MDU - MDU Resources Group: Spinoff Could Lead To Positive Margin Improvements

2024-01-10 22:23:06 ET

Summary

- MDU Resources Group Inc has seen solid growth in its top line, with a 5.4% CAGR over the last decade.

- The company's net income has increased by 85% YoY, reaching $78 million or $0.38 per share.

- MDU is diversifying its business and spinning off its construction services segment, which could lead to higher margins and growth opportunities.

Investment Rundown

MDU Resources Group Inc ( MDU ) has been able to diversify its business and over the last decade, it has meant a quite solid 5.4% CAGR for the top line. Over the past few years, the top line has started to expand quickly following the spinoff of Knife River Corporation. The net income reached $78 million or $0.38 per share, an 85% increase YoY. The company remains incredibly committed to delivering value for shareholders and the past 32 years, the dividend has been raised. I think this is where a lot of the appeal for the company comes from, a consistent and quality dividend addition to a portfolio looking to diversify more into the energy and industrial sectors.

I think a more fair valuation would be closer to 17x earnings, a slight discount to the sector to provide some margin of safety, but leaving enough upside here that MDU is a buy, given that it's trading below this multiple right now. The multiple indicates a premium to MDU's historical valuation, but I would argue the improvements in the business leave a higher valuation justified here. With that multiple, I land at a target price of $24 per share, provided that the EPS is roughly $1.66 for FY2024. This comes from my estimate that MDU will be better off after the spinoff and that earnings will grow at a good rate. The company has announced they are also spinning off their construction services business which will leave an even more streamlined business model, and potentially a tailwind for higher margins too. I like the quite aggressive and rapid moves that MDU is taking to maximize its market position and continue to grow for the next decades. I am initiating coverage on the company and will do so by rating it a buy.

Company Segments

MDU is involved in a variety of different industries but has as I mentioned earlier made moves to divest and spinoff business segments. Some of the markets it in is are energy delivery, construction materials, and services sectors. The company is structured into five distinct segments, each contributing to its comprehensive portfolio: Electric, Natural Gas Distribution, Pipeline, Construction Materials and Contracting, and Construction Services.

Market Overview (Investor Presentation)

{kind=link}

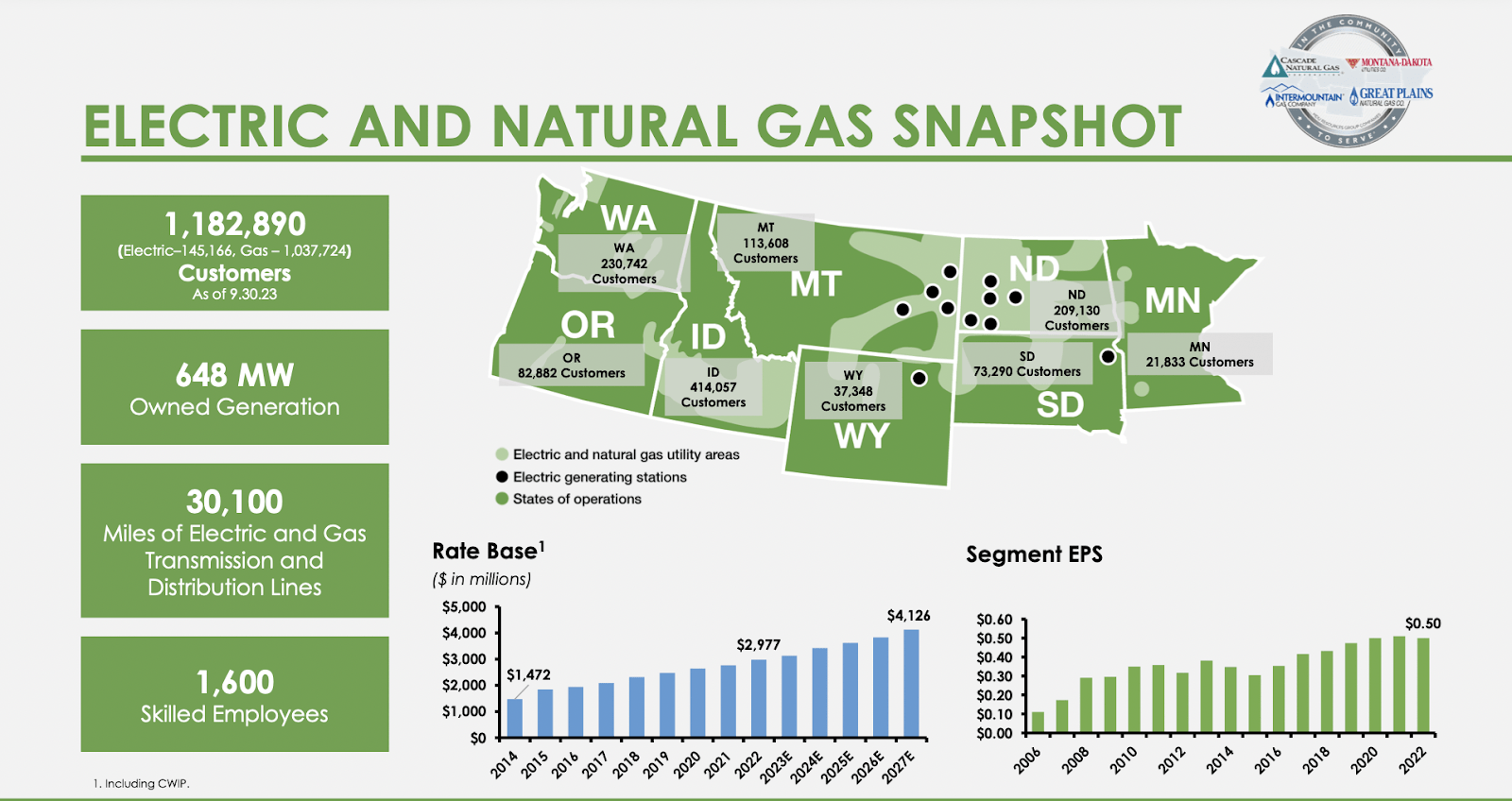

Within the Electric segment, MDU is actively engaged in the generation, transmission, and distribution of electricity. Its operational reach spans residential, commercial, industrial, and municipal customers across the states of Montana, North Dakota, South Dakota, and Wyoming. During the last decade, MDU has also made improvements to its energy generation mix, with more and more coming from renewable sources. The generation mix is now made up of 33% renewables and the remaining quite equally dividend with coal and gas.

Rate Base (Investors Presentation)

{kind=link}

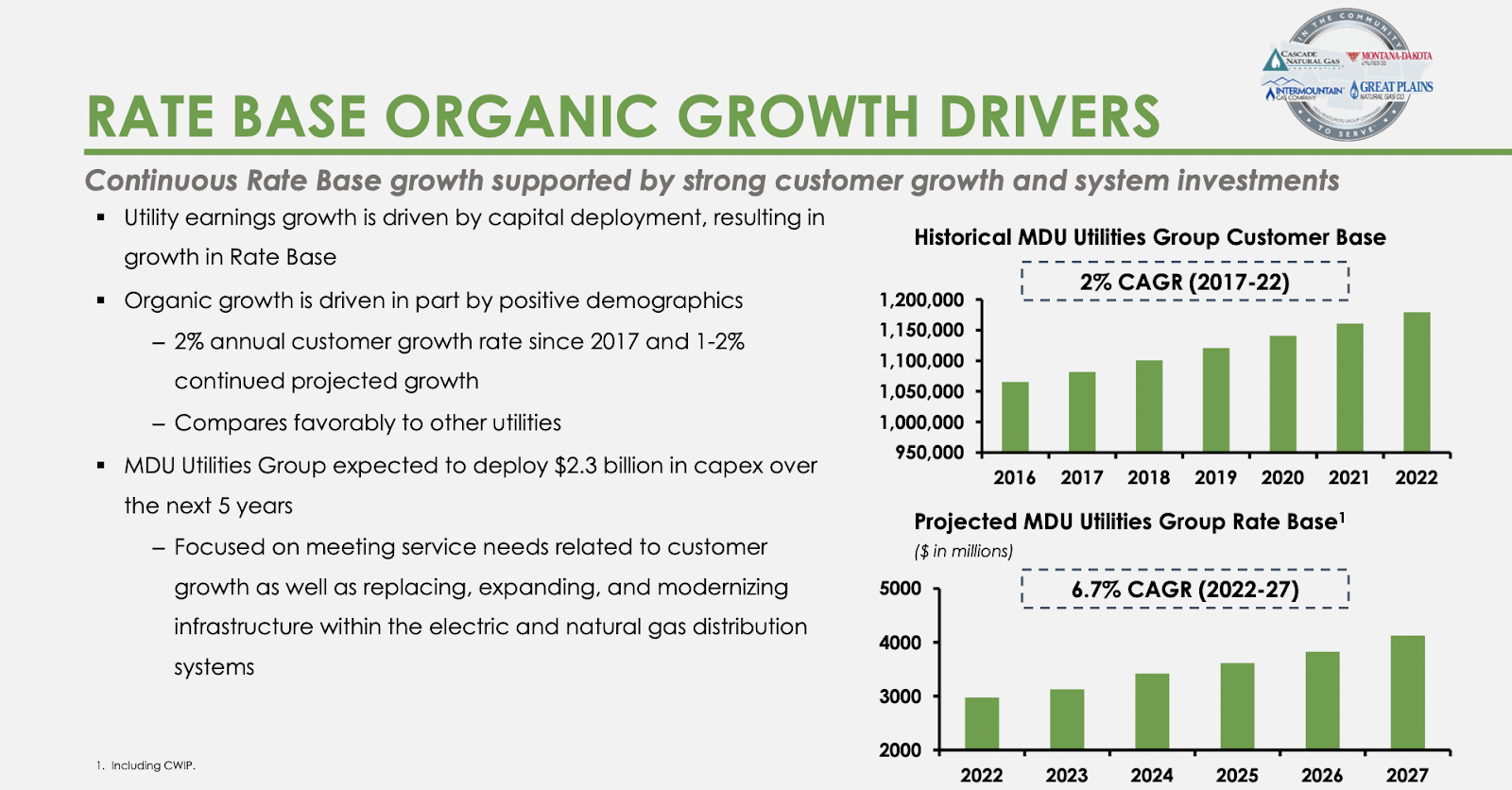

Going forward there are several growth drivers for the company, like a continued climb for the rate base. Between now and 2027 the projected CAGR for MDU utilities group rate base is 6.7%. This type of growth means that MDU is expecting to deploy around $2.3 billion in capex in the next 5 years in total. Much of these capital expenditures will be going into the natural gas distribution. The largest year of investments seems to be this year where $337 million is going towards natural gas. One of these significant investments includes the establishment of an 88-megawatt simple cycle natural gas-fired combustion turbine in North Dakota.

Earnings Highlights

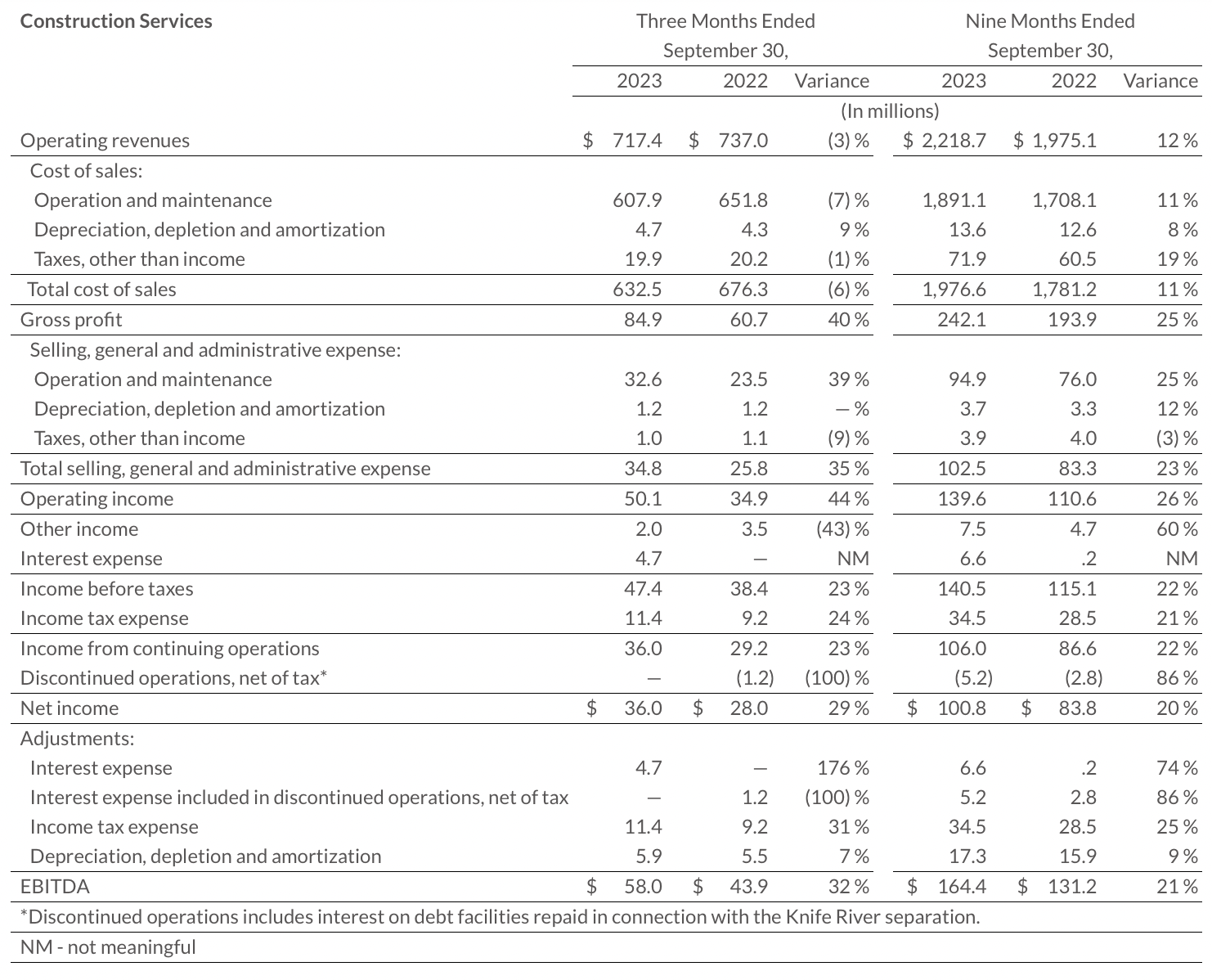

Let's take a look at the income statement from the company. It has made some slight improvements YoY, with the operating revenues now at $279 million in total, up from $263 million in Q3 FY2022. A slightly noticeable trend has been the increase of maintenance expense YoY, now amounting to roughly $730 million, making up a little over 70% of the total operating expenses. This does put the company in a position where they can't necessarily take on too much debt to fuel growth, at least not right now when the interest rates are at the current levels. MDU already has $143 million in TTM interest expenses.

Income Statement (Earnings Report)

{kind=link}

Looking more specifically at the construction services that will be spun off it makes up a very large portion of the total operating revenues, roughly 70% in total in combination with the non-regulated pipelines as well. Gross profits for this segment are at 40% right now which in terms of other segments is quite similar to the industrials segment as well. I think that once the spinoff goes through investors will be eyeing how MDU can manage to raise margins. The 5-year average in terms of net margins is 4.89% for the company, and it sits a fair bit below that right now. If we can see a recovery to that I think the share price could rally. Nonetheless, the commitment that MDU has had to its shareholders these last several decades I think is enough to warrant the buy case. As far as growth goes I think MDU looks very positively on its own future and I tend to agree. The last report had the management raise guidance and achieve something similar to the CAGR sales growth of 5.4% I think can realistically continue. After the spinoff, I would estimate that the depreciation expenses will decrease as it seems that segment of the business was quite demanding in that aspect. This should raise overall margins and the earnings of the business I think, leading to EPS growth.

Risks

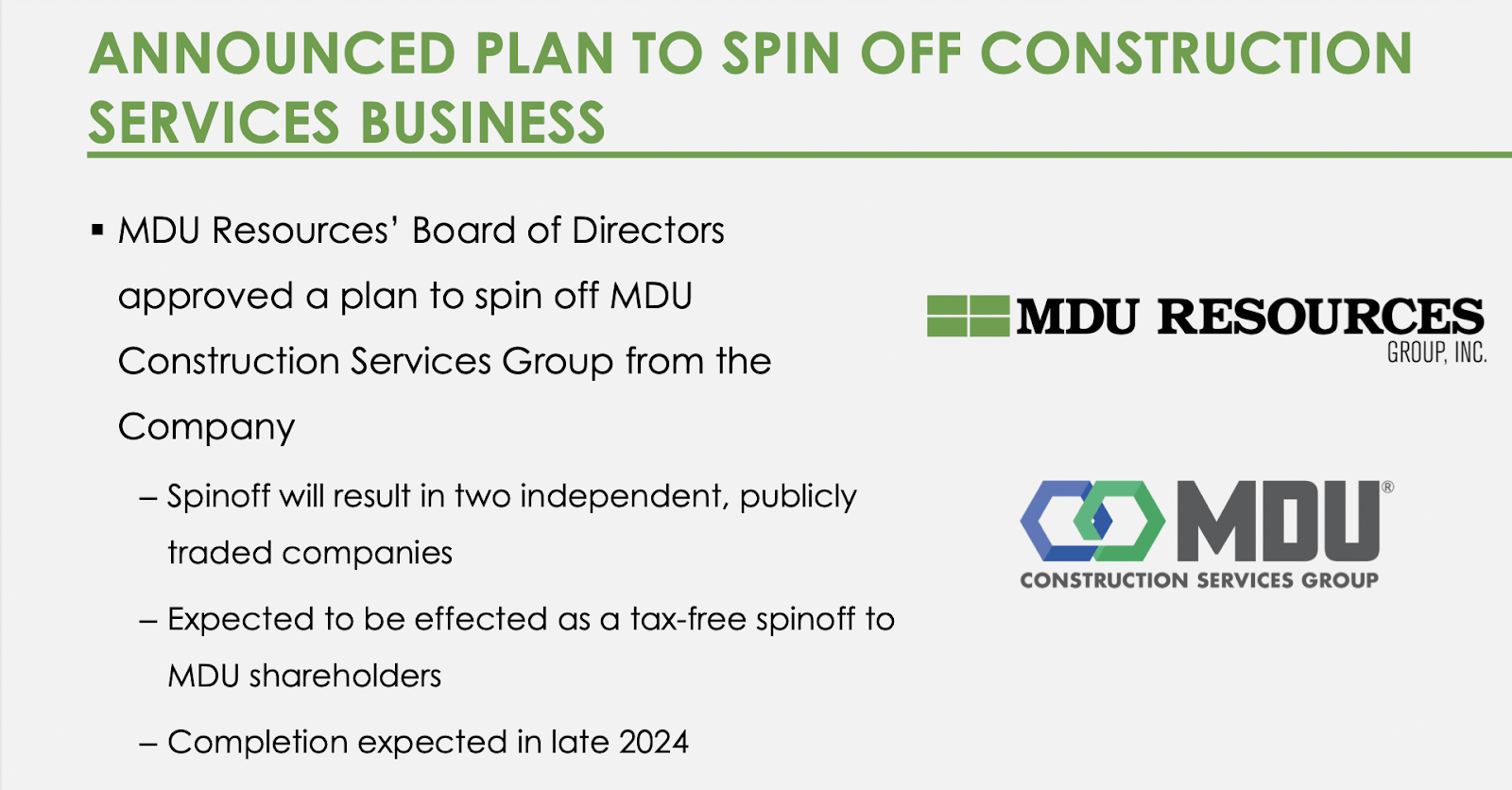

In a strategic move, MDU is embarking on a spinoff of one of its business units, aiming to refine its operational model to achieve enhanced efficiency and potentially drive higher profit margins. This initiative reflects the company's commitment to adapt to evolving market dynamics and unlock additional value for its stakeholders.

Spin Off Plans (Investor Presentation)

{kind=link}

However, the success of such spinoff endeavors is contingent on the new entity's ability to deliver stronger margins and improved growth prospects. If the results fall short of expectations, it could impact MDU's overall valuation, potentially justifying a lower standing in comparison to its sector peers. I think a P/E closer to around 12 - 13 might be justified, leaving a nearly 15% potential drop from today's levels. This P/E range is only applicable I think if the spin-off is not successful and MDUs see falling earnings and margins to something I am basing the company on right now, but I range rather I will be looking out for.

Final Words

MDU is a strong dividend payer that I think can provide investors with a lot of value over the next several decades. The spinoff of the construction services will lead to more flexibility and investment opportunities for MDU and a key driver for continued sales growth. The share price sits at a discount to the rest of the sector and this together with the shareholder commitment warrants a buy now.

For further details see:

MDU Resources Group: Spinoff Could Lead To Positive Margin Improvements