year in a row and appears rather expensive. As such, it is challenging to recommend purchasing it today, although I would personally be interested in picking up some shares if it ever swings to a discount.

For further details see:

MCN: Suitability Depends On Your View Of The Market